|

시장보고서

상품코드

1766187

자동차용 엣지 컴퓨팅 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Edge Computing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

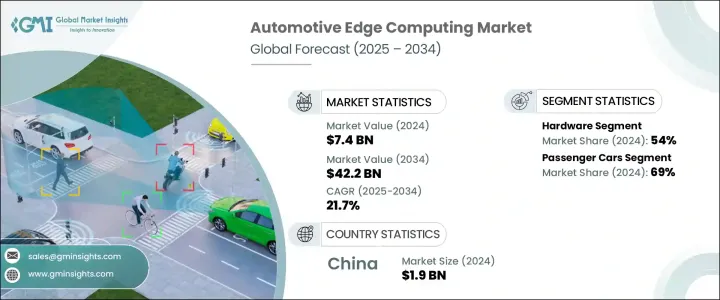

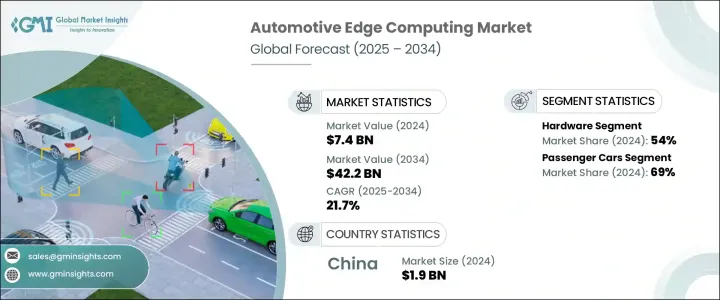

세계의 자동차용 엣지 컴퓨팅 시장 규모는 2024년 74억 달러로 평가되었으며, 2034년까지 422억 달러에 이르고 CAGR 21.7%의 성장이 예측되고 있습니다.

자동차 산업이 급속히 진화함에 따라 자동차는 방대한 양의 데이터를 실시간으로 처리할 수 있는 지능형 플랫폼이 되고 있습니다. 이러한 변화는 자율주행 기술과 커넥티드 모빌리티 솔루션의 급증으로 추진되고 있습니다. 결과적으로 기존의 중앙 집중식 컴퓨팅 모델에서 에지 기반 데이터 처리로 크게 이동합니다.

자동차 엣지 컴퓨팅은 복잡한 자동차 기능을 관리하는 데 필요한 낮은 대기 시간과 높은 대역폭을 제공함으로써 이러한 이동을 지원하는 중요한 역할을 합니다. 엣지 컴퓨팅은 현대 자동차의 안전하고 효율적인 운영에 필수적인 실시간 의사 결정 능력을 강화합니다. 커넥티드 기능의 보급과 첨단 차량 탑재 센서의 이용 확대는 데이터의 폭발적인 증가에 기여하고 있으며, 차량 탑재 분석과 즉각 대응 시스템에 대한 절박한 요구를 창출하고 있습니다. 엣지 컴퓨팅은 데이터를 멀리 떨어진 클라우드 센터로 라우팅하는 대신 차량이 출처에서 분석하고 이를 기반으로 행동할 수 있도록 합니다. 이렇게 하면 네트워크 혼잡과 응답 시간이 줄어들어 성능, 안전성 및 신뢰성이 향상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 74억 달러 |

| 예측 금액 | 422억 달러 |

| CAGR | 21.7% |

이는 운전 지원, 예지 보전, 지능형 경로 계획 등의 용도에 필수적이 되고 있습니다. 제조업체가 소프트웨어 중심 차량 아키텍처로 전환하는 동안 차세대 이동성을 위해 구축된 확장성이 높고 안전하고 효율적인 운송 시스템을 구축하려면 첨단 에지 플랫폼 통합이 필수적입니다.

구성 요소의 관점에서 시장은 하드웨어, 소프트웨어, 서비스로 분류됩니다. 하드웨어는 2024년 세계 시장 점유율의 거의 54%를 차지하는 주요 부문으로 떠오르며, 예측 기간 동안 22% 이상의 CAGR로 성장할 것으로 예측됩니다. 고성능 컴퓨팅 유닛, AI에 최적화된 프로세서, 차량용 등급 모듈의 도입이 증가하고 있다는 것은 복잡한 데이터 스트림을 처리하는 에지 하드웨어의 중요성이 높아지고 있음을 뒷받침합니다. 이러한 구성 요소는 실시간 모니터링 및 자율 주행 네비게이션과 같은 용도의 지속적인 처리 능력을 보장하면서 가혹한 차량 환경을 견딜 수 있도록 설계되었습니다.

차량별로, 시장은 승용차와 상용차로 나뉘어져 있습니다. 승용차는 2024년에 시장 총 수익의 약 69%를 차지하고 지배적인 지위를 차지했습니다. ADAS(첨단 운전 지원 시스템)에 대한 수요가 증가함에 따라 엣지 컴퓨팅 기술의 도입을 촉진하고 있습니다.

