|

시장보고서

상품코드

1755332

팬 코일 유닛 시장 : 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Fan Coil Unit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

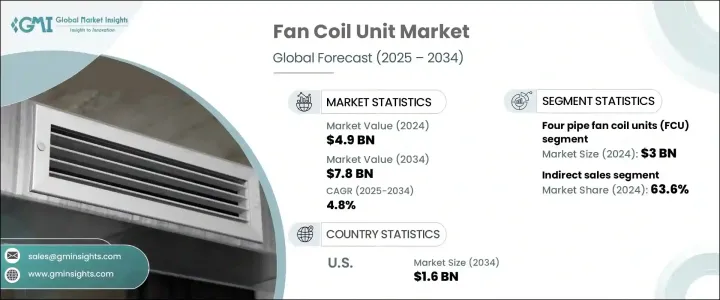

세계 팬 코일 유닛(FCU) 시장은 2024년에는 49억 달러로 평가되었으며 CAGR 4.8%로 성장하여 2034년에는 78억 달러에 이를 것으로 추정됩니다.

이 성장의 주요 요인은 실내 공기 환경의 중요성에 대한 의식의 증가입니다. 사람들이 가정이나 사무실, 기타 폐쇄된 환경 속에서 많은 시간을 보내게 되어, 대기 오염이나 습도 관리에 관련되는 우려가 현저해지고 있습니다. 공조 솔루션을 요구하고 있습니다. 고성능의 공기 여과 기능과 습도 조정 기능을 갖춘 FCU는 주택과 상업시설의 양쪽 모두의 구매자로부터 점점 지지되고 있습니다. 오피스, 학교, 헬스케어등의 환경에서는 실내 공기의 질의 향상이 웰니스나 생산성의 향상과 밀접하게 연결되어 있어 이것이 채택을 더욱 촉진합니다.

게다가 노후화된 인프라를 현대의 에너지 기준에 맞추기 위해 현대화하는 동향은 FCU와 같은 에너지 효율적인 HVAC 솔루션에 대한 강한 수요를 창출하고 있습니다. 사용량의 가장 큰 요인 중 하나이기 때문에 효율적인 에어컨 제어 시스템을 통합하는 것은 에너지 풋 프린트를 줄이는 데 필수적입니다. FCU, 특히 스마트 기술과 통합된 FCU는 향상된 제어 및 자동화 기능을 제공함에 따라 더욱 탄력을 받고 있습니다.원격 감시, 점유율 기반의 설정, 빌딩 관리 시스템과의 통합에 의해 FCU는 시설 관리자나 빌딩 소유자에게 보다 매력적인 것이 되고 있습니다. 에너지 사용량을 보다 효과적으로 조정하고 운영 비용을 최소화하면서 성능을 최적화하는 데 도움이 됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 초기 시장 규모 | 49억 달러 |

| 시장 규모 예측 | 78억 달러 |

| CAGR | 4.8% |

팬 코일 유닛 시장은 구성별로 2개 배관식 FCU와 4개 배관식 FCU로 구분됩니다. 2025년부터 2034년까지 CAGR 4.9%로 성장할 것으로 예측됩니다. 4개의 배관식 시스템은 난방과 냉방을 동시에 공급할 수 있기 때문에 다른 구역에 걸쳐 다양한 공조 요구가 있는 건물에서는 기능적으로 유리합니다. 이러한 시스템은 여러 방과 부서에 걸쳐 일관된 편안함을 필요로 하는 대규모 상업시설과 시설에 특히 적합합니다.

판매 채널별로 평가하면 시장은 직접 판매와 간접 판매로 나뉩니다. 이 부문의 강점은 딜러, 유통업체, 소매 파트너 등의 중개인의 광범위한 네트워크에 있습니다. 현지 건설업자, 건축업자, 최종 사용자와의 확립된 관계는 판매주기를 보다 효율적이고 신속하게 하고 있습니다. 유통업체가 제공하는 판매 후 지원, 설치 및 유지보수와 같은 부가가치 서비스는 이 채널의 매력을 더욱 높여줍니다. 간접판매는 지역에 특화된 마케팅 전략과 깊은 시장 지식으로부터도 혜택을 받아 지역 시장의 브랜드 인지도와 고객의 신뢰를 높이는데 도움이 됩니다.

미국의 팬 코일 유닛 시장은 2024년에 금액 기준으로 10억 달러를 돌파했고 2034년에는 16억 달러에 이를 것으로 예측되고 있습니다. 실내 온도 제어를 최적화함으로써 FCU는 에너지 낭비를 최소화하고 전국적인 목표에 맞춰 지속 가능한 건축 관행을 촉진합니다. 그린 빌딩의 설계에 임베디드되는 케이스가 늘어나고 있습니다.

