|

시장보고서

상품코드

1750498

부패하지 않는 우유 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Non-Perishable Milk Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

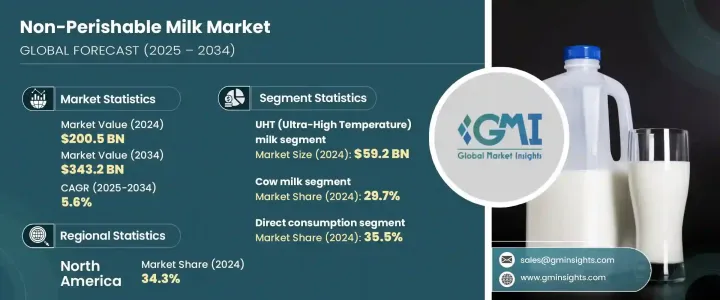

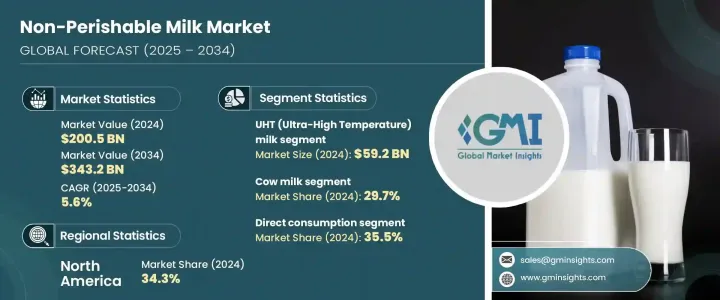

세계의 부패하지 않는 우유 시장은 2024년에는 2,005억 달러로 평가되었고 CAGR 5.6%를 나타내 2034년까지는 3,432억 달러에 이를 것으로 추정됩니다.

이 성장의 주요 요인은 보존 기간이 길고 냉장의 필요성이 적은 유제품에 대한 수요 증가입니다. 소비자는 편의성, 영양가, 보다 긴 사용기간을 제공하는 선택지에 매료되고 있습니다.

시장은 강화 우유, 유기 우유 및 무유당 우유에 대한 관심 증가에 의해 형성되고 있습니다. 기술 혁신, 특히 가공 방법도 시장 확대에 기여하고 있습니다. 무결성, 품질 및 내구성이 향상되었습니다. 이러한 요인으로 인해 특히 냉장품에 대한 접근이 제한된 지역에서보다 광범위한 유통과 소비 확대가 가능해지고 있습니다. 풍부한 식생활에 대한 의식이 높아져 우유의 소비 패턴이 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 2,005억 달러 |

| 예측 금액 | 3,432억 달러 |

| CAGR | 5.6% |

시장 세분화는 UHT 우유, 증발 우유, 가당 연유, 밀가루 우유 등을 포함합니다. 도시에서도 농촌에서도 선호되는 선택지가 되고 있습니다. 분유와 증발우유도 또한, 특히 저렴한 가격과 장기 보존이 불가결한 경우에 자주 이용되고 있습니다.

소스별로 평가하면 시장은 우유, 염소 우유, 물 우유, 식물성 우유 등으로 구분됩니다. 이점으로 곧바로 사용할 수 있는 유제품의 선택지를 요구하는 현재의 소비자 수요에 잘 합치하고 있습니다.

부패하지 않는 우유 유통 채널에는 슈퍼마켓 하이퍼마켓, 전문점, 편의점, 온라인 소매, 외식점포, B2B 직접 판매 등이 포함됩니다. 슈퍼마켓 및 하이퍼마켓의 인기는 폭넓은 물건 세트의 상품을 한곳에서 제공할 수 있는 것으로부터, 일상적으로 이용하는 소비자에게 선택되고 있는 것에 기인하고 있습니다. 전문점은 특히 건강 지향이나 식물 유래의 우유 등 프리미엄인 상품을 제공하는 것으로 점점 지지되어 편의점은 싱글서브와 온더고 형식 수요를 충족하는데 있어 중요한 역할을 하고 있습니다. 기업에 직접 판매는 특히 시설과 상업 부문에서 계속 견조합니다.