배포 모드를 기반으로 업계는 클라우드 기반과 On-Premise 솔루션으로 구분됩니다. 클라우드 기반 배포는 유연성, 확장성, 폭넓은 커넥티드카 기능을 보조하는 능력으로, 계속해서 시장에서 큰 점유율을 차지하고 있습니다. 이러한 플랫폼은 원격 업데이트, 중앙 집중식 조정, 자율 주행 및 차량 관리의 새로운 이용 사례에 필수적입니다.

지역별로는 중국이 2024년 세계의 자동차용 엣지 컴퓨팅 시장을 선도해 약 19억 달러의 수익을 올리고 아시아태평양 시장의 약 63%를 차지했습니다. 중국은 세계 최대 자동차 생산국이라는 지위와 맞물려, 스마트 모빌리티 구상의 급속한 확대로 에지 기술 채용의 최전선에 위치하고 있습니다.

자동차 제조업체와 기술 제공업체가 보다 빠르고 지능적인 분산 처리 시스템을 선호하기 때문에 자동차용 엣지 컴퓨팅의 상황은 구조적인 변혁기를 맞이하고 있습니다. 각 회사는 현재 AI 기능, 경량 데이터 처리 프레임워크, 견고한 보안 프로토콜을 자동차 환경에 직접 통합하는 데 주력하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 자율주행차와 커넥티드카 수요 증가

- 차재 센서로부터의 데이터량 증가

- 강화된 인포테인먼트와 차내 체험

- 도로 안전과 데이터의 현지화에 관한 정부 규제

- 업계의 잠재적 위험 및 과제

- 높은 초기 인프라 비용

- 데이터 프라이버시와 컴플라이언스의 복잡성

- 시장 기회

- 의사결정을 위한 AI와 ML 통합

- 스마트 시티와 V2X 에코시스템 확대

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 비용 내역 분석

- 소프트웨어 개발 및 라이선싱 비용

- 도입 및 통합 비용

- 보수 및 지원 비용

- 사이버 보안 및 컴플라이언스 비용

- 교육 및 변경 관리 비용

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 삭감 전략

- 생산에 있어서의 에너지 효율

- 친환경적 노력

- 탄소발자국의 고려

- 이용 사례

- 최상의 시나리오

- 소비자 행동과 채용 동향

- 사용자 경험과 인터페이스 동향

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카 항공

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추정 및 예측 : 컴포넌트별, 2021-2034년

- 주요 동향

- 하드웨어

- 에지 노드

- 게이트웨이

- 에지 서버

- 소프트웨어

- 엣지 디바이스 관리

- 애널리틱스 및 처리 소프트웨어

- 보안 소프트웨어

- 서비스

- 전문

- 시스템 통합 및 전개

- 컨설팅 및 전략

- 트레이닝 및 지원

- 매니지드

- 원격 모니터링 및 관리

- 유지 보수 업데이트

- 보안관리

- 전문

제6장 시장 추정 및 예측 : 차량별, 2021-2034년

- 주요 동향

- 승용차

- 세단

- 해치백

- SUV

- 상용차

- 소형

- 중형

- 대형

제7장 시장 추정 및 예측 : 배포 모드별, 2021-2034년

- 주요 동향

- 클라우드 기반

- On-Premise

제8장 시장 추정 및 예측 : 기업 규모별, 2021-2034년

- 주요 동향

- 중소기업

- 대기업

제9장 시장 추정 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 자율주행 및 커넥티드 드라이빙

- 차내 경험 및 인포테인먼트

- 예측 유지 보수 및 진단

- 차량 및 트래픽 관리

- 사이버 보안 데이터 보호

제10장 시장 추정 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Amazon

- Arteris IP

- Autotalks

- Bosch Group

- Cisco

- ETAS GmbH

- FogHorn Systems

- GreenWave Systems

- Hewlett Packard Enterprise(HPE)

- Huawei

- IBM

- Infineon Technologies

- Intel

- Microsoft

- Mobileye

- NVIDIA

- NXP Semiconductors

- Qualcomm Technologies

- Siemens

- Teradata

The Global Automotive Edge Computing Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 21.7% to reach USD 42.2 billion by 2034. As the automotive industry rapidly evolves, vehicles are increasingly becoming intelligent platforms capable of processing vast amounts of data in real time. This transformation is being driven by the surge in autonomous driving technologies and connected mobility solutions. As a result, there is a significant shift away from traditional centralized computing models to edge-based data processing, which places computational power closer to the source-inside the vehicle itself.

Automotive edge computing is playing a pivotal role in supporting this shift by delivering the low latency and high bandwidth required to manage complex in-vehicle functions. It enhances real-time decision-making capabilities critical to the safe and efficient operation of modern vehicles. The proliferation of connected features and the growing use of advanced in-vehicle sensors are contributing to an explosion of data, creating a pressing need for on-board analytics and instant response systems. Rather than routing data to distant cloud centers, edge computing empowers vehicles to analyze and act on information at the source, reducing network congestion and response time while enhancing performance, safety, and reliability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $42.2 Billion |

| CAGR | 21.7% |

This is becoming essential for applications such as driver assistance, predictive maintenance, and intelligent route planning. As manufacturers transition toward software-centric vehicle architectures, the integration of advanced edge platforms becomes vital for creating scalable, secure, and efficient transportation systems built for the next generation of mobility.

