|

시장보고서

상품코드

1755266

철도 슬라이딩 베어링 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Railway Sliding Bearing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

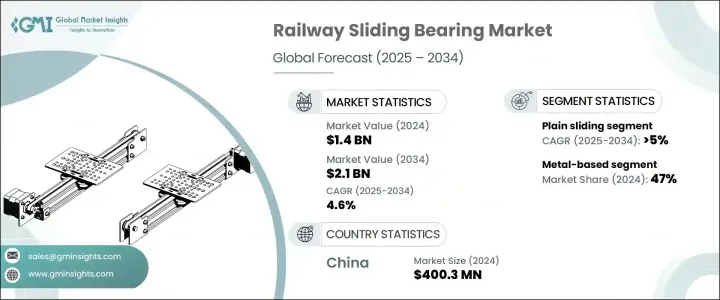

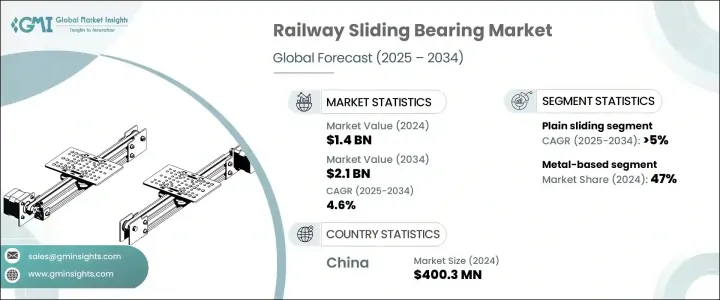

세계의 철도 슬라이딩 베어링 시장 규모는 2024년에 14억 달러로 평가되었고, 2034년에는 21억 달러에 이를 것으로 예측되고며, CAGR 4.6%로 성장할 전망입니다. 이러한 성장은 전 세계적으로 철도 인프라 프로젝트가 확대되고 고속 철도 시스템이 인기를 끌고 있는 데에 크게 촉진되고 있습니다. 운송 산업이 더 빠르고 효율적이며 지속 가능한 솔루션으로 전환됨에 따라 슬라이딩 베어링은 현대 철도 네트워크의 필수 구성 요소로 자리매김하고 있습니다. 이러한 베어링은 더 이상 기본적인 기계 부품으로 간주되지 않으며, 성능, 안전성, 신뢰성을 보장하는 데 결정적인 역할을 합니다.

화물 통로, 지하철 철도, 고속 여객 노선에 대한 국가들의 대규모 투자로 인해 극한의 운영 조건을 견딜 수 있도록 설계된 고성능 슬라이딩 베어링에 대한 의존도가 증가하고 있습니다. 이에는 중량 화물, 극한 속도, 변동하는 환경 스트레스 등이 포함됩니다. 슬라이딩 베어링은 산업과 함께 진화하며, 새로운 재료, 디지털 진단 기술, 구조적 혁신을 도입해 교통 효율성과 인프라 복원력 향상을 목표로 하는 광범위한 목표와 일치하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 14억 달러 |

| 예측 금액 | 21억 달러 |

| CAGR | 4.6% |

고성능 베어링 시스템에 대한 수요는 최소한의 유지보수, 우수한 차축 효율성 및 첨단 보기 플랫폼과의 통합에 대한 요구로 인해 증가하고 있습니다. 제조업체들은 복합 재료를 활용하고, 스마트 모니터링 기능을 통합하며, 장기적인 신뢰성을 향상시키는 혁신적인 베어링 솔루션을 개발하여 이러한 요구에 대응하고 있습니다. 이러한 변화는 슬라이딩 베어링 부문을 기술 선진 시장 부문으로 변화시키고 있으며, 지능형 및 미래 준비형 철도 시스템의 진화를 지원하고 있습니다. 전 세계 철도 전략이 속도, 지속 가능성 및 내구성에 점점 더 초점을 맞추고 있는 가운데, 베어링 공급업체들은 이러한 기대에 부응하기 위해 제품을 조정하고 있으며, 현대 철도 생태계에서 자신의 가치를 강화하고 있습니다.

