|

시장보고서

상품코드

1750493

PVT 콜렉터 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)PVT Collectors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

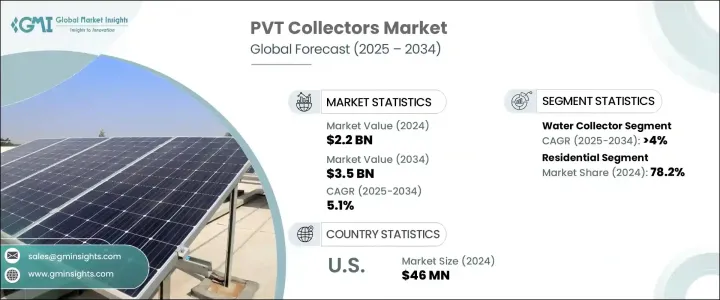

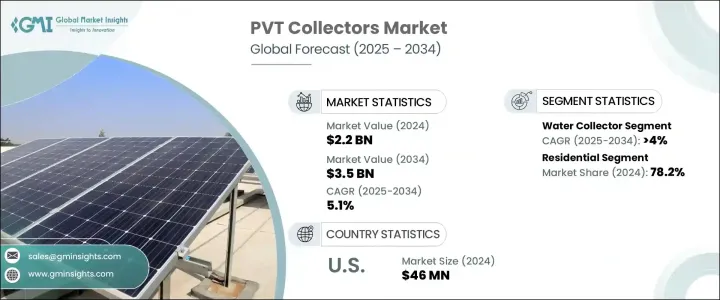

세계의 PVT 콜렉터 시장 규모는 2024년에는 22억 달러로 평가되었고, 2034년에는 35억 달러에 이를 것으로 예측되며, CAGR 5.1%로 성장할 전망입니다.

원격 및 독립형 지역에서의 하이브리드 태양열 에너지 시스템에 대한 수요가 증가하면서 전 세계적으로 PVT 콜렉터의 채택이 가속화되고 있습니다. 이 시스템은 태양광 및 열 기술을 단일 패널에 결합하여 전기와 열을 모두 제공합니다. 태양 에너지를 효율적으로 활용하는 PVT 수집기는 기존 연료 원에 대한 의존도를 줄여 비용 효율적이고 지속 가능한 에너지 솔루션을 제공합니다. 서비스가 부족한 지역에서 전기 공급이 확대됨에 따라, 특히 에너지 인프라가 제한적인 지역에서 이러한 수요가 더욱 촉진될 것으로 예상됩니다.

농촌의 전기 공급 외에도, 건물 에너지 관리에 대한 하이브리드 재생 가능 시스템에 대한 관심이 높아지면서 PVT 콜렉터의 사용이 더욱 확대되고 있습니다. 이러한 시스템은 토지 사용 및 설치 비용을 최소화하면서 이중 에너지 출력을 제공하는 공간 효율적인 설치를 가능하게 합니다. 도시 지역이 점점 혼잡해짐에 따라 최소한의 표면적으로 최대의 에너지를 생산할 수 있는 기술에 대한 관심이 높아지고 있습니다. PVT 콜렉터는 이러한 요구 사항을 잘 충족하여 인구 밀집 지역에 실용적인 솔루션을 제공합니다. 에너지 효율적이고 저공해 건축을 장려하는 규제가 강화됨에 따라, 정부도 PVT 시스템과 같은 통합 재생 가능 기술로의 전환을 촉진하는 데 중요한 역할을 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 22억 달러 |

| 예측 금액 | 35억 달러 |

| CAGR | 5.1% |

PVT 콜렉터가 히트 펌프와 같은 다른 친환경 기술과 통합이 진행되면서 시장 성장이 더욱 촉진되고 있습니다. 이러한 통합을 통해 가정용 온수 시스템과 공간 난방 솔루션 모두에서 에너지 효율이 향상됩니다. PVT 패널과 히트 펌프의 시너지 효과는 상당한 에너지 절약에 기여하여 성능 최적화와 비용 절감을 추구하는 주거 및 상업용 에너지 소비자에게 실행 가능한 옵션이 되고 있습니다. 이러한 통합 솔루션을 개발하는 기업과 기관이 증가함에 따라 시장 침투가 가속화될 것으로 예상됩니다.

