|

시장보고서

상품코드

1755214

일렉트로크로믹 재료 시장 : 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Electrochromic Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

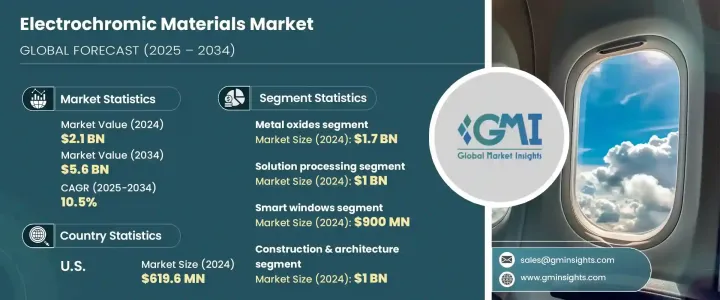

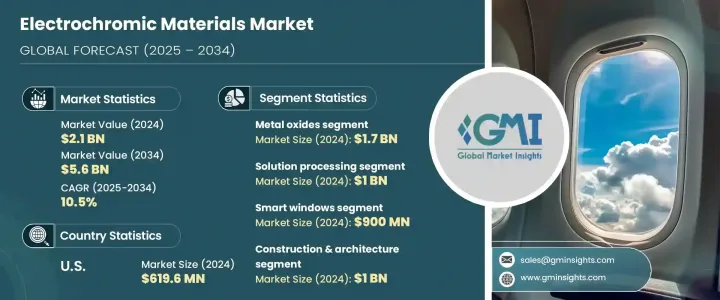

일렉트로크로믹 재료 세계 시장은 2024년에는 21억 달러로 평가되었고 주택과 상업용 건물 모두에서 인기를 끌고 있는 스마트 창 수요 증가에 견인되어 CAGR 10.5%로 성장하여 2034년에는 56억 달러에 이를 것으로 예측되고 있습니다.

이 창문은 빛과 열을 제어하여 에너지 소비를 줄이는 데 도움이 되며 에너지 효율 기준을 충족시키기 위한 녹색 빌딩 프로젝트의 중요한 구성 요소가 되었습니다.

게다가 일렉트로크로믹 재료는 자동차 산업, 특히 자동 조광 미러, 어댑티브 선루프, 사이드 윈도우에의 응용이 확대되고 있습니다. 이러한 기술 혁신은 사용자의 편안함을 향상시키고 눈부심을 줄일뿐만 아니라 자동차 브랜드 힘을 향상시킵니다. 전도성 폴리머와 하이브리드 복합재료를 포함한 재료 과학의 발전은 일렉트로크로믹 재료의 성능과 비용 효율성을 향상시키고 그 채택을 뒷받침하고 있습니다. 에너지 절약이 중요해짐에 따라, 특히 지속가능성 기준이 엄격한 지역에서는 이러한 재료에 대한 수요가 크게 급증하고 있습니다. 에너지 효율을 높이는 능력은 응용 분야에서 중요한 구성 요소가 되어 에너지 소비를 줄이려는 산업에 필수적인 솔루션으로 자리매김하고 있습니다. 그린인증 취득을 목표로 하는 건설 프로젝트부터 연비 개선에 초점을 맞춘 자동차 용도에 이르기까지 이러한 재료는 환경적 및 경제적 목표를 달성하는데 중요한 역할을 하고 있습니다. 범용성, 규제 압력 증가, 지속 가능한 솔루션을 요구하는 소비자 수요가 이러한 재료의 보급을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 21억 달러 |

| 예측 금액 | 56억 달러 |

| CAGR | 10.5% |

2024년 솔루션 처리 분야는 10억 달러를 차지했으며 2034년까지 연평균 복합 성장률(CAGR) 9.6%로 성장할 것으로 예측됩니다.

2024년에 9억 달러로 평가된 스마트 창 분야도 에너지 효율적인 제품에 대한 수요가 높아짐에 따라 급격히 확대될 것으로 예측되고 있습니다.

