|

시장보고서

상품코드

1750353

폴리케톤(PK) 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Polyketone (PK) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

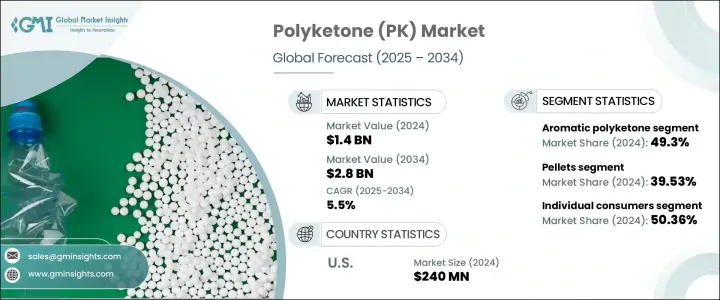

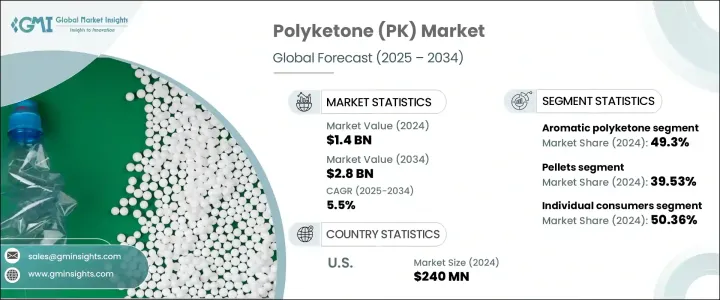

세계의 폴리케톤 시장은 2024년에 14억 달러로 평가되었고, 일부 산업에서 고성능 폴리머 수요가 증가하고 있기 때문에 CAGR 5.5%로 성장할 전망이며, 2034년에는 28억 달러에 이를 것으로 추정됩니다.

이 성장은 뛰어난 내약품성, 저흡습성, 향상된 마모 특성을 제공하는 고급 대체 재료의 탐색에 의해 크게 뒷받침되고 있습니다. 폴리케톤은 이러한 특성 때문에, 폴리아미드나 폴리옥시메틸렌이라고 하는 기존의 재료를 대신하는 경쟁력이 있는 재료로서 자리 매김하고 있습니다. 폴리케톤의 용도는, 특히 엄격한 성능이나 규제 기준을 만족시키는 재료를 필요로 하는 분야에서 계속 확대되고 있습니다. 환경 의식의 고조와 경량으로 연비가 좋은 솔루션의 추진이, 폴리케톤의 채용을 뒷받침하고 있습니다.

폴리케톤 시장 실적은 특히 내구성과 내약품성이 요구되는 분야에서 호조입니다. PK와 같은 경량 폴리머는 연료 시스템이나 자동차 구조 부품과 같은 고스트레스 환경에서 사용이 증가하고 있습니다. 폴리케톤은 제품 성능을 향상시켜 자동차 전체 무게를 줄이는 동시에 제조사가 엄격한 배기가스 규제를 충족시키는 데 도움을 주고 있습니다. 폴리케톤은 가혹한 조건에서도 기계적 강도를 유지할 수 있기 때문에, 특히 연료나 윤활유, 고온에 노출되는 경우가 많은 장소에서는, 종래의 엔지니어링 플라스틱을 대신하는 귀중한 선택사항이 됩니다. 이 재료는 펠릿, 섬유, 시트, 필름 등 다양한 형상에 적응할 수 있기 때문에 일렉트로닉스, 소비재, 운수 등의 산업에서 그 매력을 더욱 넓히고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 14억 달러 |

| 예측 금액 | 28억 달러 |

| CAGR | 5.5% |

펠릿 부문은 가공이 용이하고 압출 성형과 사출 성형과 같은 표준 제조 기술에 적합하기 때문에 2024년에는 39.53%의 점유율을 차지했습니다. 균일성, 저흡습성, 우수한 치수 안정성으로 복잡한 부품의 정밀한 제조가 가능합니다. 게다가 가혹한 화학물질이나 탄화수소에 대한 내성이 강하기 때문에 가혹한 환경에 노출되는 부품에 적합합니다. 이러한 이점에 의해, 펠릿은, 성능, 안전성, 규제에의 준거가 양보할 수 없는 자동차와 같은 요구가 어려운 분야에서, 최적의 형상이 되고 있습니다.

