|

시장보고서

상품코드

1755352

척추 임플란트 시장 : 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Spinal Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

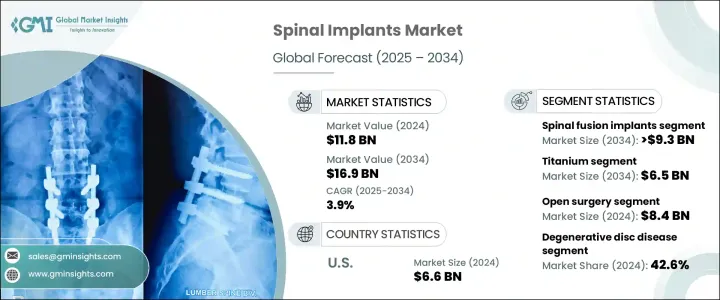

세계 척추 임플란트 시장은 2024년에는 118억 달러로 평가되었으며 CAGR 3.9%로 성장하여 2034년에는 169억 달러에 이를 것으로 예측됩니다.

수요 증가는 고령화 인구 증가, 척추 질환 증가, 낮은 침습 수술로의 이동, 임플란트 재료 및 수술 절차의 기술 진보가 배경에 있습니다. 변성, 추간판 탈장 등의 척추 질환이 특히 노인들 사이에서 만연함에 따라 외과적 개입과 척추 안정화 솔루션의 필요성은 상승의 길을 따라가고 있습니다.

비만과 좌식 라이프스타일은 척추변성에 더욱 박차를 가합니다. 정도가 높아졌을 뿐만 아니라, 합병증의 발생률도 최소화 되었기 때문에 선진적인 임플란트의 사용이 장려되고 있습니다. 많은 기기 제조업체는 저침습 수기에 맞춘 임플란트를 설계하는 것으로 대응하고 있어, 비용이 서서히 저하해, 이용의 용이성이 향상됨에 따라, 세계적으로 폭넓은 임상 채용을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 초기 시장 규모 | 118억 달러 |

| 시장 규모 예측 | 169억 달러 |

| CAGR | 3.9% |

척추 고정 임플란트 분야는 CAGR 4.3%로 성장하여 2034년에는 93억 달러에 이를 것으로 예측됩니다. 척추 유돌증이나 디스크 장애와 같은 퇴행성 질환이 흔해짐에 따라 척추 융합 시술의 양이 계속 증가하고 있습니다. PEEK와 티타늄과 같은 첨단 재료로 만들어진 새로운 고정 임플란트의 설계는 인체와의 적합성, 강도 향상, 주위 뼈 조직과의 더 나은 통합으로 현재는 더 일반적으로 사용되고 있습니다.

티타늄 기반 척추 임플란트의 부문은 2034년까지 65억 달러를 생산할 것으로 예상되고 있습니다. 티타늄 임플란트는 강인하면서도 경량이며, 회복기 및 회복 후의 환자의 쾌적성과 퍼포먼스에 있어서 필수적입니다.

미국 척추 임플란트의 2024년 시장 규모는 66억 달러로 평가되었고, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 3.5%로 성장할 것으로 예측되고 있습니다. 기술 혁신의 최전선에 있으며, 수술 정밀도와 임상 결과를 향상시키는 로봇 공학과 스마트 임플란트의 개발에 투자하고 있습니다.

세계 척추 임플란트 시장을 형성하는 주요 기업은 Spineart, Ulrich, Orthofix Holdings, B. Braun, CENTINEL SPINE, INTEGRA, Seaspine, RTI Surgical, Zimmer Biomet, Stryker, Johnson & Johnson, Globus Medical, Alphatec Spine, Medtronic, NuVasive 등이 있습니다. 척추 임플란트 업계의 각 사는 시장의 발자취를 확대하기 위해, 임플란트의 기능성과 저침습 수기와의 적합성을 높이는 전략적 연구 개발 투자에 주력하고 있습니다. 채널을 강화하기 위해 로봇 공학 및 디지털 내비게이션을 제품 포트폴리오에 통합하면 수술 정확성과 환자 만족도를 향상시키는 데 도움이 됩니다.

