|

시장보고서

상품코드

1750317

수술용 가위 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Surgical Scissors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

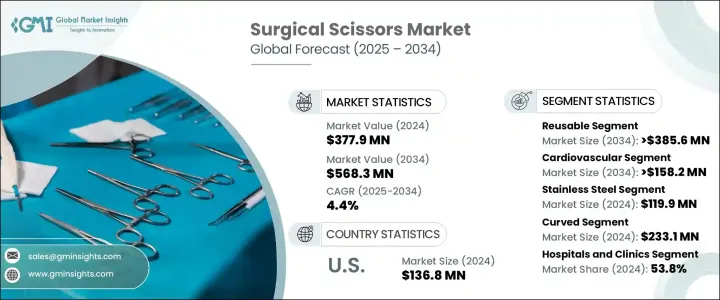

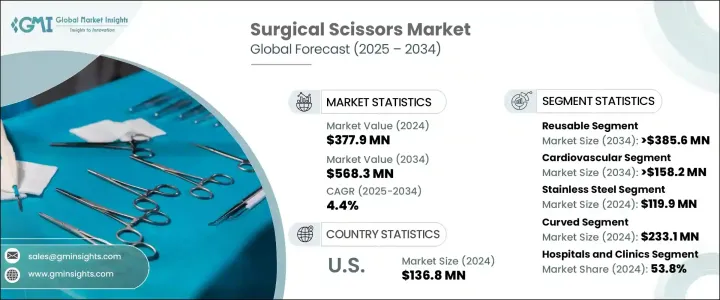

세계의 수술용 가위 시장은 2024년에는 3억 7,790만 달러로 평가되었고, 세계 인구의 고령화 및 만성 질환 환자 증가로 인한 수술 건수 증가를 배경으로 CAGR 4.4%로 성장할 전망이며, 2034년에는 5억 6,830만 달러에 이를 것으로 추정되고 있습니다.

헬스케어 시스템이 수요 증가에 대응함에 따라, 병원과 수술센터는 고도로 고정밀 수술 기구에 투자하게 됩니다. 저침습 수술의 혁신은 내구성이 뛰어나고 환자의 예후를 개선하도록 설계된 수술 기구의 필요성을 더욱 높이고 있습니다. 정밀도 및 안전성이 최우선 사항이 됨에 따라 효율적인 수술 수행을 지원하는 고품질 가위가 필수적입니다.

심혈관 장애, 암, 당뇨병 등의 만성 질환이 증가함에 따라 수술의 수는 증가하는 길을 따릅니다. 이러한 경향은 특히 고령자들 사이에서 현저하며, 신뢰성이 높고 효율적인 수술용 가위의 수요가 높아지고 있습니다. 많은 헬스케어 시설은 처치의 정확도를 높이고 수술 시간을 단축하기 위해 기술적으로 강화된 전동 공구에 투자하고 있습니다. 시장에서도 외과수술 인프라가 정비되고 있고, 선진적 툴의 조달이 진행되고 있기 때문에 마찬가지로 수요가 증가하고 있습니다. 다양한 종류 중에서도 재사용 가능한 가위는 장기적인 운영 비용을 절감하고 헬스케어의 지속 가능성 목표에 부합하기 때문에 강력한 지지를 받고 있습니다. 이 가위들은 텅스텐 카바이드나 고급 스테인리스 같은 재료로 만들어졌으며, 긴 수명, 날렵한 절삭력, 높은 성능을 제공합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 3억 7,790만 달러 |

| 예측 금액 | 5억 6,830만 달러 |

| CAGR | 4.4% |

수술용 가위 시장은 재사용형과 일회용형의 두 가지로 크게 나뉩니다. 재사용 가능한 가위 부문은 예측 CAGR 4.7%로 성장하여 2034년에는 3억 8,560만 달러에 이를 것으로 예측됩니다. 헬스케어 시설이 장기적인 비용 절감에 주력함에 따라, 재사용 가능한 기구로의 시프트가 진행되고 있습니다. 수술센터나 병원에서는 멸균하여 여러 번 재사용할 수 있는 가위의 채용이 증가하고 있어 일회용 대체품에 의한 폐기물을 최소화하고 있습니다. 게다가 재사용 가능한 가위는 스테인리스나 텅스텐 카바이드와 같은 고품질의 재료로 만들어져 있어 그 정확성과 내구성을 높이고 있습니다. 이러한 재료는 수술 중 봉합사의 신뢰성을 향상시키고 있습니다.

