|

시장보고서

상품코드

1755197

POC 지질 검사 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Point of Care Lipid Test Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

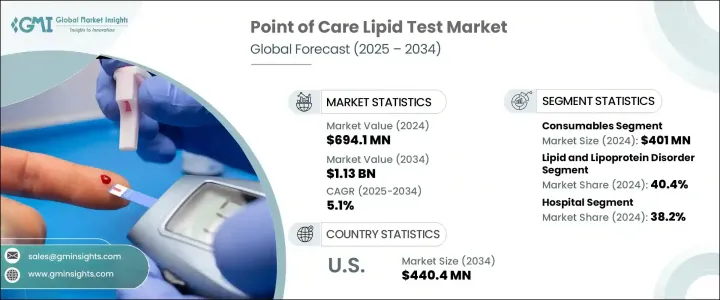

세계의 POC 지질 검사 시장은 2024년에는 6억 9,410만 달러에 달했고, CAGR 5.1%를 나타내 2034년에는 11억 3,000만 달러에 이를 것으로 예측됩니다.

이 시장은 트리글리세리드와 콜레스테롤과 같은 혈중 지질 농도를 기존의 실험실 이외에서 측정하도록 설계된 휴대용 진단 솔루션을 포함하고 있습니다. 임상 현장과 일반 건강 관리 환경, 가정에서의 개인적인 사용에 필수적입니다. 지질 수준의 이상과 관련이 많은 심혈관 질환의 세계 부담 증가는 쉽게 이용할 수 있는 대체 검사에 대한 수요를 계속 밀어 올리고 있습니다.

신속하고 사용하기 쉬운 검사법은 개인이 적극적으로 건강을 관리하고자 하는 가운데, 점점 더 요구되고 있습니다. 이러한 장비는 보다 정밀하고 사용하기 쉬워지고 있으며, 그 매력은 점점 높아지고 있습니다. 전통적인 진단에서 온디맨드 지질 프로파일링으로의 전환은 헬스케어의 전망을 재형성하고, 사람들은 종래의 의료 예약에 의존하지 않고 자신의 건강을 관리할 것을 요구하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 6억 9,410만 달러 |

| 예측 금액 | 11억 3,000만 달러 |

| CAGR | 5.1% |

2024년 소모품 부문은 4억 100만 달러를 창출했고 2034년까지 연평균 복합 성장률(CAGR) 5%를 나타낼 것으로 예측됩니다. 국제보건기구가 강조하고 있는 바와 같이, 심혈관질환의 세계 발생률 증가가 지질검사제품 수요 급증의 중요한 원동력이 되고 있습니다. 시약 카트리지와 테스트 스트립과 같은 소모품은 지질 프로파일 검사에 필수적이며 단일 사용을 위해 재구매 빈도가 높습니다. Point of Care 진단이 외래 센터, 1차 케어 오피스, 개인 건강 설정 등 다양한 건강 관리 환경에 통합됨에 따라 신뢰할 수 있는 일회용 구성 요소에 대한 필요성이 커지고 있습니다. 빠르고 위생적이고 정확한 검사 솔루션에 대한 선호도가 높아짐으로써 소모품 사용을 촉진하고 있습니다.

지질 및 지단백질 장애 분절은 유전적 및 후천적 지질 불균형을 포함한 지질 이상증의 유병률 증가로 2024년에 40.4%를 차지하며 최대 시장 점유율을 차지했습니다. 이러한 질병은 심장 관련 질환의 개발에 중심적인 역할을 하고 있으며, 세계 사망 원인의 1위를 유지하고 있습니다. 지질 이상증의 진단과 관리의 긴급성은 요지 지질 패널의 보급을 뒷받침합니다. 특히 내과 및 순환기과를 전문으로 하는 의료 종사자들은 조기 개입을 지원하기 위해 이러한 검사에 큰 신뢰를 갖고 있습니다. 정기적 인 지질 모니터링에 대한 수요로 인해 이러한 진단 방법은 전문 의료 및 일반 건강 관리 모두에서 기본적인 도구가되었습니다.

