|

시장보고서

상품코드

1755291

자동차 고장 회로 컨트롤러 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Automotive Fault Circuit Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

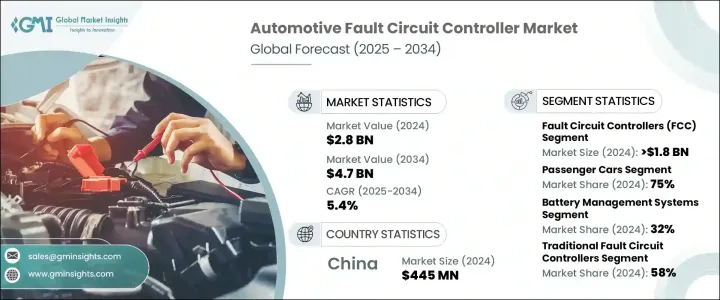

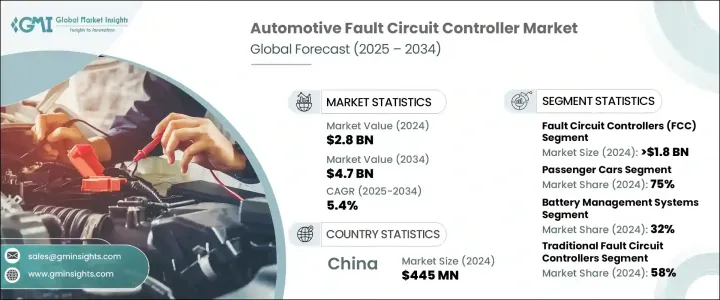

세계의 자동차 고장 회로 컨트롤러 시장 규모는 2024년에는 28억 달러로 평가되었고, 2034년에는 47억 달러에 이를 것으로 예측되며, CAGR 5.4%로 성장할 전망입니다.

이러한 성장은 주로 전기자동차(EV) 및 하이브리드 모델로의 전환이 증가함에 따라 촉진되고 있으며, 이러한 차량은 복잡한 전력 전자 장치와 고전압 배터리를 사용하기 때문에 더욱 정교한 전기 안전 시스템이 필요합니다. 고장 회로 컨트롤러는 고장을 신속하게 식별하고 격리하여 필수 부품을 손상으로부터 보호하기 때문에 이러한 차량의 안전한 운행에 필수적입니다.

특히 배출 규제가 강화되고 정부의 인센티브가 확대됨에 따라 EV의 채택이 계속 증가함에 따라 FCC에 대한 수요도 증가하고 있습니다. 이러한 장치는 차량의 안전을 보장하고, 다운타임을 최소화하며, 전기 시스템의 신뢰성을 유지하는 데 도움이 됩니다. 이는 차량이 성능, 내비게이션 및 운전자 지원에 대해 첨단 전자 장치에 점점 더 의존하게 되는 상황에서 매우 중요합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 28억 달러 |

| 예측 금액 | 47억 달러 |

| CAGR | 5.4% |

커넥티드 및 자율주행 차량(AV)의 부상은 자동차 시스템에 새로운 차원의 복잡성을 가져옵니다. 이러한 차량은 실시간 의사 결정 및 환경 탐색을 위해 첨단 센서, 통신 네트워크 및 인공 지능(AI) 알고리즘에 크게 의존합니다. 이러한 기술이 발전함에 따라 고도로 신뢰할 수 있고 안전한 전기 시스템에 대한 수요도 증가하고 있습니다. 고장 회로 컨트롤러(FCC)는 전기적 장애가 발생한 경우에도 이러한 복잡한 시스템이 계속 작동할 수 있도록 하는 데 중요한 역할을 합니다. 자율주행 차량에서는 파워트레인이나 통신 시스템에 사소한 결함이 발생해도 치명적인 결과를 초래할 수 있으므로, 이러한 보호 장치는 차량의 안전과 성능을 유지하는 데 매우 중요합니다.