수술용 가위 시장의 심혈관 수술 부문은 CAGR 4.8%로 성장하여 2034년까지 1억 5,820만 달러에 달할 것으로 예측되고 있습니다. 심혈관 외과용 가위는 민감한 심장 조직에 손상을 최소화하고 더 나은 수술 결과를 보장하기 위해 특별히 예리한 칼날로 설계되었습니다. 이 가위의 선진적 기술에 의해, 이러한 복잡하고 선진적 처치에 불가결한 높은 정밀도가 실현되고 있습니다.

미국의 수술용 가위 2024년 시장 규모는 1억 3,680만 달러로, 강력한 헬스케어 시스템 및 많은 수술 건수, 수술 기구 기술의 끊임없는 혁신으로부터 혜택을 받고 있습니다. 미국은 계속해서 시장의 리더이며, 빈번한 신제품의 도입 및 진보에 의해, 다양한 부문에서 수술 기구의 가용성과 전문성을 향상시키고 있습니다. 그 결과, 미국 시장은 계속해서 고액의 투자를 유치해, 정밀하고 효율적인 수술을 위한 보다 고도의 전문적인 툴의 개발을 추진하고 있습니다.

경쟁을 보장하기 위해 Elixir Surgical, Surgicalholdings, INTEGRA, Storz, WPI, Teleflex, Aspen, HuFriedy, Stryker, KLS Martin, Medline, B. Braun, Millenium Surgical, BD, Scanlan 등의 기업은 연구 개발 및 정밀 제조에 많은 투자를 하고 있습니다. 이들 기업은 인체공학을 기반으로 한 특수 가위 설계, 제품 포트폴리오 확대, 세계 판매 파트너십 강화에 주력하여 세계적으로 증가하는 수술 수요에 부응하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- 산업에 미치는 영향요인

- 성장 촉진요인

- 수술용 가위 기술의 진보

- 만성질환 유병률 상승

- 저침습 수술 수요

- 외래 수술의 급증

- 산업의 잠재적 리스크 및 과제

- 짧은 제품 수명주기

- 재사용 가능한 기구에 의한 감염 위험에 대한 우려

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 국가별 대응

- 산업에 미치는 영향

- 공급측의 영향(제조 비용)

- 주요 원료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(소비자의 비용)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(제조 비용)

- 영향을 받는 주요 기업

- 전략적인 산업 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 시책관여

- 전망 및 향후 검토 사항

- 무역에 미치는 영향

- 가격 분석

- 기술

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 장래 시장 동향

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정 및 예측 : 가위 유형별(2021-2034년)

- 주요 동향

- 재사용형

- 일회용형

제6장 시장 추정 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 심혈관계

- 정형외과

- 소화기내과

- 신경학

- 기타

제7장 시장 추정 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 스테인리스

- 티타늄

- 텅스텐

- 세라믹

- 기타

제8장 시장 추정 및 예측 : 첨단 형태별(2021-2034년)

- 주요 동향

- 커브

- 스트레이트

- 기타 첨단 형태

제9장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원 및 클리닉

- 외래수술센터(ASC)

- 기타

제10장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Aspen

- B. Braun

- Becton, Dickinson and Company

- ELIXIR SURGICAL

- HuFriedy

- INTEGRA

- STORZ

- KLS Martin

- MEDLINE

- MILLENNIUM SURGICAL

- SCANLAN

- stryker

- Surgicalholdings

- Teleflex

- WPI

The Global Surgical Scissors Market was valued at USD 377.9 million in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 568.3 million by 2034, fueled by the growing number of surgeries driven by an aging global population and an uptick in chronic disease cases. As healthcare systems respond to rising demand, hospitals and surgical centers invest in advanced, high-precision surgical instruments. Innovations in minimally invasive procedures further push the need for surgical tools that are both durable and designed to support better patient outcomes. As precision and safety become top priorities, high-quality scissors have become essential in supporting efficient surgical performance.