미국 일렉트로크로믹 재료 2024년 시장 규모는 6억 1,960만 달러로 평가되었고, 스마트 빌딩 및 자동차에서 에너지 절약 기술 수요 증가를 배경으로 2034년까지 연평균 복합 성장률(CAGR) 10%로 성장할 것으로 예측됩니다. 미국 시장은 지속가능성과 에너지 효율이 우수한 기술에 초점을 맞춘 강력한 정부 규제와 기술 혁신과 기술진보를 추진하는 업계 대기업의 적극적인 관여로부터 혜택을 받고 있습니다.

일렉트로크로믹 재료 세계 시장의 주요 기업은 Gentex Corporation, AGC Inc., Sage Electrochromics, Inc.(산고반), PPG Industries, Inc., View, Inc. 등이 포함되어 있습니다. 일렉트로크로믹 재료 시장에서의 지위를 강화하기 위해 기업은 여러 전략에 주력하고 있습니다. 기업은 시장 경쟁력을 높이는 것을 목표로 하고 있습니다. 많은 기업이 주택, 상업시설, 자동차 용도의 스마트 윈도우 솔루션 등 제품 포트폴리오를 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 시장 소개

- 트럼프 정권의 관세 영향 - 구조화된 개요

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS 코드) 참고 : 위의 무역 통계는 주요 국가에 대해서만 제공됩니다

- 주요 수출국

- 국가 1

- 국가 2

- 국가 3

- 주요 수입국

- 국가 1

- 국가 2

- 국가 3

- 주요 수출국

- 업계 밸류체인 분석

- 소재 개요

- 일렉트로크로미즘: 원리와 메커니즘

- 산화 환원 반응과 색 변화의 프로세스

- 광 변조 특성

- 스위칭 속도와 착색 효율

- 내구성과 사이클링 안정성

- 에너지 효율 특성

- 다른 스마트 머티리얼과의 비교

- 시장 역학

- 시장 성장 촉진요인

- 에너지 절약 스마트 윈도우 수요 증가

- 자동차 용도로의 채용 증가

- 일렉트로크로믹 재료에 있어서의 기술의 진보

- 그린 빌딩 인증의 중요성 증가

- 시장 성장 억제요인

- 일렉트로크로믹 디바이스의 초기 비용이 증가

- 일부 재료 유형에서는 스위칭 속도가 제한된다

- 시장 기회

- 시장의 과제

- 시장 성장 촉진요인

- 업계에 미치는 영향요인

- 성장 가능성 분석

- 업계의 잠재적 위험 및 과제

- 규제 프레임워크과 기준

- 에너지 효율 규제

- 건축 기준법

- 자동차 안전기준

- 환경규제

- 성능 시험 기준

- 제조 공정 분석

- 재료 합성 방법

- 박막 퇴적 기술

- 디바이스 제조 공정

- 품질 관리 절차

- 원재료 분석 및 조달 전략

- 가격 분석

- 지속가능성과 환경영향 평가

- PESTEL 분석

- Porter's Five Forces 분석

제4장 경쟁 구도

- 시장 점유율 분석

- 전략적 틀

- 합병과 인수

- 합작투자와 콜라보레이션

- 신제품 개발

- 확대 전략

- 경쟁 벤치마킹

- 벤더 상황

- 경쟁 포지셔닝 매트릭스

- 전략적 대시보드

- 특허 분석과 혁신평가

- 신규 참가자를 위한 시장 진출 전략

- 조사 개발 집약도 분석

제5장 시장 추정 및 예측 : 재료별, 2021년-2034년

- 주요 동향

- 금속 산화물

- 산화텅스텐(WO3)

- 산화니켈(NiO)

- 이산화티탄(TiO2)

- 오산화 바나듐(V2O5)

- 산화 몰리브덴(MoO3)

- 기타 금속 산화물

- 전도성 폴리머

- 폴리아닐린(PANI)

- 폴리피롤(PPy)

- 폴리(3,4-에틸렌디옥시티오펜)(PEDOT)

- 기타 전도성 폴리머

- 비올로겐

- 프루시안 블루 유사체

- 액정

- 하이브리드 및 복합재료

- 기타 일렉트로크로믹 재료

제6장 시장 추정 및 예측 : 기술별, 2021년-2034년

- 주요 동향

- 솔루션 처리

- 졸겔법

- 전착

- 스핀 코팅

- 기타 용액 처리 방법

- 증착

- 물리 증착(PVD)

