|

시장보고서

상품코드

1755381

자동 모터 스타터 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Automatic Motor Starter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

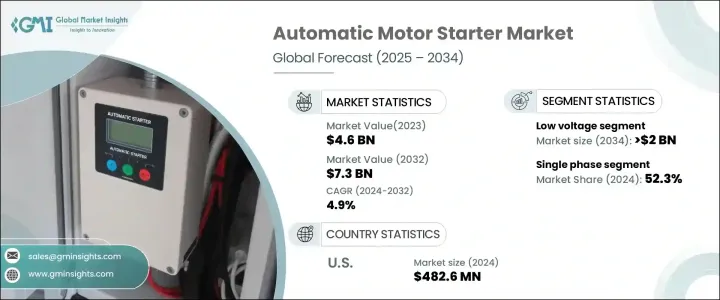

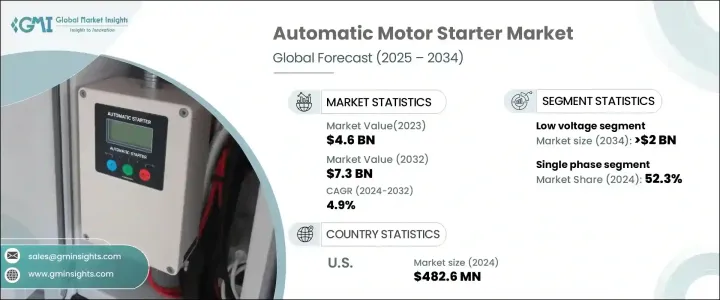

세계의 자동 모터 스타터 시장 규모는 2024년에는 46억 달러로 평가되었고, 2034년에는 73억 달러에 이를 것으로 예측되며, CAGR 4.9%로 성장할 전망입니다.

이러한 성장은 산업 자동화의 급속한 발전과 에너지 효율적인 운영에 대한 수요 증가에 의해 촉진되고 있습니다. 자동 모터 스타터는 전기 모터를 제어하여 시작 및 정지 기능을 최적화하고 과부하, 상실, 단락 회로로부터 보호합니다. 전력 공급을 제어함으로써 이 장치는 모터의 효율적인 작동, 부드러운 시작을 보장하며 잠재적인 전기적 위험으로부터 보호합니다.

화학, 석유 및 가스, 제조, 수처리 등 다양한 산업에서 전기 모터의 사용이 확대되면서 시장이 강화되고 있습니다. 이러한 산업들이 지속 가능한 실천과 디지털 전환을 추구함에 따라 자동 모터 스타터는 에너지 관리 시스템과 통합되어 에너지 사용량을 줄이고 시작 시 과부하를 방지합니다. 또한 산업용 IoT와 스마트 공장 프레임워크의 발전은 이러한 솔루션에 대한 수요를 지원합니다. 트럼프 행정부 기간 중 산업용 전기 부품, 특히 중국에서 수입된 부품에 대한 관세 인상으로 생산 비용과 공급망 차질이 발생했습니다. 단기적 영향은 어려웠지만, 이러한 무역 제한은 국내 생산을 촉진해 외국 의존도를 줄이고 장기적 공급 안정성을 개선하는 새로운 기회를 창출했습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025년-2034년 |

| 시작 금액 | 46억 달러 |

| 예측 금액 | 73억 달러 |

| CAGR | 4.9% |

중전압 부문은 2034년까지 연평균 4.5%의 성장률을 보일 것으로 예상됩니다. 이러한 시스템은 장비의 안전과 운영 효율성을 위해 대형 모터를 정밀하게 관리해야 하는 석유 및 가스, 광업, 수처리 등 고전력 운영에 필수적입니다. 중전압 스타터는 모터 시동 시 기계적 스트레스를 줄여주므로, 열악한 조건에서 중부하 산업 부하를 처리하는 시설에 필수적입니다. 이러한 시스템에 대한 수요는 인프라 업그레이드와 유틸리티 및 중공업 전반에 걸친 에너지 수요 증가에 의해 더욱 촉진되고 있습니다.