한편, 환경 친화적인 대체품에 대한 소비자의 의식이 개인 소비자 부문에서 수요를 밀어 올렸고, 2024년에는 50.36%의 점유율을 차지했습니다. 사람들은 일상 제품에 지속 가능한 소재를 찾는 경향이 있으며, 이러한 경향은 폴리케톤의 재활용 가능하고 친환경적인 특성과 잘 부합합니다. 소비자의 생각의 변화는 녹색 제품의 판매를 촉진할 뿐만 아니라 기업이 고성능의 지속 가능한 폴리머를 사용하여 기존 제품을 개량하도록 촉구하고 있습니다. 이 시프트는, 스포츠 용품, 웨어러블 테크놀로지, 주방용품, 신변의 액세서리 등, 내구성이나 기능에 타협하는 일 없이, 환경을 배려한 디자인을 유저가 요구하는 아이템의 생산에 있어서, 폴리케톤에 새로운 가능성을 가져왔습니다.

미국의 폴리케톤(PK) 시장은 2024년에 2억 4,000만 달러로 평가되었으며, 견고한 산업 틀, 혁신 중시 시장 개척, 첨단 재료에 대한 높은 수요에 힘입어 급성장을 이어가고 있습니다. 북미는 전자, 항공 우주, 자동차 분야의 활발한 활동으로 PK 용도의 주요 거점으로 계속 남아 있습니다. 지속 가능한 기술과 첨단 폴리머 과학을 중시하는 지역성은 이 지역에서 폴리케톤의 존재감을 강화하는 데 중요한 역할을 하고 있습니다.

폴리케톤(PK) 업계의 기업으로는 Nexeo Plastics, Ensinger, HYOSUNG, MITSUI PLASTICS, Avient 등을 들 수 있습니다. 시장에서 보다 견고한 지위를 확보하기 위해, 각사는 연구 개발에 다액의 투자를 실시하며, 제품의 혁신과 용도 분야의 확대에 주력하고 있습니다. 자동차 및 전자 분야의 제조업체와의 전략적 파트너십은 상업적인 채택을 뒷받침합니다. 기업은 또한 공급망의 효율을 개선하고 지속 가능한 제조 프로세스를 도입하고 있습니다. 커스텀 등급을 개발하고 제품 포트폴리오를 다양화함으로써 진화하는 최종 사용자의 요구에 대응하여 장기적인 경쟁력을 강화하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 트럼프 정권의 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망 및 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국

- 주요 수입국

참고 : 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

- 규제 상황

- 영향요인

- 성장 촉진요인

- 자동차 업계 수요 증가

- 전기자동차(EV) 및 지속 가능한 이동성의 상승

- 고성능 재료 수요 증가

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용

- 규제 및 환경에 대한 우려

- 성장 촉진요인

- 정책관여

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 방향족 폴리케톤

- 지방족 폴리케톤

- 공중합체 폴리케톤

제6장 시장 추계 및 예측 : 형태별(2021-2034년)

- 주요 동향

- 펠렛

- 섬유

- 필름

- 시트

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 자동차 부품

- 전기 및 전자공학

- 산업기계

- 소비재

- 코팅제 및 접착제

- 의료기기

- 포장

- 기타

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- AKRO-PLASTIC

- Avient

- Distrupol

- Ensinger

- HYOSUNG

- KD Feddersen

- LEHVOSS

- MITSUI PLASTICS

- Nexeo Plastics

- POLYOLS &POLYMERS

- Rochling

- Specialist Engineering Plastics

- Technoform

The Global Polyketone Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 2.8 billion by 2034 due to increasing demand for high-performance polymers across several industries. This growth is largely fueled by the search for advanced material alternatives that offer superior chemical resistance, low moisture absorption, and improved wear properties. These characteristics position polyketones as a competitive substitute for traditional materials like polyamides and polyoxymethylene. Their applications continue to expand, especially in sectors requiring materials that meet stringent performance and regulatory standards. Rising environmental consciousness and the push for lightweight, fuel-efficient solutions drive adoption.

