|

시장보고서

상품코드

1766219

전도성 폴리머 시장 : 기회, 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Conductive Polymers (PEDOT, PANI) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

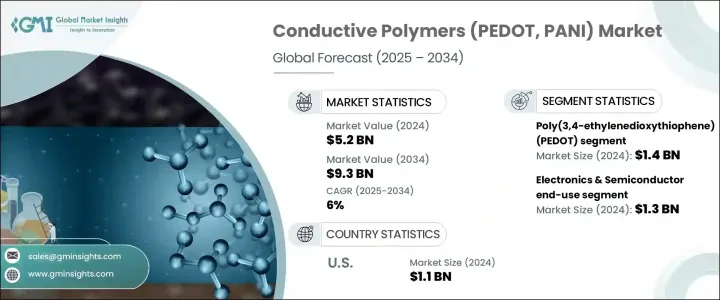

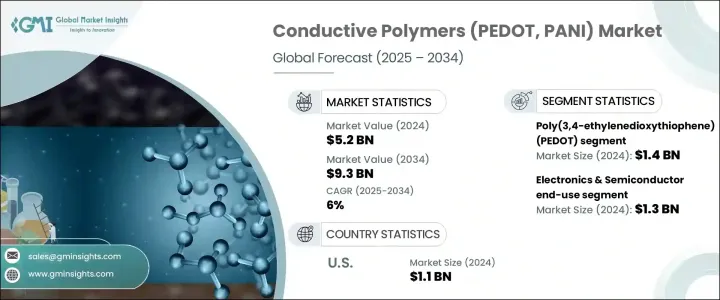

세계의 전도성 폴리머(PEDOT, PANI) 시장은 2024년 52억 달러로 평가되었고 2034년에는 93억 달러에 이를 것으로 예측되며, CAGR 6%로 성장할 전망입니다. 시장 확장은 거시경제 성장의 촉매제 역할을 계속하고 있는 인프라 개발, 정부 지출 및 광범위한 산업 생산과 밀접한 관련이 있습니다. 전 세계 제조업의 꾸준한 성장과 도시화는 전도성 재료에 대한 강력한 수요 곡선을 형성하고 있습니다. 이러한 동향은 국제 산업 보고서와도 일치하며, 데이터와 예측의 영향을 받는 전 세계 수요가 더 광범위한 경제 변화에 의해 형성되는 방식을 잘 보여줍니다. 가공 기술의 지속적인 발전으로 생산 비용이 낮아지고 효율성이 향상되어 시장 경쟁력이 촉진되었습니다.

동시에 환경 정책 규제로 인해 공급망 전반에 걸쳐 더 깨끗한 생산 관행과 재활용이 촉진되고 있습니다. 이러한 전환은 지속 가능한 성장을 위한 새로운 기회를 창출하고 있습니다. 신흥 시장의 중산층이 증가하면서 주요 최종 사용자 부문인 전자, 운송 및 에너지 저장 솔루션에 대한 수요가 더욱 증가하고 있습니다. 전 세계적으로 공급망의 어려움이 지속되고 있지만, 적응형 프레임워크, 자동화 및 기술 혁신을 통해 예측 기간 동안 시장이 꾸준히 성장할 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 52억 달러 |

| 예측 금액 | 93억 달러 |

| CAGR | 6% |

폴리아닐린(PANI) 부문은 다양한 환경 조건에서 적응력이 뛰어난 전도성과 탄력성 덕분에 2024년에 주목할 만한 매출을 올렸습니다. 이 폴리머는 산업 및 운송 부문의 활동 증가에 힘입어 부식 방지 및 센서 기반 응용 분야에서 연간 약 10%의 수요 증가를 보였습니다. 앞으로 시장은 수요가 가속화됨에 따라 이러한 상승 추세를 유지할 것으로 예상됩니다. 다른 폴리머 유형은 복잡한 처리 문제와 제한된 확장성으로 인해 여전히 억제 요인에 직면해 있습니다. 이는 대규모 사용에서 호환성, 통합 및 구조적 안정성을 개선하기 위한 혁신의 필요성을 나타냅니다.

2024년에 본질적 전도성 폴리머(ICP) 부문은 23억 달러 규모로, 2034년까지 연평균 6.1%의 성장률을 보일 것으로 예상됩니다. 전도성 폴리머 복합재, 특히 폴리머-금속 및 폴리머-탄소 조합의 사용이 증가하면서 기계적 성능과 전도성이 향상되어 수요가 증가하고 있습니다. 탄소 기반 복합재료의 연간 수요는 자동차 및 에너지 저장 산업에서의 채택으로 인해 20% 증가한 것으로 보고되었습니다. 이 복합재료는 폴리머 매트릭스와 전도성 필러로부터 강도를 얻어 차세대 응용 분야에 적합한 고도로 다기능적인 재료로 자리매김하고 있습니다.

