|

시장보고서

상품코드

1750489

탄소섬유 주입 폴리머 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Carbon Fiber-Infused Polymers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

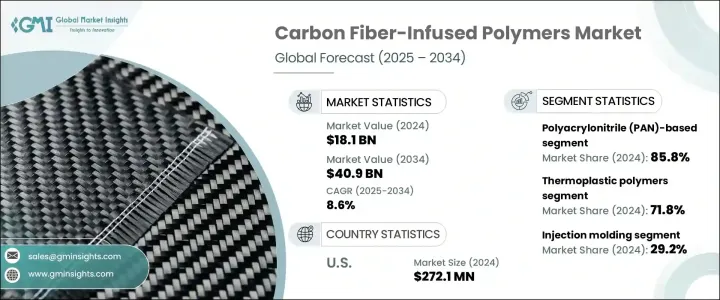

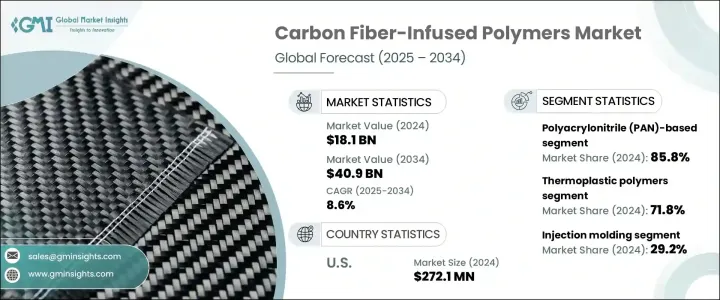

세계의 탄소섬유 주입 폴리머 시장 규모는 2024년 181억 달러로 평가되었고 자동차, 항공우주, 방위, 신재생에너지 분야 등 다양한 산업 수요 증가에 견인되어 CAGR 8.6%를 나타내 2034년까지는 409억 달러에 달할 것으로 예측되고 있습니다.

고강도 대 중량비, 내식성, 열안정성 등 탄소섬유 주입 폴리머의 독특한 특성은 경량이고 내구성이 있는 재료를 필요로 하는 용도에 이상적입니다.

마찬가지로 항공우주 및 방위산업에 있어서도 이러한 복합재를 채용함으로써 성능이 향상되어 운용비용이 절감됩니다. 다른 재료는 운전 효율을 높이면서 풍력에너지를 포착하는 가볍고 내구성 있는 블레이드를 가능하게 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 181억 달러 |

| 예측 금액 | 409억 달러 |

| CAGR | 8.6% |

탄소섬유 주입 폴리머 시장에서 폴리머 유형별로 세분화하면 열가소성 폴리머와 열경화성 폴리머가 주목됩니다.

사출 성형 분야는 정밀하고 내구성 있는 부품을 대규모로 공급할 수 있기 때문에 2024년에는 29.2%의 점유율을 차지했습니다. 특히 자동차 분야에서는 경량이면서 견고한 구조 부품의 생산이 가능 능으로 자동차의 성능과 연비 향상에 기여하기 위해 이 공정의 혜택을 받고 있습니다.

2024년 미국의 탄소섬유 주입 폴리머 시장 점유율은 85%를 나타냈고 혁신과 첨단 제조업에 대한 미국의 전략적 투자가 견인하고 있습니다. 과 테스트 베드의 설립이 촉진되고 있습니다. 이러한 노력은 탄소섬유의 비용을 낮추고, 특히 방위, 모빌리티, 클린 에너지 등의 주요 분야에서 상업 이용할 수 있도록 그 성능을 향상시키는 것을 목적으로 하고 있습니다.

