|

시장보고서

상품코드

1755359

산업용 진공 펌프 시장 : 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Industrial Vacuum Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

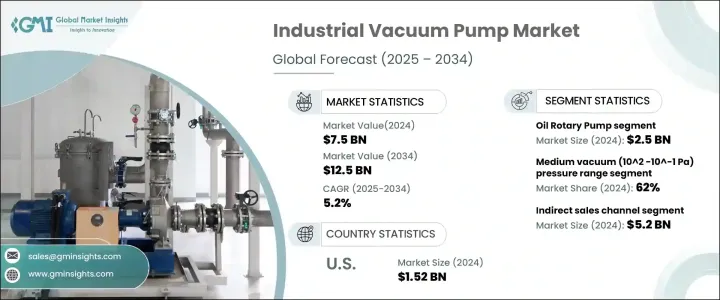

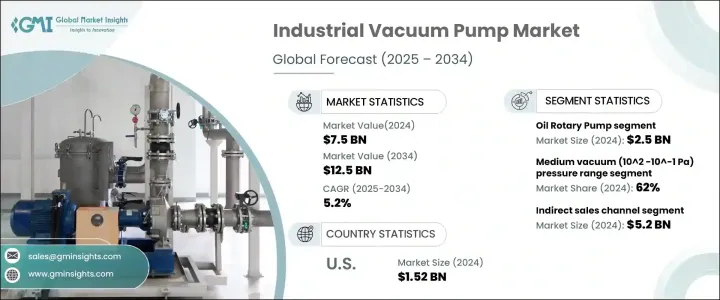

세계 산업용 진공 펌프 시장은 2024년에는 75억 달러로 평가되었으며, 여러 최종 용도 분야에 걸친 수요 증가로 CAGR 5.2%로 성장하여 2034년에는 125억 달러에 이를 것으로 예측되고 있습니다.

이러한 진공 펌프는 정밀 제조나 고순도 처리를 필요로 하는 산업에서 널리 사용되고 있으며, 시장 확대에 크게 공헌하고 있습니다.

반도체 분야의 진보에 따라 상호 연결 시장 수요도 높아지고 있습니다. 높은 선불 투자와 지속적인 유지보수 비용은 특히 중소기업에 있어서는 여전히 큰 발판이 되고 있습니다. 또한, 조작의 복잡성과 기술적인 전문지식의 필요성으로부터, 고도가 아닌 셋업에서는 채택이 어려워져, 신흥 시장에서의 성장에 한계가 생기고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 초기 시장 규모 | 75억 달러 |

| 시장 규모 예측 | 125억 달러 |

| CAGR | 5.2% |

이 지역의 대부분은 숙련된 기술자 부족에 직면해 있으며 최신 진공 시스템의 관리 및 유지 보수에 필수적인 전문 교육 프로그램에 대한 액세스가 부족합니다. 일상적인 문제 해결이나 유지보수조차도 심각한 장애가 되어 가동 중지 시간이 증가하고 장비 수명이 저하될 수 있습니다. 게다가, 복잡한 기계를 지원하기 위한 제한된 인프라와 함께, 기술 직원 파견과 관련된 높은 비용은 중소 산업이 첨단 진공 펌프 기술로 업그레이드하는 것을 더욱 망설이고 있습니다.

오일 로터리 펌프 분야는 2024년에 25억 달러를 창출하고 2034년까지 연평균 복합 성장률(CAGR) 5%로 강력한 기세를 유지할 것으로 예측됩니다. 이러한 펌프는 안정적인 진공 출력과 가변 압력 조건 하에서 지속적이고 가혹한 작동을 견딜 수 있는 능력을 특별히 평가합니다. 견고한 구조와 높은 성능으로 정확성과 일관성이 필수적인 산업 환경에서 최적의 솔루션이 되었습니다. 가혹한 공정 환경에 대한 적응성과 최소한의 다운타임은 재료 가공에서 진공 코팅에 이르기까지 다양한 분야에서의 유용성을 더욱 높여줍니다.

유통 관점에서 간접 판매 부문은 2024년 52억 달러를 창출하고 2034년까지 연평균 복합 성장률(CAGR) 4.7%로 성장할 것으로 예측됩니다. 간접 판매의 성공은 진공 펌프 제품의 광범위한 옵션을 제공하는 대리점, 리셀러 및 디지털 마켓플레이스의 확립된 네트워크에 의해 제공됩니다. 이러한 채널은 최종 사용자 조달을 단순화할 뿐만 아니라 시스템 맞춤화, 기술 교육, 구매 후 지원, 지역 재고를 통한 신속한 배송 등 부가가치 서비스를 제공합니다.

