|

시장보고서

상품코드

1755248

불소 코팅 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Fluorinated Coating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

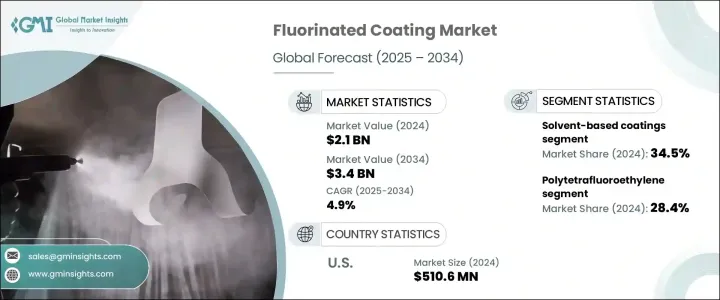

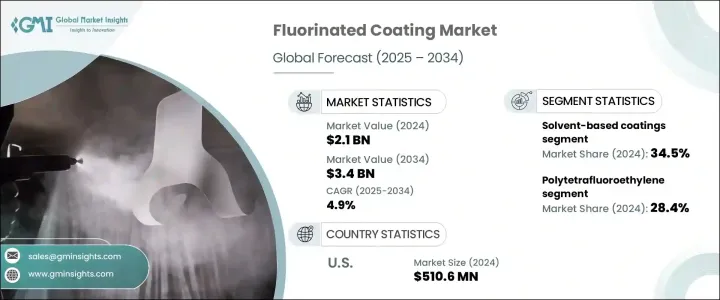

세계의 불소 코팅 시장은 2024년에 21억 달러로 평가되었고 2034년에는 34억 달러에 이를 것으로 추정되며, CAGR 4.9%로 성장할 전망입니다.

이 코팅은 주로 뛰어난 내구성, 열 안정성, 내화학성 및 내식성을 제공하는 불소 중합체 재료를 사용하여 제조됩니다. 이러한 특성으로 인해 다양한 운영 환경에서 장기적인 내구성과 고성능 코팅을 요구하는 산업 분야에서 필수적입니다. 극한 온도부터 화학적으로 반응이 활발한 환경까지, 불소화 코팅은 특히 고습도 및 환경 스트레스가 높은 지역에서 우수한 성능을 지속적으로 입증하고 있습니다.

환경 퇴화에 저항할 수 있는 고급 재료에 대한 수요가 증가함에 따라, 효율성과 재료의 수명을 중시하는 산업 분야에서 이러한 코팅의 채택이 증가하고 있습니다. 또한 교통 및 인프라 건설 분야의 투자 증가로 핵심 자산의 서비스 수명을 연장하고 장기 유지보수 비용을 줄이기 위한 보호 코팅의 사용이 확대되고 있습니다. 기술 혁신, 지속 가능성으로의 규제 변화, 환경 영향 감소에 대한 요구는 제조업체들이 수성 기반 및 자외선 경화형 등 환경 친화적 코팅 솔루션을 채택하도록 장려하고 있습니다.

| 시장 범위 | |

|---|---|

| 시장 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 21억 달러 |

| 예측 금액 | 34억 달러 |

| CAGR | 4.9% |

제품 유형 측면에서 폴리테트라플루오로에틸렌(PTFE)은 2024년에 전 세계 시장의 28.4% 이상을 차지했습니다. 낮은 표면 에너지와 비반응성 특성으로 알려진 PTFE는 최소한의 마찰, 열 내구성, 강한 화학 저항성이 필요한 응용 분야에서 필수 재료로 자리 잡았습니다. 극한 온도와 부식성 물질에 노출되는 다양한 최종 사용 산업 분야에서 널리 사용되며, 스트레스 하에서도 안정적인 성능을 보여 기계적 마모나 화학 노출에 노출된 부품에 이상적입니다.

