|

시장보고서

상품코드

1755338

전기 삼륜차 시장 : 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Electric Three-Wheeler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

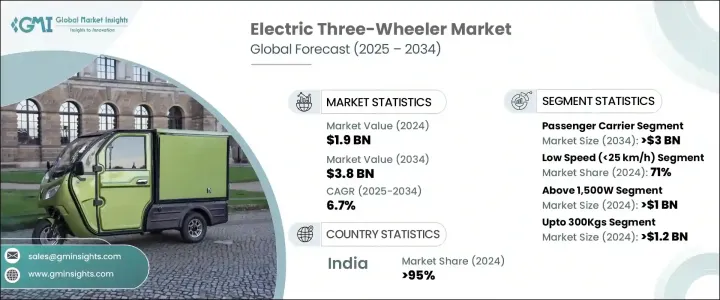

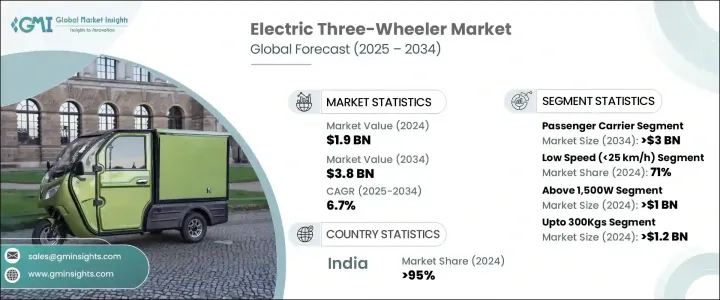

전 세계 전기 삼륜차 시장은 2024년에는 19억 달러에 달했고, CAGR 6.7%로 성장하여 2034년에는 38억 달러에 이를 것으로 추정됩니다.

이 급성장의 배경은 연료 가격의 상승, EV 도입 인센티브의 확대, 저렴한 도시 교통에 대한 주목 증가가 있습니다. 전기차 충전 인프라의 확장과 배터리 기술의 발전은 이러한 차량의 주행 거리와 성능도 향상시키고 있습니다. 각 지역의 지속 가능한 운송에 대한 지원 정책과 투자와 함께, 이 시장은 비용 효율적인 깨끗한 모빌리티 솔루션을 요구하는 개인 사용자와 상용 플릿 오퍼레이터 모두에서 큰 지지를 얻고 있습니다.

전기 삼륜차는 내연기관의 대체품에 비해 운용면에서 설득력 있는 장점을 제공합니다. 이 지역의 많은 정부는 보조금, 면세, 요금 면제 등의 제도를 통해 EV 구매에 인센티브를 주고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 초기 시장 규모 | 19억 달러 |

| 시장 규모 예측 | 38억 달러 |

| CAGR | 6.7% |

여객 수송차 부문은 2024년에 13억 달러로 평가되었고, 2034년까지 30억 달러로 성장할 것으로 예상되고 있습니다. 기존 대중교통 접근이 제한된 인구를 위해 이러한 차량은 신뢰할 수 있고 저렴한 통근 솔루션을 제공합니다. 라이드 헤일링이나 공유 모빌리티 플랫폼과의 통합에 의해 이용률은 한층 더 높아지고 있습니다. 기타 특전으로서, 소유 코스트의 낮음, 단기간의 회수, 운전의 용이함등이 있어, 기업이나 플릿 베이스의 운송 사업자가 전기 모델을 대규모로 채택하도록 동기 부여하고 있습니다.

속도 25km/h 이하의 전기 삼륜차 부문은 2024년에 71%의 점유율을 획득했습니다. 라이선싱 규제가 느리고 비용이 낮고 환경 친화적인 운전이 가능하기 때문에 인기가 높아지고 있습니다.

아시아태평양 전기 삼륜차 2024년 시장 점유율은 95%였습니다. 인도는 특히 티어 II와 티어 III 도시에서 여객 및 화물 운송을 위해 삼륜차에 대한 강한 의존도가 계속해서 채택을 촉진하고 있습니다. 국가 및 주 차원의 정책, 폐기 계획, 인식 캠페인 등 국가의 지원적인 전기차 생태계는 도심과 농촌 복도 모두에서 전기 모빌리티로의 전환을 가속화하고 있습니다. 전기 삼륜차 수요는 마이크로모빌리티와 라스트 원 마일 물류에서 왕성하고,이 섹터의 적응성과 비용 효과를 반영하고 있습니다.

전기 삼륜차 시장에 진입하는 주요 기업으로는 Hotage India, Mahindra Last Mile Mobility, Dilli Electric Auto, YC Electric, Energy Electric Vehicles, Piaggio Vehicles, Unique International, Saera Electric Auto, Bajaj Auto, Mini Metro EV 등이 있습니다. 전기 삼륜차 시장에서의 지위를 강화하기 위해, 각 사는 화물용과 여객용 모두에 맞춘 모델로 제품 포트폴리오를 확대하는 것에 주력하고 있습니다. 배터리 공급업체, 차량 운영업체 및 충전 인프라 제공업체와의 전략적 파트너십은 운영 규모를 확장하는 데 도움이 되고 있습니다.

