|

시장보고서

상품코드

1755207

물류 및 공급망 분야 AI 시장 : 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)AI in Logistics and Supply Chain Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

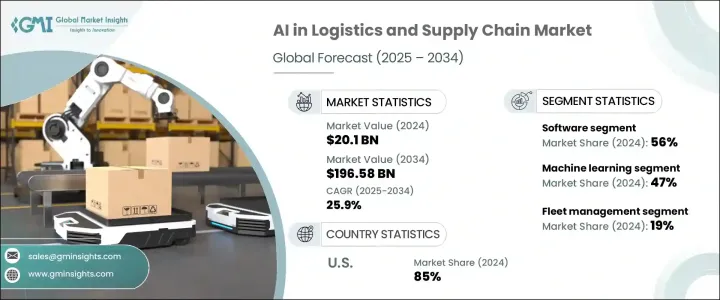

물류 및 공급망 분야 AI 세계 시장 규모는 2024년에 201억 달러로 평가되었고, 리얼타임공급 체인 가시화, 최적화된 루트 플래닝, 정확한 수요 추정 및 예측, 창고에 있어서의 자동화의 요구 증가에 의해 CAGR 25.9%로 성장하여 2034년에는 1,965억 8,000만 달러에 달할 것으로 예상됩니다.

기업은 의사 결정 프로세스를 강화하고 운영 비용을 줄이고 복잡한 물류 네트워크를 관리하기 위해 점점 AI를 비즈니스에 통합하고 있습니다. 예측 분석, 로봇 프로세스 자동화, 자율주행 차량 등의 AI 대응 솔루션은 기존공급망을 지능적이고 적응할 수 있는 생태계로 전환하고 있습니다.

세계적인 공급망의 복잡성은 예측 분석과 실시간 데이터 요구를 야기하여 기업은 센서, GPS 및 기업 자원 계획(ERP) 시스템에서 엄청난 데이터를 분석하여 재고 관리를 최적화하고 비용을 절감할 수 있습니다. AI는 기업이 시장 환경 변화에 신속하게 적응하고 혼란을 방지하고 고객 만족도를 향상시키는 데 도움이 됩니다. 전자상거래와 옴니채널 소매의 확대는 속도, 정확성, 유연성의 필요성을 더욱 강조하고 있으며, AI 기술은 주문 처리의 간소화, 배송 일정 자동화, 고객 행동 예측에 도움이 됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 201억 달러 |

| 예측 금액 | 1,965억 8,000만 달러 |

| CAGR | 25.9% |

2024년에는 소프트웨어 부서가 56%의 점유율로 시장을 선도했으며, 2034년까지 연평균 복합 성장률(CAGR)은 26%를 보일 것으로 예측됩니다. 업무를 최적화하고 비용을 절감하고 효율성을 높이기 위해 물류 제공업체가 널리 채택하고 있습니다.

머신러닝(ML) 부문은 2024년에 47%의 점유율을 차지했습니다. 방대한 데이터 세트를 처리하고 실시간으로 실행 가능한 통찰력을 생성하는 이 기능은 IoT 장치, GPS 시스템 및 고객 상호 작용에서 발생하는 구조화 및 비구조화 데이터를 분석하는 데 필수적입니다. ML 알고리즘은 재고 관리를 최적화하고 수요 패턴을 밝히고 운영 병목 현상을 해결함으로써 효율성과 비용 효율성을 높입니다.

미국의 물류 및 공급망 시장에서 AI의 점유율은 85%로 2024년에는 62억 달러에 달할 전망입니다. AI 공급자의 존재에 의해 더욱 강화되어 물류에 있어서 AI 채택을 가속화하고 있습니다.

물류 및 공급망 분야 AI 시장에서 유명한 기업은 Amazon Web Services, Oracle, Blue Yonder, SAP SE, FourKites, C3.ai, Google, Microsoft, IBM, Manhattan Associates가 포함되어 있습니다. 시장에서의 지위를 강화하기 위해 각 사는 전략적 제휴와 인수에 주력하고, AI 능력을 강화하고, 서비스 제공의 폭을 넓히고 있습니다. 알타임 분석, 루트 최적화 및 수요 예측을 위해 AI 주도 소프트웨어 솔루션에 투자하여 급속도로 진화하는 시장에서 경쟁력을 유지할 수 있도록 하고 있으며, AI 솔루션 제공업체는 전자상거래 분야에 대한 주력을 강화하고 있어 소비자의 기대 증가에 부응하기 위해 신속하고 유연하고 정확한 배송 시스템을 확보하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 기술 공급자