기술별로 분류할 때, 용매 기반 코팅은 2024년 시장 점유율의 약 34.5%를 차지했습니다. 이들의 장기적인 우위는 우수한 접착력, 긴 수명, 극한 환경에서의 내구성에 기인합니다. 이러한 코팅은 공격적인 환경에서도 신뢰성 있게 작동하며, 이는 고도의 기계적 및 열적 부하가 발생하는 산업 분야에서 널리 사용되는 이유입니다. 휘발성 유기 화합물(VOC) 배출에 대한 규제 압박에도 불구하고, 용매 기반 코팅은 산업적 이점 덕분에 여전히 견고한 입지를 유지하고 있습니다. 그러나 친환경 솔루션에 대한 관심이 높아지면서 업계의 미래는 점차 변화하고 있습니다. 수성 코팅은 특히 엄격한 배출 규제가 시행되는 지역에서 주목을 받고 있으며, UV 경화형 코팅은 빠른 경화 속도와 낮은 에너지 요구 사항 덕분에 정밀 제조 분야에서 점점 더 실용성이 높아지고 있습니다.

기판의 경우, 2024년에는 금속이 전 세계 시장에서 선두 위치를 차지했습니다. 금속은 제조업에서 광범위하게 사용되며, 날씨, 화학 물질 및 열에 노출되기 때문에 불소 코팅에 적합한 후보입니다. 이러한 코팅은 부식 및 산화를 방지하는 장벽을 제공하여 구조 부품 및 장비의 수명을 연장하는 데 필수적입니다. 플라스틱, 복합 재료 및 콘크리트와 같은 다른 기판도 특히 내후성 마감재가 필요한 인프라 프로젝트에서 수요가 증가하고 있습니다.

성능 특성 측면에서 2024년 시장에서는 화학 저항성이 가장 중요한 요소로 부상했습니다. 많은 산업 분야에서는 공격적인 화학 물질을 다루며, 이러한 환경에서 사용되는 장비는 이러한 노출을 견딜 수 있도록 코팅이 필요합니다. 불소화 코팅은 표면 퇴화, 장비 고장, 오염 위험을 방지하기 때문에 선호됩니다. 탱크, 파이프라인, 가공 장비의 신뢰할 수 있는 라이닝으로 작용하는 능력은 중단 없는 운영과 안전을 보장합니다. 열 안정성, 전기 절연성, 저마찰 표면과 같은 특성도 특히 고정밀 및 고성능 응용 분야에서 이 코팅의 채택에 크게 기여하고 있습니다.

용도별로는 항공우주 및 방위 부문이 2024년에 가장 큰 비중을 차지했습니다. 이러한 산업에서는 극한 환경을 견딜 수 있는 재료가 필요하며, 불소 코팅은 내열성, 경량성, 장기적인 보호 기능을 제공하여 이러한 요구를 충족합니다. 한편, 부식성 물질과 고온에 노출되는 기계에 코팅이 널리 사용됨에 따라 산업 장비가 시장 점유율에서 가장 큰 비중을 차지했습니다. 상업 및 주거용 응용 분야에서 비접착성, 세척이 쉬운 표면에 대한 수요가 증가함에 따라 식품 관련 부문도 여전히 강세를 보이고 있습니다.

지역별 분석에서 미국 불소 코팅 시장은 2024년에 5억 1,060만 달러를 넘어섰습니다. 미국은 잘 구축된 산업 기반, 꾸준한 기술 발전, 제품 성능에 대한 지속적인 집중을 바탕으로 북미에서 계속 선두를 달리고 있습니다. 고품질의 내구성 있는 코팅에 대한 필요성은 인프라 및 제조 부문의 지속적인 발전으로 더욱 확대되고 있습니다. 유지 보수가 쉬운 재료를 선호하는 소비자 트렌드도 가정용 및 실외용 제품 응용 분야의 성장을 뒷받침하고 있습니다.

시장은 여전히 중간 수준의 집중도를 유지하고 있으며, 몇몇 주요 기업이 상당한 시장 점유율을 차지하고 있습니다. 경쟁의 초점은 제품 혁신, 규제 준수, 특정 산업에 맞춤형 솔루션을 제공하는 데 집중되고 있습니다. 선도 기업들은 표면 보호 기능을 지속적으로 강화하고 고성장 응용 분야로의 진출을 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국

