|

시장보고서

상품코드

1755313

가스 치환 포장 장비 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Modified Atmosphere Packaging Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

세계의 가스 치환 포장 장비 시장은 2024년 22억 달러로 평가되었으며 2034년에는 35억 달러에 이를 것으로 추정되며, CAGR 4.8%로 성장할 전망입니다. 이러한 성장은 식품 폐기물을 최소화하는 데 중요한 역할을 하는 유통 기한이 긴 식품에 대한 수요 증가에 의해 촉진되고 있습니다. 이 장비는 포장 내부의 산소를 질소 및 이산화탄소와 같은 불활성 가스로 대체하여 부패를 늦추고 식품을 더 오래 신선하게 유지합니다. 이 기술은 식품 포장 산업, 특히 부패하기 쉬운 제품 부문에서 빠르게 채택되고 있습니다.

도시 생활 방식에 따라 소비자 습관이 변화함에 따라 편의 식품 및 즉석 식사에 대한 선호도가 높아지고 있습니다. 사전 포장된 식사와 사전 절단된 농산물 소비 증가로 지속 가능하고 장기간 신선도를 유지할 수 있는 포장 솔루션에 대한 수요가 급증하고 있습니다. 가스 치환 포장 장비는 친환경 재료와의 호환성을 제공하며 전통적인 단일 사용 플라스틱 포장재를 줄이는 데 기여합니다. 제품 유통기한 연장 및 환경 영향 감소라는 이중 혜택을 갖춘 이 장비는 전 세계 식품 제조업체와 소매업체의 선호하는 선택지로 부상하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 22억 달러 |

| 예측 금액 | 35억 달러 |

| CAGR | 4.8% |

2024년, 자동 가스 치환 포장 시스템은 15억 달러를 창출했습니다. 이 시스템의 인기는 대규모 생산이 필수적인 식품 가공과 같은 고부가가치 산업에서 효율성과 대규모 생산 처리 능력을 갖추었기 때문입니다. 예측 유지보수 및 실시간 시스템 모니터링과 같은 고급 기능은 다운타임을 줄이고 생산성을 향상시켜 그 매력을 더욱 높였습니다. 이러한 스마트 기술은 제조업체가 배치 간 일관된 제품 품질을 유지하면서 증가하는 생산량 요구를 충족하는 데 도움이 됩니다.

직접 판매 부문은 개인화된 솔루션을 제공하고 제조업체와 최종 사용자 간의 일대일 협업을 촉진하는 능력으로 2024년에 72%의 점유율을 차지했습니다. 가스 치환 포장 장비는 특정 식품 제품에 맞게 높은 수준의 맞춤형 설정이 필요하며, 직접 판매 채널은 이 맞춤형 프로세스를 더 효율적이고 효과적으로 만듭니다. 이러한 판매 전략은 장비 공급업체와 구매자 모두에게 이익이 되는 장기적인 파트너십을 구축하는 데도 도움이 됩니다.

미국의 가스 치환 포장 장비 2024년 시장 규모는 4억 9,000만 달러로 76%의 점유율을 차지했습니다. 바쁜 생활 방식으로 촉진된 빠른 식사에 대한 수요의 증가는 전 세계적으로 소비자의 선호도를 계속해서 형성하고 있습니다. 그 결과, 지속 가능한 재료를 사용하면서 신선도를 연장하는 포장에 대한 필요성이 더욱 중요해지고 있습니다. 포장 장비의 기술 혁신과 자동화는 미국 시장을 더욱 발전시켰으며, 미국 기업들은 성능을 개선하고 운영 비용을 절감하기 위해 스마트 시스템을 점점 더 많이 채택하고 있습니다.

