|

시장보고서

상품코드

1755202

퇴비화 가능 포장 필름 시장 : 기회, 촉진요인, 업계 동향 분석, 예측(2025-2034년)Compostable Packaging Films Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

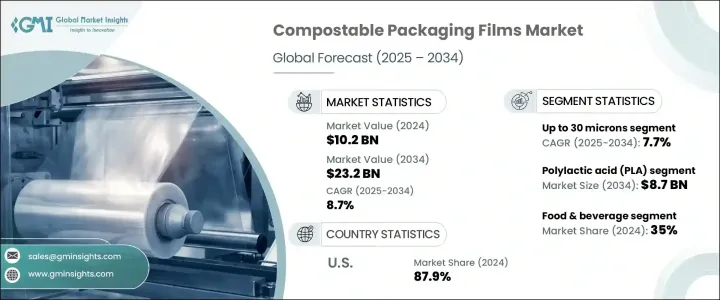

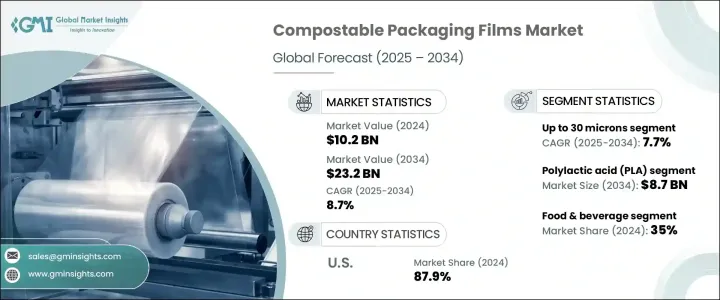

퇴비화 가능 포장 필름 세계 시장 규모는 2024년에는 102억 달러로 평가되었으며, 활발한 전자상거래 부문과 음식산업의 성장에 견인되어 CAGR 8.7%로 성장해 2034년에는 232억 달러에 달할 것으로 예측되고 있습니다.

그러나 미국의 전 정권 하에서 바이오폴리머와 필수가공기기에 관세가 도입됨에 따라 퇴비화 가능 포장 필름의 현지 제조업체에 비용 압력이 생겼습니다. 이러한 관세로 인해 글로벌 공급망이 중단되고 투입 비용이 부풀려졌으며 지속 가능한 포장 솔루션에 투자하는 사람들에게 불확실성이 발생했습니다. 추가된 비용 부담은 특히 수입 원료나 제조 기술에 의존하고 있는 중소 기업에 있어서, 퇴비화 가능한 필름의 확대를 제한할 가능성이 있습니다. 또한, 타국으로부터의 보복 관세는 국제 무역을 보다 곤란하게 해, 수출 기회를 손상시키고, 업계 전체의 경쟁력을 저하시켰습니다.

전자상거래의 성장은 지속가능한 포장 수요에 큰 영향을 미치고 있습니다. 퇴비화 가능 포장 필름의 개척자는 전자상거래 분야에 맞는 내구성, 경량성, 생분해성 필름의 개발에 주력해야 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 102억 달러 |

| 예측 금액 | 232억 달러 |

| CAGR | 8.7% |

퇴비화 가능 포장 필름 시장은 두께별로 30 마이크론까지, 30-60 마이크론, 60 마이크론 이상의 3 부문으로 분류됩니다.2034년까지 연평균 7.7%의 성장률로 성장할 것으로 예측됩니다. 이 얇은 필름은 베이커리 제품, 스낵 과자, 티백 등의 가벼운 식품 포장이나 라벨이나 오버랩 용도로 자주 사용됩니다.

소재별로 보면, 시장은 폴리유산(PLA), 대나무, 폴리히드록시알카노에이트(PHA), 전분계 필름, 셀룰로오스계 필름, 기타 등의 카테고리로 나뉩니다. PLA 기반 필름은 인쇄성, 투명성, 퇴비성이 뛰어나 식품 포장 분야에서 특히 인기가 높습니다.

미국의 퇴비화 가능 포장 필름 2024년의 동시장 점유율은 87.9%였지만, 이것은 플라스틱 폐기물의 삭감을 목적으로 한 강력한 규제 지원과, 기업에 의한 지속가능성에의 대처의 고조에 의한 것입니다 특히 유기농 식품 업계나 환경 의식의 높은 소비자로부터의 퇴비화 가능 필름에 대한 수요가 높아지고 있으며, 이것이 가정에서 퇴비화 가능한 패키징 솔루션의 기술 혁신을 촉진하고 있습니다.개발 기업은 상업적으로 실행 가능한 생분해성 대체품을 개발하기 위해 재료 기술자와 적극적으로 협력하고 있습니다.

세계 퇴비화 가능 포장 필름 시장의 주목할만한 기업은 BioBag International, BASF, Biome Bioplastics, Amtrex Nature Care, Baroda Rapids 등입니다. 시장 포지션을 강화하기 위해 각 회사는 퇴비화 가능한 포장 분야의 기술력을 강화하기 위해 제휴 및 인수 등의 전략을 채택하고 있습니다. 소비자 수요가 높아짐에 따라 고품질의 생분해성 필름 개발에 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 지속가능한 포장에 대한 소비자 수요

- 식품 및 음료 업계에서의 용도의 성장

- 일회용 플라스틱에 대한 규제 강화

- 유기농 및 내츄럴 제품 브랜드에서의 수요

- 전자상거래와 친환경 배송 요구의 확대

- 업계의 잠재적 위험 및 과제

- 높은 생산 비용과 재료 비용

- 제한된 산업용 퇴비화 인프라

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 장래 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추정 및 예측 : 재료별, 2021년-2034년

