|

시장보고서

상품코드

1871323

두개악안면 장치 시장 : 기회, 성장 요인, 업계 동향 분석, 예측(2025-2034년)Craniomaxillofacial Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

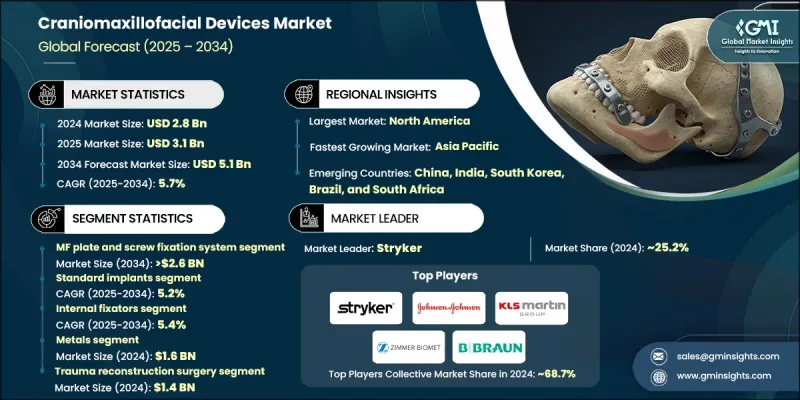

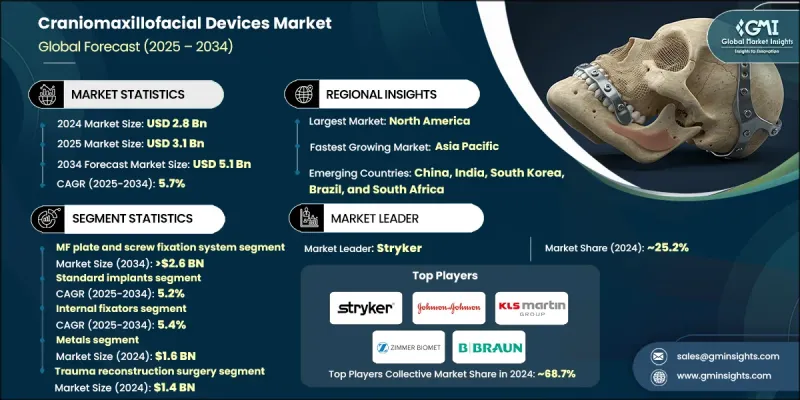

세계의 두개악안면 장치 시장은 2024년에 28억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5.7%로 성장해 51억 달러에 이를 것으로 예측되고 있습니다.

시장 성장의 배경에는 교통 사고, 스포츠 관련 사고, 폭력 사건으로 인한 안면 손상 증가가 있으며, 이는 재건 수술 수요를 촉진하고 있습니다. 또한 소아의 선천성 안면 기형도 소아 외과 수술에 있어서의 두개악안면 장치 수요 증가에 기여하고 있습니다. 회복이 빨리 입원 기간이 단축되는 저침습 수술의 동향도 시장 성장의 원인이 되고 있습니다. 생체적합성 금속과 같은 수술 재료의 진보와 영상 기술의 지속적인 개선은 수술 결과를 향상시키는 데 중요한 역할을 합니다. 이러한 혁신으로 외과의사는 보다 정확하고 침습성이 낮은 수술을 수행할 수 있어 회복 시간 단축과 합병증 위험을 줄일 수 있습니다. 첨단 영상 시스템의 지속적인 개발은 수술 중 실시간 시각화를 가능하게 하여 정확성과 환자의 전반적인 안전성을 향상시킵니다. 이러한 기술이 진화를 계속하고 있는 가운데 두개악안면 장치 시장의 성장에 크게 기여할 것으로 기대되고 있습니다. 게다가 개발도상국에서의 의료비 지출 증가는 두개악안면 장치에 대한 접근 확대를 촉진하고 있습니다. 이러한 지역에서의 상환 정책의 개선은 특히 복잡한 안면 재건 사례에서 이러한 장치를 더 쉽게 사용할 수 있도록 도와줍니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 28억 달러 |

