|

시장보고서

상품코드

1750476

영상 유도 치료 시스템 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Image-guided Therapy Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

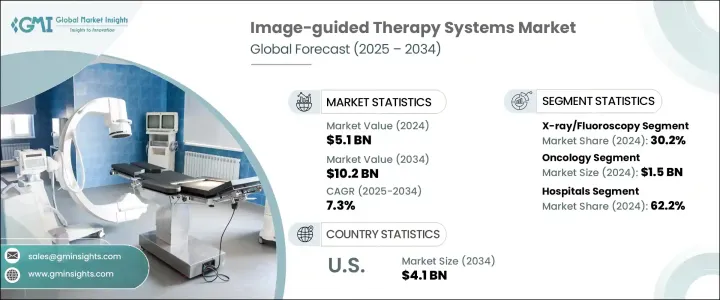

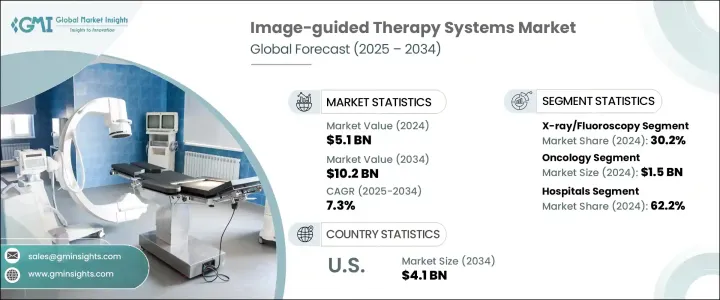

세계의 영상 유도 치료 시스템 시장은 2024년에는 51억 달러로 평가되었고 신경질환, 심혈관질환, 암을 포함한 만성질환의 유병률 상승에 촉진되어 2034년에는 102억 달러에 달할 것으로 추정되며 CAGR 7.3%로 성장할 전망입니다.

정밀 의학에 대한 의존도가 증가하고 최소 침습적 시술에 대한 강력한 수요가 결합되면서, 실시간 이미지 기반 안내를 제공하는 시스템에 대한 수요가 크게 증가했습니다. AI 기반 영상 기술, 로봇 보조 내비게이션, 3D 시각화 등 의료 기술의 발전은 정밀도를 향상시키고 시술 시간을 단축하며 임상 결과를 개선함으로써 수술을 혁신하고 있습니다.

환자와 의료진 모두 통증 감소, 빠른 회복 시간, 짧은 입원 기간 등 이점을 이유로 비침습적 접근법을 선호하고 있습니다. 인공지능과 머신러닝은 진단 과정을 간소화하고 영상 해석을 개선하며 절차 내비게이션을 자동화함으로써 영상 기반 치료의 활용도를 최적화합니다. 전 세계 의료 시스템이 환자 중심 및 가치 기반 의료로 전환함에 따라 영상 기반 솔루션은 수술 계획 및 실행의 필수 요소로 자리매김하고 있습니다. 하이브리드 수술실의 도입이 가속화되며, 고급 영상 도구를 수술실에 직접 통합해 수술 중 원활한 사용을 가능하게 함으로써 의사 결정 개선과 합병증 위험 감소에 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 51억 달러 |

| 예측 금액 | 102억 달러 |

| CAGR | 7.3% |

제품별로 X선 및 형광 투시 유도 시스템은 2024년에 30.2%의 점유율을 차지하며, 심장학, 정형외과, 중재 방사선학 등 분야에서 강력한 수요를 반영했습니다. 최소한의 외상으로 실시간 영상 유도 중재를 수행할 수 있는 능력은 병원과 외래 진료 환경에서 이러한 시스템이 널리 채택된 주요 요인입니다. 이러한 시스템의 영상 기능이 개선됨에 따라 의사는 더 높은 정확성과 더 낮은 위험으로 복잡한 시술을 수행할 수 있게 되었으며, 이는 해당 부문의 지속적인 성장에 기여하고 있습니다.