- 주요 수입국

참고: 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

- 영향요인

- 시장 성장 촉진요인

- 시장 성장 억제요인

- 시장 기회

- 시장의 과제

- 제품 개요

- 불소 폴리머의 화학과 구조

- 성능 특성

- 내약품성

- 열안정성

- 비점착성 및 저마찰성

- 기후 저항성 및 내구성

- 다른 코팅 기술과의 비교

- 제조 공정 분석

- 수지 생산

- 제형 기술

- 적용 방법

- 경화 공정

- 품질 관리 절차

- 규제 상황

- 성장 가능성 분석

- 가격 분석(USD/톤, 2021-2034년)

- 지속가능성과 환경영향 평가

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 시장 점유율 분석

- 전략 틀

- 합병과 인수

- 합작투자와 협업

- 신제품 개발

- 확대 전략

- 경쟁 벤치마킹

- 벤더 상황

- 경쟁 포지셔닝 매트릭스

- 전략적 대시보드

- 특허 분석과 혁신평가

- 신규 참가자 시장 진출 전략

- 배전망 분석

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 폴리테트라플루오로에틸렌(PTFE)

- 순수 PTFE 코팅

- PTFE 기반 복합 코팅

- 개질 PTFE 코팅

- 폴리비닐리덴 플루오라이드(PVDF)

- PVDF 호모폴리머 코팅

- PVDF 호모폴리머 코팅

- 개질 PVDF 코팅

- 불소화 에틸렌 프로필렌

- 퍼플루오로알콕시알칸

- 에틸렌테트라플루오로에틸렌

- 에틸렌클로로트리플루오로에틸렌

- 폴리클로로트리플루오로에틸렌

- 기타

제6장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 용매 기반 코팅

- 수성 코팅

- 분말 코팅

- UV 경화 코팅

- 기타

제7장 시장 추계 및 예측 : 기재별(2021-2034년)

- 주요 동향

- 금속

- 강철

- 알루미늄

- 기타

- 플라스틱 및 복합재료

- 유리

- 콘크리트 및 석재

- 기타

제8장 시장 추계 및 예측 : 성능 속성별(2021-2034년)

- 주요 동향

- 내약품성

- 내후성

- 비점착성 및 저마찰성

- 열안정성

- 전기 절연

- 부식 방지

- 기타

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 산업기기

- 화학처리장치

- 석유 및 가스 기기

- 식품 가공 장비

- 의약품 기기

- 기타

- 건축 및 건설

- 건축용 코팅

- 지붕

- 외관과 외장

- 기타

- 자동차 및 운송

- 외장 부품

- 내부 부품

- 내장 부품

- 기타

- 조리기구와 식품접촉

- 비접착 조리 도구

- 베이킹 용기

- 식품 가공 장비

- 기타

- 전자 및 전기

- PCB 코팅

- 와이어 및 케이블 코팅

- 반도체 용도

- 기타

- 항공우주 및 방위

- 해양

- 헬스케어 및 의료

- 기타

제10장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 공업제조업

- 화학약품

- 석유 및 가스

- 발전

- 기타

- 건축 및 건설

- 자동차 및 운송

- 소비재

- 조리기구 및 주방용품

- 가전제품

- 기타

- 전자 및 반도체

- 항공우주 및 방위

- 식품 및 음료

- 헬스케어&의약품

- 기타

제11장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제12장 기업 프로파일

- 3M Company

- AFT Fluorotec

- AGC Chemicals Americas

- AGC Inc.

- AkzoNobel NV

- Arkema

- Beckers Group

- Daikin Industries

- Dow

- DuPont

- Fluorotherm Polymers

- Gujarat Fluorochemicals

- Jotun A/S

- Nippon Paint Holdings

- PPG Industries, Inc.

- Sherwin-Williams Company

- Solvay SA

- The Chemours Company

- Whitford Corporation

The Global Fluorinated Coating Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 3.4 billion by 2034. These coatings are primarily formulated using fluoropolymer materials that offer outstanding durability, thermal stability, and resistance to chemicals and corrosion. These properties make them vital for industries that demand long-lasting, high-performance coatings across various operational environments. From extreme temperatures to chemically reactive surroundings, fluorinated coatings continue to demonstrate strong performance, particularly in regions prone to high humidity and environmental stress.