| 예측 금액 | 51억 달러 |

| CAGR | 5.7% |

MF 플레이트와 스크류 고정 시스템 부문은 하악골, 중안면, 두개골의 골절 치료에 대한 신뢰성으로부터 2024년에 52.4%의 점유율을 차지했습니다. 이 시스템은 두개골 안면 수술에 가장 널리 사용되는 것 중 하나입니다. 골편의 정확한 정렬을 가능하게 하여 회복 촉진 및 치유 향상에 기여합니다. MF 플레이트 및 스크류 고정 시스템은 간편한 적용성과 효율적인 안정화 능력으로 외과의사에게 선호됩니다.

제품 부문별로는 내부 고정기 부문이 2034년까지 연평균 복합 성장률(CAGR)은 5.4%를 보일 것으로 예측됩니다. 내부 고정기는 체내 안정화를 실현하고 외부 감염 위험을 줄이는 이점에서 보급이 진행되고 있습니다. 회복 과정에서 골유합 촉진 능력은 저침습 수술에서 특히 높게 평가되고 있습니다. 이 낮은 침습 수술에 대한 지향은 환자와 외과 의사 모두가 요구하는 외상성이 적은 수술과 회복 기간의 단축이라는 요구에 부합하는 것입니다.

미국 두개악안면 장치 시장은 교통사고나 스포츠 부상 발생률이 높고, 이들이 재건 수술을 필요로 하는 경우가 많기 때문에 2024년에는 13억 달러로 평가되었습니다. 정부의 의료 액세스 개선 프로그램과 의료기기의 기술 혁신에 의해 미국의 병원이나 진료소에서는 선진적인 두개턱 안면(CMF)용 의료기기의 도입이 확대되고 있습니다. 안면 재건 수술에 대한 높은 수요와 최첨단 의료 기술에 대한 접근성 향상이라는 시너지 효과로 향후 수년간 미국 시장의 성장이 지속될 것으로 예측됩니다.

메드트로닉, 스트라이커, 존슨 엔드 존슨 등 세계 두개악안면 장치 시장의 주요 기업들은 전략적 인수, 제품 혁신 및 기술 발전을 통해 시장에서의 존재감 확대에 주력하고 있습니다. B Braun과 Integra와 같은 기업들은 수술 결과를 향상시키기 위한 첨단 영상 진단 시스템과 생체적합성 소재를 도입하여 자사 제품 포트폴리오를 강화하고 있습니다. 또한 Zimmer Biomet 및 KLS Martin과 같은 기업들은 경쟁력을 유지하고 고품질, 효율적이고 침습적인 솔루션을 제공하기 위해 R&D 투자를 늘리고 있습니다. 이러한 전략은 신속하게 진화하는 두개악안면 장치 시장에서 이러한 기업들이 발판을 강화하는 데 도움이 됩니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 안면 손상 및 외상 발생률 증가

- 미용 성형 수술의 보급 확대

- 선천성 안면 기형 증가 경향

- 확대되는 의료 지출

- 업계의 잠재적 위험 및 과제

- 두개턱 안면 수술의 고비용

- 시장 기회

- 생체 흡수성 및 생체 적합성 재료의 성장

- 신흥 시장에서의 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 가격 분석, 2024

- 두개악 안면 임플란트의 수량(단위), 지역별, 2021-2034

- 환자 특이적 두개악 안면 임플란트(경쟁별)