종양학 부문은 2024년에 15억 달러의 매출을 올렸습니다. 전 세계적으로 암 발병률이 계속 증가함에 따라, 임상의들은 방사선, 생검, 절제술 등 더 표적화된 치료를 위해 영상 유도 시스템으로 눈을 돌리고 있습니다. MRI, PET, CT, 초음파 등 영상 도구와의 실시간 통합은 시술 중 안내 기능을 크게 향상시켜 종양 위치 파악, 작은 절개, 주변 조직을 보존하는 맞춤형 치료를 가능하게 했습니다. 이는 브라키테라피, SBRT, RF 절제술 등 시술에서 이러한 시스템의 사용을 가속화했습니다.

미국의 영상 유도 치료 시스템 시장은 2024년에 21억 달러로 평가되었으며, 2034년에는 두 배로 성장할 것으로 예상됩니다. 미국은 결과 중심의 의료 서비스를 추진하면서 임상적 효율성과 비용 효율성을 모두 달성하는 기술의 채택을 장려하고 있습니다. 만성 질환에 직면한 고령 인구가 증가하면서 해당 시장의 규모도 확대되고 있습니다. 병원과 외래 환자 센터는 영상 유도 치료 시스템을 통합하여 시술의 정확성을 높이고 환자의 회복 시간을 최소화하고 있습니다. 가치 기반 보상 모델로의 전환은 의료 제공자가 더 나은 결과를 달성하며 합병증을 줄이는 장비에 투자하도록 유도하고 있습니다.

시장 점유율을 강화하기 위해 Stryker, Medtronic, Siemens Healthineers, Canon Medical Systems, Intuitive Surgical 등 주요 기업들은 AI 기반 소프트웨어, 클라우드 통합 영상 플랫폼, 고급 수술 로봇 기술에 투자하고 있습니다. 이 기업들은 병원과의 전략적 파트너십을 구축하고 전문 스타트업 인수합병을 진행하며 연구개발(R&D)을 확대해 차세대 제품 파이프라인을 지원하고 있습니다. 이들은 시장별 맞춤형 기기 개발과 수술 후 분석 도구를 통해 수술 결과 개선과 의료 제공자의 브랜드 충성도를 높이는 데 집중하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성질환의 유병률 상승

- 영상 및 내비게이션 기술의 발전

- 최소 침습 수술에 대한 수요 증가

- 정부 지원 정책 및 민간 투자

- 업계의 잠재적 위험 및 과제

- 높은 자본 및 유지보수 비용

- 신흥 시장에서의 접근성 제한

- 성장 촉진요인

- 성장 가능성 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후의 검토 사항 트럼프 정권의 관세

- 무역에 미치는 영향

- 기술의 상황

- 장래 시장 동향

- 규제 상황

- 갭 분석

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품 유형별(2024-2034년)

- 주요 동향

- X선 및 형광 투시 유도 시스템

- 초음파

- 컴퓨터 단층 촬영

- 자기 공명 영상

- 양전자 방출 단층 촬영

- 기타 제품 유형

제6장 시장 추계 및 예측 : 용도별(2024-2034년)

- 주요 동향

- 심장 수술

- 뇌신경외과

- 정형외과

- 소화기내과

- 비뇨기과

- 종양학

- 이비인후과 수술

- 기타 용도

제7장 시장 추계 및 예측 : 최종 용도별(2024-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 조사 및 학술 기관

제8장 시장 추계 및 예측 : 지역별(2024-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 일본

- 중국

- 인도

- 호주

- 한국

- 라틴아메리카

- 멕시코

- 브라질

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Accuray

- Analogic

- Brainlab

- Canon Medical Systems

- Fujifilm Holdings

- GE HealthCare

- Intuitive Surgical

- Karl Storz

- Koninklijke Philips

- Medtronic

- Olympus

- Siemens Healthineers

- Smith &Nephew

- Stryker

- Zimmer Biomet

The Global Image-guided Therapy Systems Market was valued at USD 5.1 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 10.2 billion by 2034, driven by the rising prevalence of chronic illnesses, including neurological disorders, cardiovascular conditions, and cancer. Increasing reliance on precision medicine, coupled with a strong push for minimally invasive procedures, has significantly boosted demand for systems that allow real-time, image-based guidance. Medical advancements such as AI-enabled imaging, robotic-assisted navigation, and 3D visualization are transforming surgery by enhancing precision, shortening procedure durations, and improving clinical outcomes.