세계의 FCU 시장은 여전히 매우 세분화되어 있으며, 다수의 지역 기업이 국제 수준에서 사업을 전개하고 있습니다. 현지 기업들은 종종 특정 지역 수요를 충족시키며, 현지 규제 및 건축 법규 요구 사항을 충족하도록 제품을 맞춤화합니다. 또한, 지역의 기호에 맞춘 커스터마이즈 솔루션도 제공하고 있습니다. 국제적 브랜드는 대규모 생산, 확립된 국제적 네트워크, 시장에서의 높은 신뢰성으로부터, 복수의 지역에서 경쟁력을 유지할 수 있습니다.

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업체

- 리셀러

- 공급자의 상황

- 이익률 분석

- 기술 개요

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 실내 공기질에 대한 의식의 고조

- 도시화의 진전

- 기술적 진보

- 업계의 잠재적 위험과 과제

- 높은 초기 비용

- 규제 및 규정 준수 문제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 팬 코일 유닛 시장의 추정 및 예측 : 구성별(2021-2032년)

- 주요 동향

- 2개 배관식 팬 코일 유닛

- 4개 배관식 팬 코일 유닛

제6장 팬 코일 유닛 시장의 추정 및 예측 : 방향별(2021-2032년)

- 주요 동향

- 수평형

- 벽걸이식

- 덕트 블로어형

- 천장 카세트형

- 천장 이식형

- 세로형(마루치형)

제7장 팬 코일 유닛 시장의 추정 및 예측 : 공기 유량별(2021-2032년)

- 주요 동향

- 500 m³/h 이하

- 500 m³/h-1000 m³/h

- 1000 m³/h-1500 m³/h

- 1500 m³/h-2000 m³/h

- 2000m³/h이상

제8장 팬 코일 유닛 시장의 추정 및 예측 : 최종 용도별(2021-2032년)

- 주요 동향

- 주택용

- 상업용

- 사무실 공간

- 호텔

- 레스토랑

- 병원

- 소매

- 슈퍼마켓

- 백화점

- 브랜드 아울렛 스토어

- 물류(창고)

- 기타(제조업 등)

- 산업

제9장 팬 코일 유닛 시장의 추정 및 예측 : 유통 채널별(2021-2032년)

- 주요 동향

- 직접 판매

- 간접판매

제10장 팬 코일 유닛 시장의 추정 및 예측 : 지역별(2021-2032년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 기타 라틴아메리카

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제11장 기업 프로파일

- Aermec

- Carrier Global Corporation

- Daikin Industries

- Dunham-Bush

- Emerson Electric

- Fujitsu General Limited

- Gree Electric Appliances

- Honeywell International

- Johnson Controls International

- Lennox International

- LG Electronics

- Mitsubishi Electric Corporation

- Samsung Electronics

- Trane Technologies

- TROX

The Global Fan Coil Unit Market was valued at USD 4.9 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 7.8 billion by 2034. This growth is primarily fueled by rising awareness about the importance of indoor air quality. As people spend a large portion of their time inside homes, offices, and other enclosed environments, concerns around air pollution and humidity control have become more prominent. Consumers are now looking for air conditioning solutions that not only cool or heat the air but also ensure cleaner, healthier indoor environments. FCUs equipped with high-performance air filtration and humidity regulation features are increasingly favored by both residential and commercial buyers. In environments such as offices, schools, and healthcare settings, better indoor air quality is closely linked with improved wellness and productivity, which further drives adoption.

Additionally, the trend of modernizing aging infrastructure to meet contemporary energy standards has created a strong demand for energy-efficient HVAC solutions like FCUs. As buildings remain one of the highest contributors to energy use globally, integrating efficient climate control systems has become essential for reducing energy footprints. Modern FCUs, particularly those integrated with smart technology, are gaining momentum as they offer enhanced control and automation features. Remote monitoring, occupancy-based settings, and integration with building management systems are making FCUs more attractive to facility managers and building owners. These intelligent systems help regulate energy usage more effectively, optimizing performance while minimizing operational expenses. They also offer real-time insights that allow for proactive maintenance and performance tuning, leading to long-term efficiency gains.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.9 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 4.8% |

By configuration, the fan coil unit market is segmented into two-pipe and four-pipe FCUs. Among these, the four-pipe segment accounted for the largest revenue share, valued at approximately USD 3 billion in 2024, and is expected to grow at a CAGR of 4.9% from 2025 to 2034. The ability of four-pipe systems to deliver both heating and cooling at the same time gives them a functional advantage in buildings with varied climate control needs across different zones. This flexibility enables building operators to maintain precise indoor temperatures tailored to specific spaces. These systems are particularly suitable for large-scale commercial or institutional facilities that require consistent comfort across multiple rooms or departments. Although the initial installation and equipment costs are relatively high, the superior thermal control and adaptability of four-pipe FCUs make them a preferred choice in advanced HVAC design.