- 화학 증착(CVD)

- 스퍼터링

- 기타 증착법

- 인쇄 기술

- 잉크젯 인쇄

- 스크린 인쇄

- 기타 인쇄 방법

- 기타 기술

제7장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 스마트 윈도우

- 건축용 창

- 채광창과 지붕창

- 파티션과 프라이버시 유리

- 기타 스마트 윈도우 용도

- 스마트 미러

- 자동차용 미러

- 건축용 미러

- 기타 미러 용도

- 디스플레이

- 전자 종이 디스플레이

- 정보 디스플레이

- 기타 디스플레이 용도

- 자동차 용도

- 선루프

- 백미러

- 사이드 윈도우

- 기타 자동차 용도

- 항공우주용도

- 웨어러블 디바이스

- 에너지 저장 장치

- 기타 용도

제8장 시장 추정 및 예측 : 최종 이용 산업별, 2021년-2034년

- 주요 동향

- 건설 및 아키텍처

- 주택

- 상업 빌딩

- 공공시설

- 기타 건물의 유형

- 자동차 및 운송

- 승용차

- 상용차

- 기타 교통 수단

- 항공우주 및 방어

- 전자기기와 디스플레이

- 해양

- 헬스케어 및 의료

- 기타 최종 이용 산업

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Gentex Corporation

- View, Inc.

- ChromoGenics AB

- Sage Electrochromics, Inc.(Saint-Gobain)

- AGC Inc.

- Magna Glass and Window Company

- Guardian Industries Corp.

- PPG Industries, Inc.

- Kinestral Technologies, Inc.

- E Ink Holdings Inc.

- Gesimat GmbH

- EControl-Glas GmbH &Co. KG

- Merck KGaA

- 3M Company

- Nippon Sheet Glass Co., Ltd.

- Halio, Inc.

- Pleotint LLC

- Research Frontiers Inc.

- Heliotrope Technologies

- SAGE Electrochromics, Inc.

- Polytronix, Inc.

- Chromogenics AB

- Innovative Glass Corporation

- Gauzy Ltd.

- Smart Glass International Ltd.

- SPD Control Systems Corporation

- Diamond Glass

- InvisiShade

- Continental AG

The Global Electrochromic Materials Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 10.5% to reach USD 5.6 billion by 2034, driven by the increasing demand for smart windows, which are gaining popularity in both residential and commercial buildings. These windows help reduce energy consumption by controlling light and heat, making them a key component in green building projects aiming to meet energy efficiency standards.

Additionally, electrochromic materials are seeing increased applications in the automotive industry, particularly in self-dimming mirrors, adaptive sunroofs, and side windows. These innovations not only improve user comfort and reduce glare but also enhance vehicle branding. The advancement of material science, including conducting polymers and hybrid composites, has improved the performance and cost-efficiency of electrochromic materials, driving their adoption. As energy conservation gains importance, particularly in regions with stringent sustainability standards, the demand for these materials is experiencing a significant surge. Their ability to enhance energy efficiency makes them a key component in applications, positioning them as a vital solution for industries seeking to reduce energy consumption. From construction projects aiming for green certifications to automotive applications focused on improving fuel efficiency, these materials play a crucial role in meeting environmental and economic goals. Their versatility, growing regulatory pressure, and consumer demand for sustainable solutions, drive their widespread adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 10.5% |

In 2024, the solution processing segment accounted for USD 1 billion and is expected to grow at a CAGR of 9.6% through 2034. This growth is attributed to the cost-effectiveness and scalability of solution processing methods, which are increasingly used for applications like smart windows and displays. These methods offer versatility, making them compatible with a wide range of substrates, further boosting growth in the architectural and automotive sectors.

The smart windows segment, valued at USD 900 million in 2024, is also projected to expand rapidly, driven by the growing demand for energy-efficient products. These windows help reduce energy consumption in buildings and enhance comfort. Smart mirrors and sunroofs are gaining popularity for their comfort and safety benefits.