미국 산업용 진공 펌프의 2024년 시장 규모는 15억 2,000만 달러로, 2034년까지 연평균 복합 성장률(CAGR) 5.2%로 성장할 것으로 예측됩니다. 이 리더십은 전자, 의약품, 특수화학 등 고순도 제조 공정를 필요로 하는 분야에서 이 나라의 첨단 인프라가 뒷받침하고 있습니다.

세계 산업용 진공 펌프 시장에 기여하는 유명 기업은 Gardner Denver, Ebara Corporation, Pfeiffer Vacuum GmbH, Atlas Copco AB(Edwards), ULVAC Inc., Flowserve Corporation, Global Vac, Wintek Corporation, Ingersoll Rand Inc., Busch Vacuum Solutions, Becker Pump Co.Ltd., Graham Corporation, Agilent Technologies입니다. 산업용 진공 펌프 시장의 주요 기업이 채택하고 있는 주요 전략에는 제품 혁신, 생산 능력 확대, 전략적 합병 및 제휴에 대한 주력 등이 있습니다. 수술을 도입하기 위한 연구개발에 투자하고 있습니다. 각 업계에 특화된 OEM과의 제휴는 응용범위의 확대에 도움이 되고 있습니다.

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업체

- 리셀러

- 소매업체

- 트럼프 정권에 의한 관세

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(고객에 대한 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 영향요인

- 성장 촉진요인

- 반도체 및 일렉트로닉스 산업에 있어서 수요 증가

- 화학 및 제약산업 확대

- 식품 및 음료 업계에서의 채용 증가

- 제조업과 산업 프로세스의 성장

- 업계의 잠재적 위험과 과제

- 초기 투자와 유지비가 높아

- 복잡성과 기술적 과제

- 성장 촉진요인

- 기술과 혁신의 상황

- 성장 가능성 분석

- 규제 상황

- 가격 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장의 추정 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 수봉식 진공 펌프

- 오일 로터리 펌프

- 뿌리 펌프

- 건조진공펌프

- 다단 뿌리 진공 펌프

- 건조 스크류 진공 펌프

- 건조 스크롤 진공 펌프

- 건조 다이어프램 진공 펌프

- 건조 로터리 베인 진공 펌프

- 건조 잠금 피스톤 진공 펌프

- 건조 로터리 크로우 진공 펌프

- 건조 터보 진공 펌프

제6장 시장의 추정 및 예측 : 압력 범위별(2021-2034년)

- 주요 동향

- 저진공압(10^5-10^2 Pa)

- 중진공압(10^2-10^-1 Pa)

제7장 시장의 추정 및 예측 : 사이즈별(2021-2034년)

- 주요 동향

- 소형(10 m3/h 이하)

- 중형(10-100 m3/h)

- 대형(100 m3/h 이상)

제8장 시장의 추정 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 반도체

- 상하수도처리

- 화학제품 및 석유화학제품

- 광업

- 식음료

- 건설업

- 석유 및 가스

- 제약

- 기타(농업, 섬유 등)

제9장 시장의 추정 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 간접판매

제10장 시장의 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 말레이시아

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제11장 기업 프로파일

- Agilent Technologies

- Atlas Copco AB(Edwards)

- Becker Pumps Corporation

- Busch Vacuum Solutions

- Ebara Corporation

- Flowserve Corporation

- Gardner Denver

- Global Vac

- Graham Corporation

- Ingersoll Rand Inc.

- Pfeiffer Vacuum GmbH

- Tsurumi Manufacturing Co. Ltd

- ULVAC Inc.

- Wintek Corporation

The Global Industrial Vacuum Pump Market was valued at USD 7.5 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 12.5 billion by 2034, driven by the increasing demand across multiple end-use sectors. These vacuum pumps are extensively used in industries requiring precision manufacturing and high-purity processing, contributing significantly to market expansion. Their widespread application across sectors dealing with sensitive operations requiring a controlled environment has solidified their relevance in industrial workflows.

As the semiconductor segment advances, it fuels demand in interconnected markets. With rising industrial automation and cleaner production standards, vacuum pump technology is increasingly being adopted across the globe. Nevertheless, the high upfront investment and the ongoing maintenance costs remain major deterrents, especially for smaller companies. In addition, the operational complexity and the need for technical expertise make adoption more challenging in less advanced setups, creating growth limitations in emerging markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.5 Billion |

| Forecast Value | $12.5 Billion |

| CAGR | 5.2% |

Many of these regions face a shortage of skilled technicians and lack access to specialized training programs, essential for managing and maintaining modern vacuum systems. Even routine troubleshooting or maintenance can become a significant hurdle, leading to increased downtime and reduced equipment lifespan. Moreover, the high cost associated with technical staffing, coupled with limited infrastructure to support complex machinery, further deters smaller industries from upgrading to advanced vacuum pump technologies.

