|

시장보고서

상품코드

1741022

카셰어링 텔레매틱스 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Car Sharing Telematics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

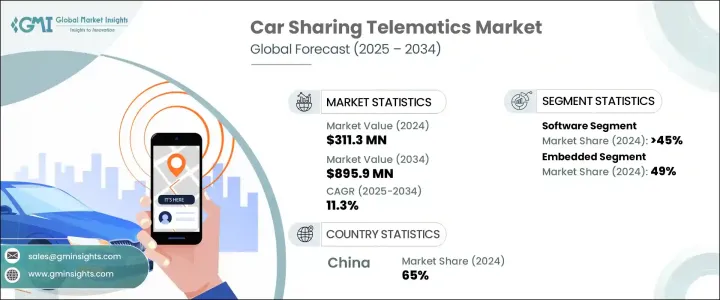

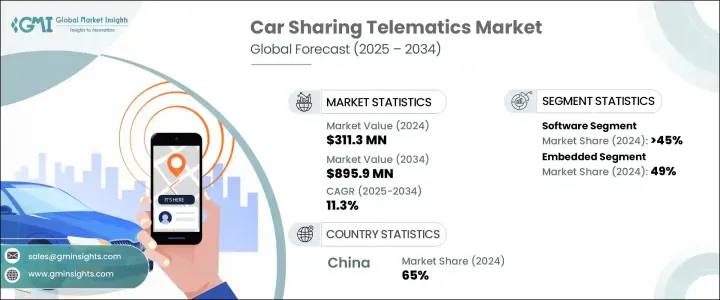

세계의 카셰어링 텔레매틱스 시장 규모는 2024년 3억 1,130만 달러였고, CAGR 11.3%로 성장하여 2034년까지 8억 9,590만 달러에 달할 것으로 예측되고 있습니다. 시장은 모빌리티 랜드스케이프의 재구축을 목표로 하는 혁신적인 전략으로 이 분야에 진입하는 기업 증가에 따라 기세가 늘어나고 있습니다. 도시 주민은 도로를 달리는 차량의 수를 줄일 뿐만 아니라 이산화탄소 배출량의 삭감과 교통 흐름의 완화에 공헌하는 지속 가능한 대체 교통 수단에 대한 인식을 깊게 하고 있습니다. 이를 통해 이러한 변화를 촉진하고 쉐어 모빌리티 사업자에게 전기자동차의 도입을 촉구하고 있습니다.

디지털화되고 친환경적인 운송 추진은 텔레매틱스 시스템의 설계와 도입 방법에 큰 영향을 미치고 있습니다. 2024년에는 소프트웨어 분야가 전체 시장 점유율의 45% 이상을 차지했으며, 예측 기간 동안 상당한 성장이 예상됩니다. 텔레매틱스 소프트웨어에 인공지능이 채용됨으로써 시스템은 실시간 수요에 따라 차량 크기를 동적으로 조정할 수 있게 되어 운영비용 절감과 서비스 품질 향상이 가능해졌습니다. 동시에 업그레이드된 암호화 프로토콜과 클라우드 기반 인프라를 통해 데이터 보호 및 사이버 보안이 보장되며 플랫폼은 더욱 견고하며 규제 표준을 준수합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 3억 1,130만 달러 |

| 예측 금액 | 8억 9,590만 달러 |

| CAGR | 11.3% |

시장을 구성 요소별로 분류하면 GPS 수신기, 가속도계, 엔진 인터페이스 모듈, SIM 카드 및 소프트웨어가 포함됩니다. 클라우드 네트워크와 통합함으로써, 소프트웨어 모듈은 사용자 인증, 지오펜싱, 예측 진단 등의 고급 기능도 가능하게 하고, 안전성을 확보하고, 차량의 가동률을 극대화합니다.

시장은 또한 형태별로 임베디드형, 테더링형, 통합형 텔레매틱스로 구분됩니다. 임베디드 시스템의 통합 수준은 차량과 백엔드 시스템 간의 즉각적인 데이터 전송을 가능하게 하고, 실시간 성능 통찰과 원격 제어 기능을 촉진합니다.

비즈니스 모델의 관점에서 볼 때 구독 기반 모델이 주요 부문으로 선정됩니다. 도시부의 사용자가 이 모델을 선호하는 것은, 예측 가능한 월정액 또는 연간 요금으로 차량 플리트에 대한 일관적인 액세스를 제공하기 때문입니다. 이 어프로치는 투명하고 예산에 맞는 가격 설정을 제공하고 자동차 소유의 번거로움을 해소함으로써 장기적인 사용자 참여를 지원합니다.