2024년에 플레인 슬라이딩 베어링 부문은 27%의 점유율을 차지했으며, 2034년까지 연평균 5%의 성장률을 보일 것으로 예상됩니다. 이 베어링은 화물 및 여객 철도 운영에서 축방향 및 반경방향 하중 처리, 기계적 마찰 감소, 부품의 부드러운 움직임을 지원하는 핵심 역할을 수행합니다. 신뢰성 있는 구조, 비용 효율적인 제조 과정, 하중 처리 능력으로 인해 플레인 슬라이딩 베어링은 다양한 철도 차량 클래스의 bogie, 브레이크 어셈블리, 서스펜션 메커니즘에 선호되는 옵션으로 자리매김했습니다. 그들의 효율성은 열차 안정성 향상과 가동 중단 시간 감소에 직접 기여하여 철도 산업에서 필수적인 요소로 인정받고 있습니다.

금속 기반 슬라이딩 베어링은 2024년 시장 점유율의 47%를 차지했으며, 2025년부터 2034년까지 연평균 성장률(CAGR) 5%로 성장할 것으로 예상됩니다. 이 베어링은 우수한 기계적 내구성, 마모 저항성, 열 저항성을 갖추어 엄격한 철도 환경에 적합합니다. 금속 기반 옵션은 차축 지지대부터 서스펜션 조인트 및 브레이크 시스템에 이르기까지 다양한 응용 분야에 널리 사용됩니다. 고속 및 고부하 조건에서 신뢰할 수 있는 성능을 발휘하기 때문에 특히 인프라 업그레이드가 가속화되고 있는 시장에서 널리 사용되고 있습니다. 대규모 화물 및 고속 네트워크에 투자하는 지역은 수명이 길고 구조가 견고한 이 베어링에 특히 주목하고 있습니다.

중국의 철도 슬라이딩 베어링 시장은 2024년에 63.3%의 점유율을 차지하고 4억 3십만 달러의 매출을 올렸습니다. 중국의 우위는 화물, 지하철 및 고속 열차 운영을 포괄하는 광범위한 철도 개발 전략에서 비롯됩니다. 철도 차량의 규모와 지속적인 인프라 투자는 첨단 슬라이딩 베어링에 대한 지속적인 수요를 촉진했습니다. 현지 베어링 제조업체들은 국내 및 전 세계 프로젝트 요구 사항에 부합하는 고성능, 자체 윤활 및 부식 방지 부품을 생산하기 위해 역량을 강화하고 있습니다. 정교한 재료, 엄격한 공차 엔지니어링 및 유지보수가 쉬운 기능을 활용하여 중국은 이 부문의 산업을 계속해서 선도하고 있습니다.

세계의 철도 슬라이딩 베어링 시장 진출 기업으로는 JTEKT, The Timken Company, MinebeaMitsumi, NTN, NSK, GGB, ZKL Group, Schaeffler Group, Liebherr Group 및 AB SKF 등이 있습니다. 철도 슬라이딩 베어링 부문에서 시장 지위를 강화하기 위해 기업들은 혁신, 재료 개발 및 글로벌 확장에 주력하고 있습니다. 주요 전략 중 하나는 극한 운영 조건에서 유지보수를 줄이고 내구성을 향상시키는 복합 재료와 자체 윤활 재료를 사용한 고성능 베어링 개발입니다. 기업들은 또한 진화하는 bogie 기술과의 호환성을 높이기 위해 정밀 공학에 투자하고 있습니다. 철도 OEM 및 인프라 공급업체와의 협력을 통해 기업들은 특정 철도 차량 요구사항에 맞는 맞춤형 솔루션을 제공할 수 있습니다. 또한 제조업체들은 철도 개발 계획이 활발한 신흥 시장에서 시장 점유율을 확대하기 위해 노력하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역 및 국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 산업에 미치는 영향요인