지역별로는 북미가 2024년 부패하지 않는 우유 시장에서 최대의 점유율을 차지해 총 매출의 34.3%를 차지했습니다. 이 지역 시장에서는 소비자의 라이프 스타일의 진화와 보존 가능한 영양 옵션에 관심 증가함에 따라 UHT 우유 및 기타 장기 보존 가능한 유제품의 채용이 증가하고 있습니다.

Lactalis International, Nestle SA, Fonterra Co-operative Group Limited, Danone SA, Arla Foods와 같은 주요 업계 기업이 시장 성장의 견인 역할을 하고 있습니다. 그들의 영향력은 기술 혁신, 가공 기술, 세계의 유통 능력에 있어서 특히 현저합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 제조업체

- 유통업체

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 공급측의 영향(원재료)

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 공급자의 상황

- 이익률 분석

- 주요 뉴스와 대처

- 규제 프레임워크과 기준

- 식품안전규제

- 라벨 요건

- 품질 기준

- 수출입 규제

- 오가닉 및 클린 라벨 인증

- 영향요인

- 성장 촉진요인

- 도시화와 라이프스타일의 진화

- 가공과 포장에 있어서 기술의 진보

- 소매업 확대와 정부의 지원

- 업계의 잠재적 리스크 및 과제

- 공급망의 혼란

- 경제 불확실성

- 시장 기회

- 성장 촉진요인

- 제품 개요

- 부패하지 않는 우유 가공 기술

- 유통기한 연장방법

- 영양 프로파일의 비교

- 감각 특성

- 제조 공정 분석

- UHT 처리

- 증발과 응축

- 스프레이 건조

- 무균 포장

- 품질 관리 프로세스

- 원재료 분석 및 조달 전략

- 가격 분석

- 지속가능성과 환경영향 평가

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 시장 점유율 분석

- 전략 틀

- 합병 및 인수

- 합작투자와 콜라보레이션

- 신제품 개발

- 확대 전략

- 경쟁 벤치마킹

- 벤더 상황

- 경쟁 포지셔닝 매트릭스

- 전략적 대시보드

- 브랜드 포지셔닝과 소비자 인식 분석

- 신규 참가자 시장 진출 전략

- 비공개 라벨 분석 및 전략

제5장 시장 추계·예측 : 제품 유형별(2021-2034년)

- 주요 동향

- UHT(초고온) 우유

- 전유 UHT 우유

- 반탈지 UHT 우유

- 탈지 UHT 우유

- 향이 첨가된 UHT 우유

- 증발 우유

- 전체 증발 우유

- 탈지 증발 우유

- 기타

- 가당 연유

- 일반 가당 연유

- 향이 가미된 가당 연유

- 기타

- 가당 연유

- 일반 가당 연유

- 향이 가미된 가당 연유

- 기타

- 분유

- 전유 분유

- 탈지 분유

- 지방이 함유된 분유

- 유아용 조제 분유

- 기타

- 기타

제6장 시장 추계·예측 : 원료별(2021-2034년)

- 주요 동향

- 젖소 우유

- 염소 우유

- 물소 우유

- 식물성 대체품

- 두유

- 아몬드 우유

- 귀리 우유

- 코코넛 우유

- 기타

- 기타

제7장 시장 추계·예측 : 지방 함유량별(2021-2034년)

- 주요 동향

- 통지방/전지방(지방분 3.5% 이상)

- 반탈지/저지방(지방분 1.5-1.8%)

- 탈지/저지방(지방분 0.5% 미만)

- 무지방(지방 0%)

- 지방 함유량의 변동

제8장 시장 추계·예측 : 포장 형태별(2021-2034년)

- 주요 동향

- 테트라팩/무균 상자

- 벽돌 상자

- 박송 상단 상자

- 기타

- 캔

- 강철 캔

- 알루미늄 캔

- 병

- 유리 병

- 플라스틱 병

- 파우치

- 백 인 박스

- 통 및 봉지(분유용)

- 기타

제9장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 슈퍼마켓 및 하이퍼마켓

- 전문점

- 편의점

- 온라인 소매

- 기업 웹사이트

- 전자상거래 플랫폼

- 구독 서비스

- 푸드서비스

- 호텔 및 레스토랑

- 카페 및 베이커리

- 기관 케이터링

- 직접 판매(B2B)

- 기타

제10장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 직접 소비

- 식품 가공

- 베이커리 및 제과류

- 유제품

- 유아식

- 조리된 식품

- 기타

- 음료업계

- 커피 및 차

- 스무디 및 쉐이크

- 기타

- 식품 서비스 산업

- 영양보조식품

- 기타

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제12장 기업 프로파일

- Nestle SA

- Danone SA

- Lactalis Group

- Fonterra Co-operative Group Limited

- FrieslandCampina

- Arla Foods amba

- Dean Foods(Dairy Farmers of America)

- Saputo Inc.