시장 역학을 형성하는 또 다른 중요한 동향은 주거 및 상업용 건물에서 효율적인 저온 열에 대한 요구가 증가하고 있다는 것입니다. PVT 시스템은 이러한 요구를 충족하면서 단일 옥상 장치로 전기를 생산하는 추가적인 이점을 제공합니다. 분산형 에너지 시스템이 전 세계적으로 주목을 받으면서 PVT 콜렉터와 같은 이중 발전 장치가 높은 투자 수익률로 인해 점점 더 선호되고 있습니다. 이러한 시스템은 특히 옥상 공간이 제한된 도시 주거 공간에서 건물의 전반적인 에너지 성능을 향상시킵니다. 이러한 효율성은 건물 통합형 태양열 솔루션의 인기가 높아지는 데 기여하고 있으며, 특히 부동산 소유주와 개발업자들이 에너지 생산량을 저하시키지 않고 지속 가능성 목표를 달성할 방법을 모색하고 있기 때문에 그 인기가 더욱 높아지고 있습니다.

긍정적인 전망에도 불구하고, 일부 규제 및 정책 관련 문제가 업계에 영향을 미치고 있습니다. 태양 전지 및 열 장치와 같은 PVT 부품에 대한 높은 수입 관세는 시스템 가격을 상승시키고, 특히 수입 기술에 크게 의존하는 시장에서 채택을 늦추고 있습니다. 이러한 비용 장벽은 첨단 고효율 시스템에 대한 접근을 제한하고 대규모 프로젝트의 배포 일정을 연장하여 일부 지역의 성장을 잠재적으로 늦추고 있습니다.

제품 부문별로 PVT 콜렉터 시장은 물 콜렉터, 공기 콜렉터 및 집중 장치 시스템으로 분류됩니다. 이 중 물 수집기 부문은 2034년까지 연평균 4% 이상의 성장률을 보일 것으로 예상됩니다. 이 시스템은 다양한 기후 조건에서 안정적인 열 출력을 제공하기 때문에 선진국과 개발도상국 모두에서 널리 채택되고 있습니다. 에너지 절약 노력이 호환되기 때문에 장기적인 탈탄소화를 목표로 하는 기관 및 기업에 선호되는 옵션입니다.

미국에서 PVT 콜렉터 시장은 꾸준한 성장을 보이며 2023년 4,300만 달러, 2022년 4,100만 달러에서 2024년에는 4,600만 달러로 성장할 것으로 예상됩니다. 북미는 현재 세계 시장의 2.3%를 차지하고 있으며, 이 수치는 2034년까지 꾸준히 증가할 것으로 예상됩니다. 미국 여러 주에서 높은 전기 요금이 소비자들이 유틸리티 비용을 절감하고 전력망 의존도를 낮추기 위해 PVT 시스템과 같은 대체 에너지 원을 모색하도록 촉진하고 있습니다.

업계 선두 기업들은 세계 시장 점유율의 약 39.5%를 차지하고 있습니다. 이 기업들은 연구개발(R&D)부터 제조, 설치, 서비스까지 모든 과정을 통합 관리하는 수직 통합 전략을 통해 경쟁 우위를 유지하고 있습니다. 건설 및 HVAC 기업과의 파트너십은 시스템 호환성을 확보하고 성능을 최적화하는 데 기여합니다. R&D에 대한 대규모 투자는 에너지 출력이 우수하고 고급 모니터링 기술을 갖춘 신세대 PVT 패널의 출시로 이어졌습니다. 이러한 기술 발전은 시스템 효율성을 향상시킬 뿐만 아니라 전 세계적으로 확산되는 지속 가능하고 탄소 중립적인 건물 건설에 부합합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 에코시스템

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율

- 전략적 대시보드

- 전략적 노력

- 경쟁 벤치마킹

- 혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 유형별(2021-2034년)

- 주요 동향

- 물 콜렉터

- 커버 첨부

- 커버 없음

- 진공관

- 공기 콜렉터

- 집중 장치

제6장 시장 규모와 예측 : 용도별(2021-2034년)

- 주요 동향

- 주거

- 상업

제7장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 이탈리아

- 그리스

- 폴란드

- 프랑스

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 중동 및 북아프리카

- 이스라엘

- 요르단

- 레바논

- 모로코

- 세계 기타 지역

제8장 기업 프로파일

- Abora Solar

- Balkansolar

- Dualsun

- Naked Energy

- NIBE Energy

- PowerPanel

- SolarPower

- Solimpeks

- SunEarth

- Sunmaxx

The Global Photovoltaic Thermal Collectors Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 3.5 billion by 2034. Increasing demand for hybrid solar energy systems in remote and off-grid locations is accelerating the adoption of PVT collectors worldwide. These systems combine photovoltaic and thermal technologies into a single panel, offering both electricity and heat. By efficiently utilizing solar energy, PVT collectors help reduce reliance on conventional fuel sources, offering cost-effective and sustainable energy solutions. Growing electrification initiatives in underserved areas are expected to further drive this demand, particularly in regions with limited energy infrastructure.