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 척추질환의 유병률 상승

- 저침습 수술 수요 증가

- 기술적 진보

- 선진국의 유리한 상환 정책

- 업계의 잠재적 위험과 과제

- 척추 임플란트와 수술의 고가 비용

- 선진국의 엄격한 규제 시나리오

- 시장 기회

- 척추 수술에서 AI와 로봇의 통합

- 외래 진료와 통원 진료에 대한 관심 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 미국

- 유럽

- 기술 상황

- 상환 시나리오

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 분석

- GAP 분석

- 밸류체인 분석

제4장 경쟁 구도

- 소개

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 지역별

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

- 주요 발전

- 기업 합병·인수(M&A)

- 사업 제휴?협력

- 신제품 발매

- 확장 계획

제5장 시장의 추정 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 척추 고정 임플란트

- 시궁근 스크류

- 추간체 고정 장치(IBFD)

- 로드

- 플레이트

- 케이지

- 기타 척추 고정 임플란트

- 동적 안정화 장치

- 인공추간판

- 경부

- 요추

- 기타 제품 유형

제6장 시장의 추정 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 티타늄

- 코발트 크롬

- 스테인레스 스틸

- 폴리에테르에테르케톤(PEEK)

- 기타 재료

제7장 시장의 추정 및 예측 : 수술유형별(2021-2034년)

- 주요 동향

- 개복 수술

- 저침습 수술

제8장 시장의 추정 및 예측 : 적응증별(2021-2034년)

- 주요 동향

- 변성 추간판 질환

- 척추 변형

- 척추 외상

- 골절

- 기타 적응증

제9장 시장의 추정 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 용도

제10장 시장의 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Alphatec Spine

- B. Braun

- CENTINEL SPINE

- Globus Medical

- INTEGRA

- Johnson &Johnson

- Medtronic

- NuVasive

- Orthofix Holdings

- RTI Surgical

- Seaspine

- Spineart

- Stryker

- Ulrich

- Zimmer Biomet

The Global Spinal Implants Market was valued at USD 11.8 billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 16.9 billion by 2034. The growing demand is fueled by a rising aging population, an increase in spinal disorders, a shift toward minimally invasive procedures, and technological advancements in implant materials and surgical techniques. As spinal conditions like spinal stenosis, degenerative disc disease, and herniated discs become more prevalent, especially among older individuals, the need for surgical intervention and spinal stabilization solutions continues to climb.

Obesity and sedentary lifestyles further contribute to spinal degeneration. As a result, more patients are opting for surgical correction, especially with new solutions offering reduced pain and faster recovery. The introduction of robotic systems and navigation tools in spinal surgeries has not only enhanced procedural precision but also minimized complication rates, encouraging greater use of advanced implants. Many device manufacturers are responding by designing implants tailored for minimally invasive techniques, driving broader clinical adoption globally as costs gradually decline and accessibility improves.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.8 Billion |

| Forecast Value | $16.9 Billion |

| CAGR | 3.9% |

The spinal fusion implants segment is projected to witness strong growth at a CAGR of 4.3%, reaching USD 9.3 billion by 2034. The widespread use of these devices stems from their critical role in treating spinal instability caused by degeneration or trauma. As degenerative conditions such as spondylolisthesis and disc disorders become more common, the volume of spinal fusion procedures continues to grow. New fusion implant designs made from advanced materials such as PEEK and titanium are now more commonly used due to their compatibility with the human body, enhanced strength, and better integration with surrounding bone tissue. These properties increase long-term patient outcomes, helping to solidify the segment's dominance in the market.

