|

시장보고서

상품코드

1750267

진공 트럭 시장 : 기회, 성장 촉진요인, 산업 동향 분석 예측(2025-2034년)Vacuum Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

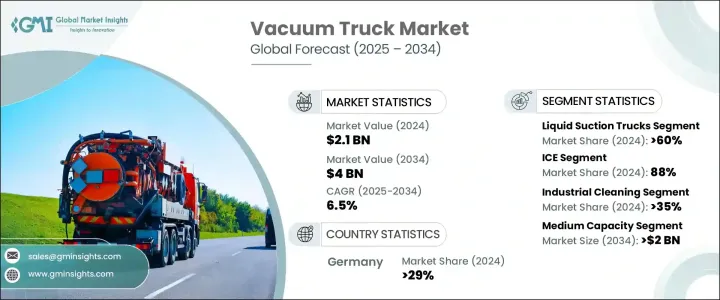

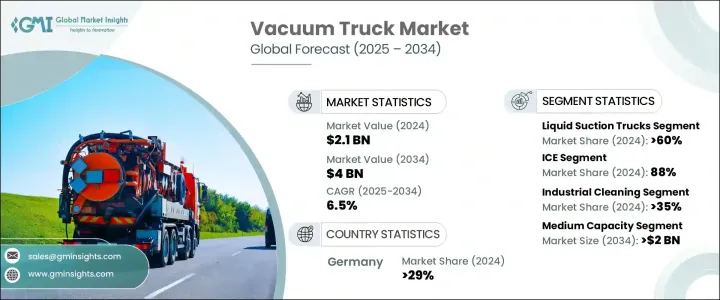

세계의 진공 트럭 시장은 2024년 21억 달러였고, 특히 신흥경제 국가에서의 도시화의 진전과 급속한 산업개척에 견인되어 CAGR 6.5%로 성장해 2034년까지 40억 달러에 달할 것으로 예측되고 있습니다.

이러한 차량은 고체 및 액체 폐기물 처리, 하수도 유지 관리 및 광범위한 산업 청소 작업에 필수적입니다. 도시가 성장하고 인프라가 확대됨에 따라 효율적인 폐기물 제거 및 위생 관리를 위해 진공 트럭을 이용하는 공공 단체와 민간 기업이 증가하고 있습니다. 광업, 건설, 에너지 등의 산업 부문도 유출물, 슬러지, 위험물 관리에 진공 트럭을 이용하여 현대의 폐기물 관리 생태계에서 진공 트럭의 중요성을 높이고 있습니다.

세계적으로 도입된 보다 엄격한 환경 규제로 인해 시정촌과 산업계는 오염 방지 요건을 충족시키기 위해 진공 트럭을 채택하게 되었습니다. 이러한 차량은 환경을 오염시키지 않고 위험물과 비위험물을 안전하게 운송하는 방법을 제공합니다. 화학제품, 유틸리티, 석유 등 섹터 전체의 안전 컴플라이언스를 확보하는데 있어서, 진공 트럭의 역할은 계속 주목받고 있습니다. 환경기준이 진화함에 따라 보다 우수한 성능, 배출가스 절감, 안전성 강화를 제공하는 기술적으로 진보된 진공 트럭에 대한 관심이 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 21억 달러 |

| 예측 금액 | 40억 달러 |

| CAGR | 6.5% |

액체 흡입 트럭 분야는 2024년 60%의 점유율을 차지했으며, 2034년에는 20억 달러에 이를 것으로 예측되고 있습니다. 이러한 스마트한 기능 강화는 더 좋은 경로 최적화를 가능하게 하고, 계획되지 않은 다운타임을 줄이고, 예측 유지보수 전략을 지원하며, 함대 운영을 보다 비용 효율적이고 신뢰할 수 있도록 합니다.

연료유형에 관해서는 내연엔진(ICE) 진공 트럭이 2024년 시장을 88%의 점유율로 차지했습니다. 탄소 배출량이 적고 규제상의 메리트가 있기 때문에 기존 디젤의 대체 연료로서 인기가 나오고 있습니다.

