|

시장보고서

상품코드

1750497

일회용 수술기구 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Disposable Surgical Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

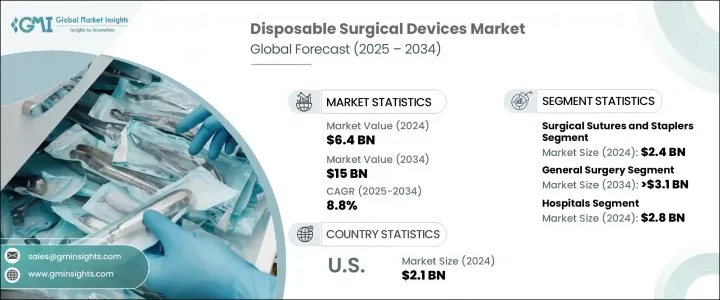

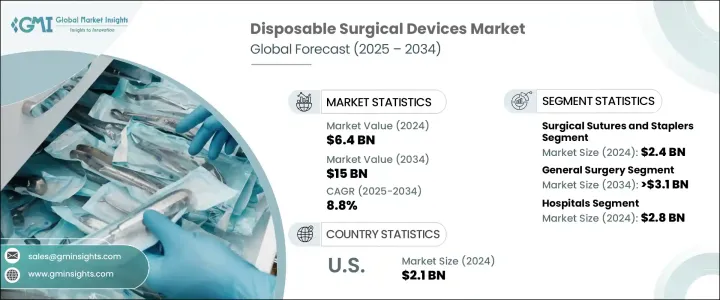

세계의 일회용 수술기구 시장은 2024년에는 64억 달러로 평가되었고, 수술 건수 증가, 감염 방지 대책 강화, 저침습 수술에 대한 세계 선호도 증가 등을 배경으로 CAGR 8.8%로 성장할 전망이며, 2034년에는 150억 달러에 달할 것으로 예측되고 있습니다.

일회용 기구는 효율성, 사용 편의성, 무균 상태를 유지하는 능력으로부터 지지를 모으고 있습니다. 선진 경제국 및 신흥 경제국의 헬스케어 시스템이 업무의 합리화 및 2차 오염의 리스크 경감에 임하는 가운데, 일회용 수술기구는 최우선 사항이 되고 있습니다. 자동화와 인체공학적으로 첨단 툴로의 전환은, 특히 높은 처리량의 의료 현장에서 채용을 한층 더 뒷받침하고 있습니다.

팬데믹 이후 헬스케어 제공업체는 보다 엄격한 감염 관리 정책을 준수합니다. 이 때문에 특히 선택적 수술과 긴급 수술의 수가 증가함에 따라 일회용 수술 솔루션으로의 전환이 가속화됩니다. 이러한 기구는 위생 측면에서 명확한 이점을 제공하고 멸균 단계를 생략하며 수술실에서의 턴어라운드 타임을 단축합니다. 일회용을 상정하여 설계된 이 기구들은 속도와 환자의 안전성이 모두 요구되는 수술환경에서 필수적인 것이 되고 있습니다. 기본적인 툴부터 고도의 스테이플러나 트랙커까지 디스포저블은 손기술의 일관성을 향상시키면서 무균 상태를 확보합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 64억 달러 |

| 예측 금액 | 150억 달러 |

| CAGR | 8.8% |

제품 유형별로 수술용 봉합사와 스테이플러 부문이 2024년에 24억 달러로 시장을 선도했습니다. 봉합사와 스테이플러는 기존의 수술 및 저침습 수술 모두에서 일관되게 사용되고 있기 때문에 없어서는 안 되는 것으로 되어 있습니다. 이 도구들은 창상 관리에 도움을 주고 적절한 창상 봉합을 보장하며 감염을 최소화하고 조기 회복을 돕습니다. 인체공학적 디자인, 매듭이 필요 없는 유자봉합사, 항균코팅 등의 기술혁신으로 안전성과 효율성이 크게 향상되어 정상급의 실적을 자랑하는 제품 카테고리가 되고 있습니다.

일반 수술 분야는 2034년까지 31억 달러에 달할 전망이며, CAGR 8.5%를 보일 것으로 예측됩니다. 이 분야에서는 여러 수술이 진행되어 일회용 수술기구의 안정적인 수요에 기여하고 있습니다. 외래 환자나 입원 환자의 개입률 증가, 만성 질환 및 급성 질환의 유병률 증가가 이러한 기구의 수요를 끌어올리고 있습니다. 의료기관은 특히 대량생산 환경에서 안전 준수와 환자 케어의 합리화를 위해 일회용 수술기구에 의존하고 있습니다.

미국의 일회용 수술기구 2024년 시장 규모는 20억 달러에 달했으며, CAGR 7.7%로 성장할 전망입니다. 강력한 규제의 틀, 세련된 헬스케어 인프라, 유리한 상환 모델 모두가 일회용 기구의 급속한 보급을 뒷받침하고 있습니다. 또한 미국에 본사를 둔 대형 의료기기 업체들이 계속해서 시장을 견인하고 있습니다.