세계의 탄소섬유 주입 폴리머 시장에서 사업을 전개하고 있는 주요 기업으로는 Toray Industries Inc. Teijin Limited, Hexcel Corporation, SGL Carbon, Solvay SA 등이 있습니다. 이러한 기업은 기술 혁신의 최전선에 서서 다양한 산업의 높아지는 수요에 부응하기 위해 첨단 재료나 제조 공정의 개발에 주력하고 있습니다. 몇 가지 전략적 이니셔티브를 채택하고 있습니다. 여기에는 재료 특성의 혁신과 개선을위한 연구 개발 투자, 시장 개척을 위한 합작 투자 및 파트너십 확립, 수요 증가에 대응하기 위한 제조 능력 강화 등이 포함됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 원재료 공급자

- 제조업체

- 유통업체

- 최종 용도

- 이익률 분석

- COVID-19에 의한 밸류체인의 혼란

- 트럼프 정권의 관세 영향 - 구조화된 개요

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국

- 주요 수입국

참고 : 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

- 이익률 분석

- 주요 뉴스와 대처

- 기술의 상황

- 전통적인 제조 기술

- 첨단 제조 기술

- 신흥기술

- 특허 분석

- 규제 상황

- 시장 역학

- 시장 성장 촉진요인

- 자동차 산업과 항공우주 산업에서 경량 소재 수요 증가

- 연비와 배출 가스 삭감에 대한 관심 증가

- 스포츠나 레저의 용도로 채용 증가

- 신재생에너지 부문 확대

- 제조 공정에 있어서 기술의 진보

- 업계의 잠재적 리스크 및 과제

- 높은 생산 비용

- 복잡한 제조 공정

- 재활용과 수명의 과제

- 공급망의 취약성

- 시장 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 시장 점유율 분석

- 경쟁 대시보드

- 전략적 노력

- 합병 및 인수

- 합작사업

- 제품 발매

- 확장 계획

- R&D 투자

- 경쟁 벤치마킹

- 벤더 채용 매트릭스

- 경쟁 포지셔닝 매트릭스

제5장 시장 추계·예측 : 폴리머 유형별(2021-2034년)

- 주요 동향

- 열가소성 폴리머

- 폴리아미드(PA)

- 폴리프로필렌(PP)

- 폴리에테르에테르케톤(PEEK)

- 폴리페닐렌설파이드(PPS)

- 폴리에테르이미드(PEI)

- 기타

- 열경화성 폴리머

- 에폭시

- 폴리에스테르

- 비닐에스테르

- 폴리우레탄

- 기타

제6장 시장 추계·예측 : 탄소 섬유 유형별(2021-2034년)

- 주요 동향

- 폴리아크릴로니트릴(PAN) 기반

- 표준 모듈러스

- 중간 모듈러스

- 높은 모듈러스

- 피치 기반

- 레이온 기반

- 재활용 탄소섬유

제7장 시장 추계·예측 : 제조 공정별(2021-2034년)

- 주요 동향

- 사출 성형

- 압축 성형

- 수지 트랜스퍼 성형

- 인발 성형

- 필라멘트 와인딩

- 적층 제조

- 기타

제8장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 항공우주 및 방위

- 항공기 부품

- 우주용도

- 방위 장비

- 자동차

- 구조 부품

- 내부 부품

- 파워트레인 부품

- 전기자동차의 용도

- 풍력에너지

- 블레이드

- 나셀

- 기타 구성 요소

- 스포츠 및 레저

- 자전거

- 테니스 라켓

- 골프 클럽

- 기타

- 건설

- 보강재

- 구조 부품

- 기타

- 해양

- 선체 구조

- 데크 구성 요소

- 기타

- 의료

- 보철

- 화상 기기

- 기타

- 산업기기

- 기타

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Carbon Fiber Composite Design

- Composite Horizons LLC

- Cytec Industries Inc.

- DowAksa

- Formosa Plastics Corporation

- Hexcel Corporation

- Hyosung Advanced Materials

- Kureha Corporation

- Mitsubishi Chemical Holdings Corporation

- Nippon Carbon Co.Ltd.

- Plasan Carbon Composites

- SABIC

- SGL Carbon

- Sigmatex

- Solvay SA

- Teijin Limited

- Toho Tenax Co.Ltd.

- Toray Industries, Inc.

- Zhongfu Shenying Carbon Fiber Co. Ltd.

- Zoltek Companies, Inc.

The Global Carbon Fiber-Infused Polymers Market was valued at USD 18.1 billion in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 40.9 billion by 2034, driven by the increasing demand across various industries, including automotive, aerospace, defense, and renewable energy sectors. The unique properties of carbon fiber-infused polymers-such as high strength-to-weight ratios, corrosion resistance, and thermal stability-make them ideal for applications requiring lightweight and durable materials. In the automotive industry, these materials contribute to fuel efficiency and reduced emissions, aligning with stringent environmental regulations.