미국의 POC 지질 검사 시장은 2034년까지 4억 4,040만 달러에 이를 것으로 예측됩니다. 심혈관 위험에 대한 사회적 관심 증가는 지질 검사의 중요성을 널리 인식하고 편리하고 사용하기 쉬운 진단 키트의 보급을 뒷받침하고 있습니다. 보다 많은 개인이 적극적인 건강 관리를 목표로 하는 가운데, 즉각적인 집 검사로의 시프트가 가속하고 있습니다. 전국적인 지질이상증의 이환율 상승으로 신뢰성이 높고 이용하기 쉬운 솔루션에 대한 요구가 높아지고 있습니다. 의식이 계속 증가하고 있는 가운데, 공식적인 실험실 방문을 필요로 하지 않고 정기적인 스크리닝을 가능하게 하는 소형 진단 툴 수요가 급증하고, 시장은 그 혜택을 받고 있습니다.

세계의 POC 지질 검사 산업의 혁신과 확대를 견인하는 주요 업계 참가자로는 F. Hoffmann-La Roche, VivaChek Biotech, Kanlife, Abbott Laboratories, SD Biosensor, Sinocare, Callegari, MiCoBio, Nova Biomedical, Menarini Group이 포함됩니다. 시장에서 포지셔닝을 강화하기 위해 주요 기업은 지속적인 제품 혁신과 기술 강화를 중심으로 한 전략을 실시했습니다. 각 회사는 사용성을 향상시키면서 보다 빠르고 정확한 결과를 제공하는 고급 진단 장비 개발에 투자하고 있습니다. 많은 기업들이 건강 관리 판매자와 클리닉과의 파트너십과 전략적 제휴를 통해 지리적 도달범위를 확대하고 있습니다. 이러한 제휴는 다양한 시장에서 지질 검사 키트에 대한 액세스를 향상시키는 데 도움이 됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 심혈관질환의 유병률 증가

- 예방 헬스케어로의 시프트의 고조

- POC 지질 검사 기기의 기술적 진보

- 신흥국에서의 도입 확대

- 업계의 잠재적 위험 및 과제

- 엄격한 규제 시나리오

- 지방에서의 낮은 인지도

- 성장 가능성 분석

- 규제 상황

- 기술적 상황

- 향후 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 기기

- 소모품

제6장 시장 추계·예측 : 적응 질환별(2021-2034년)

- 주요 동향

- 지질 및 지단백질 장애

- 내인성 고지혈증

- 탄지에르병

- 고지단백혈혈증

- 가족성 고콜레스테롤혈증

- 기타 지질 및 지단백질 장애

- 죽상 동맥경화증

- 간 및 신장 질병

- 당뇨병

- 기타 질환 적응증

제7장 시장 추계·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 클리닉

- 진단실험실

- 기타 용도

제8장 시장추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott Laboratories

- Callegari

- F. Hoffmann-La Roche

- Kanlife

- Menarini Group

- MiCoBio

- Nova Biomedical

- SD Biosensor

- Sinocare

- VivaChek Biotech

The Global Point of Care Lipid Test Market was valued at USD 694.1 million in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 1.13 billion by 2034. This market encompasses portable diagnostic solutions designed to measure blood lipid levels, such as triglycerides and cholesterol, outside traditional laboratory settings. These tools provide real-time results, making them essential in clinical practice, general healthcare environments, and for personal use at home. The mounting global burden of cardiovascular conditions, which are often linked with abnormal lipid levels, continues to drive demand for easily accessible testing alternatives.