U.S. Electrochromic Materials Market was valued at USD 619.6 million in 2024 and is expected to grow at a 10% CAGR through 2034 driven by the increasing demand for energy-saving technologies in smart buildings and vehicles. The U.S. market benefits from strong governmental regulations focused on sustainability and energy-efficient technologies, and the active involvement of leading industry players driving innovation and technical advancements.

Key players in the Global Electrochromic Materials Market include Gentex Corporation, AGC Inc., Sage Electrochromics, Inc. (Saint-Gobain), PPG Industries, Inc., and View, Inc. To strengthen their position in the electrochromic materials market, companies are focusing on multiple strategies. One key approach is the continued investment in research and development to create innovative, high-performance products that cater to the growing demand for energy-efficient applications. By advancing the capabilities of electrochromic materials, companies aim to enhance their market competitiveness. Many are expanding their product portfolios to include smart window solutions for residential, commercial, and automotive applications. In addition, partnerships with construction firms, automotive manufacturers, and governments are vital for securing new market opportunities and ensuring the integration of these technologies into large-scale projects.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research methodology

- 1.2 Research scope & assumptions

- 1.3 List of data sources

- 1.4 Market estimation technique

- 1.5 Market segmentation & breakdown

- 1.6 Research limitations

Chapter 2 Executive Summary

- 2.1 Market snapshot

- 2.2 Segment highlights

- 2.3 Competitive landscape snapshot

- 2.4 Regional market outlook

- 2.5 Key market trends

- 2.6 Future market outlook

Chapter 3 Industry Insights

- 3.1 Market Introduction

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (hs code) Note: The above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.1.1 Country 1

- 3.3.1.2 Country 2

- 3.3.1.3 Country 3

- 3.3.2 Major importing countries

- 3.3.2.1 Country 1

- 3.3.2.2 Country 2

- 3.3.2.3 Country 3

- 3.3.1 Major exporting countries

- 3.4 Industry value chain analysis

- 3.5 Material overview

- 3.5.1 Electrochromism: principles & mechanisms

- 3.5.2 Redox reactions & color change processes

- 3.5.3 Optical modulation properties

- 3.5.4 Switching speed & coloration efficiency

- 3.5.5 Durability & cycling stability

- 3.5.6 Energy efficiency characteristics

- 3.5.7 Comparison with other smart materials

- 3.6 Market dynamics

- 3.6.1 Market drivers

- 3.6.1.1 Rising demand for energy-efficient smart windows

- 3.6.1.2 Increasing adoption in automotive applications

- 3.6.1.3 Technological advancements in electrochromic materials

- 3.6.1.4 Growing emphasis on green building certifications

- 3.6.2 Market restraints

- 3.6.2.1 High initial cost of electrochromic devices

- 3.6.2.2 Limited switching speed for some material types

- 3.6.3 Market opportunities

- 3.6.4 Market challenges

- 3.6.1 Market drivers

- 3.7 Industry impact forces

- 3.7.1 Growth potential analysis

- 3.7.2 Industry pitfalls & challenges

- 3.8 Regulatory framework & standards

- 3.9 Energy efficiency regulations

- 3.9.1 Building codes & standards

- 3.9.2 Automotive safety standards

- 3.9.3 Environmental regulations

- 3.9.4 Performance testing standards

- 3.10 Manufacturing process analysis

- 3.10.1 Material synthesis methods

- 3.10.2 Thin film deposition techniques

- 3.10.3 Device fabrication processes

- 3.10.4 Quality control procedures

- 3.11 Raw material analysis & procurement strategies

- 3.12 Pricing analysis

- 3.13 Sustainability & environmental impact assessment

- 3.14 Pestle analysis

- 3.15 Porter's five forces analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Market Share Analysis

- 4.2 Strategic Framework

- 4.2.1 Mergers & Acquisitions

- 4.2.2 Joint Ventures & Collaborations

- 4.2.3 New Product Developments

- 4.2.4 Expansion Strategies

- 4.3 Competitive Benchmarking

- 4.4 Vendor Landscape

- 4.5 Competitive Positioning Matrix

- 4.6 Strategic Dashboard

- 4.7 Patent Analysis & Innovation Assessment

- 4.8 Market Entry Strategies for New Players

- 4.9 Research & Development Intensity Analysis

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Metal oxides

- 5.2.1 Tungsten oxide (WO3)