Similarly, in aerospace and defense, adopting these composites enhances performance and reduces operational costs. The renewable energy industry, especially the wind power segment, continues to gain from integrating carbon fiber composites into turbine blade production. These materials allow lighter, more durable blades that capture wind energy while enhancing operational efficiency. Their high strength-to-weight ratio supports the design of longer blades, which leads to greater energy output without compromising structural integrity-an essential factor for large-scale wind installations both onshore and offshore.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.1 Billion |

| Forecast Value | $40.9 Billion |

| CAGR | 8.6% |

Within the carbon fiber-infused polymers market, segmentation by polymer type highlights thermoplastic and thermoset variants. The thermoplastic polymers segment held 71.8% share in 2024, favored for their recyclability, fast processing times, and ability to withstand repeated heating and reshaping. These features make them attractive for high-volume applications in automotive and aerospace manufacturing, where sustainability and cost-efficiency are becoming increasingly important.

The injection molding segment held a 29.2% share in 2024 due to its ability to deliver precise, durable parts at scale. The automotive sector, in particular, benefits from this process, as it enables the production of lightweight yet robust structural parts that contribute to improved vehicle performance and fuel efficiency. Injection molding's adaptability to complex geometries and compatibility with thermoplastic composites further amplify its market relevance.

United States Carbon Fiber-Infused Polymers Market held 85% share in 2024, driven by the nation's strategic investment in innovation and advanced manufacturing. Public and private sector funding has facilitated the establishment of dedicated research centers and test beds focused on optimizing composite material production. These efforts aim to lower the cost of carbon fiber and improve its performance for commercial use, particularly in key sectors like defense, mobility, and clean energy.

Key companies operating in the Global Carbon Fiber-Infused Polymers Market include Toray Industries Inc., Teijin Limited, Hexcel Corporation, SGL Carbon, and Solvay S.A. These companies are at the forefront of innovation, focusing on developing advanced materials and manufacturing processes to meet the growing demands of various industries. To strengthen their market position, companies in the carbon fiber-infused polymers industry are adopting several strategic initiatives. These include investing in research and development to innovate and improve material properties, establishing joint ventures and partnerships to expand market reach, and enhancing manufacturing capabilities to meet increasing demand.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research methodology

- 1.1.1 Initial data exploration

- 1.1.2 Primary research methodology

- 1.1.3 Secondary research methodology

- 1.1.4 Market size estimation approach

- 1.1.5 Data triangulation techniques

- 1.1.6 Research assumptions

- 1.2 Market definition and scope

- 1.2.1 Base year and forecast period

- 1.2.2 Market segmentation

- 1.2.3 Regional scope

- 1.2.4 Currency conversion rates

- 1.3 Information procurement

- 1.3.1 Purchased database

- 1.3.2 GMI's internal database

- 1.3.3 Secondary sources

- 1.3.4 Primary research

- 1.4 Information analysis

- 1.4.1 Data analysis models

- 1.4.2 Market breakdown and data triangulation

Chapter 2 Executive Summary

- 2.1 Carbon fiber-infused polymers industry 3600 synopsis, 2021-2034

- 2.1.1 Business trends

- 2.1.2 Regional trends

- 2.1.3 Polymer type trends

- 2.1.4 Carbon fiber type trends

- 2.1.5 Manufacturing process trends

- 2.1.6 End use industry trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Manufacturers

- 3.1.3 Distributors

- 3.1.4 End use

- 3.1.5 Profit margin analysis

- 3.1.6 Value chain disruptions due to COVID-19

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.5.1 Technology landscape

- 3.5.2 Traditional manufacturing technologies

- 3.5.3 Advanced manufacturing technologies

- 3.5.4 Emerging technologies

- 3.5.5 Patent analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Market dynamics

- 3.7.1 Market drivers

- 3.7.1.1 Increasing demand for lightweight materials in the automotive and aerospace industries