Rapid and user-friendly testing methods are becoming increasingly sought after as individuals seek to manage health proactively. With a greater emphasis on preventive care and early detection, there's been a noticeable push for reliable devices that are simple to operate and provide fast, accurate outcomes. Ongoing technological improvements are making these devices more precise and user-friendly, reinforcing their growing appeal. The move away from traditional diagnostics and toward on-demand lipid profiling reshape the healthcare landscape, as people demand control over their wellness without depending on conventional healthcare appointments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $694.1 Million |

| Forecast Value | $1.13 Billion |

| CAGR | 5.1% |

In 2024, the consumables segment generated USD 401 million and is projected to grow at a 5% CAGR through 2034. The increasing global incidence of cardiovascular ailments, as highlighted by international health organizations, is a significant driver behind the surge in demand for lipid testing products. Consumables such as reagent cartridges and test strips are essential for every lipid profile test and are intended for single use, resulting in high repurchase frequency. As point-of-care diagnostics become more integrated into various healthcare environments like outpatient centers, primary care offices, and personal health setups, the necessity for reliable, disposable components is rising. The growing preference for fast, hygienic, and accurate testing solutions is enhancing the uptake of consumables.

The lipid and lipoprotein disorder segment accounted for the largest market share in 2024, holding 40.4% due to the rising prevalence of dyslipidemia, including genetic and acquired lipid imbalances. These disorders play a central role in the development of heart-related illnesses, which continue to be the foremost cause of mortality worldwide. The urgency of diagnosing and managing lipid irregularities reinforces the widespread use of point-of-care lipid panels. Medical professionals-particularly those specializing in internal medicine and cardiology-heavily rely on these tests to support early interventions. The demand for regular lipid monitoring has made these diagnostics a fundamental tool in both specialized and general healthcare.

United States Point of Care Lipid Test Market is anticipated to reach USD 440.4 million by 2034. Increasing public concern regarding cardiovascular risk has sparked widespread awareness about the importance of lipid testing, which is pushing the adoption of convenient, easy-to-use diagnostic kits. The shift toward immediate, at-home testing is accelerating as more individuals aim to manage their health proactively. The rising incidence of lipid disorders across the country is intensifying the need for dependable, accessible solutions. As awareness continues to grow, the market is benefiting from a surge in demand for compact diagnostic tools that allow regular screening without the need for formal lab visits.

Major industry participants driving innovation and expansion in the Global Point of Care Lipid Test Industry include F. Hoffmann-La Roche, VivaChek Biotech, Kanlife, Abbott Laboratories, SD Biosensor, Sinocare, Callegari, MiCoBio, Nova Biomedical, and Menarini Group. To strengthen their market positioning, key players are implementing strategies centered around continuous product innovation and technological enhancement. Companies are investing in the development of advanced diagnostic devices that deliver faster and more accurate results while enhancing user-friendliness. Many are expanding their geographic reach through partnerships and strategic collaborations with healthcare distributors and clinics. These alliances help improve accessibility to lipid testing kits across various markets.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.3 Growth drivers

- 3.3.1 Increasing prevalence of cardiovascular diseases

- 3.3.2 Rising shift towards preventive healthcare

- 3.3.3 Technological advancements in POC lipid testing devices

- 3.3.4 Growing adoption in emerging economies

- 3.4 Industry pitfalls and challenges

- 3.4.1 Stringent regulatory scenario

- 3.4.2 Limited awareness in rural areas

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.7 Technological landscape

- 3.8 Future market trends

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.3 Consumables

Chapter 6 Market Estimates and Forecast, By Disease Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Lipid and lipoprotein disorder

- 6.2.1 Endogenous hyperlipemia

- 6.2.2 Tangier disease

- 6.2.3 Hyperlipoproteinemia

- 6.2.4 Familial hypercholesterolemia

- 6.2.5 Other lipid and lipoprotein disorders

- 6.3 Atherosclerosis

- 6.4 Liver and renal diseases

- 6.5 Diabetes mellitus

- 6.6 Other disease indication

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Clinics

- 7.4 Diagnostic laboratories

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Callegari

- 9.3 F. Hoffmann-La Roche

- 9.4 Kanlife

- 9.5 Menarini Group

- 9.6 MiCoBio

- 9.7 Nova Biomedical

- 9.8 SD Biosensor

- 9.9 Sinocare

- 9.10 VivaChek Biotech