- 5.2.2 Nickel oxide (NiO)

- 5.2.3 Titanium dioxide (TiO2)

- 5.2.4 Vanadium pentoxide (V2O5)

- 5.2.5 Molybdenum oxide (MoO3)

- 5.2.6 Other metal oxides

- 5.3 Conducting polymers

- 5.3.1 Polyaniline (PANI)

- 5.3.2 Polypyrrole (PPy)

- 5.3.3 Poly(3,4-ethylenedioxythiophene) (PEDOT)

- 5.3.4 Other conducting polymers

- 5.4 Viologens

- 5.5 Prussian blue analogs

- 5.6 Liquid crystals

- 5.7 Hybrid & composite materials

- 5.8 Other electrochromic materials

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solution processing

- 6.2.1 Sol-gel method

- 6.2.2 Electrodeposition

- 6.2.3 Spin coating

- 6.2.4 Other solution processing methods

- 6.3 Vapor deposition

- 6.3.1 Physical vapor deposition (PVD)

- 6.3.2 Chemical vapor deposition (CVD)

- 6.3.3 Sputtering

- 6.3.4 Other vapor deposition methods

- 6.4 Printing technologies

- 6.4.1 Inkjet printing

- 6.4.2 Screen printing

- 6.4.3 Other printing methods

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Smart windows

- 7.2.1 Architectural windows

- 7.2.2 Skylights & roof windows

- 7.2.3 Partitions & privacy glass

- 7.2.4 Other smart window applications

- 7.3 Smart mirrors

- 7.3.1 Automotive mirrors

- 7.3.2 Architectural mirrors

- 7.3.3 Other mirror applications

- 7.4 Displays

- 7.4.1 E-paper displays

- 7.4.2 Information displays

- 7.4.3 Other display applications

- 7.5 Automotive applications

- 7.5.1 Sunroofs

- 7.5.2 Rearview mirrors

- 7.5.3 Side windows

- 7.5.4 Other automotive applications

- 7.6 Aerospace applications

- 7.7 Wearable devices

- 7.8 Energy storage devices

- 7.9 Other applications

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Construction & architecture

- 8.2.1 Residential buildings

- 8.2.2 Commercial buildings

- 8.2.3 Institutional buildings

- 8.2.4 Other building types

- 8.3 Automotive & transportation

- 8.3.1 Passenger vehicles

- 8.3.2 Commercial vehicles

- 8.3.3 Other transportation

- 8.4 Aerospace & defense

- 8.5 Electronics & displays

- 8.6 Marine

- 8.7 Healthcare & medical

- 8.8 Other end-use industries

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Gentex Corporation

- 10.2 View, Inc.

- 10.3 ChromoGenics AB

- 10.4 Sage Electrochromics, Inc. (Saint-Gobain)

- 10.5 AGC Inc.

- 10.6 Magna Glass and Window Company

- 10.7 Guardian Industries Corp.

- 10.8 PPG Industries, Inc.

- 10.9 Kinestral Technologies, Inc.

- 10.10 E Ink Holdings Inc.

- 10.11 Gesimat GmbH

- 10.12 EControl-Glas GmbH & Co. KG

- 10.13 Merck KGaA

- 10.14 3M Company

- 10.15 Nippon Sheet Glass Co., Ltd.

- 10.16 Halio, Inc.

- 10.17 Pleotint LLC

- 10.18 Research Frontiers Inc.

- 10.19 Heliotrope Technologies

- 10.20 SAGE Electrochromics, Inc.

- 10.21 Polytronix, Inc.

- 10.22 Chromogenics AB

- 10.23 Innovative Glass Corporation

- 10.24 Gauzy Ltd.

- 10.25 Smart Glass International Ltd.

- 10.26 SPD Control Systems Corporation

- 10.27 Diamond Glass

- 10.28 InvisiShade

- 10.29 Continental AG