|

시장보고서

상품코드

1755212

자율 화물기 시장 : 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Autonomous Cargo Aircraft Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

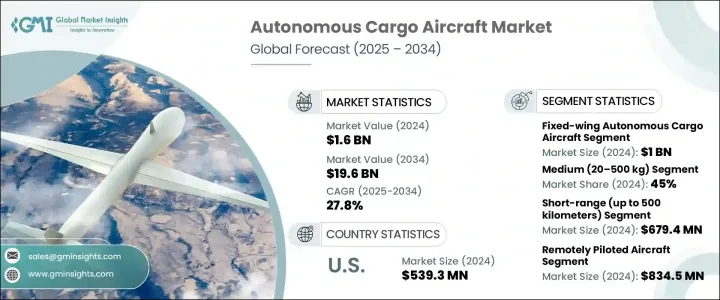

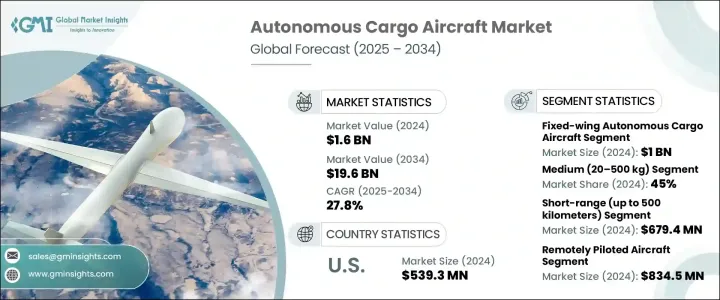

자율 화물기 세계 시장 규모는 2024년에 16억 달러로 평가되었고, 중거리 및 라스트마일의 딜리버리 혁신에 대한 주목이 높아지고, 방위 및 군사 분야에서의 채택 증가, 신흥국에서의 도시 개척의 가속 등을 배경으로 CAGR 27.8%로 성장하여 2034년에는 196억 달러에 달할 것으로 예상됩니다.

인프라 정비가 도시 확대를 따라가지 못하는 도시에서는 자율 화물기가 물류의 과제에 대한 중요한 솔루션으로 부상하고 있습니다. 기존의 교통 정체를 우회하고 복잡한 도시 지형에서도 신속하게 상품을 배송하는 그 능력은 차세대 공급망의 매우 중요한 요소가 되고 있습니다.

보다 신속한 정착에 대한 수요가 증가함에 따라 항공화물 플랫폼은 기존 지상 운송으로 해결할 수 없었던 마지막 원 마일의 비효율성을 극복하기 위해 필수적입니다. 항공기 이용은 교통 체증과 지리적 장애, 도로 인프라가 제한된 지역 등 기존 트럭에서는 서비스 수준 유지에 어려움을 겪는 지역에서 특히 큰 변화를 가져오고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 16억 달러 |

| 예측 금액 | 196억 달러 |

| CAGR | 27.8% |

수직 이착륙(VTOL) 분야는 2034년까지 80억 달러로 성장할 성장할 전망입니다. 좁은 공간, 활주로 없이 운영할 수 있는 능력, 그리고 대응력 덕분에 밀집된 도시 환경, 원격 배송 임무, 그리고 의료 물류와 같은 시간 민감한 요구 사항에 매우 적합합니다. 배터리 효율과 경량 복합재료에 대한 대규모 투자는 VTOL 기계의 확장성을 높입니다.

중형 페이로드 부문은 2024년에 45%의 점유율을 차지하며 용량과 항속 거리를 필요로 하는 물류 시나리오를 지원합니다. 확장성과 비용 효율성 덕분에 단거리 운영이 빈번하게 이루어지며, 특히 원격 위치와 주요 물류 센터 간의 격차를 해소하는 데 유용합니다.

미국의 자율 화물기 2024년 시장 규모는 5억 3,930만 달러로 평가되었고 국가 영공에 대한 무인시스템 통합에 대한 연방정부의 강력한 뒷받침에 지지되고 있습니다. 머신러닝, 인공지능 기반 라우팅 및 재해 대응 센서의 급속한 성장으로 운영 효율성이 향상되었으며 미국은 이 부문의 리더가 되었습니다.

Airbus, eHang, Natilus, Elroy Air, Dronamics는 혁신, 파트너십 및 확장 가능한 기술 플랫폼을 통해 자율 화물기 시장의 미래를 적극적으로 형성하고 있습니다. 물류 네트워크 및 공급망 운영자와의 전략적 협력은 실제 사용 사례를 파일럿하고 운영을 확장하는 데 도움이 되고 있습니다. VTOL 설계 최적화와 첨단 센서 기술의 통합에 중점을 둔 이 회사는 안전하고 지속가능하며 신속한 자율화물 운송에 대한 수요 증가에 대응할 준비를 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 자연재해와 인도주의 위기 발생률 증가

- 미들 마일과 라스트 마일의 배송 솔루션의 보급 확대

- 군 및 방위 투자 증가

- 신흥 경제의 급속한 도시화

- AI, 네비게이션, 비행 제어 시스템의 진보

- 업계의 잠재적 위험 및 과제

- 전동 무인 항공기의 적재량과 항속 거리의 제한

- 사이버 보안 위협과 통신 방해

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 대시보드

제5장 시장 추정 및 예측 : 기술 유형별, 2021년-2034년

- 주요 동향

- 고정날개 자율 화물기

- VTOL(수직 이착륙) 자율 항공기

제6장 시장 추정 및 예측 : 적재량별, 2021년-2034년

- 주요 동향

- 소형(20kg 이하)

- 중형(20-500kg)

- 대형(500kg 이상)

제7장 시장 추정 및 예측 : 거리별, 2021년-2034년

- 주요 동향

- 단거리(최대 500킬로미터)

- 중거리(500-2,000킬로미터)

- 장거리(2,000킬로미터 이상)

제8장 시장추정 및 예측 : 자율레벨별, 2021년-2034년

- 주요 동향

- 완전 자율형

- 원격 조종 항공기

- 반자율형

제9장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 전자상거래와 소매 물류

- 산업 및 해양 물류

- 군 및 방위

- 인도적 지원과 재해 구호

제10장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Airbus

- Dronamics Group Limited

- Ehang

- Elroy Air

- Jestar Logistics

- MightyFly

- Natilus

- Pipistrel

- Pyka Inc.