목차

제1장 분석 방법

- 시장의 범위와 정의

- 분석 디자인

- 분석 접근

- 데이터 수집 방법

- 데이터 마이닝의 소스

- 지역

- 국가

- 기본적인 추정·계산법

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 분석과 검증

- 1차 정보

- 예측 모델

- 분석의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 운용·보수 비용의 낮음

- 정부 인센티브와 보조금

- 배터리 기술의 진보와 배터리 가격의 저하

- 엄격한 배출기준과 환경규제

- 스마트 기술 통합

- 업계의 잠재적 위험과 과제

- 제한된 충전 인프라

- 초기 구입 비용이 높아

- 시장 기회

- 충전 인프라 개발

- 경상용차의 대체

- 마지막 마일 배송 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 국가별

- 차량별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 삭감 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적 인 노력

- 카본 풋 프린트의 고려

- 소비자 행동 분석

- 이용 동향 : 여객 통근 vs. 화물 수송

- 구매 결정 요인(가격, 브랜드, 범위)

- 보험과 애프터마켓의 동향 분석

- 상업용 E3W의 보험 채용

- 배터리 교환과 현지화된 애프터마켓 서비스

- 유지 보수 비용 비교 : 전기자동차와 ICE 삼륜차

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 기업 합병 및 인수(M&A)

- 사업 제휴 및 협력

- 신제품 발매

- 확장계획과 자금조달

- 제품 벤치마킹

- 범위

- 배터리 수명

- 구축과 설계

- 접속성과 기술 기능

- 애프터 서비스

제5장 시장의 추정 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 여객 수송차

- 화물 수송차

제6장 시장의 추정 및 예측 : 배터리별(2021-2034년)

- 주요 동향

- 리튬 이온

- 납축전지

제7장 시장의 추정 및 예측 : 전력 용량별(2021-2034년)

- 주요 동향

- 1,000W 이하

- 1,000W-1,500W

- 1,500W 이상

제8장 시장의 추정 및 예측 : 배터리용량별(2021-2034년)

- 주요 동향

- 3kWh 미만

- 3-6kWh

- 6kWh 이상

제9장 시장의 추정 및 예측 : 속도별(2021-2034년)

- 주요 동향

- 저속(25 km/h 미만)

- 고속(25 km/h 이상)

제10장 시장의 추정 및 예측 :적재량별(2021-2034년)

- 주요 동향

- 300kg 미만

- 300kg 이상

제11장 시장의 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 강소성

- 허난성

- 허베이성

- 산동성

- 광동성

- 절강성

- 기타

- 인도

- 우타르프라데시주

- 비하르주

- 아쌈

- 라자스탄주

- 기타

- 기타

- 일본

- 한국

- 호주

- 동남아시아

- 중국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제12장 기업 프로파일

- Altigreen Propulsion Labs

- Atul Auto

- Avon EV

- Bajaj Auto

- Dilli Electric Auto

- Energy Electric Vehicles

- Euler Motors

- Greaves Electric Mobility

- Hotage India

- JS Auto

- Mahindra Last Mile Mobility

- Mini Metro EV

- Montra Electric

- Omega Seiki Mobility

- Piaggio Vehicles

- Saera Electric Auto

- TVS Motor Company

- Unique International

- VeeEss Eelectric

- YC Electric

The Global Electric Three-Wheeler Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 3.8 billion by 2034. This rapid growth is driven by rising fuel prices, expanding EV adoption incentives, and an increasing focus on affordable urban transportation. Electric three-wheelers offer an ideal solution for short-distance and last-mile connectivity in densely populated urban settings. The expansion of EV charging infrastructure and advances in battery technology are also improving the range and performance of these vehicles. Coupled with supportive policies and investment in sustainable transport across regions, the market is witnessing significant traction among both private users and commercial fleet operators seeking cost-efficient, clean mobility solutions.

Electric three-wheelers offer compelling operational advantages over internal combustion engine alternatives. With minimal maintenance needs and significantly lower fuel costs, they present an attractive total cost of ownership. This makes them especially viable for daily-use commercial applications. Many governments across regions like Africa, Asia, and Europe are incentivizing EV purchases through schemes offering subsidies, tax exemptions, and fee waivers. These measures, along with country-specific programs to promote electric mobility, are helping bridge the price gap and accelerate the shift to electric fleets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.8 Billion |

| CAGR | 6.7% |

The passenger carrier segment generated USD 1.3 billion in 2024 and is expected to generate USD 3 billion by 2034. The widespread use of electric three-wheelers as public transport alternatives in urban and semi-urban areas is fueling this growth. For populations with limited access to conventional public transit, these vehicles offer a reliable and low-cost commuting solution. Their integration with ride-hailing and shared mobility platforms is further increasing utilization rates. Additionally, benefits such as low ownership costs, quick returns, and ease of driving are motivating entrepreneurs and fleet-based transport providers to adopt electric models at scale.

