|

시장보고서

상품코드

1755238

항공 산업 IoT 시장 기회 : 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)IoT in Aviation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

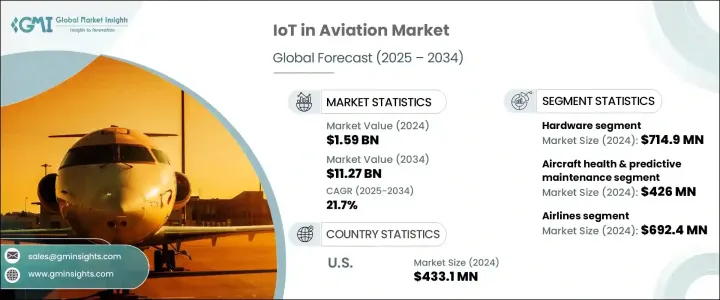

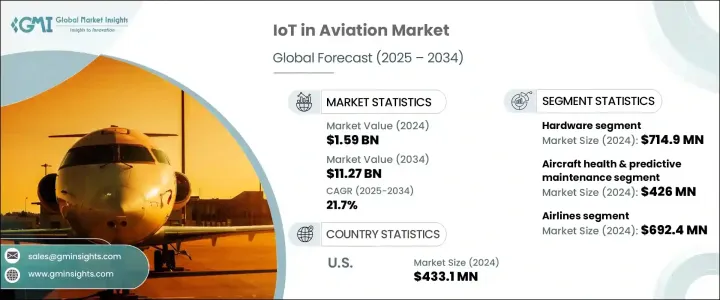

세계의 항공 산업 IoT 시장은 2024년에 15억 9,000만 달러로 평가되었으며 2034년까지는 112억 7,000만 달러에 이를 것으로 예측되며, CAGR 21.7%로 성장할 전망입니다.

이러한 성장은 운영 효율성, 비용 절감, 실시간 의사 결정에 대한 요구가 증가함에 따라 촉진되고 있으며, 항공 업계의 이해 관계자들은 운영을 현대화하기 위해 IoT를 도입하고 있습니다. 전자제품 및 반도체 부품에 대한 관세 부과로 생산 비용이 급증하며 IoT 기기 공급과 공급망 유연성에 차질이 발생했습니다. 이 비용 증가는 제조업체가 흡수하거나 최종 소비자에게 전가되면서 광범위한 채택이 지연되었습니다. 항공 전자 장비, 센서, 연결 모듈 등 핵심 항공기 기술이 특히 영향을 받아 국내 조달로 전환되는 추세가 나타났습니다. 국내 공급업체의 제한된 생산 능력에도 불구하고 이 전환은 단기적인 마찰을 유발했지만, 결국 미국 시장에서 자급자족형 혁신을 촉진했습니다. 이 혼란은 핵심 기술 분야에서의 생산 현지화의 도전 과제와 전략적 우위를 강조했습니다.

실시간 센서 기술은 항공기 운영자가 기내 시스템을 모니터링하고 비행 경로를 최적화하며 연료 소비를 더 효과적으로 관리할 수 있도록 합니다. IoT를 통해 가능해진 예측 유지보수는 엔진 상태, 구조적 안정성, 시스템 성능을 추적함으로써 가동 중단 시간을 줄이고 안전성을 향상시킵니다. 공항과 항공사는 연결된 기술로 구동되는 자동화를 통해 승무원 일정 관리와 수하물 물류를 효율화해 운영 비용을 절감하고 신뢰성을 향상시키고 있습니다. IoT를 통해 제공되는 향상된 승객 서비스는 여행객의 브랜드 충성도를 강화합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 15억 9,000만 달러 |

| 예측 금액 | 112억 7,000만 달러 |

| CAGR | 21.7% |

하드웨어 부문은 항공기 시스템과 제어 센터 간의 강력한 데이터 흐름을 가능하게 하는 센서, 액추에이터 및 통신 모듈에 대한 수요에 힘입어 2024년에 7억 1,490만 달러에 도달했습니다. RFID 및 비콘 기술은 수하물 추적 및 재고 관리를 지원하며, 항공 전자 기기 등급 모듈은 비행 중 중단 없는 연결을 보장합니다. 기내에 설치된 엣지 컴퓨팅 솔루션은 중요한 데이터를 로컬에서 처리하여 지연 시간과 외부 네트워크에 대한 의존성을 최소화합니다. 이러한 기술은 더 안전한 운영과 더 나은 기내 및 지상 서비스 효율성을 가능하게 합니다.