- 밸류체인 분석

- 장래 시장 동향

- 상환 시나리오

- 기술 상황

- 현행 기술

- 신흥기술

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 제품별, 2021-2034

- 주요 동향

- MF 플레이트 및 스크류 고정 시스템

- 두개골 플랩 고정 시스템

- 두개 안면 골 연장 시스템

- 턱관절 치환 시스템

- 뼈 이식 대체 시스템

제6장 시장 추정 및 예측 : 임플란트 유형별, 2021-2034

- 주요 동향

- 표준 임플란트

- 커스텀/환자 특이적 임플란트

제7장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 내부 고정기

- 외부 고정기

제8장 시장 추정 및 예측 : 재료별, 2021-2034

- 주요 동향

- 금속

- 생체 흡수성 재료

- 세라믹

- 폴리머

제9장 시장 추정 및 예측 : 용도별, 2021-2034

- 주요 동향

- 외상 재건 수술

- 두개골 수술

- 중안면 수술

- 하악 수술

- 안와저 재건 수술

- 악교정 수술

- 성형외과

제10장 시장 추정 및 예측 : 흡수성별, 2021-2034

- 주요 동향

- 비흡수성 고정기

- 흡수성 고정기

제11장 시장 추정 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 최종 용도

제12장 시장 추정 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 네덜란드

- 스위스

- 벨기에

- 스웨덴

- 폴란드

- 오스트리아

- 덴마크

- 아일랜드

- 포르투갈

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 칠레

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제13장 기업 프로파일

- Acumed

- Anatomics

- B. BRAUN

- Beijing Naton Medical Technology

- BIOPLATE

- Cavendish Implants

- CranioTech

- JEIL MEDICAL

- Johnson & Johnson

- Kelyniam Global

- KLS Martin Group

- Matrix Surgical USA

- Medartis AG

- MEDPRIN

- Medtronic

- Stryker

- Xilloc Medical

- Zimmer Biomet

The Global Craniomaxillofacial Devices Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 5.1 billion by 2034.

Market growth is attributed to the rising occurrence of facial injuries resulting from road accidents, sports-related incidents, and violence, which are fueling the demand for reconstructive surgeries. Additionally, congenital facial deformities in children contribute to the increased need for CMF devices in pediatric surgeries. The trend toward minimally invasive surgical procedures, which offer faster recovery and shorter hospital stays, is also contributing to the growth. Advancements in surgical materials, such as biocompatible metals, and the continuous improvement in imaging technologies are playing a significant role in enhancing surgical outcomes. These innovations enable surgeons to perform more accurate and minimally invasive procedures, leading to quicker recovery times and reduced risk of complications. The ongoing development of advanced imaging systems allows for real-time visualization during surgeries, improving precision and overall safety for patients. As these technologies continue to evolve, they are expected to significantly contribute to the growth of the craniomaxillofacial devices market. Additionally, the rising healthcare spending in developing countries is facilitating greater access to CMF devices. Improved reimbursement policies in these regions are helping to make these devices more accessible, especially for complex facial reconstruction cases.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 5.7% |

The MF plate and screw fixation system segment held 52.4% share in 2024 driven by the reliability in treating fractures of the mandible, midface, and skull, these systems remain among the most widely used in craniomaxillofacial surgeries. They offer precise alignment of bone fragments, contributing to faster recovery and enhanced healing. MF plate and screw fixation systems are favored by surgeons due to their straightforward application and efficient stabilization capabilities.

In terms of product segmentation, the internal fixators segment will grow at a CAGR of 5.4% through 2034, gaining popularity because internal fixators offer the benefit of providing internal stabilization, which reduces the risk of external infections. Their ability to promote bone healing during recovery makes them highly favored for minimally invasive surgeries. This preference for less invasive procedures aligns with patient and surgeon demand for less traumatic surgeries that also offer quicker recovery times.

U.S. Craniomaxillofacial Devices Market was valued at USD 1.3 billion in 2024 owing to the high incidence of traffic-related accidents and sports injuries, which often require reconstructive surgeries. With government programs improving healthcare access and technological innovations in medical devices, hospitals and clinics in the U.S. are increasingly adopting advanced CMF devices. This combination of high demand for facial reconstruction procedures and enhanced access to cutting-edge medical technologies is expected to continue driving the U.S. market growth in the coming years.