- 시스템 통합사업자 및 컨설팅 회사

- 물류 기술 공급자

- 하드웨어 및 로봇 기업

- 매니지드 서비스 제공업체(MSP)

- 이익률 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 타국에 의한 보복조치

- 업계에 미치는 영향

- 주요 원재료의 가격 변동

- 공급망 재구성

- 제공비용의 영향

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제공 전략

- 무역에 미치는 영향

- 기술과 혁신의 상황

- 가격 동향 s

- 코스트 내역 분석

- 특허 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 실시간 공급망 시각화에 대한 수요 증가

- 전자상거래와 옴니채널 소매업의 성장

- 예측 분석과 머신러닝의 진보

- 스마트 창고를 위한 IoT와 AI의 통합

- 자율주행차와 드론의 도입

- 업계의 잠재적 위험 및 과제

- 높은 초기 도입 비용

- 데이터 프라이버시 및 보안에 대한 우려

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추정 및 예측 : 컴포넌트별, 2021년-2034년

- 주요 동향

- 하드웨어

- 센서

- 로봇(예 : 무인 반송차, 드론)

- 소프트웨어

- 예측 분석

- 운송 관리 시스템

- 재고 관리

- 창고 관리

- 서비스

- 매니지드 서비스

- 전문 서비스

- 전개 및 통합

- 컨설팅

- 지원 및 유지 보수

제6장 시장 추정 및 예측 : 기술별, 2021년-2034년

- 주요 동향

- 머신러닝

- 자연언어처리(NLP)

- 컴퓨터 비전

- 컨텍스트 인식 컴퓨팅

- 로보틱스 프로세스 오토메이션(RPA)

제7장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 차량 관리

- 공급 체인 계획

- 재고 및 창고 관리

- 화물 중개 및 위험 관리

- 수요 예측

- 고객 서비스(챗봇, 가상 어시스턴트)

- 주문 처리와 마지막 마일 배송

제8장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 소매 및 E-Commerce

- 제조업

- 자동차

- 식음료

- 헬스케어 및 의약품

- 운송 및 물류

- 에너지·유틸리티

- 기타

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- Amazon Web Services

- Blue Yonder

- C3.ai

- ClearMetal

- Fetch Robotics

- FourKites

- GE Digital

- Honeywell International

- Infor

- Korber Supply Chain

- Llamasoft

- Manhattan Associates

- Microsoft Corporation

- NVIDIA Corporation

- SAP SE

- Siemens AG

- Zebra Technologies

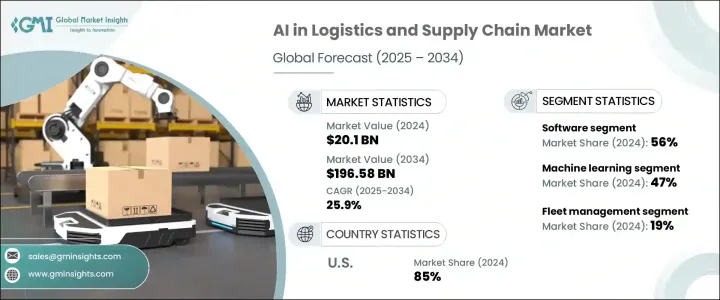

The Global AI in Logistics and Supply Chain Market was valued at USD 20.1 billion in 2024 and is estimated to grow at a CAGR of 25.9% to reach USD 196.58 billion by 2034, driven by the increasing need for real-time supply chain visibility, optimized route planning, accurate demand forecasting, and automation in warehouses. Companies are increasingly incorporating AI into their operations to enhance decision-making processes, reduce operational costs, and manage complex logistics networks. AI-enabled solutions such as predictive analytics, robotic process automation, and autonomous vehicles are transforming traditional supply chains into intelligent, adaptable ecosystems.

The growing intricacy of global supply chains has created a need for predictive analytics and real-time data, allowing businesses to analyze massive amounts of data from sensors, GPS, and enterprise resource planning (ERP) systems to optimize inventory management and reduce costs. AI helps companies adapt quickly to shifts in market conditions, prevent disruptions, and improve customer satisfaction. The expansion of e-commerce and omnichannel retail further emphasizes the need for speed, accuracy, and flexibility, where AI technologies help streamline order processing, automate delivery schedules, and forecast customer behavior.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20.1 Billion |

| Forecast Value | $196.58 Billion |

| CAGR | 25.9% |

In 2024, the software sector led the market with a share of 56%, anticipated to grow at a CAGR of 26% through 2034. Software helps in empowering intelligent decision-making, automation, and real-time data analysis throughout the supply chain. AI-driven software solutions, including route optimization, demand forecasting, and warehouse automation, are widely adopted by logistics providers to optimize operations, reduce costs, and enhance efficiency. These solutions are key to improving planning accuracy, minimizing human error, and quickly adjusting to market fluctuations. The emphasis on predictive analytics and real-time visibility significantly contributes to the growing demand for AI-powered software applications.

