|

시장보고서

상품코드

1741041

CNG 및 LPG 자동차 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)CNG and LPG Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

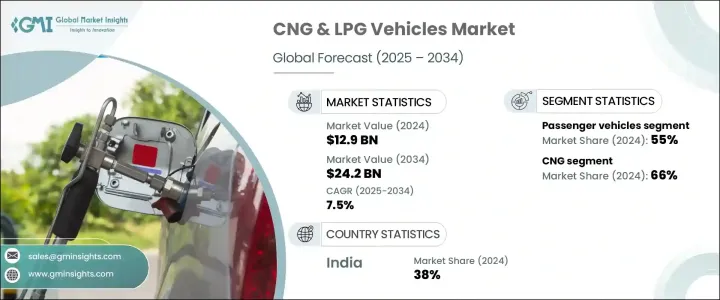

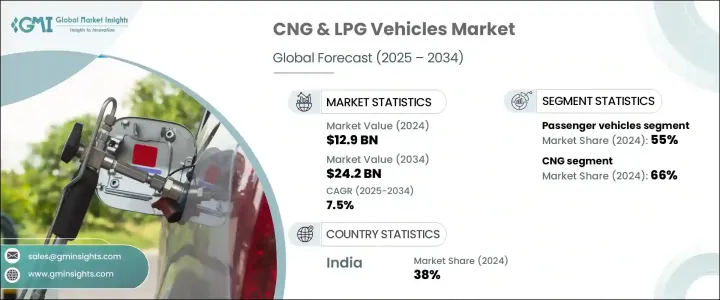

세계의 CNG 및 LPG 자동차 시장 규모는 2024년 129억 달러로 평가되었고, CAGR 7.5%로 성장할 전망이며, 2034년 242억 달러에 이를 것으로 추정됩니다.

기후 변화와 대기환경의 악화에 대한 사회적 의식이 높아짐에 따라 정부와 소비자 모두를 친환경 모빌리티 솔루션으로 밀어 올리고 있습니다. 에너지 안보가 세계적으로 주목받는 가운데 기존 가솔린차나 디젤차를 대체할 실용적인 선택지로 대폭적인 비용 절감과 저탄소 배출을 실현하는 CNG 및 LPG 자동차가 대두되고 있습니다. 세계 각국은 적극적인 배기가스 규제를 도입해 연비 기준을 강화하고 대체연료 도입을 장려하고 있으며, CNG 및 LPG 자동차는 갈수록 매력적인 선택지가 되고 있습니다. CNG 엔진의 기술적 진보는 유해한 오염물질을 대폭 줄이면서 차량 성능을 더욱 향상시켜 시장을 미래의 강력한 성장을 위해 자리매김하고 있습니다. 클린 에너지 인프라, 개조 솔루션, 급유 네트워크의 확대에 대한 투자는, 장기적인 보급을 지지하는 에코 시스템을 구축하고 있습니다. 게다가 연료 가격의 급등락으로 플리트 사업자나 개인 소비자는 보다 경제적이고 지속 가능한 선택지를 모색하게 되었고, CNG 및 LPG 자동차는 미래 모빌리티 동향의 최전선에 위치하고 있습니다.

CNG 및 LPG 자동차는 각국이 환경에 대한 책임과 경제적 실현가능성을 균형잡힌 대체교통 수단을 추진하는 가운데 세계 지속가능성 이니셔티브의 중요한 기업이 되고 있습니다. 각국 정부는 보다 청정한 연료의 채용을 촉진하기 위해 보다 엄격한 배출규제를 실시하고, 세금 환불 및 보조금 등 매력적인 인센티브를 제공함으로써 대담한 조치를 취하고 있습니다. 일부 주요 시장에서 차량 운행 회사는 장기 운행 비용의 이점을 실현하기 위해 디젤에서 CNG로의 전환을 추진하고 있습니다. 합리적인 가격의 리모델링 키트를 사용할 수 있으며 비용 효율적인 솔루션을 선호하는 대중 교통의 존재감이 높아짐에 따라 비용에 민감한 소비자들 사이에서 CNG 및 LPG 차량을 채택하는 경향이 커지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 129억 달러 |

| 예측 금액 | 242억 달러 |

| CAGR | 7.5% |

승용차 부문은 2024년에 55%의 점유율을 차지하고 시장을 석권했습니다. 구매자는 저렴한 가격과 환경 성능을 우선시하기 때문에 2034년까지 CAGR 7%로 성장할 것으로 예측됩니다. 상용차 분야에서는, CNG를 연료로 하는 트럭이나 배달용 밴의 대두가, 기존의 차량을 대신하는 깨끗하고 연료 효율이 높은 선택사항을 제공하는 것으로, 도시 지역의 물류를 재구축하고 있습니다. 특히 도시 환경에서 상용차는 운행 효율과 지원적인 정책 틀의 혜택을 받고 있습니다. 밀집한 대도시권에서는 CNG 및 LPG로 달리는 삼륜차가 빠르게 보급되고 있어 단거리 수송에 실용적이고 저렴한 솔루션을 제공하고 있습니다.