In addition to rural electrification, growing interest in hybrid renewable systems in building energy management is encouraging the broader use of PVT collectors. These systems allow for space-efficient installations that deliver dual energy outputs while minimizing land use and installation costs. As urban areas become more congested, there is an increasing focus on technologies that enable maximum energy generation from minimal surface area. PVT collectors fit this requirement well, offering a practical solution for densely populated areas. With stricter regulations encouraging energy-efficient and low-emission building practices, governments are also playing a key role in driving the shift toward integrated renewable technologies like PVT systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.5 Billion |

| CAGR | 5.1% |

Market growth is being further stimulated by the increasing integration of PVT collectors with other green technologies, such as heat pumps. The combination enables greater energy efficiency in both domestic hot water systems and space heating solutions. The synergy between PVT panels and heat pumps contributes to notable energy savings, making it a viable option for both residential and commercial energy consumers seeking performance optimization and cost reduction. As more companies and institutions develop these integrated solutions, market penetration is expected to accelerate.

Another important trend shaping market dynamics is the rising need for efficient low-temperature heat in residential and commercial buildings. PVT systems can meet this demand while offering the added benefit of electricity generation, all from a single rooftop unit. As decentralized energy systems gain traction globally, dual-generation units like PVT collectors are increasingly preferred for their high return on investment. These systems enhance overall building energy performance, especially in urban residential spaces where rooftop space is limited. This efficiency is contributing to the growing popularity of building-integrated solar solutions, especially as property owners and developers seek ways to meet sustainability targets without compromising on energy output.

Despite the positive outlook, some regulatory and policy-related challenges are impacting the industry. High import duties on PVT components such as solar cells and thermal units have increased system prices and slowed adoption, especially in markets heavily dependent on imported technology. This cost barrier limits access to advanced, high-efficiency systems and extends the deployment timeline for larger projects, potentially slowing growth in some regions.

In terms of product segmentation, the PVT collectors market is categorized into water collectors, air collectors, and concentrator systems. Among these, the water collectors segment is projected to expand at a CAGR exceeding 4% through 2034. These systems are gaining popularity for their ability to deliver reliable thermal output in a wide range of climatic conditions, supporting broader adoption in both developed and developing markets. Their compatibility with energy-saving initiatives makes them a preferred option for institutions and enterprises targeting long-term decarbonization.

By application, the market is split between residential and commercial sectors. The residential segment accounted for a dominant 78.2% share of global revenue in 2024. This strong presence is due to the increasing burden of utility bills and a rising preference among homeowners for energy self-sufficiency. The compact design and dual-energy output make PVT systems ideal for residential buildings, especially in urban areas where space is limited. Government-backed incentives and rebate programs for solar technology adoption further encourage household-level installations, reinforcing the growth of this segment.

In the United States, the PVT collectors market has shown steady growth, reaching USD 46 million in 2024, up from USD 43 million in 2023 and USD 41 million in 2022. North America currently holds a 2.3% share of the global market, a figure expected to rise steadily through 2034. High electricity prices in several US states are driving consumers to explore alternative energy sources like PVT systems to cut down on utility costs and reduce grid dependency.

Leading players in the industry collectively account for around 39.5% of the global market share. These companies maintain competitive advantages through vertical integration, managing everything from R&D and manufacturing to installation and service. Their partnerships with construction and HVAC firms further enhance their market position, ensuring seamless system compatibility and optimized performance. Heavy investment in R&D has led to the rollout of new-generation PVT panels that offer superior energy output and are equipped with advanced monitoring technologies. These developments not only improve system efficiency but also align with growing global commitments to sustainable, net-zero energy buildings.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Type, 2021 - 2034 (USD Million, m2 & MW)

- 5.1 Key trends

- 5.2 Water collectors

- 5.2.1 Covered

- 5.2.2 Uncovered

- 5.2.3 Evacuated tube

- 5.3 Air collectors

- 5.4 Concentrators

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million, m2 & MW)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, m2 & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Greece

- 7.3.4 Poland

- 7.3.5 France

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.5 Middle East & North Africa

- 7.5.1 Israel

- 7.5.2 Jordan

- 7.5.3 Lebanon

- 7.5.4 Morocco

- 7.6 Rest of World

Chapter 8 Company Profiles

- 8.1 Abora Solar

- 8.2 Balkansolar

- 8.3 Dualsun

- 8.4 Naked Energy

- 8.5 NIBE Energy

- 8.6 PowerPanel

- 8.7 SolarPower

- 8.8 Solimpeks

- 8.9 SunEarth

- 8.10 Sunmaxx