When assessed by distribution channel, the market is divided into direct and indirect sales. The indirect sales segment held the dominant share in 2024, contributing roughly 63.6% of the overall revenue, and is forecasted to rise at a CAGR of 4.9% over the forecast period. The strength of this segment lies in its widespread network of intermediaries, including dealers, distributors, and retail partners. These channels help manufacturers expand their reach into diverse geographic locations and customer bases. Established relationships with local contractors, builders, and end-users make the sales cycle more efficient and responsive. Additionally, value-added services such as post-sale support, installation, and maintenance offered by distributors further enhance the attractiveness of this channel. Indirect sales also benefit from localized marketing strategies and in-depth market knowledge, which help boost brand visibility and customer trust in regional markets.

In the United States, the fan coil unit market surpassed USD 1 billion in value in 2024 and is projected to hit USD 1.6 billion by 2034. The increasing shift toward energy-efficient and sustainable building systems is a major factor behind this growth. FCUs are increasingly being incorporated into green building designs as they offer localized climate control, which contributes to significant energy savings compared to centralized HVAC systems. By optimizing temperature control at the room level, FCUs minimize energy waste and align with nationwide goals to promote sustainable building practices. This has made FCUs a vital component in the drive toward environmentally conscious infrastructure upgrades.

The global FCU market remains highly fragmented, with numerous regional players operating on an international level. Collectively, these companies account for approximately 10% to 15% of the total market share. Local firms often cater to specific regional demands, tailoring their offerings to meet local regulatory and building code requirements. They also provide customized solutions that appeal to regional preferences. On the other hand, global brands benefit from large-scale production, established international networks, and strong market credibility, enabling them to maintain competitiveness across multiple regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technological overview

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increased awareness of indoor air quality

- 3.7.1.2 Rising urbanization

- 3.7.1.3 Technological advancements

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High initial costs

- 3.7.2.2 Regulatory and compliance issues

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Fan Coil Unit Market Estimates & Forecast, By Configuration, 2021 - 2032 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Two pipe fan coil unit

- 5.3 Four pipe fan coil unit

Chapter 6 Fan Coil Unit Market Estimates & Forecast, By Orientation, 2021 - 2032 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Horizontal

- 6.2.1 Wall mounted

- 6.2.2 Ducted blower type

- 6.2.3 Ceiling cassette type

- 6.2.4 Ceiling concealed type

- 6.3 Vertical (floor mounted)

Chapter 7 Fan Coil Unit Market Estimates & Forecast, By Air Flow, 2021 - 2032 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Below 500 m³/h

- 7.3 500 m³/h - 1000 m³/h

- 7.4 1000 m³/h - 1500 m³/h

- 7.5 1500 m³/h - 2000 m³/h

- 7.6 Above 2000 m³/h

Chapter 8 Fan Coil Unit Market Estimates & Forecast, By End Use, 2021 - 2032 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Office spaces

- 8.3.2 Hotels

- 8.3.3 Restaurants

- 8.3.4 Hospitals

- 8.3.5 Retail

- 8.3.5.1 Supermarkets

- 8.3.5.2 Departmental stores

- 8.3.5.3 Brand outlet stores

- 8.3.6 Logistics (warehouse)

- 8.3.7 Others (manufacturing, etc.)

- 8.4 Industrial

Chapter 9 Fan Coil Unit Market Estimates & Forecast, By Distribution Channel, 2021 - 2032 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Fan Coil Unit Market Estimates & Forecast, By Region, 2021 - 2032 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Rest of Latin America

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of MEA

Chapter 11 Company Profiles

- 11.1 Aermec

- 11.2 Carrier Global Corporation

- 11.3 Daikin Industries

- 11.4 Dunham-Bush

- 11.5 Emerson Electric

- 11.6 Fujitsu General Limited

- 11.7 Gree Electric Appliances

- 11.8 Honeywell International

- 11.9 Johnson Controls International

- 11.10 Lennox International

- 11.11 LG Electronics

- 11.12 Mitsubishi Electric Corporation

- 11.13 Samsung Electronics

- 11.14 Trane Technologies

- 11.15 TROX