3상 자동 모터 스타터 부문은 상업용 HVAC, 스마트 관개 시스템 및 대규모 건물 인프라에 대한 설치 증가에 힘입어 2034년까지 35억 달러 규모로 성장할 것으로 예상됩니다. Modbus 및 BACnet과 같은 지능형 통신 기능을 갖춘 이러한 스타터는 실시간 시스템 모니터링, 예측 진단 및 빌딩 자동화 시스템과의 원활한 통합을 가능하게 합니다. 이는 에너지 효율, 시스템 최적화 및 원격 제어 기능을 우선으로 하는 스마트한 산업 환경으로의 성장 추세와 일치합니다.

미국의 자동 모터 스타터 2024년 시장은 산업 자동화에 고급 마이크로프로세서 기반 제어 시스템이 채택됨에 따라 2024년에 4억 8,260만 달러로 평가되었습니다. 미국 시장은 디지털 산업 생태계로의 전환이 가속화되고 재생 가능 에너지에 대한 의존도가 높아짐에 따라 강력한 모멘텀을 보이고 있습니다. 이러한 요인들은 연결되고 저공해이며 에너지 효율이 높은 모터 제어 솔루션의 확장을 위한 유리한 환경을 조성하고 있습니다.

세계의 자동 모터 스타터 산업의 혁신과 시장 경쟁을 견인하는 주요 기업은 Eaton, ABB, Danfoss, General Electric, Schneider Electric, Rockwell Automation, 미쓰비시 전기, Honeywell International, Siemens, WEG, Emerson Electric, Fuji Electric FA Components &Automation, Kalp Controls, CHINT Group, C&S Electric, Havells India, SKN-BENTEX GROUP, LOVATO ELECTRIC 등이 있습니다. 자동 모터 스타터 시장 선도 기업들은 경쟁 우위를 강화하기 위해 디지털 통합 및 에너지 효율적인 솔루션을 개발하는 데 집중하고 있습니다. 이러한 솔루션은 진화하는 산업 표준과 일치하며, 실시간 고장 감지 및 원격 모니터링 기능을 갖춘 더 스마트한 스타터 개발을 위한 연구 개발(R&D) 투자도 포함됩니다. 이들 브랜드는 혁신과 파트너십을 통해 제품 포트폴리오를 확장하여 다양한 산업 분야의 수요를 충족시키고 있습니다. 무역 장벽을 우회하고 납품 기간을 단축하기 위한 생산 현지화도 주요 전략으로 부상하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 전략적 대시보드

- 전략적 노력

- 경쟁 벤치마킹

- 혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 전압별(2021-2034년)

- 주요 동향

- 저

- 중

- 고

제6장 시장 규모와 예측 : 페이즈별(2021-2034년)

- 주요 동향

- 단상

- 삼상

제7장 시장 규모와 예측 : 용도별(2021-2034년)

- 주요 동향

- 주거용

- 상업용

- 산업용

제8장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 프랑스

- 러시아

- 영국

- 이탈리아

- 스페인

- 네덜란드

- 오스트리아

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 뉴질랜드

- 말레이시아

- 인도네시아

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 카타르

- 이집트

- 남아프리카

- 나이지리아

- 쿠웨이트

- 오만

- 라틴아메리카

- 브라질

- 페루

- 아르헨티나

제9장 기업 프로파일

- ABB

- C&S Electric

- CHINT Group

- Danfoss

- Eaton

- Emerson Electric

- Fuji Electric FA Components &Systems

- General Electric

- Havells India

- Honeywell International

- Kalp Controls

- L&T Electrical &Automation

- LOVATO ELECTRIC

- Mitsubishi Electric

- Rockwell Automation

- Schneider Electric

- Siemens

- SKN-BENTEX GROUP

- WEG

The Global Automatic Motor Starter Market was valued at USD 4.6 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 7.3 billion by 2034. The growth is fueled by the surge in industrial automation and the rising demand for energy-efficient operations. Automatic motor starters help control electric motors, enabling streamlined start-stop functions and offering protection from overloads, phase faults, and short circuits. By controlling power delivery, these devices ensure efficient motor operation, smoother startups, and safeguard against potential electrical hazards.