지역별로는 아시아태평양이 2024년 시장을 선도했고 중국이 지역시장 점유율의 약 65%를 차지하며 7,420만 달러의 매출을 계상했습니다. 스마트 모빌리티와 차량 전기화 촉진을 목적으로 한 국가 개발 정책으로 인해, 공유 전기자동차와 하이브리드 차량에 대한 텔레매틱스 시스템의 광범위한 배포가 가능해졌으며, 5G 네트워크, 클라우드 컴퓨팅, 사물인터넷(IoT) 플랫폼에 대한 투자가 첨단 카셰어링 에코시스템의 확대를 지원하고 있습니다.

세계의 카셰어링 텔레매틱스 산업을 형성하는 주요 기업은 실시간 추적, 행동 분석, 예지 보전 기술공급자를 포함합니다. 시장의 진화는 도시의 라이프스타일과 지속가능성 목표에 부합하는 보다 스마트하고 안전하며 효율적인 운송 솔루션에 대한 요구를 지속적으로 견인하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 카셰어링 텔레매틱스의 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 부품 공급업자

- 자동차 제조업체

- 테크놀로지 프로바이더

- 시스템 통합자

- 최종 용도

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(고객에 대한 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 이익률 분석

- 기술과 혁신의 상황

- 특허 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 운송 업계에서 IoT와 AI의 통합

- 지속 가능한 수송 수단에 대한 수요 증가

- 공유 모빌리티를 촉진하는 지원적인 규제와 정부의 대처

- 업계의 잠재적 리스크 및 과제

- 데이터 프라이버시에 대한 우려

- 다액의 초기 비용과 계속 비용

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 서비스별, 2021-2034년

- 주요 동향

- 자동 충돌 알림(ACN)

- 긴급시 대응

- 네비게이션

- 어시스턴스 액세스

- 진단

- 차량 관리

- 청구

- 기타

제6장 시장 추계 및 예측 : 형태별, 2021-2034년

- 주요 동향

- 임베디드형

- 테더링형

- 통합형

제7장 시장 추계 및 예측 : 컴포넌트별, 2021-2034년

- 주요 동향

- GPS 수신기

- 가속도계

- 엔진 인터페이스

- SIM 카드

- 소프트웨어

- 기타

제8장 시장 추계 및 예측 : 비즈니스 모델별, 2021-2034년

- 주요 동향

- 구독 모델

- 종량 과금 모델

- 기업 차량 관리

- OEM 파트너십

- 기타

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- CalAmp

- cambio Mobilitatsservice

- Cantamen

- Carmine

- Citiz Reseau

- CityBee Solutions

- Continental Aftermarket & Services

- Fleetster(Next Generation Mobility)

- Geotab

- INVERS

- Mobility Tech Green

- Mojio

- Octo Group

- Ridecell

- Samsara

- Targa Telematics

- Turo

- Verizon Communications

- Vulog

- WeGo

The Global Car Sharing Telematics Market was valued at USD 311.3 million in 2024 and is estimated to grow at a CAGR of 11.3% to reach USD 895.9 million by 2034. The market is gaining momentum due to the increasing number of companies entering the sector with innovative strategies aimed at reshaping the mobility landscape. Rising concerns over environmental degradation and traffic congestion are fueling the shift from traditional car ownership to shared vehicle models. Urban populations are becoming more aware of sustainable transportation alternatives that not only reduce the number of vehicles on the road but also contribute to lowering carbon emissions and easing traffic flow. Municipal governments are encouraging these changes by implementing green transportation policies and emission-reduction targets, pushing shared mobility operators to adopt electric vehicles in their fleets. This transition aligns with broader smart city initiatives that aim to optimize urban infrastructure and reduce environmental impact.