압축천연가스(CNG) 부문은 2024년 세계 시장 세분화에서 66%의 압도적 점유율을 차지했습니다. CNG의 리더십은 저렴한 가격, 배출가스 감축, 갈수록 엄격해지는 환경규제에 대한 대응이라는 점에서 CNG가 제공하는 뚜렷한 장점에 기인하고 있습니다. CNG는 탄소발자국 감소와 비용 절감으로 상용차와 개인 소비자 모두에게 바람직한 선택지로 계속 대두되고 있습니다.

인도의 CNG 및 LPG 자동차 시장은 2024년 24억 달러를 창출했으며, 세계 시장의 38% 점유율을 차지했습니다. 급속한 도시화, 재래식 연료 가격의 인플레이션 압력, 대체 연료를 지지하는 강력한 공공 정책이 이러한 성장을 뒷받침하고 있습니다. 주요 도시에서는 보다 깨끗한 대중교통으로의 전환이 꾸준히 진행되고 있으며, CNG 버스 및 택시가 그 선두를 달리고 있습니다. 내연 엔진 차량에 CNG 키트를 장착함으로써 도시 경관의 이행이 더욱 가속화되고 있습니다.

Toyota, Hyundai Motor Company, Mahindra and Mahindra, Tata Motors, Ford Motor Company, General Motors, Volkswagen Group, IVECO, MAN SE 및 Honda 등 주요 기업들은 제품 혁신에 많은 투자를 하고, CNG 및 LPG 자동차 포트폴리오를 확대하며, 판매망을 강화하고 있습니다. 특히 신흥 시장에서는 연료 공급 회사와 협력하여 연료 보급 인프라를 개선 하고 있는 곳이 많습니다. 하이브리드 CNG 기술, 스마트 차량 통합, 플릿 파트너십 모델등의 전략은 각사가 진화하는 CNG 및 LPG 자동차 시장에서의 발판을 굳히는데 도움이 되고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 연료 공급업체

- 부품 제조업체

- 자동차 제조업체(OEM)

- 개조업자와 애프터마켓 공급자

- 유통 및 소매 인프라

- 이익률 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 업계에 미치는 영향

- 기술 및 혁신의 상황

- 특허 분석

- 주요 뉴스 및 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- CNG 기술의 급속한 진보

- 지속 가능한 이동성에 중점화

- 비용 효율적인 운송 수단에 대한 요구 증가

- 가솔린 차량보다 낮은 유지 보수 비용

- 업계의 잠재적 위험 및 과제

- 높은 초기 비용

- 가솔린차에 비해 낮은 성능

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

5.3 삼륜차

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제6장 시장 추계 및 예측 : 연료별(2021-2034년)

- 주요 동향

- LPG

- CNG

제7장 시장 추계 및 예측 : 엔진 시스템별(2021-2034년)

- 주요 동향

- 전용 시스템

- 바이퓨엘

- 듀얼 연료

제8장 시장 추계 및 예측 : 피팅별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- Ashok Leyland

- Bajaj Auto

- Ford Motor Company

- General Motors

- Honda

- Hyundai Motor Company

- Isuzu Motors

- IVECO

- Kia Motors

- Landi Renzo

- Mahindra &Mahindra

- MAN SE

- Maruti Suzuki

- Renault

- SEAT

- Skoda Auto

- Tata Motors

- Toyota

- Volkswagen Group

- Westport Fuel Systems

The Global CNG and LPG Vehicles Market was valued at USD 12.9 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 24.2 billion by 2034, driven by the surging demand for environmentally friendly and fuel-efficient vehicles. Growing public awareness about climate change and deteriorating air quality has pushed both governments and consumers toward greener mobility solutions. As energy security gains prominence worldwide, CNG and LPG vehicles are emerging as practical alternatives to traditional gasoline and diesel vehicles, offering substantial cost savings and lower carbon emissions. Countries around the world are rolling out aggressive emission norms, tightening fuel economy standards, and incentivizing alternative fuel adoption, making CNG and LPG vehicles an increasingly attractive choice. Technological advancements in CNG engines are further elevating vehicle performance while significantly cutting down harmful pollutants, positioning the market for strong future growth. Investment in clean energy infrastructure, retrofitting solutions, and the expansion of refueling networks is creating an ecosystem that supports long-term adoption. Moreover, rising fuel price volatility is pushing fleet operators and individual consumers to explore more economical and sustainable options, putting CNG and LPG vehicles at the forefront of future mobility trends.