- Parmalat SpA(Lactalis)

- Amul(Gujarat Cooperative Milk Marketing Federation)

- China Mengniu Dairy Company Limited

- Inner Mongolia Yili Industrial Group Co. Ltd.

- Morinaga Milk Industry Co.Ltd.

- Meiji Holdings Co.Ltd.

- Savencia Fromage &Dairy

- DMK Deutsches Milchkontor GmbH

- Muller Group

- Dairy Farmers of America, Inc.

- Almarai Company

- Grupo LALA

- Vinamilk(Vietnam Dairy Products JSC)

- Borden Dairy Company

- Dairy Partners Americas(DPA)

- Darigold, Inc.

- California Dairies, Inc.

- Sodiaal

- Glanbia plc

- Schreiber Foods Inc.

- Land O'Lakes, Inc.

- Dairy Crest Group plc(Saputo)

The Global Non-Perishable Milk Market was valued at USD 200.5 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 343.2 billion by 2034. This growth is largely fueled by the increasing demand for milk products with extended shelf life and minimal refrigeration requirements. Non-perishable milk has evolved from being a practical option in regions lacking cold storage to a mainstream choice worldwide. Consumers are gravitating toward options that offer convenience, nutritional value, and longer usability. With rising urbanization and shifting dietary preferences, the industry continues to expand its reach across diverse consumer groups.

The market has been shaped by growing interest in fortified, organic, and lactose-free milk variants. These preferences are reshaping product development strategies as manufacturers respond to changing health and lifestyle trends. Technological innovations, especially in processing methods, are also contributing to market expansion. Advancements in Ultra-High Temperature (UHT) treatment and high-temperature short-time (HTST) techniques, combined with aseptic packaging, have improved the safety, quality, and durability of non-perishable milk. These factors are enabling broader distribution and increased consumption, especially in areas with limited access to refrigerated goods. In parallel, there's a rise in awareness regarding calcium-rich diets, which plays into higher milk consumption patterns. Even plant-based alternatives are gaining space in the non-perishable segment, reflecting evolving consumer priorities toward sustainability and wellness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $200.5 Billion |

| Forecast Value | $343.2 Billion |

| CAGR | 5.6% |

In terms of product segmentation, the non-perishable milk market includes UHT milk, evaporated milk, sweetened condensed milk, powdered milk, and others. Among these, UHT milk led the category in 2024 with a market share of 29.5%, representing USD 59.2 billion. Its dominance is attributed to its versatility and ability to remain fresh without refrigeration for extended periods, making it a preferred option in both urban and rural settings. Powdered and evaporated variants are also well-established, particularly where affordability and long-term storage are essential. Sweetened condensed milk maintains its relevance in culinary applications, though health concerns are slightly dampening its growth rate in some areas.

When evaluated by source, the market is segmented into cow milk, goat milk, buffalo milk, plant-based milk, and others. Cow milk accounted for 29.7% of the total market in 2024 and is expected to grow at a CAGR of 5.3% through 2034. Its continued popularity is supported by its availability in UHT and powdered forms, which align well with current consumer demands for convenient, ready-to-use dairy options. Goat milk is steadily gaining traction among consumers seeking lactose-intolerant-friendly or easily digestible alternatives. Meanwhile, buffalo milk retains niche appeal due to its higher fat content and regional preferences.

Distribution channels for non-perishable milk include supermarkets and hypermarkets, specialty stores, convenience stores, online retail, food service outlets, direct B2B sales, and others. Supermarkets and hypermarkets commanded the largest share of the market in 2024, accounting for 31.5%. Their popularity stems from their ability to offer a wide selection of products in one location, making them a go-to choice for everyday consumers. Specialty stores are increasingly favored for premium offerings, especially for health-centric or plant-based milk variants. Convenience stores play a key role in fulfilling demand for single-serve or on-the-go formats. Online retail is experiencing rapid growth, driven by the convenience of doorstep delivery and the expansion of e-commerce platforms. Food service channels continue to rely on UHT and powdered milk for consistent supply and ease of storage. Direct sales to businesses remain robust, particularly in institutional and commercial sectors. Additional distribution methods include vending and export-focused channels that are helping brands tap into untapped markets.