유럽의 진공 트랙 시장은 2024년에 29%의 점유율을 차지했습니다. 이 지역의 엄격한 환경 규제가 효율적인 폐기물 처리와 오염 방지 기술을 필수로 하고, 진공 트럭을 유틸리티, 건설, 산업 청소에 필수적인 것으로 자리잡고 있는 것이 그 요인입니다. 이러한 차량은 하수도 시스템의 유지 관리, 유해 폐기물 처리, 인프라 개발 프로젝트의 갈라짐 관리에 널리 사용됩니다. 유럽 전역에서의 도시화의 지속과 그린 인프라 투자는 기술적으로 진보된 저배출 진공 트럭에 대한 요구 증가를 더욱 뒷받침하고 있습니다. 지속가능성과 지방자치단체의 청결이 중요해지게 되고, 이 지역의 관민 양부문에서 수요는 견조하게 추이할 것으로 예측됩니다.

시장 포지셔닝을 유지하고 강화하기 위해 주요 기업은 기술 혁신과 지속가능성에 투자하고 있습니다. Amphitec BV, Federal Signal, GapVax, Dongzheng Special Purpose Vehicle, DISAB Vacuum Technology, Alamo Group, Fulongma Group, Cappellotto, Baker Hughes, Super Products 등 기업들은 보다 깨끗한 연료 시스템을 통합하여 진공 기술을 발전시키고, 진공 기술을 진보하고 있습니다. 또한 장기 계약과 신뢰할 수 있는 서비스 파이프라인을 확보하기 위해 지자체 및 산업 사업자와의 전략적 파트너십 구축에도 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- OEM 제조업체

- 부품 공급자

- 섀시 및 엔진 프로바이더

- 렌탈 및 플릿 서비스 제공업체

- 시스템 인티그레이터 및 커스텀 패브리케이터

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 주요 원재료의 가격 변동

- 공급망 재구성

- 최종 시장에의 가격 전달

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 무역에 미치는 영향

- 이익률 분석

- 기술과 혁신의 상황

- 주요 뉴스와 대처

- 코스트 내역 분석

- 가격 분석

- 제품

- 지역

- 특허 분석

- 규제 상황

- 영향요인

- 성장 촉진요인

- 도시화의 진전과 도시 폐기물 관리의 요구의 고조

- 석유 및 가스와 광업 사업 확대

- 보다 엄격한 환경 및 안전 규제

- 기술의 진보와 자동화

- 업계의 잠재적 리스크 및 과제

- 고액의 자본 비용과 유지비

- 개발 도상 지역의 인프라 부족

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

- 주요 동향

- 액체 흡입 트럭

- 건식 흡입 트랙

- 콤비네이션 트랙

제6장 시장 추계 및 예측 : 연료별, 2021-2034년

- 주요 동향

- ICE

- 전기

제7장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 산업용 청소

- 발굴

- 지자체

- 일반 청소

- 기타

제8장 시장 추계 및 예측 : 용량별, 2021-2034년

- 주요 동향

- 소용량(5m3 미만)

- 중용량(5-10m3)

- 대용량(10m3 이상)

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- Alamo Group

- Amphitec BV

- Cappellotto

- DISAB Vacuum Technology

- Dongzheng Special Purpose Vehicle

- Federal Signal

- Fulongma Group

- GapVax

- Gradall Industries

- Guzzler Manufacturing

- Hi-Vac Corporation

- Kanematsu Engineering

- Keith Huber

- KOKS Group

- Ledwell & Son

- Rivard

- Sewer Equipment

- Super Products

- Vacall Industries

- Vac-Con

The Global Vacuum Truck Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 4 billion by 2034, driven by the rise in urbanization and rapid industrial development, especially across emerging economies. These vehicles are essential for handling solid and liquid waste, sewer maintenance, and cleaning operations across a wide range of industries. As cities grow and infrastructure expands, public and private entities are increasingly turning to vacuum trucks for efficient waste removal and sanitation. Industrial sectors such as mining, construction, and energy also rely on vacuum trucks to manage spills, sludge, and hazardous materials, reinforcing the vehicle's importance in modern waste management ecosystems.

Stricter environmental regulations introduced globally have prompted municipalities and industries to adopt vacuum trucks to meet pollution control requirements. These vehicles offer a secure method of transporting hazardous and non-hazardous materials without contaminating the environment. Their role in ensuring safety compliance across sectors like chemicals, utilities, and petroleum continues to gain prominence. As environmental standards evolve, there's growing interest in technologically advanced vacuum trucks that provide better performance, reduced emissions, and enhanced safety.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $4 Billion |

| CAGR | 6.5% |

The liquid suction truck segment held a 60% share in 2024 and is projected to reach USD 2 billion by 2034. This growth is largely fueled by the adoption of advanced technologies, including real-time data monitoring, IoT integration, and telematics. These smart enhancements enable better route optimization, reduce unplanned downtimes, and support predictive maintenance strategies, making fleet operations more cost-effective and reliable. Additionally, innovations in hydraulic components and vacuum pump systems have resulted in trucks that operate with higher suction power and reduced noise levels, which improves operational efficiency while aligning with stricter environmental mandates.