CNG and LPG vehicles are becoming vital players in global sustainability initiatives as nations push for transportation alternatives that balance environmental responsibility with economic feasibility. Governments are taking bold steps by implementing stricter emission norms and offering attractive incentives, including tax rebates and grants, to drive the adoption of cleaner fuels. In several key markets, fleet operators are increasingly transitioning from diesel to CNG to realize long-term operational cost benefits. The availability of affordable retrofitting kits, combined with the growing presence of public transportation systems that favor cost-effective solutions, is reinforcing the trend toward CNG and LPG vehicle adoption among cost-sensitive consumers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.9 Billion |

| Forecast Value | $24.2 Billion |

| CAGR | 7.5% |

The passenger vehicles segment dominated the market with a 55% share in 2024 and is projected to grow at a CAGR of 7% through 2034, as buyers prioritize affordability and environmental performance. On the commercial side, the rise of CNG-powered trucks and delivery vans is reshaping urban logistics by offering clean, fuel-efficient alternatives to traditional fleets. Commercial vehicles, particularly in urban environments, are benefiting from operational efficiencies and supportive policy frameworks. In dense metropolitan areas, three-wheelers running on CNG and LPG are gaining rapid traction, offering a practical and affordable solution for short-distance transportation.

The compressed natural gas (CNG) segment held a commanding 66% share of the global CNG and LPG vehicles market in 2024. Its leadership stems from the clear benefits it offers in terms of affordability, reduced emissions, and compliance with increasingly stringent environmental regulations. CNG continues to emerge as a preferred choice for both commercial fleets and individual consumers, thanks to its reduced carbon footprint and cost savings.

India's CNG and LPG Vehicles Market generated USD 2.4 billion in 2024, capturing a 38% share of the global market. Rapid urbanization, inflationary pressures on conventional fuel prices, and robust public policies favoring alternative fuels are driving this growth. Major cities are witnessing a steady shift toward cleaner public transportation options, with CNG buses and taxis leading the way. Retrofitting of internal combustion engine vehicles with CNG kits is further accelerating this transition across urban landscapes.

Leading automakers like Toyota, Hyundai Motor Company, Mahindra and Mahindra, Tata Motors, Ford Motor Company, General Motors, Volkswagen Group, IVECO, MAN SE, and Honda are heavily investing in product innovations, expanding their CNG and LPG vehicle portfolios, and strengthening their distribution networks. Many are collaborating with fuel providers to improve refueling infrastructure, especially in emerging markets. Strategies such as hybridized CNG technologies, smart vehicle integrations, and fleet partnership models are helping companies solidify their foothold in the evolving CNG and LPG vehicles market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Fuel providers

- 3.2.2 Component manufacturers

- 3.2.3 Vehicle manufacturers (OEMs)

- 3.2.4 Retrofitters and aftermarket suppliers

- 3.2.5 Distribution and retail infrastructure

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on the industry

- 3.4.1.1 Supply-side impact (raw materials)

- 3.4.1.1.1 Price volatility in key materials

- 3.4.1.1.2 Supply chain restructuring

- 3.4.1.1.3 Production cost implications

- 3.4.1.2 Demand-side impact (selling price)

- 3.4.1.2.1 Price transmission to end markets

- 3.4.1.2.2 Market share dynamics

- 3.4.1.1 Supply-side impact (raw materials)

- 3.4.2 Key companies impacted

- 3.4.1 Impact on the industry

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rapid advancements in CNG technology

- 3.9.1.2 Increasing emphasis on sustainable mobility

- 3.9.1.3 Rising need for cost-effective transportation

- 3.9.1.4 Lower maintenance cost than petrol-powered vehicles

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Higher upfront costs

- 3.9.2.2 Reduced performance compared to petrol-powered vehicles

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUV

5.3 Three-wheelers

- 5.4 Commercial vehicles

- 5.4.1 Light Commercial Vehicles (LCV)

- 5.4.2 Medium Commercial Vehicles (MCV)

- 5.4.3 Heavy Commercial Vehicles (HCV)

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 LPG

- 6.3 CNG

Chapter 7 Market Estimates & Forecast, By Engine System, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Dedicated system

- 7.3 Bi-fuel

- 7.4 Dual fuel

Chapter 8 Market Estimates & Forecast, By Fitting, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Ashok Leyland

- 10.2 Bajaj Auto

- 10.3 Ford Motor Company

- 10.4 General Motors

- 10.5 Honda

- 10.6 Hyundai Motor Company

- 10.7 Isuzu Motors

- 10.8 IVECO

- 10.9 Kia Motors

- 10.10 Landi Renzo

- 10.11 Mahindra & Mahindra

- 10.12 MAN SE

- 10.13 Maruti Suzuki

- 10.14 Renault

- 10.15 SEAT

- 10.16 Skoda Auto

- 10.17 Tata Motors

- 10.18 Toyota

- 10.19 Volkswagen Group

- 10.20 Westport Fuel Systems