2024년, 고장 회로 컨트롤러(FCC) 분야의 매출은 18억 달러에 이르렀습니다. FCC는 고전압 시스템이 결함을 신속하게 감지하지 못하면 심각한 고장을 일으킬 수 있는 전기자동차의 파워트레인에서 특히 중요합니다. 전기자동차는 400V-800V의 전압 범위에서 작동하기 때문에, 초기 단계에서 결함을 분리하여 잠재적인 재해를 방지하는 FCC의 역할은 아무리 강조해도 지나치지 않습니다. 비정상적인 전류 흐름을 감지하고 결함이 있는 회로를 차단하는 FCC의 기능은 이러한 차량의 안전을 유지하는 데 필수적입니다. 그 결과, EV 제조업체들이 이러한 안전 장치를 자동차에 점점 더 많이 통합함에 따라 이 시장 부문은 빠르게 성장하고 있습니다.

배터리 관리 시스템 부문은 2024년에 32%의 점유율을 차지했으며, 2034년까지 상당한 성장이 예상됩니다. 이 시스템에 포함된 배터리 모니터링 장치는 전기자동차의 안전과 신뢰성을 보장하는 데 중요한 역할을 합니다. 이 장치는 전압, 온도, 전류와 같은 주요 매개 변수를 추적하여 결함이 있는 셀이나 회로를 조기에 식별할 수 있습니다. 이 시스템은 결함 회로 컨트롤러와 함께 사용되면 정전 및 열 문제를 방지하여 배터리의 수명과 차량의 전반적인 성능을 향상시킵니다. 안전 스위치 역할을 하는 배터리 분리 장치는 고장이나 유지보수 시 차량의 전기 시스템의 안전을 더욱 강화합니다.

아시아태평양의 자동차 고장 회로 컨트롤러 시장은 2024년에 43%의 점유율을 차지해 4억 4,500만 달러를 창출했습니다. 중국은 전 세계에서 가장 큰 EV 시장으로, 현지 제조업체들이 전기자동차 제품을 빠르게 확장하고 있어 FCC 수요의 주요 요인이 되고 있습니다. 차량 안전에 대한 규제 요건이 엄격해짐에 따라 중국 자동차 제조업체들은 배터리 관리 시스템, 전력 전자 장치 및 e-드라이브 장치의 과전류 보호를 위해 첨단 FCC를 점점 더 많이 채택하고 있습니다. 차량 안전 및 신뢰성 향상을 위한 중국의 노력으로 FCC는 전기 구동계에서 필수적인 부품이 되었으며, 이는 시장 성장을 더욱 가속화하고 있습니다.

세계의 자동차 고장 회로 컨트롤러 시장의 주요 기업으로는 Siemens, Mitsubishi Electric, Honeywell International, Infineon Technologies, ABB, Panasonic Corporation, Eaton, Bosch Automotive Electronics, General Electric (GE) 및 Schneider Electric이 있습니다. 자동차 결함 회로 컨트롤러 시장에서 입지를 강화하기 위해 기업들은 자동차 산업의 진화하는 안전 기준을 충족하는 최신기술, 신뢰성 및 효율성을 갖춘 솔루션 개발에 주력하고 있습니다. 결함 보호 기술을 혁신하기 위해 연구 개발에 막대한 투자를 하고 있으며, 자사 제품이 고전압 전기자동차 및 커넥티드 카에 최적화될 수 있도록 보장하고 있습니다. 또한, 이러한 기업들은 FCC를 최신 파워트레인 및 배터리 관리 시스템에 원활하게 통합하기 위해 자동차 제조업체들과의 파트너십을 확대하고 있습니다. 다양한 차량 모델 및 유형의 특정 요구 사항을 충족하는 맞춤형 솔루션을 제공하는 것도 우선 과제가 되었습니다. 기업들은 생산 능력을 확대하고 전기자동차의 채택이 증가하는 신흥 시장에서 입지를 강화하여 시장 지위를 강화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 차량 전기화 및 고전압 아키텍처 채택의 급증