- 성장 촉진요인

- 철도 인프라 프로젝트 확대

- 고속철도 수요 증가

- 화물 수송 증가

- 베어링 재료의 기술적 발전

- 산업의 잠재적 리스크 및 과제

- 고급 베어링의 높은 초기 비용

- 엄격한 품질 기준 및 인증

- 시장 기회

- 도시 이동 시스템의 확장

- 예측 유지 보수를 위한 스마트 베어링의 채택

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경 측면

- 지속 가능한 사례

- 폐기물 삭감 전략

- 생산에 있어서의 에너지 효율

- 친환경 활동

- 탄소 발자국의 고려

- 이용 사례

- 최상의 시나리오

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카 항공

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확대계획과 자금조달

제5장 시장 추정 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 플레인 슬라이드

- 구면 슬라이드

- 원통형 슬라이드

- 플랜지 부착 슬라이드

- 스러스트 슬라이드

- 맞춤형 및 복합재료

제6장 시장 추정 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 금속 기반

- 폴리머 기반

- 복합재료 베어링

- 세라믹 기반

제7장 시장 추정 및 예측 : 전철별(2021-2034년)

- 주요 동향

- 화물열차

- 여객열차

- 고속열차

- 경전철 및 트램

- 지하철

- 모노레일

제8장 시장 추정 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 리셀러

- 온라인 플랫폼

제9장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- AB SKF

- ABC Bearings

- Beijing Bearing Manufacturing

- Boca Bearings

- China Railway Rolling Stock Corporation(CRRC)

- Emerson Bearing Company

- FAG Bearings

- GGB

- JTEKT Corporation

- Liebherr Group

- MinebeaMitsumi

- NSK

- NTN Industrial Bearings

- Rexnord Corporation

- RHP Bearings

- Schaeffler Group

- SKF USA

- Taikisha

- Timken Aerospace Bearings

- ZKL Group

The Global Railway Sliding Bearing Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 2.1 billion by 2034. This growth is largely driven by expanding rail infrastructure projects worldwide and the increasing popularity of high-speed rail systems. As the transportation sector shifts toward faster, more efficient, and more sustainable solutions, sliding bearings are becoming essential components in modern rail networks. These bearings are no longer regarded as basic mechanical parts-they now play a critical role in ensuring performance, safety, and reliability.

With countries investing heavily in freight corridors, metro rail, and high-speed passenger lines, there is a growing reliance on high-grade sliding bearings designed to withstand intense operational conditions. These include heavy loads, extreme speeds, and fluctuating environmental stresses. Sliding bearings are evolving alongside the industry, incorporating new materials, digital diagnostics, and structural advancements that align with broader goals of improving transportation efficiency and infrastructure resilience.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $2.1 Billion |

| CAGR | 4.6% |

The demand for high-performance bearing systems is rising due to the need for minimal maintenance, superior axle efficiency, and integration with advanced bogie platforms. Manufacturers are responding by developing innovative bearing solutions that utilize composite materials, incorporate smart monitoring features, and enhance long-term reliability. These changes are transforming the sliding bearing segment into a technology-forward market segment, supporting the evolution of intelligent and future-ready railway systems. As global rail strategies increasingly focus on speed, sustainability, and durability, bearing providers are adapting their offerings to meet these expectations, reinforcing their value in the modern rail ecosystem.

In 2024, the plain sliding bearings segment held a 27% share and is projected to grow at a CAGR of 5% throughout 2034. These bearings serve critical roles in freight and passenger rail operations, offering essential support for handling axial and radial loads, reducing mechanical friction, and facilitating smooth component movement. With their reliable structure, cost-effective manufacturing, and load-handling capability, plain sliding bearings remain a favored option for use in bogies, brake assemblies, and suspension mechanisms across various rail vehicle classes. Their efficiency contributes directly to improved train stability and reduced downtime, making them indispensable in the rail industry.