세계의 가스 치환 포장 장비 시장을 선도하는 주요 기업으로는 ULMA Packaging, Webomatic, Proseal, Ross Industries, Robert Reiser, MULTIVAC Group, Ishida, ORICS Industries, GEA Group, Ilapak, Reepack, Henkelman, PFM Group, G. Mondini, Coesia Group 등이 있습니다. 이러한 주요 진출기업은 혁신, 규모, 맞춤형으로 경쟁하고 있습니다. 이러한 주요 기업들은 혁신, 규모 및 맞춤화에서 경쟁을 벌이고 있습니다. 시장에서 경쟁 우위를 유지하기 위해 주요 제조업체들은 장비에 첨단 자동화 및 디지털 모니터링 기능을 통합하여 신뢰성을 높이고 운영 중단 시간을 줄이는 데 주력하고 있습니다. 맞춤형 장비와 유연한 가격 모델을 통해 식품 가공 회사들과의 파트너십을 강화하고 있습니다. 또한, 지속 가능한 포장재에 대한 R&D 투자를 통해 환경 규제와 변화하는 소비자 기대에 부응하고 있습니다. 직접 판매 전략을 통해 지리적 범위를 확대하고 애프터 서비스를 강화하는 것은 장기적인 고객 유지와 전 세계적 입지를 강화하기 위한 일반적인 접근 방식입니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 산업에 미치는 영향

- 공급측의 영향(원료)

- 주요 원료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원료)

- 영향을 받는 주요 기업

- 전략적인 산업 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 시책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 공급자의 상황

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 유통기한 연장 및 식품 폐기물 감소

- 즉석 식품 및 편의 식품에 대한 수요 증가

- 지속 가능성 및 규제 준수 압력

- 산업의 잠재적 리스크 및 과제

- 높은 초기 자본 투자

- 가스 혼합물 교정 및 모니터링의 복잡성

- 플라스틱 포장 폐기물에 관한 환경 우려

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추정 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 진공 기반 MAP

- 트레이 밀봉 MAP

- 수평 플로우 팩 MAP

- 수직 플로우 팩 MAP

- 기타

제6장 시장 추정 및 예측 : 조작별(2021-2034년)

- 주요 동향

- 자동

- 반자동

제7장 시장 추정 및 예측 : 포장 형태별(2021-2034년)

- 주요 동향

- 트레이 밀봉

- 열 성형

- 파우치/백

- 경질 용기

제8장 시장 추정 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 고기, 닭고기, 해산물

- 베이커리 및 과자류

- 신선한 식품(과일 및 채소)

- 유제품

- 즉석식(RTE) 식사

- 기타

제9장 시장 추정 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접

- 간접

제10장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제11장 기업 프로파일

- Coesia Group

- G. Mondini

- GEA Group

- Henkelman

- Ilapak

- Ishida

- MULTIVAC Group

- ORICS Industries

- PFM Group

- Proseal

- Reepack

- Robert Reiser

- Ross Industries

- ULMA Packaging

- Webomatic

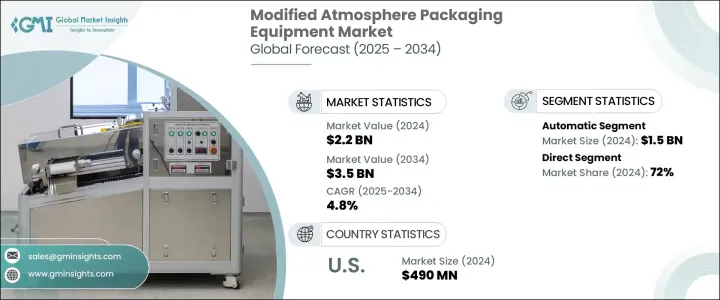

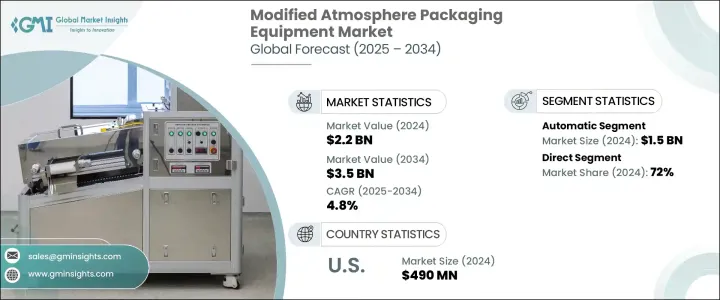

The Global Modified Atmosphere Packaging Equipment Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 3.5 billion by 2034. The growth is driven by the increasing demand for food products with extended shelf life, which plays a crucial role in minimizing food waste. These machines replace oxygen inside the packaging with inert gases like nitrogen and carbon dioxide, which slows down spoilage and keeps food fresh longer. This technology is rapidly being adopted in the food packaging industry, particularly in perishable product categories.