- 승객 안전과 규제 준수 강조의 강화

- 연결형 및 자율주행 차량 기술의 확장

- 고급 운전자 보조 시스템(ADAS)에 결함 감지 시스템 통합

- 업계의 잠재적 위험 및 과제

- 높은 복잡성과 통합 비용

- 열악한 자동차 환경에서의 신뢰성 문제

- 시장 기회

- 전기자동차(EV) 제조 확대

- 첨단 운전자 지원 시스템(ADAS)과의 통합

- 전기 안전 준수를 위한 규제 추진

- 신흥 자동차 시장의 성장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 삭감 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적 노력

- 탄소 발자국의 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카 항공

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 고장 회로 컨트롤러(FCC)

- 회로 보호 장치

- 센서 및 모니터링 장치

- 제어 모듈

제6장 시장 추계 및 예측 : 차종별(2021-2034년)

- 주요 동향

- 승용차

- 세단

- SUV

- 해치백

- 상용차

- LCV(소형 상용차)

- MCV(중형 상용차)

- HCV(대형 상용차)

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 엔진 관리 시스템

- 배터리 관리 시스템

- 조명 시스템

- 인포테인먼트 및 커넥티비티 시스템

- 안전 시스템

- HVAC(난방, 환기, 에어컨)

제8장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 기존

- 스마트/지능형

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 말레이시아

- 싱가포르

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제11장 기업 프로파일

- ABB

- Alstom

- American Superconductor

- Autoliv

- Bosch Automotive Electronics

- Continental

- Denso

- Eaton

- General Electric(GE)

- Honeywell International

- Infineon Technologies

- Liaoning Rongxin Electric Power Electronic Co.

- Mitsubishi Electric

- Nexans

- Panasonic

- Schneider Electric

- Siemens

- Superconductor Technologies

- TE Connectivity

- Valeo

The Global Automotive Fault Circuit Controller Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 4.7 billion by 2034. This growth is largely driven by the increasing shift towards electric vehicles (EVs) and hybrid models, which require more sophisticated electrical safety systems due to their complex power electronics and high-voltage batteries. Fault circuit controllers are integral to the safe operation of these vehicles, as they identify and isolate faults quickly, protecting essential components from damage.

As the adoption of EVs continues to rise, especially with stricter emission regulations and government incentives, the demand for FCCs is growing. These devices help ensure vehicle safety, minimize downtime, and maintain the reliability of electrical systems, which is crucial as vehicles become increasingly dependent on advanced electronics for performance, navigation, and driver assistance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $4.7 Billion |

| CAGR | 5.4% |

The rise of connected and autonomous vehicles (AVs) introduces a new layer of complexity to automotive systems. These vehicles rely heavily on advanced sensors, communication networks, and artificial intelligence (AI) algorithms to make real-time decisions and navigate environments. As these technologies evolve, so does the demand for highly reliable and secure electrical systems. Fault circuit controllers (FCCs) play a pivotal role in ensuring that these intricate systems remain operational, even in the face of electrical disruptions. In autonomous vehicles, even a minor fault in the powertrain or communication system leads to catastrophic outcomes, making these protective devices critical for maintaining vehicle safety and performance.

In 2024, the fault circuit controller (FCC) segment generated USD 1.8 billion. FCCs are particularly critical in electric vehicle powertrains, where high-voltage systems can cause significant failures if faults are not detected quickly. With electric vehicles operating within voltage ranges of 400V to 800V, the role of FCCs in preventing potential disasters by isolating faults at the earliest stages cannot be overstated. Their ability to detect abnormal current flow and disconnect faulty circuits is essential for maintaining the safety of these vehicles. Consequently, this market segment has grown rapidly as EV manufacturers increasingly incorporate these safety devices into their automobiles.

The battery management systems segment captured a 32% share in 2024 and is expected to see notable expansion through 2034. Battery monitoring units within these systems play a pivotal role in ensuring the safety and reliability of electric vehicles. These units track key parameters like voltage, temperature, and current, allowing early identification of faulty cells or circuits. When paired with fault circuit controllers, these systems help prevent power failures and thermal issues, thus enhancing battery longevity and overall vehicle performance. Battery disconnects units, which act as safety switches, further contribute to ensuring the safety of the vehicle's electrical system during faults or maintenance.