이 시장의 주요 기업는 Smith Nephew, CooperSurgical, Xenco Medical, BD, Johnson & Johnson, ZIMMER BIOMET, B Braun, Medtronic, Ambu, Surgical Innovations, Accutome, Boston Scientific 등이 있습니다. 발판을 굳히기 위해 각사는 사용의 용이성, 안전성, 성능을 높이기 위한 연구개발 투자를 통해 기술 혁신을 우선하고 있습니다. 항균 코팅이나 매듭 없는 봉합사 등 스마트한 기능을 갖춘 제품 포트폴리오를 확충하고 있는 기업도 많습니다. 병원이나 수술 센터와의 전략적 제휴도 공급 계약의 확보나 시장 침투의 심화에 도움이 되고 있습니다. 게다가 제조업체 각사는, 비용 효율을 유지하면서 증대하는 수요에 대응하기 위해, 자동화와 정밀 제조를 활용해, 세계 시장에서의 경쟁력을 높이고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 수술 건수 증가

- 급속한 기술 혁신

- 일회용 기기를 우선하는 엄격한 감염 관리 기준

- 저침습 수술에 대한 관심 증가

- 업계의 잠재적 위험 및 과제

- 환경의 지속가능성에 대한 우려

- 비용 및 상환의 장벽

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망 및 향후 검토 사항

- 무역에 미치는 영향

- 기술의 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 수술용 봉합사 및 스테이플러

- 휴대용 수술용 기기

- 일회용 내시경 장치

- 전기 수술용 장비

제6장 시장 추계 및 예측 : 순서별(2021-2034년)

- 주요 동향

- 일반 외과

- 성형외과 및 재건외과

- 정형외과

- 심장혈관 수술

- 뇌신경외과

- 산부인과

- 상처 폐쇄

- 기타 절차

제7장 시장 추계 및 예측 : 최종 용도별 2021-2034

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 전문 클리닉

- 기타 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Accutome

- Ambu

- B Braun

- BD

- Boston Scientific

- CooperSurgical

- Johnson & Johnson

- Medtronic

- Smith Nephew

- Surgical Innovations

- Xenco Medical

- ZIMMER BIOMET

The Global Disposable Surgical Devices Market was valued at USD 6.4 billion in 2024 and is estimated to grow at a CAGR of 8.8% to reach USD 15 billion by 2034, driven by increasing surgical volumes, heightened infection control measures, and the rising global preference for minimally invasive procedures. Disposable instruments are gaining traction due to their efficiency, ease of use, and ability to maintain sterile conditions. As healthcare systems across developed and emerging economies look to streamline operations and reduce the risk of cross-contamination, single-use surgical tools are becoming a top priority. The shift toward automation and ergonomically advanced tools further supports adoption, particularly in high-throughput medical settings.

In the wake of the pandemic, healthcare providers adhere to stricter infection control policies. This has accelerated the move toward disposable surgical solutions, particularly as the number of elective and emergency procedures rebounds. These instruments offer clear benefits in hygiene, eliminate sterilization steps, and reduce turnaround times in operating rooms. Designed for single-use scenarios, they are proving vital in surgical environments that demand both speed and patient safety. From basic tools to advanced staplers and trocars, disposables ensure sterile conditions while improving procedural consistency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.4 Billion |

| Forecast Value | $15 Billion |

| CAGR | 8.8% |

Among product types, the surgical sutures and staplers segment led the market with USD 2.4 billion in 2024. Their consistent usage in both traditional and minimally invasive procedures makes them indispensable. These tools help in wound management, ensuring proper closure, minimizing infections, and aiding faster recovery. Innovations like ergonomic designs, barbed sutures requiring no knots, and antimicrobial coatings have significantly enhanced their safety and efficiency, making them the top-performing product category.

The general surgery segment is projected to reach USD 3.1 billion by 2034, growing at a CAGR of 8.5%. This category covers several procedures, contributing to consistent demand for disposable surgical tools. The increasing rate of outpatient and inpatient interventions, along with the growing prevalence of chronic and acute conditions, is boosting demand for these devices. Medical institutions rely on single-use surgical tools for safety compliance and streamlined patient care, especially in high-volume environments.

U.S. Disposable Surgical Devices Market accounted for USD 2 billion in 2024 and is expected to grow at a CAGR of 7.7%. A strong regulatory framework, sophisticated healthcare infrastructure, and favorable reimbursement models all support rapid adoption of disposable instruments. Additionally, major medical device companies headquartered in the U.S. continue to drive market momentum.

Key players in this market include Smith+Nephew, CooperSurgical, Xenco Medical, BD, Johnson & Johnson, ZIMMER BIOMET, B Braun, Medtronic, Ambu, Surgical Innovations, Accutome, and Boston Scientific. To strengthen their foothold, companies prioritize innovation through R&D investments to enhance usability, safety, and performance. Many are expanding product portfolios with smart features such as antimicrobial coatings and knotless sutures. Strategic collaborations with hospitals and surgical centers are also helping secure supply contracts and deepen market penetration. Furthermore, manufacturers leverage automation and precision manufacturing to meet growing demand while maintaining cost-efficiency, enhancing their competitive edge across global markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global surgical volume

- 3.2.1.2 Rapid technological innovation

- 3.2.1.3 Stringent infection control standards favoring disposable devices

- 3.2.1.4 Rising preference for minimally invasive procedures

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental sustainability concerns

- 3.2.2.2 Cost and reimbursement barriers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Retaliatory measures

- 3.5.2 Impact on the Industry

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (selling price)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (raw materials)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Surgical sutures and staplers

- 5.3 Handheld surgical devices

- 5.4 Disposable endoscopy devices

- 5.5 Electrosurgical devices

Chapter 6 Market Estimates and Forecast, By Procedure, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Plastic and reconstructive Surgery

- 6.4 Orthopedic surgery

- 6.5 Cardiovascular surgery

- 6.6 Neurosurgery

- 6.7 Obstetrics and gynecology

- 6.8 Wound closure

- 6.9 Other procedures

Chapter 7 Market Estimates and Forecast, By End Use 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accutome

- 9.2 Ambu

- 9.3 B Braun

- 9.4 BD

- 9.5 Boston Scientific

- 9.6 CooperSurgical

- 9.7 Johnson & Johnson

- 9.8 Medtronic

- 9.9 Smith+Nephew

- 9.10 Surgical Innovations

- 9.11 Xenco Medical

- 9.12 ZIMMER BIOMET