The oil rotary pump segment generated USD 2.5 billion in 2024 and is projected to maintain strong momentum with a CAGR of 5% through 2034. These pumps are particularly valued for their stable vacuum output and ability to withstand continuous, demanding operations under variable pressure conditions. Their robust construction and high performance make them a go-to solution in industrial environments where precision and consistency are mission-critical. Their adaptability to harsh process environments and minimal downtime further boost their utility across various sectors, from material processing to vacuum coating.

From a distribution standpoint, the indirect sales segment generated USD 5.2 billion in 2024 and is anticipated to grow at a CAGR of 4.7% through 2034. The success of indirect sales is driven by a well-established network of distributors, resellers, and digital marketplaces that offer a broad selection of vacuum pump products. These channels simplify procurement for end-users but provide value-added services like system customization, technical training, post-purchase support, and faster delivery through regional inventories.

United States Industrial Vacuum Pump Market was valued at USD 1.52 billion in 2024, projected to grow at a CAGR of 5.2% by 2034. This leadership is fueled by the country's advanced infrastructure in sectors requiring high-purity manufacturing processes, such as electronics, pharmaceuticals, and specialty chemicals. Government support for modernizing manufacturing and the widespread integration of automation technologies further strengthens the market outlook.

Prominent companies contributing to the Global Industrial Vacuum Pump Market include Gardner Denver, Ebara Corporation, Pfeiffer Vacuum GmbH, Atlas Copco AB (Edwards), ULVAC Inc., Flowserve Corporation, Global Vac, Wintek Corporation, Ingersoll Rand Inc., Busch Vacuum Solutions, Becker Pumps Corporation, Tsurumi Manufacturing Co. Ltd, Graham Corporation, and Agilent Technologies. Key strategies adopted by leading players in the industrial vacuum pump market include a strong focus on product innovation, capacity expansion, and strategic mergers or partnerships. Companies are investing in R&D to introduce energy-efficient and smart vacuum technologies, targeting increased automation and digital integration. Collaborations with industry-specific OEMs help broaden their application reach. Geographic expansion through distribution networks ensures stronger regional footprints, while after-sales services and customized offerings help boost customer retention.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Trade impact

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (Cost to customers)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook & future considerations

- 3.2.1 Trade impact

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing demand in semiconductor and electronics industry

- 3.3.1.2 Expansion in chemical and pharmaceutical industries

- 3.3.1.3 Rising adoption in food and beverage industry

- 3.3.1.4 Growth in manufacturing and industrial processes

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High initial investment and maintenance costs

- 3.3.2.2 Complexity and technical challenges

- 3.3.1 Growth drivers

- 3.4 Technology & innovation landscape

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.7 Pricing analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 – 2034, (USD Billion) (Million Units)

- 5.1 Key trends

- 5.2 Liquid ring vacuum pump

- 5.3 Oil rotary pump

- 5.4 Roots pump

- 5.5 Dry vacuum pump

- 5.6 Multi-stage roots vacuum pump

- 5.6.1 Dry screw vacuum pump

- 5.6.2 Dry scroll vacuum pump

- 5.6.3 Dry diaphragm vacuum pump

- 5.6.4 Dry rotary vane vacuum pump

- 5.6.5 Dry rocking piston vacuum pump

- 5.6.6 Dry rotary crow vacuum pump

- 5.6.7 Dry turbo vacuum pump

Chapter 6 Market Estimates & Forecast, By Pressure Range, 2021 – 2034, (USD Billion) (Million Units)

- 6.1 Key trends

- 6.2 Low vacuum (10^5-10^2 Pa)

- 6.3 Medium vacuum (10^2 -10^-1 Pa)

Chapter 7 Market Estimates & Forecast, By Size, 2021 – 2034, (USD Billion) (Million Units)

- 7.1 Key trends

- 7.2 Small (< 10 m3/h)

- 7.3 Medium (10-100 m3/h)

- 7.4 Large (> 100 m3/h)

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021 – 2034, (USD Billion) (Million Units)

- 8.1 Key trends

- 8.2 Semiconductor

- 8.3 Water & wastewater treatment

- 8.4 Chemicals and petrochemicals

- 8.5 Mining

- 8.6 Food and beverages

- 8.7 Construction

- 8.8 Oil & gas

- 8.9 Pharmaceutical

- 8.10 Others (Agricultural, textile, etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 – 2034, (USD Billion) (Million Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Billion) (Million Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 11.1 Agilent Technologies

- 11.2 Atlas Copco AB (Edwards)

- 11.3 Becker Pumps Corporation

- 11.4 Busch Vacuum Solutions

- 11.5 Ebara Corporation

- 11.6 Flowserve Corporation

- 11.7 Gardner Denver

- 11.8 Global Vac

- 11.9 Graham Corporation

- 11.10 Ingersoll Rand Inc.

- 11.11 Pfeiffer Vacuum GmbH

- 11.12 Tsurumi Manufacturing Co. Ltd

- 11.13 ULVAC Inc.

- 11.14 Wintek Corporation