|

시장보고서

상품코드

1750470

항공기용 와이어 및 케이블 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Aircraft Wire and Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

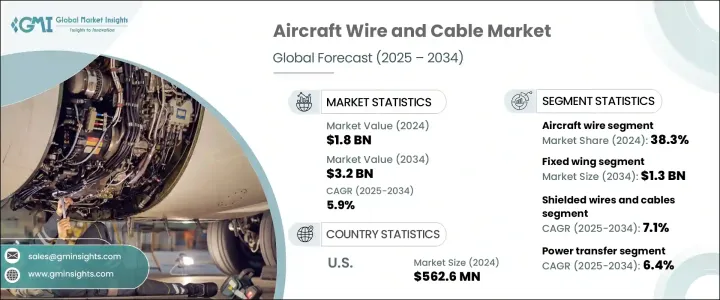

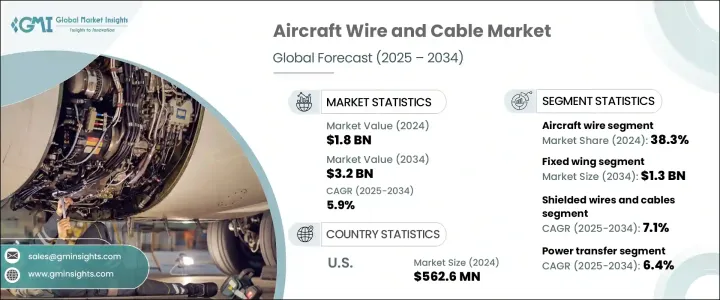

세계의 항공기용 와이어 및 케이블 시장은 2024년에는 18억 달러로 평가되었으며 항공기 생산량의 급증과 전동화 및 도시형 에어모빌리티 플랫폼의 급속한 진보로 CAGR 5.9%를 나타내 2034년까지는 32억 달러에 이를 것으로 예측되고 있습니다.

항공기가 복잡한 시스템과 추진의 전동화에 의해 진화함에 따라 혁신적인 배선 솔루션에 대한 수요가 급증하고 있습니다.

기업 간부는 이전의 무역 제한, 특히 수입 알루미늄과 강철에 대한 관세가 항공우주 밸류체인을 어떻게 혼란시켰는지 되돌아 보았습니다. 또한 국제 보복 관세로 인해 조달 업무가 혼란스럽고 중요한 케이블 재료의 가격과 조달이 불안정 해졌습니다. 오늘날의 전기 항공기 및 eVTOL 플랫폼에서는 어비오닉스, 배터리 추진, 열 제어 등의 시스템에 고급 배선이 필요합니다. 그러나 가혹한 조건에도 견딜 수 있는 케이블이 필요합니다. 애널리스트는 첨단 항공기 설계 동향으로 인해 항공우주 기업은 차세대 항공기의 목표에 따른 견고하고 컴팩트한 케이블 시스템 개발에 많은 투자를 하고 있다고 강조하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 18억 달러 |

| 예측 금액 | 32억 달러 |

| CAGR | 5.9% |

와이어 및 케이블 제품 부문의 항공기용 와이어 부문은 2024년에 38.3%의 점유율을 차지했는데, 그 이유는 다양한 항공기 시스템 전체에서 전력, 제어 신호, 데이터 전송에 필수적인 역할을 담당하고 있었기 때문입니다. 기술과 자동화가 확대됨에 따라 내열성이 뛰어나고 가벼운 배선 솔루션에 대한 수요가 높아지고 있음을 강조하고 있습니다.

고정 날개 항공기 부문은 생산 라인 확대와 노후화된 항공기의 지속적인 업그레이드로 인해 2034년까지 13억 달러에 달할 것으로 예측됩니다. 전익기 및 무인 항공기보다 복잡한 배선 시스템이 필요하다고 지적합니다. 이 항공기는 일반적으로 장거리 작동과 고급 안전 기능을 지원하는 고밀도 모듈식 와이어 하네스가 필요합니다.