Regionally, North America held the largest share of the non-perishable milk market in 2024, contributing 34.3% of the total revenue. The regional market has seen increasing adoption of UHT milk and other long-lasting dairy products, thanks to evolving consumer lifestyles and greater interest in shelf-stable nutrition options. Europe follows closely with a strong preference for UHT milk due to its convenience and reduced reliance on cold chains.

Major industry players such as Lactalis International, Nestle S.A., Fonterra Co-operative Group Limited, Danone S.A., and Arla Foods are instrumental in driving market growth. Their influence is particularly evident in innovation, processing technology, and global distribution capabilities. These companies are consistently investing in product development and expanding their presence to meet the growing global demand for non-perishable milk products.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Methodology and scope

- 1.2 Research methodology

- 1.3 Research scope & assumptions

- 1.4 List of data sources

- 1.5 Market estimation technique

- 1.6 Research limitations

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Manufacturers

- 3.1.4 Distributors

- 3.1.5 Impact on trade

- 3.1.6 Trade volume disruptions

- 3.2 Retaliatory measures

- 3.3 Impact on the industry

- 3.3.1 Supply-side impact (Raw Materials)

- 3.3.1.1 Price volatility in key materials

- 3.3.1.2 Supply chain restructuring

- 3.3.1.3 Production cost implications

- 3.3.1 Supply-side impact (Raw Materials)

- 3.4 Demand-side impact (Selling Price)

- 3.4.1 Price transmission to end markets

- 3.4.2 Market share dynamics

- 3.4.3 Consumer response patterns

- 3.5 Key companies impacted

- 3.6 Strategic industry responses

- 3.6.1 Supply chain reconfiguration

- 3.6.2 Pricing and product strategies

- 3.6.3 Policy engagement

- 3.7 Outlook and future considerations

- 3.8 Supplier landscape

- 3.9 Profit margin analysis

- 3.10 Key news & initiatives

- 3.11 Regulatory framework and standards

- 3.11.1 Food safety regulations

- 3.11.2 Labeling requirements

- 3.11.3 Quality standards

- 3.11.4 Import/export regulations

- 3.11.5 Organic & clean label certifications

- 3.12 Impact forces

- 3.12.1 Growth drivers

- 3.12.1.1 Urbanization and evolving lifestyles

- 3.12.1.2 Technological advancements in processing and packaging

- 3.12.1.3 Retail expansion and government support

- 3.12.2 Industry pitfalls & challenges

- 3.12.2.1 Supply chain disruptions

- 3.12.2.2 Economic uncertainty

- 3.12.3 Market opportunities

- 3.12.1 Growth drivers

- 3.13 Product overview

- 3.13.1 Nonperishable milk processing technologies

- 3.13.2 Shelf-life extension methods

- 3.13.3 Nutritional profile comparison

- 3.13.4 Sensory characteristics

- 3.14 Manufacturing process analysis

- 3.14.1 UHT processing

- 3.14.2 Evaporation & Condensation

- 3.14.3 Spray drying

- 3.14.4 Aseptic packaging

- 3.14.5 Quality control processes

- 3.15 Raw material analysis & procurement strategies

- 3.16 Pricing analysis

- 3.17 Sustainability & environmental impact assessment

- 3.18 Growth potential analysis

- 3.19 Porter's analysis

- 3.20 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Market share analysis

- 4.3 Strategic framework

- 4.3.1 Mergers & acquisitions

- 4.3.2 Joint ventures & collaborations

- 4.3.3 New product developments

- 4.3.4 Expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Vendor landscape

- 4.6 Competitive positioning matrix

- 4.7 Strategic dashboard

- 4.8 Brand positioning & consumer perception analysis

- 4.9 Market entry strategies for new players

- 4.10 Private label analysis & strategies

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 UHT (Ultra-High Temperature) milk