When it comes to fuel types, internal combustion engine (ICE) vacuum trucks dominated the market in 2024 with an 88% share. Despite this dominance, the shift toward sustainability is evident with increased interest in cleaner fuel alternatives. Renewable natural gas (RNG), often captured from agricultural or landfill methane, and liquefied natural gas (LNG) are emerging as popular substitutes to conventional diesel, offering lower carbon emissions and regulatory benefits. Hydrogen-powered ICEs are also gaining traction as an interim solution, bridging the gap between traditional diesel engines and fully electric or zero-emission vehicles.

Europe Vacuum Truck Market held 29% share in 2024, driven by the region's strict environmental regulations have made efficient waste handling and pollution control technologies mandatory, positioning vacuum trucks as essential for public utilities, construction, and industrial cleaning. These vehicles are widely utilized for maintaining sewer systems, handling hazardous waste, and managing debris from infrastructure development projects. Continued urbanization and investments in green infrastructure across Europe further support the rising need for technologically advanced, low-emission vacuum trucks. With a growing emphasis on sustainability and municipal cleanliness, demand is expected to stay strong across both public and private sectors in the region.

To maintain and strengthen market positioning, key companies are investing in innovation and sustainability. Players like Amphitec BV, Federal Signal, GapVax, Dongzheng Special Purpose Vehicle, DISAB Vacuum Technology, Alamo Group, Fulongma Group, Cappellotto, Baker Hughes, and Super Products are integrating cleaner fuel systems, advancing vacuum technologies, and expanding their geographic presence. They also focus on building strategic partnerships with municipalities and industrial operators to ensure long-term contracts and dependable service pipelines.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 OEM Manufacturers

- 3.2.2 Component Suppliers

- 3.2.3 Chassis & Engine Providers

- 3.2.4 Rental & Fleet Service Providers

- 3.2.5 System Integrators & Custom Fabricators

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on the Industry

- 3.3.2.1 Price volatility in key materials

- 3.3.2.2 Supply chain restructuring

- 3.3.2.3 Price transmission to end markets

- 3.3.3 Strategic industry responses

- 3.3.3.1 Supply chain reconfiguration

- 3.3.3.2 Pricing and product strategies

- 3.3.1 Impact on trade

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Key news & initiatives

- 3.7 Cost breakdown analysis

- 3.8 Pricing analysis

- 3.8.1 Product

- 3.8.2 Region

- 3.9 Patent analysis

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Increasing Urbanization and Municipal Waste Management Needs

- 3.11.1.2 Expansion in Oil & Gas and Mining Operations

- 3.11.1.3 Stricter Environmental and Safety Regulations

- 3.11.1.4 Technological Advancements and Automation

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High Capital and Maintenance Costs

- 3.11.2.2 Limited Infrastructure in Developing Regions

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Liquid suction trucks

- 5.3 Dry suction trucks

- 5.4 Combination trucks

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Industrial cleaning

- 7.3 Excavation

- 7.4 Municipal

- 7.5 General cleaning

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Small capacity (Up to 5 m³)

- 8.3 Medium capacity (5–10 m³)

- 8.4 Large capacity (Above 10 m³)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alamo Group

- 10.2 Amphitec BV

- 10.3 Cappellotto

- 10.4 DISAB Vacuum Technology

- 10.5 Dongzheng Special Purpose Vehicle

- 10.6 Federal Signal

- 10.7 Fulongma Group

- 10.8 GapVax

- 10.9 Gradall Industries

- 10.10 Guzzler Manufacturing

- 10.11 Hi-Vac Corporation

- 10.12 Kanematsu Engineering

- 10.13 Keith Huber

- 10.14 KOKS Group

- 10.15 Ledwell & Son

- 10.16 Rivard

- 10.17 Sewer Equipment

- 10.18 Super Products

- 10.19 Vacall Industries

- 10.20 Vac-Con