항공기 상태 및 예측 유지보수 용도 부문은 2024년에 4억 2,600만 달러로 평가되었습니다. 이 분야는 센서 데이터와 고급 분석을 사용하여 부품 마모, 엔진 성능 및 시스템 진단을 실시간으로 평가합니다. 예측 모델링은 예기치 않은 고장을 줄이고, 유지보수 작업을 더 잘 계획할 수 있게 하며, 항공기 자산의 운영 수명을 연장합니다.

미국의 항공 산업 IoT 시장은 2024년에 4억 3,310만 달러에 달했습니다. 이 나라는 항공 인프라 전반에 걸쳐 연결 기술의 광범위한 통합으로 인해 선도적인 위치를 유지하고 있습니다. GE Aviation, Cisco Systems Inc., Siemens, Honeywell International Inc., 및 International Business Machines Corporation과 같은 주요 항공우주 기업들은 항공기 및 공항 운영을 위한 IoT 시스템 개발을 주도해 왔습니다. 스마트 캐빈 환경, 유지보수 자동화, 공항 최적화 등 미국 항공 산업의 발전은 미국을 전 세계 항공 산업에서 IoT 도입의 선두 주자로 만들었습니다.

경쟁 우위를 강화하기 위해 IoT 항공 분야의 선도 기업들은 센서 혁신, 실시간 분석, 엣지 컴퓨팅에 대한 R&D 투자를 확대하는 데 주력하고 있습니다. 항공우주 제조업체 및 공항 당국과의 전략적 협력을 통해 신규 및 기존 기종에 걸쳐 IoT 시스템의 신속한 도입이 가능해졌습니다. 이들 기업은 비행 안전에 критически 중요한 시스템에서의 안전한 데이터 전송을 보장하기 위해 사이버 보안에 우선순위를 두고 있습니다. 또한, 기업들은 예측 진단 제공 및 승객 및 화물 운영 효율화를 위해 AI 통합 IoT 프레임워크에 투자해 시장 리더십을 더욱 공고히 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 인사이트

- 산업 생태계 분석

- 트럼프 정권의 관세 분석(하드웨어)

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 산업에 미치는 영향

- 공급측의 영향

- 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향

- 영향을 받는 주요 기업

- 전략적인 산업 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 산업에 미치는 영향요인

- 성장 촉진요인

- 운영 효율성 향상 및 비용 절감

- 승객 경험 개선 및 개인화

- 예측 유지보수 및 안전 기술의 발전

- 스마트 공항 및 연결된 생태계의 성장

- 산업의 잠재적 리스크 및 과제

- 높은 도입 비용

- 사이버 보안 취약성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 솔루션별(2021-2034년)

- 주요 동향

- 하드웨어

- 소프트웨어

- 서비스

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 공급망 및 물류

- 공항 및 지상 업무

- 승객 경험 및 연결성

- 비행 운용 및 항공기관리

- 항공기 상태 및 예측 유지보수

- 항공기의 제조 및 조립

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 항공사

- 공항

- MRO 공급업체

- 항공기 제조업체

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Honeywell International Inc.

- Siemens

- General Electric Company

- International Business Machines Corporation

- Cisco Systems Inc.

- SITA

- Airbus

- The Boeing Company

- Thales

- Lufthansa Technik

- Collins Aerospace

- Panasonic Avionics Corporation

- SAP SE

- Microsoft

- Amadeus IT Group SA

- Palantir Technologies

- Tata Communications Limited

The Global IoT in Aviation Market was valued at USD 1.59 billion in 2024 and is estimated to grow at a CAGR of 21.7% to reach USD 11.27 billion by 2034. The growth is driven by the increasing demand for operational efficiency, cost reduction, and real-time decision-making, aviation stakeholders are embracing IoT to modernize their operations. The implementation of tariffs on electronics and semiconductor components caused a significant uptick in production costs, disrupting IoT device availability and supply chain agility. These increased costs were either absorbed by manufacturers or shifted to end users, slowing widespread adoption. Key aircraft technologies such as avionics hardware, sensors, and connectivity modules were particularly impacted, prompting a shift toward domestic sourcing. Although domestic suppliers offered limited capacity, this transition stimulated short-term friction but eventually encouraged self-reliant innovation in the U.S. market. The disruption highlighted the challenges and strategic advantages of localizing production in critical technology sectors.