In terms of components, the market is categorized into hardware, software, and services. Hardware emerged as the leading segment in 2024, contributing nearly 54% of the global market share, and is anticipated to grow at a CAGR exceeding 22% throughout the forecast period. The rising deployment of high-performance computing units, AI-optimized processors, and automotive-grade modules underscores the growing importance of edge hardware in handling complex data streams. These components are engineered to endure extreme vehicle environments while ensuring continuous processing power for applications like real-time monitoring and autonomous navigation.

By vehicle type, the market is divided into passenger cars and commercial vehicles. Passenger cars held a dominant position in 2024, accounting for approximately 69% of the total market revenue. This segment is set to expand at a CAGR of over 23% between 2025 and 2034. The increasing demand for integrated digital features, personalized driver experiences, and advanced driver-assist systems in passenger vehicles is driving the uptake of edge computing technologies. These vehicles require robust processing capabilities to manage data inputs from various embedded systems, enabling real-time decisions that improve both user experience and vehicle safety.

Based on deployment mode, the industry is segmented into cloud-based and on-premises solutions. Cloud-based deployment continues to command a significant share of the market due to its flexibility, scalability, and ability to support a wide range of connected vehicle functions. These platforms allow seamless software integration, remote updates, and centralized coordination, which are critical for emerging use cases in autonomous driving and fleet management. Their widespread adoption is being propelled by the increasing reliance on vehicle-to-cloud infrastructure that supports services like dynamic route optimization, infotainment delivery, and predictive diagnostics.

Regionally, China led the global automotive edge computing market in 2024, generating around USD 1.9 billion in revenue and capturing roughly 63% of the Asia Pacific market. The country's rapid expansion in smart mobility initiatives, coupled with its position as the world's largest automotive producer, has positioned it at the forefront of edge technology adoption. Strong governmental support, fast-paced development in electric vehicles, and massive deployment of connected vehicle systems continue to bolster market growth in the region.

The automotive edge computing landscape is undergoing a structural transformation as automakers and technology providers prioritize faster, more intelligent, and decentralized processing systems. Growing requirements for instantaneous data interpretation, especially in safety-sensitive driving conditions, are prompting a fundamental rethinking of how information is handled within vehicles. Companies are now focused on integrating AI capabilities, lightweight data processing frameworks, and robust security protocols directly into in-vehicle environments. These advancements are designed to transform raw sensor outputs into meaningful insights that can be acted upon in real time, thus enabling safer, more adaptive, and more efficient transportation systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Vehicle

- 2.2.4 Deployment mode

- 2.2.5 Enterprise size

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for autonomous and connected vehicles

- 3.2.1.2 Increasing data volume from in-vehicle sensors

- 3.2.1.3 Enhanced infotainment and in-vehicle experience

- 3.2.1.4 Government regulations for road safety and data localization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial infrastructure cost

- 3.2.2.2 Data privacy & compliance complexities

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with AI and ML for decision-making

- 3.2.3.2. Smart city & V2 X ecosystem expansion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

- 3.13 Consumer behaviour & adoption trends

- 3.14 User experience & interface trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Edge nodes

- 5.2.2 Gateways

- 5.2.3 Edge servers

- 5.3 Software

- 5.3.1 Edge device management

- 5.3.2 Analytics & processing software

- 5.3.3 Security software

- 5.4 Services

- 5.4.1 Professional

- 5.4.1.1 System integration & deployment

- 5.4.1.2 Consulting & strategy

- 5.4.1.3 Training & support

- 5.4.2 Managed

- 5.4.2.1 Remote monitoring & management

- 5.4.2.2 Maintenance & updates

- 5.4.2.3 Security management

- 5.4.1 Professional

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Sedans

- 6.2.2 Hatchbacks

- 6.2.3 SUVs

- 6.3 Commercial vehicles

- 6.3.1 Light duty

- 6.3.2 Medium duty

- 6.3.3 Heavy duty

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Cloud-based

- 7.3 On-premises

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Autonomous and connected driving

- 9.3 In-vehicle experience & infotainment

- 9.4 Predictive maintenance & diagnostics

- 9.5 Fleet & traffic management

- 9.6 Cybersecurity & data protection

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Amazon

- 11.2 Arteris IP

- 11.3 Autotalks

- 11.4 Bosch Group

- 11.5 Cisco

- 11.6 ETAS GmbH

- 11.7 FogHorn Systems

- 11.8 GreenWave Systems

- 11.9 Hewlett Packard Enterprise (HPE)

- 11.10 Huawei

- 11.11 IBM

- 11.12 Infineon Technologies

- 11.13 Intel

- 11.14 Microsoft

- 11.15 Mobileye

- 11.16 NVIDIA

- 11.17 NXP Semiconductors

- 11.18 Qualcomm Technologies

- 11.19 Siemens

- 11.20 Teradata