미국의 항공기용 와이어 및 케이블 시장은 민간 항공우주 및 방위 부문에 대한 강력한 자금 공급에 힘입어 2024년 5억 6,260만 달러의 규모가 되었습니다. 우리는 특수 와이어 재료와 차폐 기술의 개발을 촉진하고 있다고 지적합니다.

세계의 항공기용 와이어 및 케이블 시장에서 사업을 전개하는 기업은 시장 실적을 강화하기 위해 여러 전략을 채택하고 있습니다. Aerospace와 같은 주요 기업들은 보다 가볍고 열적으로 안정적인 케이블 솔루션을 개발하기 위해 R&D 투자를 선도하고 있습니다. 게다가, 각 회사는 제품 포트폴리오와 경쟁력을 강화하는 전략적 인수와 인증 취득에 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 항공기 생산과 납품 증가

- 신흥국의 상업항공 확대

- 군용기의 조달과 개수의 급증

- 유지보수, 수리, 오버홀(MRO) 부문의 성장

- 도시항공모빌리티 및 전기항공기 프로그램에 대한 투자 증가

- 업계의 잠재적 리스크 및 과제

- 첨단 항공우주 등급 재료의 높은 비용

- 구형 항공기의 개수에 있어서의 과제

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 유형별(2021-2034년)

- 주요 동향

- 항공기 와이어

- 항공기 케이블

- 동축 케이블

- 데이터 케이블

- 전원 케이블

- 광섬유 케이블

- RF 케이블

- 기타

- 항공기 하네스

제6장 시장 추계·예측 : 항공기 유형별(2021-2034년)

- 주요 동향

- 고정익

- 회전익

- 무인 항공기

제7장 시장 추계·예측 : 실드 유형별(2021-2034년)

- 주요 동향

- 차폐 전선 및 케이블

- 비차폐 전선 및 케이블

제8장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 비행 제어 시스템

- 조명 시스템

- 데이터 전송

- 전력 전송

- 항공전자공학

- 랜딩 기어 및 제동 시스템

- 기타

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Aerospace Wire &Cable

- Ametek

- Amphenol

- Bergen Cable Technology

- Collins Aerospace

- Eaton

- HUBER SUHNER

- Lexco Cable

- Miracle Electronics Devices

- Molex

- Nexans

- PIC Wire &Cable

- Prysmian Group

- Radiall

- Sanghvi Aerospace

- TE Connectivity

- Tyler Madison

- WL Gore and Associates

The Global Aircraft Wire and Cable Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 3.2 billion by 2034, driven by the surge in aircraft production volumes, paired with rapid advancements in electric and urban air mobility platforms. As aircraft evolve with complex systems and propulsion electrification, the demand for innovative wiring solutions continues to surge. Several stakeholders also pointed out that as next-generation aircraft become more reliant on high-performance cables, the role of lightweight, thermally stable, and high-voltage wiring systems becomes even more crucial in both commercial and military applications.

Company officials recalled how earlier trade restrictions, particularly the tariffs on imported aluminum and steel, disrupted the aerospace value chain. These policy changes elevated raw material prices, complicating budgeting for OEMs and major tier-1 suppliers. Additionally, international retaliatory tariffs disrupted sourcing operations, leading to instability in pricing and procurement of vital cabling materials. Firms with globally integrated supply chains faced the most severe setbacks, as sourcing delays and elevated costs strained manufacturing timelines. As noted by engineers, electrical aircraft and eVTOL platforms today demand sophisticated wiring for systems like avionics, battery propulsion, and thermal control. These applications require cables that can withstand extreme conditions while keeping weight minimal. Analysts emphasized that advanced aircraft design trends have driven aerospace firms to invest more in developing robust and compact cable systems that align with next-gen aviation goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 5.9% |

The aircraft wire segment in the wire and cable product segment held a 38.3% share in 2024, attributed to its essential role in transmitting power, control signals, and data throughout various aircraft systems. Industry suppliers emphasized that demand is growing for heat-resistant, lightweight wiring solutions, particularly as aircraft programs transition toward next-generation electric architectures and increased automation. Regulatory pressures around electromagnetic interference and fire resistance also shape design parameters, making advanced wire configurations vital for airworthiness certifications and fleet retrofits.