Electric three-wheelers with a top speed of 25 km/h segment captured a 71% share in 2024. These low-speed vehicles are increasingly being deployed for specialized utility tasks such as waste management, local delivery, and institutional transport, particularly in developing countries where short-distance, low-speed travel is the norm. Their popularity is bolstered by lenient licensing norms, lower costs, and eco-friendly operation. Government support aimed at rural electrification and clean mobility is further encouraging the use of light-duty EVs for local transport applications.

Asia Pacific Electric Three-Wheeler Market held a 95% share in 2024. India's strong reliance on three-wheeled vehicles for both passenger and cargo transport-especially in Tier II and Tier III cities-continues to drive adoption. The country's supportive EV ecosystem, including national and state-level policies, scrappage schemes, and awareness campaigns, is accelerating the transition to electric mobility in both urban centers and rural corridors. Demand for electric three-wheelers is strong in micro-mobility and last-mile logistics, reflecting the sector's adaptability and cost-effectiveness.

Major companies operating in the Electric Three-Wheeler Market include Hotage India, Mahindra Last Mile Mobility, Dilli Electric Auto, YC Electric, Energy Electric Vehicles, Piaggio Vehicles, Unique International, Saera Electric Auto, Bajaj Auto, and Mini Metro EV. To strengthen their position in the electric three-wheeler market, companies are focusing on expanding their product portfolios with models tailored to both cargo and passenger applications. Many players are investing in R&D to improve battery efficiency, enhance range, and reduce charging time. Strategic partnerships with battery suppliers, fleet operators, and charging infrastructure providers are helping them scale operations. Manufacturers are also prioritizing cost optimization through localized production and lean manufacturing to meet the needs of price-sensitive markets. Branding efforts, dealer expansion, and after-sales service improvements are further enabling deeper market penetration.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Region

- 1.3.2 Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Battery

- 2.2.4 Power capacity

- 2.2.5 Battery capacity

- 2.2.6 Speed

- 2.2.7 Payload capacity

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Low operating and maintenance costs

- 3.2.1.2 Government incentives and subsidies

- 3.2.1.3 Advancements in battery technology and reducing battery prices

- 3.2.1.4 Stringent emission norms and environmental regulations

- 3.2.1.5 Integration of smart technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited charging infrastructure

- 3.2.2.2 High initial purchase cost

- 3.2.3 Market opportunities

- 3.2.3.1 Charging infrastructure development

- 3.2.3.2 Light commercial vehicle replacement

- 3.2.3.3 Last-mile delivery expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By country

- 3.8.2 By vehicle

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Consumer behavior analysis

- 3.13.1 Usage trends: passenger commute vs. goods transport

- 3.13.2 Purchase decision factors (price, brand, range)

- 3.14 Analysis of insurance and aftermarket trends

- 3.14.1. Insurance adoption for commercial E3 Ws

- 3.14.2 Battery replacement & localized aftermarket services

- 3.14.3 Comparative maintenance costs: Electric vs. ICE 3-wheelers

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Product benchmarking

- 4.7.1 Range

- 4.7.2 Battery life

- 4.7.3 Build and design

- 4.7.4 Connectivity & tech features

- 4.7.5 Aftermarket service

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger carrier

- 5.3 Load carrier

Chapter 6 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Lithium-ion

- 6.3 Lead acid

Chapter 7 Market Estimates & Forecast, By Power Capacity, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Below 1,000W

- 7.3 1,000W-1,500W

- 7.4 Above 1,500W

Chapter 8 Market Estimates & Forecast, By Battery Capacity, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Below 3kWh

- 8.3 3-6kWh

- 8.4 Above 6kWh

Chapter 9 Market Estimates & Forecast, By Speed, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Low speed (<25 km/h)

- 9.3 High speed (≥25 km/h)

Chapter 10 Market Estimates & Forecast, By Payload Capacity, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 Upto 300Kgs

- 10.3 Above 300Kgs

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.1.1 Jiangsu

- 11.4.1.2 Henan

- 11.4.1.3 Hebei

- 11.4.1.4 Shandong

- 11.4.1.5 Guangdong

- 11.4.1.6 Zhejiang

- 11.4.1.7 Others

- 11.4.2 India

- 11.4.2.1 Uttar Pradesh

- 11.4.2.2 Bihar

- 11.4.2.3 Assam

- 11.4.2.4 Rajasthan

- 11.4.2.5 Others

- 11.4.2.6 Others

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Southeast Asia

- 11.4.1 China

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Altigreen Propulsion Labs

- 12.2 Atul Auto

- 12.3 Avon EV

- 12.4 Bajaj Auto

- 12.5 Dilli Electric Auto

- 12.6 Energy Electric Vehicles

- 12.7 Euler Motors

- 12.8 Greaves Electric Mobility

- 12.9 Hotage India

- 12.10 J.S. Auto

- 12.11 Mahindra Last Mile Mobility

- 12.12 Mini Metro EV

- 12.13 Montra Electric

- 12.14 Omega Seiki Mobility

- 12.15 Piaggio Vehicles

- 12.16 Saera Electric Auto

- 12.17 TVS Motor Company

- 12.18 Unique International

- 12.19 VeeEss Eelectric

- 12.20 YC Electric