Key players in the Global Craniomaxillofacial Devices Market, such as Medtronic, Stryker, and Johnson & Johnson, focus on expanding their market presence through strategic acquisitions, product innovations, and technological advancements. Companies like B Braun and Integra are enhancing their portfolios by incorporating advanced imaging systems and biocompatible materials to improve surgical outcomes. Additionally, firms like Zimmer Biomet and KLS Martin are increasing their investments in research and development to stay competitive, ensuring they provide high-quality, efficient, and minimally invasive solutions. These strategies are helping these players strengthen their foothold in the rapidly evolving craniomaxillofacial devices market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Implant type trends

- 2.2.4 Location trends

- 2.2.5 Metals trends

- 2.2.6 Application trends

- 2.2.7 Resorbability trends

- 2.2.8 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of facial injuries and trauma

- 3.2.1.2 Increasing adoption of cosmetic surgeries

- 3.2.1.3 Growing prevalence of congenital facial deformities

- 3.2.1.4 Expanding healthcare expenditure

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of craniomaxillofacial procedures

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in bioresorbable and biocompatible materials

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Pricing analysis, 2024

- 3.6 Number of craniomaxillofacial implants volume (units), by region, 2021 - 2034

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Patient-specific craniomaxillofacial implants, by competitor

- 3.8 Value chain analysis

- 3.9 Future market trends

- 3.10 Reimbursement scenario

- 3.11 Technology landscape

- 3.11.1 Current technologies

- 3.11.2 Emerging technologies

- 3.12 Gap analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 MF plate and screw fixation system

- 5.3 Cranial flap fixation system

- 5.4 CMF distraction system

- 5.5 Temporomandibular joint replacement system

- 5.6 Bone graft substitute system

Chapter 6 Market Estimates and Forecast, By Implant Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Standard implants

- 6.3 Customized/patient-specific implants

Chapter 7 Market Estimates and Forecast, By Location, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Internal fixators

- 7.3 External fixators

Chapter 8 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Metals

- 8.3 Bioabsorbable materials

- 8.4 Ceramics

- 8.5 Polymers

Chapter 9 Market Estimates and Forecast, By Applications, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Trauma reconstruction surgery

- 9.2.1 Cranial surgery

- 9.2.2 Mid-face surgery

- 9.2.3 Mandibular surgery

- 9.2.4 Orbital floor reconstruction surgery

- 9.3 Orthognathic surgery

- 9.4 Plastic surgery

Chapter 10 Market Estimates and Forecast, By Resorbability, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Non-resorbable fixators

- 10.3 Resorbable fixators

Chapter 11 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 Hospitals

- 11.3 Ambulatory surgery centers

- 11.4 Other end use

Chapter 12 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Russia

- 12.3.7 Netherlands

- 12.3.8 Switzerland

- 12.3.9 Belgium

- 12.3.10 Sweden

- 12.3.11 Poland

- 12.3.12 Austria

- 12.3.13 Denmark

- 12.3.14 Ireland

- 12.3.15 Portugal

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 Japan

- 12.4.3 India

- 12.4.4 South Korea

- 12.4.5 Australia

- 12.4.6 Thailand

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Colombia

- 12.5.5 Chile

- 12.6 Middle East and Africa

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Acumed

- 13.2 Anatomics

- 13.3 B. BRAUN

- 13.4 Beijing Naton Medical Technology

- 13.5 BIOPLATE

- 13.6 Cavendish Implants

- 13.7 CranioTech

- 13.8 JEIL MEDICAL

- 13.9 Johnson & Johnson

- 13.10 Kelyniam Global

- 13.11 KLS Martin Group

- 13.12 Matrix Surgical USA

- 13.13 Medartis AG

- 13.14 MEDPRIN

- 13.15 Medtronic

- 13.16 Stryker

- 13.17 Xilloc Medical

- 13.18 Zimmer Biomet