The expanding use of electric motors across industries such as chemicals, oil and gas, manufacturing, and water treatment is strengthening the market. As these sectors pursue sustainable practices and digital transformation, automatic motor starters are integrated with energy management systems to cut energy usage and prevent surges during startup. In addition, the advancement of industrial IoT and smart factory frameworks support the demand for these solutions. During the Trump administration, tariffs on industrial electrical parts, especially those imported from China increased production costs and supply chain disruption. Although the short-term impact was challenging, these trade restrictions also opened new opportunities for domestic production, reducing dependence on foreign sourcing and improving long-term supply stability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.6 Billion |

| Forecast Value | $7.3 Billion |

| CAGR | 4.9% |

The medium voltage segment will grow at a CAGR of 4.5% by 2034. These systems are vital for high-power operations in sectors like oil and gas, mining, and water treatment, where managing large motors with precision is critical for equipment safety and operational efficiency. Medium voltage starters help reduce mechanical stress during motor startup, making them essential for facilities handling heavy-duty industrial loads under harsh conditions. The demand for these systems is further driven by infrastructure upgrades and rising energy needs across utilities and heavy industries.

The three-phase automatic motor starter segment is expected to reach USD 3.5 billion by 2034 fueled by increased installations in commercial HVAC, smart irrigation systems, and large-scale building infrastructure. These starters with intelligent communication features like Modbus and BACnet, enabling real-time system monitoring, predictive diagnostics, and seamless integration with building automation systems. This aligns with the growing trend toward smarter industrial environments prioritizing energy efficiency, system optimization, and remote-control capabilities.

United States Automatic Motor Starter Market was valued at USD 482.6 million in 2024, bolstered by the adoption of advanced microprocessor-based control systems in industrial automation. The U.S. market is also experiencing strong momentum due to an accelerated transition to digital industrial ecosystems and an increasing reliance on renewable energy. These factors create a favorable climate for expanding connected, low-emission, and energy-conscious motor control solutions.

Key players driving innovation and market competition in the Global Automatic Motor Starter Industry include Eaton, ABB, Danfoss, General Electric, Schneider Electric, Rockwell Automation, Mitsubishi Electric, Honeywell International, Siemens, WEG, Emerson Electric, Fuji Electric FA Components & Systems, L&T Electrical & Automation, Kalp Controls, CHINT Group, C&S Electric, Havells India, SKN-BENTEX GROUP, and LOVATO ELECTRIC. To strengthen their competitive edge, leading companies in the automatic motor starter market focus on developing digitally integrated and energy-efficient solutions that align with evolving industrial standards. Strategies include investing in R&D for smarter starters with real-time fault detection and remote monitoring. These brands expand their product portfolios through innovation and partnerships to meet demand across multiple industries. Localization of production to bypass trade barriers and improve lead times has also become a key focus.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Low

- 5.3 Medium

- 5.4 High

Chapter 6 Market Size and Forecast, By Phase, 2021 - 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Single phase

- 6.3 Three phase

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Russia

- 8.3.4 UK

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Austria

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.4.6 New Zealand

- 8.4.7 Malaysia

- 8.4.8 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Qatar

- 8.5.4 Egypt

- 8.5.5 South Africa

- 8.5.6 Nigeria

- 8.5.7 Kuwait

- 8.5.8 Oman

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Peru

- 8.6.3 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 C&S Electric

- 9.3 CHINT Group

- 9.4 Danfoss

- 9.5 Eaton

- 9.6 Emerson Electric

- 9.7 Fuji Electric FA Components & Systems

- 9.8 General Electric

- 9.9 Havells India

- 9.10 Honeywell International

- 9.11 Kalp Controls

- 9.12 L&T Electrical & Automation

- 9.13 LOVATO ELECTRIC

- 9.14 Mitsubishi Electric

- 9.15 Rockwell Automation

- 9.16 Schneider Electric

- 9.17 Siemens

- 9.18 SKN-BENTEX GROUP

- 9.19 WEG