- Skydio, Inc.

- UAVOS

- Unmanned Systems Technology

- Xwing

- Zipline

The Global Autonomous Cargo Aircraft Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 27.8% to reach USD 19.6 billion by 2034 fueled by the increasing focus on middle-mile and last-mile delivery innovation, rising defense and military adoption, and the accelerating pace of urban development across emerging nations. In cities where infrastructure development can't keep pace with urban expansion, autonomous cargo aircraft are emerging as a critical solution to logistical challenges. Their ability to bypass traditional traffic congestion and deliver goods quickly over complex urban terrain makes them a pivotal element in next-gen supply chains.

As demand for faster fulfillment grows, aerial cargo platforms are essential to overcoming last-mile inefficiencies that conventional ground transport cannot resolve. Autonomous cargo aircraft enable point-to-point delivery with fewer handoffs, which helps reduce delays, improve supply chain visibility, and lower operational costs. Their use is particularly transformative in areas prone to traffic congestion, geographic barriers, or limited road infrastructure, where traditional trucks struggle to maintain service standards. For logistics companies, these aircraft present an opportunity to streamline operations and ensure timely delivery even during peak demand or emergencies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $19.6 Billion |

| CAGR | 27.8% |

The Vertical Take-off and Landing (VTOL) segment will generate USD 8 billion by 2034. Its compact footprint, ability to operate without runways, and responsiveness make it highly suitable for dense urban settings, remote delivery missions, and time-sensitive needs like medical logistics. Significant investments in battery efficiency and lightweight composite materials enhance VTOL aircraft's scalability. By delivering cargo where conventional transport fails, these aircraft are reshaping urban air logistics.

The medium payload segment held a 45% share in 2024, supporting logistics scenarios that require capacity and range. With capabilities suited to regional delivery lanes, these aircraft are increasingly used to transport time-sensitive goods like medical supplies, spare parts, and retail inventory. Their scalability and cost-effectiveness allow frequent short-haul operations, making them especially valuable in bridging gaps between remote locations and major distribution centers. As the need for agile, decentralized supply networks grows, the medium payload category is well-positioned to become the backbone of autonomous air freight systems in developed and developing regions.

United States Autonomous Cargo Aircraft Market generated USD 539.3 million in 2024, supported by strong federal backing for unmanned systems integration into national airspace. The country is making major strides in adopting these aircraft for healthcare logistics, emergency response, and urban air mobility. Rapid growth in machine learning, AI-based routing, and disaster-response sensors is boosting operational efficiency, making the U.S. a leader in this segment. Government incentives, evolving FAA guidelines, and rising private-sector participation contribute to accelerated deployment across commercial and public service applications.

Airbus, eHang, Natilus, Elroy Air, and Dronamics are actively shaping the future of the autonomous cargo aircraft market through innovation, partnerships, and scalable technology platforms. These companies emphasize R&D investments in AI-based navigation systems, electric propulsion, and modular cargo designs. Strategic collaborations with logistics networks and supply chain operators are helping to pilot real-world use cases and scale operations. Many are also securing regulatory approvals and airworthiness certifications across multiple geographies to expand their global reach. With a focus on optimizing VTOL designs and integrating advanced sensor technologies, these firms are preparing to meet the growing demand for safe, sustainable, and fast autonomous cargo delivery.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising incidences of natural disasters & humanitarian crises

- 3.3.1.2 Growing proliferation of middle-mile and last-mile delivery solutions

- 3.3.1.3 Increased military and defense investments

- 3.3.1.4 Rapid urbanization in emerging economies

- 3.3.1.5 Growing advancement in AI, navigation & flight control systems

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 Payload and range limitations of electric UAVs

- 3.3.2.2 Cybersecurity threats and communication interference

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic dashboard

Chapter 5 Market Estimates & Forecast, By Technology Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Fixed-wing autonomous cargo aircraft

- 5.3 VTOL (vertical take-off and landing) autonomous aircraft)

Chapter 6 Market Estimates & Forecast, By Payload Capacity, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Small (up to 20 kg)

- 6.3 Medium (20–500 kg)

- 6.4 Large (500 kg and above)

Chapter 7 Market Estimates & Forecast, By Range, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Short-range (Up to 500 kilometers)

- 7.3 Medium-range (500-2,000 kilometers)

- 7.4 Long-range (Over 2,000 kilometers)

Chapter 8 Market Estimates & Forecast, By Autonomy Level, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Fully autonomous

- 8.3 Remotely piloted aircraft

- 8.4 Semi-autonomous

Chapter 9 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 E-commerce & retail logistics

- 9.3 Industrial & offshore logistics

- 9.4 Military & defense

- 9.5 Humanitarian and disaster relief

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Airbus

- 11.2 Dronamics Group Limited

- 11.3 Ehang

- 11.4 Elroy Air

- 11.5 Jestar Logistics

- 11.6 MightyFly

- 11.7 Natilus

- 11.8 Pipistrel

- 11.9 Pyka Inc.

- 11.10 Skydio, Inc.

- 11.11 UAVOS

- 11.12 Unmanned Systems Technology

- 11.13 Xwing

- 11.14 Zipline