As the demand for advanced materials capable of resisting environmental degradation grows, these coatings are seeing increased adoption across sectors that prioritize efficiency and longevity in materials. Moreover, investments in transportation and civil infrastructure have led to greater use of protective coatings designed to increase the service life of key assets while also reducing long-term maintenance costs. Technological innovations, regulatory shifts toward sustainability, and the push for lower environmental impact are encouraging manufacturers to adopt eco-conscious coating solutions, including water-based and UV-curable alternatives.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 4.9% |

In terms of product type, polytetrafluoroethylene (PTFE) accounted for over 28.4% of the global market in 2024. Known for its low surface energy and non-reactive nature, PTFE has become a staple material for applications that require minimal friction, thermal endurance, and strong chemical resistance. Its utility spans a broad spectrum of end-use sectors where exposure to extreme temperatures and corrosive agents is common. PTFE is widely used in manufacturing processes due to its stable behavior under stress, making it ideal for components exposed to mechanical wear or chemical exposure.

When categorized by technology, solvent-based coatings captured nearly 34.5% of the market share in 2024. Their long-standing dominance is attributed to superior adhesion, extended service life, and resilience in tough operating conditions. These coatings perform reliably under aggressive environments, which explains their widespread use in sectors involving high mechanical and thermal loads. Despite regulatory pressure around volatile organic compound (VOC) emissions, solvent-based coatings continue to maintain a solid presence due to their industrial advantages. However, rising interest in eco-friendly solutions is gradually shifting the industry landscape. Waterborne coatings are gaining traction, especially in regions enforcing stricter emission norms, while UV-curable coatings are becoming increasingly viable in precision manufacturing thanks to their rapid curing and low energy requirements.

Based on substrate, metal held the leading position in the global market in 2024. Metals are extensively used in manufacturing, and their exposure to weather, chemicals, and heat makes them suitable candidates for fluorinated coatings. These coatings provide a barrier against corrosion and oxidation, making them essential for extending the life of structural components and equipment. Other substrates such as plastics, composites, and concrete are also witnessing growing demand, particularly in infrastructure projects requiring weather-resistant finishes.

Regarding performance attributes, chemical resistance led the market in 2024. Many industrial sectors handle aggressive chemicals, and equipment used in these settings must be coated to withstand such exposure. Fluorinated coatings are preferred because they prevent surface degradation, equipment failure, and contamination risks. Their ability to act as reliable linings for tanks, pipelines, and processing equipment ensures uninterrupted operation and safety. Properties like thermal stability, electrical insulation, and low-friction surfaces also contribute significantly to their adoption, particularly in high-precision and high-performance applications.

By application, the aerospace and defense segment emerged as the dominant category in 2024. These industries require materials that can endure extreme environments, and fluorinated coatings meet that demand by offering heat resistance, lightweight performance, and long-term protection. Meanwhile, industrial equipment claimed the largest share of the market due to the widespread use of coatings in machinery exposed to corrosive substances and elevated temperatures. The food-related segment also remains strong as demand for non-stick, easy-clean surfaces grows in commercial and residential applications.

In regional analysis, the United States fluorinated coating market surpassed USD 510.6 million in 2024. The country continues to lead in North America, backed by a well-established industrial base, steady technological advancements, and an ongoing focus on product performance. The need for high-quality, durable coatings is further amplified by the continuous development of infrastructure and manufacturing sectors. Consumer trends favoring easy-maintenance materials also support growth in household and outdoor product applications.

The market remains moderately consolidated, with several key players commanding significant shares. Competitive focus revolves around product innovation, regulatory compliance, and customized solutions tailored for specific industries. Leading companies are consistently enhancing surface protection capabilities and expanding their reach across high-growth application areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

Note: the above trade statistics will be provided for key countries only.

- 3.4 Impact forces

- 3.4.1 Market drivers

- 3.4.2 Market restraints

- 3.4.3 Market opportunities

- 3.4.4 market challenges

- 3.5 Product overview

- 3.5.1 Fluoropolymer chemistry & structure

- 3.5.2 Performance characteristics

- 3.5.3 Chemical resistance properties

- 3.5.4 Thermal stability

- 3.5.5 Non-stick & low friction properties

- 3.5.6 Weather resistance & durability

- 3.5.7 Comparison with other coating technologies

- 3.6 Manufacturing process analysis

- 3.6.1 Resin production

- 3.6.2 Formulation techniques

- 3.6.3 Application methods

- 3.6.4 Curing processes

- 3.6.5 Quality control procedures

- 3.7 Regulatory landscape

- 3.8 Growth potential analysis

- 3.9 Pricing analysis (USD/Tons) 2021-2034

- 3.10 Sustainability & environmental impact assessment

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Market share analysis

- 4.2 Strategic framework

- 4.2.1 Mergers & acquisitions

- 4.2.2 Joint ventures & collaborations

- 4.2.3 New product developments

- 4.2.4 Expansion strategies

- 4.3 Competitive benchmarking

- 4.4 Vendor landscape

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Patent analysis & innovation assessment