Asia Pacific Automotive Fault Circuit Controller Market held a 43% share and generated USD 445 million in 2024. China's status as the largest EV market globally is a key factor in the demand for FCCs, as local manufacturers are rapidly expanding their electric vehicle offerings. As regulatory requirements for vehicle safety become stricter, Chinese automakers are increasingly adopting advanced FCCs for overcurrent protection in battery management systems, power electronics, and e-drive units. The country's push toward enhancing vehicle safety and reliability has made FCCs a vital component in electric drivetrains, further accelerating market growth.

Key players in the Global Automotive Fault Circuit Controller Market include Siemens, Mitsubishi Electric, Honeywell International, Infineon Technologies, ABB, Panasonic Corporation, Eaton, Bosch Automotive Electronics, General Electric (GE), and Schneider Electric. To strengthen their position in the automotive fault circuit controller market, companies are focusing on developing cutting-edge, reliable, and efficient solutions that meet the evolving safety standards of the automotive industry. They are investing heavily in research and development to innovate fault protection technologies, ensuring their products are optimized for high-voltage electric vehicles and connected cars. Additionally, these companies are expanding their partnerships with automotive manufacturers to integrate FCCs seamlessly into modern powertrains and battery management systems. Offering customized solutions that cater to the specific needs of different vehicle models and types has also become a priority. Companies enhance their market foothold by expanding their production capabilities and increasing their presence in emerging markets, where the adoption of electric vehicles rises.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Application

- 2.2.5 Technology

- 2.2.6 End use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in vehicle electrification and high-voltage architecture adoption

- 3.2.1.2 Growing emphasis on passenger safety and regulatory compliance

- 3.2.1.3 Expansion of connected and autonomous vehicle technologies

- 3.2.1.4 Integration of fault detection systems in advanced driver-assistance systems (ADAS)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High complexity and cost of integration

- 3.2.2.2 Reliability issues in harsh automotive environments

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in electric vehicle (EV) manufacturing

- 3.2.3.2 Integration with advanced driver assistance systems (ADAS)

- 3.2.3.3 Regulatory push for electrical safety compliance

- 3.2.3.4 Growth in emerging automotive markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD, Million, Units)

- 5.1 Key trends

- 5.2 Fault circuit controllers (FCC)

- 5.3 Circuit protection devices

- 5.4 Sensors & monitoring units

- 5.5 Control modules

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD, Million, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedan

- 6.2.2 SUV

- 6.2.3 Hatchback

- 6.3 Commercial vehicles

- 6.3.1 LCVs (light commercial vehicles)

- 6.3.2 MCVs (medium commercial vehicles)

- 6.3.3 HCVs (heavy commercial vehicles)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD, Million, Units)

- 7.1 Key trends

- 7.2 Engine management systems

- 7.3 Battery management systems

- 7.4 Lighting systems

- 7.5 Infotainment and connectivity systems

- 7.6 Safety systems

- 7.7 HVAC (heating, ventilation, air conditioning)

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD, Million, Units)

- 8.1 Key trends

- 8.2 Traditional fault circuit controllers

- 8.3 Smart/intelligent fault circuit controllers

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD, Million, Units)

- 9.1 Key trends

- 9.2 OEM (original equipment manufacturers)

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 ABB

- 11.2 Alstom

- 11.3 American Superconductor

- 11.4 Autoliv

- 11.5 Bosch Automotive Electronics

- 11.6 Continental

- 11.7 Denso

- 11.8 Eaton

- 11.9 General Electric (GE)

- 11.10 Honeywell International

- 11.11 Infineon Technologies

- 11.12 Liaoning Rongxin Electric Power Electronic Co.

- 11.13 Mitsubishi Electric

- 11.14 Nexans

- 11.15 Panasonic

- 11.16 Schneider Electric

- 11.17 Siemens

- 11.18 Superconductor Technologies

- 11.19 TE Connectivity

- 11.20 Valeo