Titanium-based spinal implants segment is expected to generate USD 6.5 billion by 2034. Titanium remains the preferred material in spinal surgeries due to its high biocompatibility, corrosion resistance, and structural durability. It integrates seamlessly with the body, minimizing the risk of immune rejection while maintaining resilience in fluid-rich environments. Titanium implants are strong yet lightweight, which is essential for patient comfort and performance during and after the recovery phase. They withstand significant mechanical loads, making them ideal for applications such as interbody cages, rods, and plates in both cervical and lumbar spine procedures. Their long-term safety record further reinforces their position in modern spinal procedures.

U.S. Spinal Implants Market was valued at USD 6.6 billion in 2024 and is expected to grow at a CAGR of 3.5% between 2025 and 2034. The U.S. remains a global leader in spinal implant production, supported by the presence of major manufacturers including Johnson & Johnson, Stryker, Medtronic, Zimmer Biomet, and NuVasive. These companies are at the forefront of innovation, investing in the development of robotics and smart implants that enhance surgical precision and clinical outcomes. With extensive R&D networks and manufacturing facilities across the country, these firms accelerate product deployment and adoption, strengthening the country's influence in the global spinal care landscape.

Key players shaping the Global Spinal Implants Market include Spineart, Ulrich, Orthofix Holdings, B. Braun, CENTINEL SPINE, INTEGRA, Seaspine, RTI Surgical, Zimmer Biomet, Stryker, Johnson & Johnson, Globus Medical, Alphatec Spine, Medtronic, and NuVasive. To expand their market footprint, companies within the spinal implants industry are focusing on strategic R&D investments to enhance implant functionality and compatibility with minimally invasive techniques. They are actively pursuing global expansion through mergers, partnerships, and acquisitions to reach new customer bases and reinforce distribution channels. Integration of robotics and digital navigation into their product portfolios is helping them improve surgical accuracy and patient satisfaction. Firms are also collaborating with clinical institutions to validate product performance, obtain faster regulatory approvals, and strengthen their credibility among healthcare providers worldwide.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Material trends

- 2.2.4 Surgery type trends

- 2.2.5 Indication trends

- 2.2.6 End use trends

- 2.3 CXO Perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of spinal diseases

- 3.2.1.2 Increasing demand for minimally invasive procedures

- 3.2.1.3 Technological advancements

- 3.2.1.4 Favorable reimbursement policies in developed countries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of spinal implants and surgeries

- 3.2.2.2 Stringent regulatory scenario in developed countries

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and robotics in spine surgery

- 3.2.3.2 Growing focus on outpatient and ambulatory settings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 U.S.

- 3.4.2 Europe

- 3.5 Technology landscape

- 3.6 Reimbursement scenario

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis

- 3.10 GAP analysis

- 3.11 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1 By region

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Spinal fusion implants

- 5.2.1 Pedicle screws

- 5.2.2 Intervertebral body fusion device (IBFD)

- 5.2.3 Rods

- 5.2.4 Plates

- 5.2.5 Cages

- 5.2.6 Other spinal fusion implants

- 5.3 Dynamic stabilization devices

- 5.4 Artificial discs

- 5.4.1 Cervical

- 5.4.2 Lumbar

- 5.5 Other product types

Chapter 6 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Titanium

- 6.3 Cobalt chrome

- 6.4 Stainless steel

- 6.5 Polyetheretherketone (PEEK)

- 6.6 Other materials

Chapter 7 Market Estimates and Forecast, By Surgery Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Open surgery

- 7.3 Minimally invasive surgery

Chapter 8 Market Estimates and Forecast, By Indication, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Degenerative disc disease

- 8.3 Spinal deformities

- 8.4 Spinal trauma

- 8.5 Fractures

- 8.6 Other indications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Ambulatory surgical centers

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Alphatec Spine

- 11.2 B. Braun

- 11.3 CENTINEL SPINE

- 11.4 Globus Medical

- 11.5 INTEGRA

- 11.6 Johnson & Johnson

- 11.7 Medtronic

- 11.8 NuVasive

- 11.9 Orthofix Holdings

- 11.10 RTI Surgical

- 11.11 Seaspine

- 11.12 Spineart

- 11.13 Stryker

- 11.14 Ulrich

- 11.15 Zimmer Biomet