- 4.8 Market entry strategies for new players

- 4.9 Distribution network analysis

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polytetrafluoroethylene

- 5.2.1 Pure PTFE coatings

- 5.2.2 PTFE-based composite coatings

- 5.2.3 Modified PTFE coatings

- 5.3 Polyvinylidene fluoride

- 5.3.1 PVDF homopolymer coatings

- 5.3.2 PVDF copolymer coatings

- 5.3.3 Modified PVDF coatings

- 5.4 Fluorinated ethylene propylene

- 5.5 Perfluoroalkoxy alkane

- 5.6 Ethylene tetrafluoroethylene

- 5.7 Ethylene chlorotrifluoroethylene

- 5.8 Polychlorotrifluoroethylene

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solvent-based coatings

- 6.3 Water-based coatings

- 6.4 Powder coatings

- 6.5 UV-curable coatings

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Substrate, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Metal

- 7.2.1 Steel

- 7.2.2 Aluminum

- 7.2.3 Others

- 7.3 Plastic & composites

- 7.4 Glass

- 7.5 Concrete & masonry

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Performance Attribute, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Chemical resistance

- 8.3 Weather resistance

- 8.4 Non-stick/low friction

- 8.5 Thermal stability

- 8.6 Electrical insulation

- 8.7 Corrosion protection

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Industrial equipment

- 9.2.1 Chemical processing equipment

- 9.2.2 Oil & gas equipment

- 9.2.3 Food processing equipment

- 9.2.4 Pharmaceutical equipment

- 9.2.5 Others

- 9.3 Building & construction

- 9.3.1 Architectural coatings

- 9.3.2 Roofing materials

- 9.3.3 Facades & cladding

- 9.3.4 Others

- 9.4 Automotive & transportation

- 9.4.1 Exterior components

- 9.4.2 Interior components

- 9.4.3 Under-the-hood applications

- 9.4.4 Others

- 9.5 Cookware & food contact

- 9.5.1 Non-Stick cookware

- 9.5.2 Bakeware

- 9.5.3 Food processing equipment

- 9.5.4 Others

- 9.6 Electronics & electrical

- 9.6.1 PCB coatings

- 9.6.2 Wire & cable coatings

- 9.6.3 Semiconductor applications

- 9.6.4 Others

- 9.7 Aerospace & defense

- 9.8 Marine

- 9.9 Healthcare & medical

- 9.10 Others

Chapter 10 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Industrial manufacturing

- 10.2.1 Chemical

- 10.2.2 Oil & gas

- 10.2.3 Power generation

- 10.2.4 Others

- 10.3 Building & construction

- 10.4 Automotive & transportation

- 10.5 Consumer goods

- 10.5.1 Cookware & kitchenware

- 10.5.2 Appliances

- 10.5.3 Others

- 10.6 Electronics & semiconductors

- 10.7 Aerospace & defense

- 10.8 Food & beverage

- 10.9 Healthcare & pharmaceutical

- 10.10 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 3M Company

- 12.2 AFT Fluorotec

- 12.3 AGC Chemicals Americas

- 12.4 AGC Inc.

- 12.5 AkzoNobel N.V.

- 12.6 Arkema

- 12.7 Beckers Group

- 12.8 Daikin Industries

- 12.9 Dow

- 12.10 DuPont

- 12.11 Fluorotherm Polymers

- 12.12 Gujarat Fluorochemicals

- 12.13 Jotun A/S

- 12.14 Nippon Paint Holdings

- 12.15 PPG Industries, Inc.

- 12.16 Sherwin-Williams Company

- 12.17 Solvay S.A.

- 12.18 The Chemours Company

- 12.19 Whitford Corporation