The machine learning (ML) segment held a 47% share in 2024. Its capability to process massive datasets and generate actionable insights in real time makes it essential for analyzing structured and unstructured data from IoT devices, GPS systems, and customer interactions. ML algorithms optimize inventory management, uncover demand patterns, and eliminate operational bottlenecks, thus enhancing efficiency and cost-effectiveness. These algorithms evolve continuously, providing predictive insights and automation opportunities that outperform traditional systems.

United States AI in the Logistics and Supply Chain Market held an 85% share and generated USD 6.2 billion in 2024 due to its advanced digital infrastructure and widespread adoption of emerging technologies. U.S.-based logistics firms are among the first to integrate AI for solutions such as route optimization, demand forecasting, warehouse automation, and predictive maintenance. The country's leading position is further bolstered by the presence of major tech companies and AI providers, accelerating AI adoption in logistics. Public and private sector investments in AI research and development, coupled with government initiatives like the National AI Initiative Act, support the adoption of AI technologies across the logistics and supply chain landscape.

Prominent players in the AI in Logistics and Supply Chain Market include Amazon Web Services, Oracle, Blue Yonder, SAP SE, FourKites, C3.ai, Google, Microsoft, IBM, and Manhattan Associates. To strengthen their market position, companies are focusing on strategic partnerships and acquisitions to enhance their AI capabilities and broaden service offerings. Leveraging cutting-edge technologies, these companies are integrating machine learning, robotics, and automation into logistics and supply chain operations to improve efficiency and reduce costs. Many firms invest in AI-driven software solutions for real-time analytics, route optimization, and demand forecasting, allowing them to stay competitive in a rapidly evolving market. Additionally, AI solution providers are increasing their focus on the e-commerce sector, ensuring quick, flexible, and accurate delivery systems to meet growing consumer expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 System integrators and consulting firms

- 3.2.3 Logistics technology providers

- 3.2.4 Hardware and robotics companies

- 3.2.5 Managed service providers (MSPs)

- 3.3 Profit margin analysis

- 3.4 Impact of Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Offering cost implications

- 3.4.3 Strategic industry responses

- 3.4.3.1 Supply chain reconfiguration

- 3.4.3.2 Pricing and Offering strategies

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Price trends

- 3.7 Cost breakdown analysis

- 3.8 Patent analysis

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rising demand for real-time supply chain visibility

- 3.11.1.2 Growth of e-commerce and omnichannel retailing

- 3.11.1.3 Advancements in predictive analytics and machine learning

- 3.11.1.4 Integration of IoT and AI for smart warehousing

- 3.11.1.5 Adoption of autonomous vehicles and drones

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High initial implementation costs

- 3.11.2.2 Data privacy and security concerns

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 Robots (e.g., automated guided vehicles, drones)

- 5.3 Software

- 5.3.1 Predictive analytics

- 5.3.2 Transportation management systems

- 5.3.3 Inventory management

- 5.3.4 Warehouse management

- 5.4 Services

- 5.4.1 Managed services

- 5.4.2 Professional services

- 5.4.2.1 Deployment & integration

- 5.4.2.2 Consulting

- 5.4.2.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Machine learning

- 6.3 Natural language processing (NLP)

- 6.4 Computer vision

- 6.5 Context-aware computing

- 6.6 Robotics process automation (RPA)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Fleet management

- 7.3 Supply chain planning

- 7.4 Inventory & warehouse management

- 7.5 Freight brokerage & risk management

- 7.6 Demand forecasting

- 7.7 Customer service (chatbots, virtual assistants)

- 7.8 Order fulfillment & last-mile delivery

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Retail & e-commerce

- 8.3 Manufacturing

- 8.4 Automotive

- 8.5 Food & beverage

- 8.6 Healthcare & pharmaceuticals

- 8.7 Transportation & logistics

- 8.8 Energy & utilities

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Amazon Web Services

- 10.2 Blue Yonder

- 10.3 C3.ai

- 10.4 ClearMetal

- 10.5 Fetch Robotics

- 10.6 FourKites

- 10.7 GE Digital

- 10.8 Google

- 10.9 Honeywell International

- 10.10 Infor

- 10.11 Korber Supply Chain

- 10.12 Llamasoft

- 10.13 Manhattan Associates

- 10.14 Microsoft Corporation

- 10.15 NVIDIA Corporation

- 10.16 SAP SE

- 10.17 Siemens AG

- 10.18 Zebra Technologies