- 5.2.1 Whole UHT milk

- 5.2.2 Semi-skimmed UHT milk

- 5.2.3 Skimmed UHT milk

- 5.2.4 Flavored UHT milk

- 5.3 Evaporated milk

- 5.3.1 Whole evaporated milk

- 5.3.2 Skimmed evaporated milk

- 5.3.3 Others

- 5.4 Sweetened condensed milk

- 5.4.1 Regular sweetened condensed milk

- 5.4.2 Flavored sweetened condensed milk

- 5.4.3 Others

- 5.5 Sweetened condensed milk

- 5.5.1 Regular sweetened condensed milk

- 5.5.2 Flavored sweetened condensed milk

- 5.5.3 Others

- 5.6 Powdered milk

- 5.6.1 Whole milk powder

- 5.6.2 Skimmed milk powder

- 5.6.3 Fat-filled milk powder

- 5.6.4 Infant formula

- 5.6.5 Others

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Source, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cow milk

- 6.3 Goat milk

- 6.4 Buffalo milk

- 6.5 Plant-based alternatives

- 6.5.1 Soy milk

- 6.5.2 Almond milk

- 6.5.3 Oat milk

- 6.5.4 Coconut milk

- 6.5.5 Others

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Fat Content, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Whole/full fat (≥3.5% Fat)

- 7.3 Semi-skimmed/reduced fat (1.5-1.8% Fat)

- 7.4 Skimmed/low fat (≤0.5% Fat)

- 7.5 Fat-free (0% Fat)

- 7.6 Variable fat content

Chapter 8 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Tetra packs/aseptic cartons

- 8.2.1 Brick cartons

- 8.2.2 Gable top cartons

- 8.2.3 Others

- 8.3 Cans

- 8.3.1 Steel cans

- 8.3.2 Aluminum cans

- 8.4 Bottles

- 8.4.1 Glass bottles

- 8.4.2 Plastic bottles

- 8.5 Pouches

- 8.6 Bag-in-box

- 8.7 Tins & sachets (for Powdered Milk)

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Supermarkets & hypermarkets

- 9.3 Specialty stores

- 9.4 Convenience stores

- 9.5 Online retail

- 9.5.1 Company websites

- 9.5.2 E-commerce platforms

- 9.5.3 Subscription services

- 9.6 Foodservice

- 9.6.1 Hotels & restaurants

- 9.6.2 Cafes & bakeries

- 9.6.3 Institutional catering

- 9.7 Direct sales (B2B)

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Direct consumption

- 10.3 Food processing

- 10.3.1 Bakery & confectionery

- 10.3.2 Dairy products

- 10.3.3 Infant food

- 10.3.4 Prepared foods

- 10.3.5 Others

- 10.4 Beverage industry

- 10.4.1 Coffee & tea

- 10.4.2 Smoothies & shakes

- 10.4.3 Others

- 10.5 Food service industry

- 10.6 Nutritional supplements

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.3.7 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 Nestle S.A.

- 12.2 Danone S.A.

- 12.3 Lactalis Group

- 12.4 Fonterra Co-operative Group Limited

- 12.5 FrieslandCampina

- 12.6 Arla Foods amba

- 12.7 Dean Foods (Dairy Farmers of America)

- 12.8 Saputo Inc.

- 12.9 Parmalat S.p.A. (Lactalis)

- 12.10 Amul (Gujarat Cooperative Milk Marketing Federation)

- 12.11 China Mengniu Dairy Company Limited

- 12.12 Inner Mongolia Yili Industrial Group Co., Ltd.

- 12.13 Morinaga Milk Industry Co., Ltd.

- 12.14 Meiji Holdings Co., Ltd.

- 12.15 Savencia Fromage & Dairy

- 12.16 DMK Deutsches Milchkontor GmbH

- 12.17 Muller Group

- 12.18 Dairy Farmers of America, Inc.

- 12.19 Almarai Company

- 12.20 Grupo LALA

- 12.21 Vinamilk (Vietnam Dairy Products JSC)

- 12.22 Borden Dairy Company

- 12.23 Dairy Partners Americas (DPA)

- 12.24 Darigold, Inc.

- 12.25 California Dairies, Inc.

- 12.26 Sodiaal

- 12.27 Glanbia plc

- 12.28 Schreiber Foods Inc.

- 12.29 Land O'Lakes, Inc.

- 12.30 Dairy Crest Group plc (Saputo)