The push for digitized and eco-conscious transportation has significantly influenced how telematics systems are designed and deployed. As car sharing becomes more mainstream, telematics software is emerging as the most crucial component, transforming vehicles into connected data hubs. In 2024, the software segment held more than 45% of the total market share, and it is expected to witness substantial growth during the forecast period. These platforms allow operators to track vehicle performance, monitor maintenance schedules, analyze user behavior, and improve overall fleet efficiency. The adoption of artificial intelligence in telematics software now enables systems to adjust fleet sizes dynamically based on real-time demand, reducing operational costs and boosting service quality. Features such as keyless vehicle entry, remote locking, billing automation, and user-friendly interfaces all stem from advanced software capabilities. At the same time, upgraded encryption protocols and cloud-based infrastructure ensure data protection and cybersecurity, making the platforms more robust and compliant with regulatory standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $311.3 Million |

| Forecast Value | $895.9 Million |

| CAGR | 11.3% |

When segmented by component, the market includes GPS receivers, accelerometers, engine interface modules, SIM cards, and software. These components work together to offer seamless connectivity and precise analytics. Software continues to lead in importance, offering real-time visibility and operational control for fleet managers. By integrating with cloud networks, software modules also enable advanced functions like user authentication, geo-fencing, and predictive diagnostics, which ensure safety and maximize fleet availability.

The market is also segmented by form into embedded, tethered, and integrated telematics. Embedded systems accounted for 49% of the market share in 2024 and are expected to dominate over the forecast timeline. These systems are installed by manufacturers directly into the vehicle and are integrated deeply into its electronics. The level of integration in embedded systems allows instant data transfer between the vehicle and backend systems, facilitating real-time performance insights and remote control capabilities. With increasing vehicle connectivity demands, embedded systems are becoming the industry standard for car sharing programs.

From a business model perspective, the subscription-based model stands out as the leading segment. Urban users gravitate toward this model because it offers consistent access to vehicle fleets at predictable monthly or annual rates. This approach supports long-term user engagement by providing transparent, budget-friendly pricing and eliminating the hassles of car ownership. Businesses operating under this model enjoy higher customer retention rates due to the dependable nature of the service.

Regionally, Asia Pacific led the market in 2024, with China holding around 65% of the regional market share and generating USD 74.2 million in revenue. China's leadership position is driven by its rapid urbanization, extensive car production capabilities, and technological advancements in connected vehicle infrastructure. National development policies aimed at promoting smart mobility and vehicle electrification have enabled widespread deployment of telematics systems across shared electric and hybrid vehicles. Additionally, investments in 5G networks, cloud computing, and Internet of Things (IoT) platforms support the expansion of sophisticated car sharing ecosystems. Battery management systems, AI-based vehicle tracking, and real-time fleet analytics are being integrated into shared mobility services, making the country a global leader in this sector.

The major players shaping the global car sharing telematics industry include providers of real-time tracking, behavior analysis, and predictive maintenance technologies. These systems now feature advanced sensor arrays, centralized control units, and 5G-enabled eSIMs that offer cross-border data exchange and cloud-based diagnostics. The market's evolution continues to be driven by a need for smarter, safer, and more efficient transportation solutions tailored to urban lifestyles and sustainability goals.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Car Sharing Telematics Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component providers

- 3.2.2 Automotive manufacturers

- 3.2.3 Technology provider

- 3.2.4 System integrators

- 3.2.5 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news and initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Integration of IOT and AI in transportation industry

- 3.9.1.2 Rising demand for sustainable transportation

- 3.9.1.3 Supportive regulations and government initiatives promoting shared mobility

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Concerns about data privacy

- 3.9.2.2 Significant upfront and ongoing costs

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Service, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Automatic Crash Notification (ACN)

- 5.3 Emergency

- 5.4 Navigation

- 5.5 Assistance & access

- 5.6 Diagnostics

- 5.7 Fleet management

- 5.8 Billing

- 5.9 Others

Chapter 6 Market Estimates & Forecast, By Form, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Embedded

- 6.3 Tethered

- 6.4 Integrated

Chapter 7 Market Estimates & Forecast, By Component, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 GPS receiver

- 7.3 Accelerometer

- 7.4 Engine interface

- 7.5 Sim card

- 7.6 Software

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Business Model, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Subscription-based model

- 8.3 Pay-per-use model

- 8.4 Corporate fleet management

- 8.5 Partnerships with OEMs

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 U.K.

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 CalAmp

- 10.2 cambio Mobilitatsservice

- 10.3 Cantamen

- 10.4 Carmine

- 10.5 Citiz Reseau

- 10.6 CityBee Solutions

- 10.7 Continental Aftermarket & Services

- 10.8 Fleetster (Next Generation Mobility)

- 10.9 Geotab

- 10.10 INVERS

- 10.11 Mobility Tech Green

- 10.12 Mojio

- 10.13 Octo Group

- 10.14 Ridecell

- 10.15 Samsara

- 10.16 Targa Telematics

- 10.17 Turo

- 10.18 Verizon Communications

- 10.19 Vulog

- 10.20 WeGo