- 주요 동향

- 폴리유산(PLA)

- 대나무

- 폴리하이드록시알칸산(PHA)

- 전분계 필름

- 셀룰로오스계 필름

- 기타

제6장 시장 추정 및 예측 : 두께별, 2021년-2034년

- 주요 동향

- 최대 30 미크론

- 30-60 미크론

- 60 미크론 이상

제7장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 식품?음료

- 헬스케어 및 의약품

- 소매 및 E-Commerce

- 홈&퍼스널케어

- 기타

제8장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Amtrex Nature Care

- Baroda Rapids

- BASF

- BI-AX International

- BioBag International

- Biome Bioplastics

- Cortec Corporation

- Easy Flux

- Futamura Group

- Novamont

- Plascon Group

- Polynova Industries

- Polystar Plastics

- Taghleef Industries

- TIPA

The Global Compostable Packaging Films Market was valued at USD 10.2 billion in 2024 and is estimated to grow at a CAGR of 8.7% to reach USD 23.2 billion by 2034 driven by the booming e-commerce sector and the growing food and beverage industry. However, the introduction of tariffs on biopolymers and essential processing equipment under the previous administration in the U.S. has created cost pressures for local manufacturers of compostable packaging films. These tariffs have disrupted global supply chains, inflated input costs, and generated uncertainty for those investing in sustainable packaging solutions. The added cost burden could limit the expansion of compostable films, especially for smaller businesses that rely on imported feedstock or manufacturing technologies. Additionally, retaliation tariffs from other countries have made international trade more difficult, hurting export opportunities and reducing the overall competitiveness of the industry.

E-commerce growth is significantly impacting the demand for sustainable packaging, as the increasing volume of products being shipped online requires packaging that meets both consumer preferences and regulatory standards. Compostable films are gaining traction in e-commerce logistics because they are lightweight, flexible, and biodegradable. Manufacturers in the compostable packaging films market should focus on developing durable, lightweight, and biodegradable films tailored to the e-commerce sector. This will help meet consumer demand and address the growing regulatory pressures for sustainable packaging, particularly in emerging markets like India.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.2 Billion |

| Forecast Value | $23.2 Billion |

| CAGR | 8.7% |

The compostable packaging films market is categorized by thickness into three segments: up to 30 microns, 30-60 microns, and above 60 microns. The market for films up to 30 microns is projected to grow at a CAGR of 7.7% through 2034. These thin films are commonly used for packaging light food items such as bakery products, snacks, or tea bags, as well as for label and overwrap applications. Their minimal material usage makes them cost-effective while ensuring compliance with compostable standards for short-shelf-life products.

By material, the market is divided into several categories, including polylactic acid (PLA), bamboo, polyhydroxyalkanoate (PHA), starch-based films, cellulose-based films, and others. The PLA market is expected to reach USD 8.7 billion by 2034. PLA-based films are particularly popular in the food packaging sector due to their excellent printability, transparency, and compostability. PLA films present a viable alternative to fossil-fuel-based plastics, and their compatibility with existing converting equipment facilitates their rapid commercial adoption.

U.S. Compostable Packaging Films Market held a share of 87.9% in 2024 attributed to strong regulatory support aimed at reducing plastic waste and the growing commitment to sustainability by businesses. There is a rising demand for compostable films, particularly from the organic food industry and environmentally conscious consumers, which is driving innovation in home-compostable packaging solutions. Companies are actively collaborating with material engineers to develop commercially viable biodegradable alternatives.

Notable players in the Global Compostable Packaging Films Market include BioBag International, BASF, Biome Bioplastics, Amtrex Nature Care, and Baroda Rapids. To strengthen their market position, companies are adopting strategies such as forming partnerships and acquisitions to enhance their technical capabilities in the compostable packaging sector. Many companies are focusing on the development of high-quality, biodegradable films that meet the growing consumer demand for sustainable packaging. By improving their manufacturing processes and increasing the availability of compostable materials, businesses are seeking to gain a competitive edge in the market.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1.1 Supply chain reconfiguration

- 3.2.4.1.2 Pricing and product strategies

- 3.2.4.1.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Consumer demand for sustainable packaging

- 3.3.1.2 Growth in food & beverage industry applications

- 3.3.1.3 Increasing restrictions on single-use plastics

- 3.3.1.4 Demand from organic and natural product brands

- 3.3.1.5 Growth of e-commerce and eco-friendly shipping needs

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High production and material costs

- 3.3.2.2 Limited industrial composting infrastructure

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 Pestel analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Material, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Polylactic acid (PLA)

- 5.3 Bamboo

- 5.4 Polyhydroxyalkanoate (PHA)

- 5.5 Starch-based films

- 5.6 Cellulose-based films

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Thickness, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Up to 30 microns

- 6.3 30–60 microns

- 6.4 Above 60 microns

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Healthcare & pharmaceuticals

- 7.4 Retail & e-commerce

- 7.5 Home & personal care

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amtrex Nature Care

- 9.2 Baroda Rapids

- 9.3 BASF

- 9.4 BI-AX International

- 9.5 BioBag International

- 9.6 Biome Bioplastics

- 9.7 Cortec Corporation

- 9.8 Easy Flux

- 9.9 Futamura Group

- 9.10 Novamont

- 9.11 Plascon Group

- 9.12 Polynova Industries

- 9.13 Polystar Plastics

- 9.14 Taghleef Industries

- 9.15 TIPA