The fixed-wing aircraft segment is anticipated to reach USD 1.3 billion by 2034, driven by expanding production lines and continued upgrades to aging fleets. Aviation engineers pointed out that fixed-wing designs generally require more intricate cabling systems than rotary-wing or unmanned aerial vehicles, as they host a greater concentration of avionics, flight control, and cabin systems. These aircraft typically demand dense, modular wiring harnesses that support long-range operations and advanced safety features.

United States Aircraft Wire and Cable Market generated USD 562.6 million in 2024, underpinned by strong funding for the commercial aerospace and defense sectors. Industry insiders noted that U.S.-based programs prioritize reliability and survivability under harsh conditions, prompting the development of specialized wire materials and shielding technologies. The country remains a testing ground for high-voltage and fiber-optic cabling systems designed for more electric aircraft platforms, signaling long-term growth potential.

Companies operating in the Global Aircraft Wire and Cable Market are adopting multiple strategies to bolster their market footprint. Key players such as Ametek, Eaton, Aerospace Wire & Cable, Bergen Cable Technology, Amphenol, and Collins Aerospace have prioritized R&D investments to develop lighter, more thermally stable cable solutions. Many firms are expanding their global manufacturing capabilities to improve supply chain agility and meet growing demand. Collaborations with aircraft OEMs and system integrators are also rising, enabling tailored wiring architectures that align with evolving aircraft designs. In addition, companies are focusing on strategic acquisitions and certifications that enhance their product portfolios and competitive standing. These moves aim to ensure resilience and sustained growth in a highly technical and regulation-driven market.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising aircraft production and deliveries

- 3.3.1.2 Expansion of commercial aviation in emerging economies

- 3.3.1.3 Surge in military aircraft procurement and upgrades

- 3.3.1.4 Growth of the maintenance, repair, and overhaul (mro) sector

- 3.3.1.5 Rising investments in urban air mobility and electric aircraft programs

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High cost of advanced aerospace-grade materials

- 3.3.2.2 Challenges in retrofitting legacy aircraft

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 Pestel analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Aircraft wire

- 5.3 Aircraft cable

- 5.3.1 Coaxial cables

- 5.3.2 Data cables

- 5.3.3 Power cables

- 5.3.4 Fiber optic cables

- 5.3.5 RF cables

- 5.3.6 Others

- 5.4 Aircraft harness

Chapter 6 Market Estimates & Forecast, By Aircraft Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Fixed wing

- 6.3 Rotary wing

- 6.4 Unmanned aerial vehicles

Chapter 7 Market Estimates & Forecast, By Shielding Type, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Shielded wires and cables

- 7.3 Unshielded wires and cables

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Flight control systems

- 8.3 Lighting systems

- 8.4 Data transfer

- 8.5 Power transfer

- 8.6 Avionics

- 8.7 Landing gear & braking systems

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion & Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aerospace Wire & Cable

- 10.2 Ametek

- 10.3 Amphenol

- 10.4 Bergen Cable Technology

- 10.5 Collins Aerospace

- 10.6 Eaton

- 10.7 HUBER+SUHNER

- 10.8 Lexco Cable

- 10.9 Miracle Electronics Devices

- 10.10 Molex

- 10.11 Nexans

- 10.12 PIC Wire & Cable

- 10.13 Prysmian Group

- 10.14 Radiall

- 10.15 Sanghvi Aerospace

- 10.16 TE Connectivity

- 10.17 Tyler Madison

- 10.18 WL Gore and Associates