Real-time sensor technology allows aircraft operators to monitor onboard systems, optimize flight paths, and manage fuel consumption more effectively. Predictive maintenance enabled by IoT reduces downtime and enhances safety by tracking engine health, structural integrity, and system performance. Airports and airlines streamline crew planning and baggage logistics using automation powered by connected technologies, cutting operational costs and improving reliability. Enhanced passenger services delivered through IoT also foster stronger brand loyalty among travelers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.59 Billion |

| Forecast Value | $11.27 Billion |

| CAGR | 21.7% |

The hardware segment reached USD 714.9 million in 2024, driven by demand for sensors, actuators, and communication modules that enable robust data flow between aircraft systems and control centers. RFID and beacon technology support baggage tracking and inventory control, while avionics-grade modules ensure uninterrupted connectivity in flight. Edge computing solutions installed onboard process critical data locally, minimizing latency and dependency on external networks. These technologies enable safer operations and better in-flight and ground service efficiency.

The aircraft health and predictive maintenance application segment was valued at USD 426 million in 2024. This area uses sensor data and advanced analytics to evaluate component wear, engine performance, and system diagnostics in real-time. Predictive modeling helps reduce unexpected breakdowns, allows better planning of maintenance tasks, and extends the operational lifespan of aircraft assets.

United States IoT in Aviation Market was valued at USD 433.1 million in 2024. The country maintains a leading role owing to the extensive integration of connected technologies across its aviation infrastructure. Major aerospace companies including GE Aviation, Cisco Systems Inc., Siemens, Honeywell International Inc., and International Business Machines Corporation have spearheaded the development of IoT systems for aircraft and airport operations. U.S. aviation advancements in smart cabin environments, maintenance automation, and airport optimization have pushed the country to the forefront of global IoT adoption in aviation.

To strengthen their competitive edge, leading companies in the IoT aviation sector are focusing on scaling R&D investments in sensor innovation, real-time analytics, and edge computing. Strategic collaborations with aerospace manufacturers and airport authorities allow faster deployment of IoT systems across new and existing fleets. These firms prioritize cybersecurity to ensure safe data transmission in flight-critical systems. Additionally, companies are investing in AI-integrated IoT frameworks to deliver predictive diagnostics and streamline passenger and cargo operations, further solidifying their market leadership.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis (Hardware)

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.1.3 Impact on the industry

- 3.2.1.3.1 Supply-side impact

- 3.2.1.3.1.1 Price volatility

- 3.2.1.3.1.2 Supply chain restructuring

- 3.2.1.3.1.3 Production cost implications

- 3.2.1.3.2 Demand-side impact

- 3.2.1.3.2.1 Price transmission to end markets

- 3.2.1.3.2.2 Market share dynamics

- 3.2.1.3.2.3 Consumer response patterns

- 3.2.1.3.1 Supply-side impact

- 3.2.1.4 Key companies impacted

- 3.2.1.5 Strategic industry responses

- 3.2.1.5.1 Supply chain reconfiguration

- 3.2.1.5.2 Pricing and product strategies

- 3.2.1.5.3 Policy engagement

- 3.2.1.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Enhanced operational efficiency and cost savings

- 3.3.1.2 Improved passenger experience and personalization

- 3.3.1.3 Advancements in predictive maintenance and safety

- 3.3.1.4 Growth of smart airports and connected ecosystems

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High implementation costs

- 3.3.2.2 Cybersecurity vulnerabilities

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Solution, 2021 - 2034 (USD million)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD million)

- 6.1 Key trends

- 6.2 Supply chain & logistics

- 6.3 Airport & ground operations

- 6.4 Passenger experience & connectivity

- 6.5 Flight operations & fleet management

- 6.6 Aircraft health & predictive maintenance

- 6.7 Aircraft manufacturing & assembly

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD million)

- 7.1 Key trends

- 7.2 Airlines

- 7.3 Airports

- 7.4 Mro providers

- 7.5 Aircraft manufacturers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Honeywell International Inc.

- 9.2 Siemens

- 9.3 General Electric Company

- 9.4 International Business Machines Corporation

- 9.5 Cisco Systems Inc.

- 9.6 SITA

- 9.7 Airbus

- 9.8 The Boeing Company

- 9.9 Thales

- 9.10 Lufthansa Technik

- 9.11 Collins Aerospace

- 9.12 Panasonic Avionics Corporation

- 9.13 SAP SE

- 9.14 Microsoft

- 9.15 Amadeus IT Group SA

- 9.16 Palantir Technologies

- 9.17 Tata Communications Limited