- 3.7.1.2 Growing focus on fuel efficiency and emission reduction

- 3.7.1.3 Rising adoption in sports and leisure applications

- 3.7.1.4 Expanding the renewable energy sector

- 3.7.1.5 Technological advancements in manufacturing processes

- 3.7.2 Industry pitfalls and challenges

- 3.7.2.1 High production costs

- 3.7.2.2 Complex manufacturing processes

- 3.7.2.3 Recycling and end-of-life challenges

- 3.7.2.4 Supply chain vulnerabilities

- 3.7.1 Market drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.9.1 Supplier power

- 3.9.2 Buyer power

- 3.9.3 Threat of new entrants

- 3.9.4 Threat of substitutes

- 3.9.5 Industry rivalry

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis, 2024

- 4.2 Competitive dashboard

- 4.3 Strategic initiatives

- 4.3.1 Mergers & acquisitions

- 4.3.2 Joint ventures

- 4.3.3 Product launches

- 4.3.4 Expansion plans

- 4.3.5 R&D investments

- 4.4 Competitive benchmarking

- 4.5 Vendor adoption matrix

- 4.6 Competitive positioning matrix

Chapter 5 Market Estimates and Forecast, By Polymer Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Thermoplastic polymers

- 5.2.1 Polyamide (PA)

- 5.2.2 Polypropylene (PP)

- 5.2.3 Polyether ether ketone (PEEK)

- 5.2.4 Polyphenylene sulfide (PPS)

- 5.2.5 Polyetherimide (PEI)

- 5.2.6 Others

- 5.3 Thermoset polymers

- 5.3.1 Epoxy

- 5.3.2 Polyester

- 5.3.3 Vinyl ester

- 5.3.4 Polyurethane

- 5.3.5 Others

Chapter 6 Market Estimates and Forecast, By Carbon Fiber Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Polyacrylonitrile (PAN)-based

- 6.2.1 Standard modulus

- 6.2.2 Intermediate modulus

- 6.2.3 High modulus

- 6.3 Pitch-based

- 6.4 Rayon-based

- 6.5 Recycled carbon fiber

Chapter 7 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Injection molding

- 7.3 Compression molding

- 7.4 Resin transfer molding

- 7.5 Pultrusion

- 7.6 Filament winding

- 7.7 Additive manufacturing

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.2.1 Aircraft components

- 8.2.2 Space applications

- 8.2.3 Defense equipment

- 8.3 Automotive

- 8.3.1 Structural components

- 8.3.2 Interior components

- 8.3.3 Powertrain components

- 8.3.4 Electric vehicle applications

- 8.4 Wind energy

- 8.4.1 Blades

- 8.4.2 Nacelles

- 8.4.3 Other components

- 8.5 Sports & leisure

- 8.5.1 Bicycles

- 8.5.2 Tennis rackets

- 8.5.3 Golf clubs

- 8.5.4 Others

- 8.6 Construction

- 8.6.1 Reinforcement materials

- 8.6.2 Structural components

- 8.6.3 Others

- 8.7 Marine

- 8.7.1 Hull structures

- 8.7.2 Deck components

- 8.7.3 Others

- 8.8 Medical

- 8.8.1 Prosthetics

- 8.8.2 Imaging equipment

- 8.8.3 Others

- 8.9 Industrial equipment

- 8.10 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Carbon Fiber Composite Design

- 10.2 Composite Horizons LLC

- 10.3 Cytec Industries Inc.

- 10.4 DowAksa

- 10.5 Formosa Plastics Corporation

- 10.6 Hexcel Corporation

- 10.7 Hyosung Advanced Materials

- 10.8 Kureha Corporation

- 10.9 Mitsubishi Chemical Holdings Corporation

- 10.10 Nippon Carbon Co., Ltd.

- 10.11 Plasan Carbon Composites

- 10.12 SABIC

- 10.13 SGL Carbon

- 10.14 Sigmatex

- 10.15 Solvay S.A.

- 10.16 Teijin Limited

- 10.17 Toho Tenax Co., Ltd.

- 10.18 Toray Industries, Inc.

- 10.19 Zhongfu Shenying Carbon Fiber Co., Ltd.

- 10.20 Zoltek Companies, Inc.