Metal-based sliding bearings represented 47% share in 2024 and are also expected to grow at a CAGR of 5% from 2025 - 2034. These bearings are known for their exceptional mechanical durability, wear resistance, and heat tolerance, making them ideal for rigorous rail environments. Metal-based options are widely implemented in applications ranging from axle supports to suspension joints and brake systems. Their reliable performance under high-speed and heavy-load conditions continues to drive their widespread use, particularly in markets where infrastructure upgrades are accelerating. Regions investing in large-scale freight and high-speed networks are particularly focused on these bearings for their extended lifespan and robust structural benefits.

China Railway Sliding Bearing Market held a 63.3% share and generated USD 400.3 million in 2024. The country's dominance stems from its expansive rail development strategy, which encompasses freight, metro, and high-speed train operations. The scale of its rolling stock and continued infrastructure investments have driven consistent demand for advanced sliding bearings. Local bearing manufacturers are enhancing their capabilities to produce high-performance, self-lubricating, and corrosion-resistant components that align with both domestic and global project requirements. Using sophisticated materials, tight-tolerance engineering, and maintenance-friendly features, China continues to set the pace in this segment of the industry.

Key industry participants in the Global Railway Sliding Bearing Market include JTEKT, The Timken Company, MinebeaMitsumi, NTN, NSK, GGB, ZKL Group, Schaeffler Group, Liebherr Group, and AB SKF. To strengthen their market position in the railway sliding bearing sector, companies are focusing on innovation, material advancement, and global expansion. One major strategy is the development of high-performance bearings using composite and self-lubricating materials that reduce maintenance and improve durability under extreme operating conditions. Firms are also investing in precision engineering to enhance load-bearing capacity and system compatibility with evolving bogie technologies. Collaborations with rail OEMs and infrastructure providers allow companies to customize solutions for specific rolling stock requirements. Additionally, manufacturers are expanding their footprint in emerging markets with strong rail development agendas.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Train

- 2.2.5 Sales channel

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of rail infrastructure projects

- 3.2.1.2 Rising demand for high-speed rail

- 3.2.1.3 Increasing freight transportation

- 3.2.1.4 Technological advancements in bearing materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial cost of advanced bearings

- 3.2.2.2 Stringent quality standards & certifications

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of urban mobility systems

- 3.2.3.2 Adoption of smart bearings for predictive maintenance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.10 Export and import

- 3.11 Cost breakdown analysis

- 3.12 Patent analysis

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Use cases

- 3.15 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Plain sliding

- 5.3 Spherical sliding

- 5.4 Cylindrical sliding

- 5.5 Flanged sliding

- 5.6 Thrust sliding

- 5.7 Custom/Composite

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Metal-based

- 6.3 Polymer-based

- 6.4 Composite bearings

- 6.5 Ceramic-based

Chapter 7 Market Estimates & Forecast, By Train, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Freight trains

- 7.3 Passenger trains

- 7.4 High-Speed trains

- 7.5 Light Rail/Trams

- 7.6 Metro/Subway systems

- 7.7 Monorails

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Distributors/Dealers

- 8.4 Online platforms

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AB SKF

- 11.2 ABC Bearings

- 11.3 Beijing Bearing Manufacturing

- 11.4 Boca Bearings

- 11.5 China Railway Rolling Stock Corporation (CRRC)

- 11.6 Emerson Bearing Company

- 11.7 FAG Bearings

- 11.8 GGB

- 11.9 JTEKT Corporation

- 11.10 Liebherr Group

- 11.11 MinebeaMitsumi

- 11.12 NSK

- 11.13 NTN Industrial Bearings

- 11.14 Rexnord Corporation

- 11.15 RHP Bearings

- 11.16 Schaeffler Group

- 11.17 SKF USA

- 11.18 Taikisha

- 11.19 Timken Aerospace Bearings

- 11.20 ZKL Group

(주말 및 공휴일 제외)