Polyketone's market performance has been strong, particularly in segments that demand durability and chemical resistance. Lightweight polymers like PK are increasingly used in high-stress environments, such as fuel systems and structural automotive components. They help manufacturers meet strict emissions standards while improving product performance and reducing overall vehicle weight. Polyketone's ability to maintain mechanical strength under extreme conditions makes it a valuable alternative to conventional engineering plastics, especially where exposure to fuels, lubricants, and high temperatures is common. The material's adaptability in various forms-like pellets, fibers, sheets, and films-has further widened its appeal across industries, including electronics, consumer goods, and transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.8 Billion |

| CAGR | 5.5% |

The pellets segment accounted for 39.53% share in 2024 due to their ease of processing and compatibility with standard manufacturing techniques such as extrusion and injection molding. Their uniformity, low moisture absorption, and excellent dimensional stability allow precision in manufacturing complex parts. Additionally, their strong resistance to harsh chemicals and hydrocarbons makes them a preferred choice for components exposed to aggressive environments. These advantages make pellets the go-to form in demanding sectors like automotive, where performance, safety, and compliance with regulations are non-negotiable.

Meanwhile, consumer awareness of eco-friendly alternatives has pushed demand within the individual consumer segment, representing a 50.36% share in 2024. People lean toward sustainable materials in everyday products, a trend that aligns well with polyketone's recyclable and environmentally conscious profile. The shift in consumer mindset is not only driving sales of green products but also encouraging companies to reformulate existing goods using high-performance sustainable polymers. This shift has opened new opportunities for polyketone in the production of items such as sporting goods, wearable tech, kitchenware, and personal accessories-areas where users are now expecting eco-conscious design without compromising on durability or function.

United States Polyketone (PK) Market was valued at USD 240 million in 2024 and continues to grow rapidly, backed by a robust industrial framework, innovation-focused development, and a high demand for advanced materials. North America remains a major hub for PK applications due to strong activity in the electronics, aerospace, and automotive sectors. Local emphasis on sustainable technologies and advanced polymer science plays a significant role in reinforcing polyketone's presence in the region.

The Polyketone (PK) industry players include Nexeo Plastics, Ensinger, HYOSUNG, MITSUI PLASTICS, and Avient. To secure a stronger position in the market, companies are heavily investing in research and development, focusing on product innovations and expanding application areas. Strategic partnerships with manufacturers across the automotive and electronics sectors help boost commercial adoption. Businesses are also improving supply chain efficiency and introducing sustainable manufacturing processes. By developing custom grades and diversifying product portfolios, they're addressing evolving end-user needs and reinforcing long-term competitiveness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.3 Supply-side impact (raw materials)

- 3.2.3.1 Price volatility in key materials

- 3.2.3.2 Supply chain restructuring

- 3.2.3.3 Production cost implications

- 3.2.4 Demand-side impact (selling price)

- 3.2.4.1 Price transmission to end markets

- 3.2.4.2 Market share dynamics

- 3.2.4.3 Consumer response patterns

- 3.2.5 Key companies impacted

- 3.2.6 Strategic industry responses

- 3.2.6.1 Supply chain reconfiguration

- 3.2.6.2 Pricing and product strategies

- 3.2.6.3 Policy engagement

- 3.2.7 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Regulatory landscape

- 3.5 Impact forces

- 3.5.1 Growth drivers

- 3.5.1.1 Growing demand in the automotive industry

- 3.5.1.2 Rise of electric vehicles (EVs) and sustainable mobility

- 3.5.1.3 Increasing demand for high-performance materials

- 3.5.2 Industry pitfalls & challenges

- 3.5.2.1 High production costs

- 3.5.2.2 Regulatory & environmental concerns

- 3.5.1 Growth drivers

- 3.6 Policy engagement

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Aromatic polyketone

- 5.3 Aliphatic polyketone

- 5.4 Copolymer polyketone

Chapter 6 Market Estimates and Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Pellets

- 6.3 Fibers

- 6.4 Films

- 6.5 Sheets

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive components

- 7.3 Electrical & electronics

- 7.4 Industrial machinery

- 7.5 Consumer goods

- 7.6 Coatings & adhesives

- 7.7 Medical devices

- 7.8 Packaging

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 AKRO-PLASTIC

- 9.2 Avient

- 9.3 Distrupol

- 9.4 Ensinger

- 9.5 HYOSUNG

- 9.6 K.D. Feddersen

- 9.7 LEHVOSS

- 9.8 MITSUI PLASTICS

- 9.9 Nexeo Plastics

- 9.10 POLYOLS & POLYMERS

- 9.11 Rochling

- 9.12 Specialist Engineering Plastics

- 9.13 Technoform