Patients and providers alike are increasingly favoring less invasive approaches due to benefits like reduced pain, quicker recovery times, and shorter hospital stays. Artificial intelligence and machine learning optimize the utility of image-guided therapy by streamlining diagnostics, improving imaging interpretation, and automating procedural navigation. As global healthcare systems move toward patient-centered and value-based care, image-guided solutions are becoming an essential part of surgical planning and execution. The adoption of hybrid operating rooms is accelerating and integrating advanced imaging tools directly into the surgical suite for seamless intraoperative use, which enhances decision-making and lowers the risk of complications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $10.2 Billion |

| CAGR | 7.3% |

Among product categories, X-ray and fluoroscopy-guided systems accounted for a 30.2% share in 2024, reflecting strong demand in fields such as cardiology, orthopedics, and interventional radiology. The ability to perform real-time image-guided interventions with minimal trauma is a key factor behind their widespread adoption across hospitals and ambulatory settings. Improved imaging functionality in these systems enables physicians to carry out complex procedures with higher accuracy and reduced risk, which is contributing to ongoing segment growth.

The oncology segment generated USD 1.5 billion in 2024. As cancer cases continue to rise globally, clinicians are turning to image-guided systems for more targeted therapies, including radiation, biopsies, and ablations. Real-time integration of imaging tools like MRI, PET, CT, and ultrasound has greatly enhanced intra-procedural guidance, allowing for better tumor localization, smaller incisions, and personalized treatments that spare surrounding tissue. This has accelerated the use of these systems in procedures such as brachytherapy, SBRT, and RF ablation.

U.S. Image-guided Therapy Systems Market was valued at USD 2.1 billion in 2024 and is projected to double by 2034. The country's push for outcome-driven healthcare is encouraging the adoption of technologies that deliver both clinical and cost efficiency. A growing elderly population facing chronic illnesses is also expanding the addressable market. Hospitals and outpatient centers integrate image-guided therapy systems to improve procedural precision and minimize patient recovery time. The shift toward value-based reimbursement models incentivizes providers to invest in equipment that supports better outcomes with fewer complications.

To strengthen their presence, leading firms like Stryker, Medtronic, Siemens Healthineers, Canon Medical Systems, and Intuitive Surgical are investing in AI-powered software, cloud-integrated imaging platforms, and advanced surgical robotics. These companies are forming strategic partnerships with hospitals, acquiring specialized startups, and expanding R&D efforts to support next-generation product pipelines. They focus on market-specific device customization and post-operative analytics tools to enhance procedural outcomes and extend brand loyalty among healthcare providers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of chronic diseases

- 3.2.1.2 Advancements in imaging and navigation technologies

- 3.2.1.3 Growing demand for minimally invasive surgeries

- 3.2.1.4 Supportive government policies and private investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital and maintenance costs

- 3.2.2.2 Limited access in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerationsTrump administration tariffs

- 3.4.1 Impact on trade

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.8 Gap analysis

- 3.9 Patent analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 X-ray/fluoroscopy

- 5.3 Ultrasound

- 5.4 Computed tomography

- 5.5 Magnetic resonance imaging

- 5.6 Positron emission tomography

- 5.7 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cardiac surgery

- 6.3 Neurosurgery

- 6.4 Orthopedic surgery

- 6.5 Gastroenterology

- 6.6 Urology

- 6.7 Oncology

- 6.8 ENT surgery

- 6.9 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Research and academic institutions

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accuray

- 9.2 Analogic

- 9.3 Brainlab

- 9.4 Canon Medical Systems

- 9.5 Fujifilm Holdings

- 9.6 GE HealthCare

- 9.7 Intuitive Surgical

- 9.8 Karl Storz

- 9.9 Koninklijke Philips

- 9.10 Medtronic

- 9.11 Olympus

- 9.12 Siemens Healthineers

- 9.13 Smith & Nephew

- 9.14 Stryker

- 9.15 Zimmer Biomet