As consumer habits evolve with urban lifestyles, there is a rising preference for convenience foods and ready-to-eat meals. The growing consumption of pre-packed meals and precut produce is creating a strong demand for packaging solutions that are both sustainable and capable of maintaining freshness for extended durations. Modified atmosphere packaging equipment supports this need by offering compatibility with eco-friendly materials and helping reduce conventional single-use plastic packaging. With the dual benefit of extending product shelf life and reducing environmental impact, this equipment is becoming a preferred choice for food manufacturers and retailers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $3.5 Billion |

| CAGR | 4.8% |

In 2024, automatic modified atmosphere packaging systems generated USD 1.5 billion. Their popularity stems from their efficiency and ability to handle large-scale production essential for high-volume sectors like food processing. Advanced features such as predictive maintenance and real-time system monitoring have increased their appeal by reducing downtime and enhancing productivity. These smart technologies help manufacturers meet growing output demands while maintaining consistent product quality across batches.

Direct sales segment accounted for a 72% share in 2024 due to its ability to provide personalized solutions and facilitate one-on-one collaborations between manufacturers and end-users. Modified atmosphere packaging machines often require high degrees of customization, tailored for specific food products, and direct sales channels make this customization process more streamlined and effective. Such sales strategies also help forge long-term partnerships that benefit equipment providers and buyers.

United States Modified Atmosphere Packaging Equipment Market was valued at USD 490 million in 2024, holding a 76% share. The rising demand for quick meals, driven by busy lifestyles, continues to shape consumer preferences globally. As a result, the need for packaging that extends freshness while using sustainable materials is becoming more important. Technological innovations and automation in packaging equipment have further advanced the market in the U.S., where companies are increasingly adopting smart systems to improve performance and reduce operational costs.

Major companies leading the Global Modified Atmosphere Packaging Equipment Market include ULMA Packaging, Webomatic, Proseal, Ross Industries, Robert Reiser, MULTIVAC Group, Ishida, ORICS Industries, GEA Group, Ilapak, Reepack, Henkelman, PFM Group, G. Mondini, and Coesia Group. These key players compete on innovation, scale, and customization. To maintain a competitive edge in the market, leading manufacturers focus on integrating advanced automation and digital monitoring features into their equipment to improve reliability and reduce operational downtimes. They strengthen partnerships with food processing companies through customized machinery and flexible pricing models. Additionally, R&D investment in sustainable packaging materials is helping them align with environmental regulations and shifting consumer expectations. Expanding their geographic footprint through direct sales strategies and enhancing after-sales support is a common approach to boost long-term client retention and global presence.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Shelf-Life Extension & Food Waste Reduction

- 3.6.1.2 Rising Demand for Ready-to-Eat & Convenience Foods

- 3.6.1.3 Sustainability & Regulatory Compliance Pressures

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High Initial Capital Investment

- 3.6.2.2 Complexity in Gas Mixture Calibration & Monitoring

- 3.6.2.3 Environmental Concerns Over Plastic Packaging Waste

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Vacuum-Based MAP Equipment

- 5.3 Tray Sealing MAP Equipment

- 5.4 Horizontal flow pack MAP

- 5.5 Vertical flow pack MAP

- 5.6 Others (multi-lane machines, custom MAP systems, etc.)

Chapter 6 Market Estimates & Forecast, By Operation, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automated

- 6.3 Semi-automated

Chapter 7 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Tray sealing

- 7.3 Thermoforming

- 7.4 Pouch/Bag

- 7.5 Rigid container

Chapter 8 Market Estimates & Forecast, By End Use Application, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Meat, poultry, and seafood

- 8.3 Bakery & confectionery

- 8.4 Fresh produce (fruits and vegetables)

- 8.5 Dairy products

- 8.6 Ready-to-Eat (RTE) meals

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Coesia Group

- 11.2 G. Mondini

- 11.3 GEA Group

- 11.4 Henkelman

- 11.5 Ilapak

- 11.6 Ishida

- 11.7 MULTIVAC Group

- 11.8 ORICS Industries

- 11.9 PFM Group

- 11.10 Proseal

- 11.11 Reepack

- 11.12 Robert Reiser

- 11.13 Ross Industries

- 11.14 ULMA Packaging

- 11.15 Webomatic