With the rise in chronic diseases such as cardiovascular disorders, cancer, and diabetes, the number of surgical interventions continues to grow. This trend, especially among elderly populations, fuels demand for highly reliable and efficient surgical scissors. Many healthcare facilities invest in technologically enhanced power tools to improve procedural accuracy and reduce operation time. Emerging markets are seeing a similar rise in demand due to developing surgical infrastructure, which is pushing procurement of sophisticated tools. Among various types, reusable scissors are gaining strong traction because they reduce long-term operational costs and align with healthcare sustainability goals. These scissors are crafted from materials like tungsten carbide or premium stainless steel and offer enhanced longevity, sharper cuts, and higher performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $ 377.9 Million |

| Forecast Value | $568.3 Million |

| CAGR | 4.4% |

The market for surgical scissors is divided into two main types: reusable and disposable. The reusable scissors segment is expected to grow with a projected CAGR of 4.7%, reaching USD 385.6 million by 2034. As healthcare facilities focus on reducing long-term costs, they are shifting toward reusable instruments. Surgical centers and hospitals are increasingly adopting scissors that can be sterilized and reused multiple times, thus minimizing waste from disposable alternatives. Additionally, reusable scissors are made from high-quality materials like stainless steel or tungsten carbide, which enhances their precision and durability. These materials improve the reliability of sutures during surgeries.

The cardiovascular procedures segment of the surgical scissors market is projected to grow at a CAGR of 4.8% and reach USD 158.2 million by 2034, driven by the precise demands of heart surgeries, where small, accurate incisions are critical for patient survival. Cardiovascular surgical scissors are specially designed with exceptionally sharp blades to minimize damage to delicate heart tissues, ensuring better surgical outcomes. The advanced engineering of these scissors allows for a high level of precision, essential for such complex and high-stakes procedures.

U.S. Surgical Scissors Market generated USD 136.8 million in 2024, benefiting from a strong healthcare system, a high volume of surgeries, and continuous innovations in surgical tool technology. The U.S. remains a leader in the market, with frequent new product introductions and advancements that improve the availability and specialization of surgical instruments across various fields. As a result, the U.S. market continues to attract significant investment, driving the development of more sophisticated and specialized tools for precise and efficient surgeries.

To secure a competitive edge, companies like Elixir Surgical, Surgicalholdings, INTEGRA, Storz, WPI, Teleflex, Aspen, HuFriedy, Stryker, KLS Martin, Medline, B. Braun, Millennium Surgical, BD, and Scanlan are heavily investing in R&D and precision manufacturing. These firms focus on designing ergonomic, specialty scissors, expanding their product portfolios, and strengthening global distribution partnerships to meet increasing surgical demands worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Advancements in surgical scissors technology

- 3.2.1.2 Rising prevalence of chronic diseases

- 3.2.1.3 Demand for minimally invasive procedures

- 3.2.1.4 Surge in outpatient surgeries

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Short product lifecycle

- 3.2.2.2 Concerns over infection risks with reusable instruments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Pricing analysis

- 3.7 Technology landscape

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

- 3.11 Future market trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Scissors Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Reusable

- 5.3 Disposable

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiovascular

- 6.3 Orthopedic surgery

- 6.4 Gastroenterology

- 6.5 Neurology

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Materials, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Stainless steel

- 7.3 Titanium

- 7.4 Tungsten

- 7.5 Ceramic

- 7.6 Other materials

Chapter 8 Market Estimates and Forecast, By Tip Shapes, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Curved

- 8.3 Straight

- 8.4 Other tip shapes

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals & clinics

- 9.3 Ambulatory surgery centers

- 9.4 Other end users

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aspen

- 11.2 B. Braun

- 11.3 Becton, Dickinson and Company

- 11.4 ELIXIR SURGICAL

- 11.5 HuFriedy

- 11.6 INTEGRA

- 11.7 STORZ

- 11.8 KLS Martin

- 11.9 MEDLINE

- 11.10 MILLENNIUM SURGICAL

- 11.11 SCANLAN

- 11.12 stryker

- 11.13 Surgicalholdings

- 11.14 Teleflex

- 11.15 WPI