독일의 전도성 폴리머(PEDOT, PANI) 시장은 최첨단 제조 기술과 지속 가능한 폴리머 복합재의 통합에 집중한 결과 2024년에 상당한 점유율을 차지했습니다. 친환경 생산으로의 전환은 엄격한 환경 정책과도 부합합니다. 지역 내 전도성 폴리머 수입량은 연간 12% 증가했으며, 이는 자동차 및 항공우주 제조업체의 수요 증가를 충족시키기 위한 것입니다. 이는 현지 산업이 EU의 지속 가능성 지침에 부합하기 위해 고급 친환경 소재로 전환하고 있음을 보여줍니다.

세계의 전도성 폴리머(PEDOT, PANI) 시장을 지배하는 주요 기업으로는 Heraeus Holding과 Sigma-Aldrich(모회사인 Merck 산하)가 있으며, 두 기업 모두 강력한 제품 포트폴리오와 확고한 시장 영향력을 보유하고 있어 지속적인 산업 확장에 크게 기여하고 있습니다. 전도성 폴리머 시장에서 활동하는 기업들은 시장 입지를 강화하기 위해 혁신, 수직 통합, 지역 확장을 병행하고 있습니다. 선도 기업들은 폴리머 가공 방법을 발전시키고, 전기적 특성을 개선하며, 진화하는 산업 표준을 충족하는 복합 재료를 개발하기 위해 R&D에 투자하고 있습니다. 특히 전자, 자동차 및 에너지 저장 분야와 같은 최종 사용 산업과의 파트너십을 통해 기업들은 응용 분야별 재료를 공동 개발할 수 있습니다. 또한 기업들은 공급망의 취약성을 줄이기 위해 전 세계 유통 채널을 강화하고 원자재의 접근성을 확보하고 있습니다. 지속 가능성은 또 다른 주요 전략적 축으로, 여러 기업들이 재활용 가능한 폴리머를 개발하고 친환경 제조 기술을 구현하고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 산업에 미치는 영향요인

- 성장 촉진요인

- 산업의 잠재적 리스크 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속 가능한 사례

- 폐기물 삭감 전략

- 생산에 있어서의 에너지 효율

- 친환경 활동

- 카본 풋 프린트의 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카 항공

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측 : 유형별(2021-2034년)

- 폴리(3,4-에틸렌디옥시티오펜)(PEDOT)

- 폴리아닐린(PANI)

- 폴리피롤(PPy)

- 폴리티오펜(PTh)

- 기타 전도성 폴리머

제6장 시장 추정 및 예측 : 전도성 메커니즘별(2021-2034년)

- 주요 동향

- 본질적 전도성 폴리머(ICP)

- 전도성 폴리머 복합재료(CPC)

- 폴리머 탄소 복합재료

- 폴리머 금속 복합재료

- 기타 복합재료

- 유기 혼합 이온 전자 전도체(OMIEC)

제7장 시장 추정 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 정전기 방지 포장

- 커패시터

- 배터리

- 센서

- 유기 LED(OLED)

- 태양전지

- 액추에이터

- 일렉트로크로믹 디바이스

- 전자기 간섭(EMI) 차폐

- 인쇄회로기판(PCB)

- 슈퍼커패시터

- 기타

제8장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 전자 및 반도체

- 에너지

- 헬스케어와 바이오메디컬

- 자동차

- 항공우주 및 방위

- 섬유 및 웨어러블

- 산업

- 포장

- 기타

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Agfa-Gevaert NV

- Celanese Corporation

- Merck KGaA

- Solvay SA

- 3M Company

- SABIC

- Covestro AG

- Henkel AG & Co. KGaA

- Heraeus Holding GmbH

- PolyOne Corporation(Avient Corporation)

- Rieke Metals, LLC

- RTP Company

- Lubrizol Corporation

- Asbury Carbons

- Sigma-Aldrich Corporation(Merck Group)

- Panipol Oy

- Polyone Corporation

- Premix Group

- Hyperion Catalysis International

- Ormecon GmbH

The Global Conductive Polymers (PEDOT, PANI) Market was valued at USD 5.2 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 9.3 billion by 2034. Market expansion is closely tied to infrastructure development, government spending, and broader industrial output, which continue to act as macroeconomic growth catalysts. The steady rise in global manufacturing and urbanization contributes to a robust demand curve for conductive materials. These trends align with international industry reports and illustrate how global demand, while influenced by data and projections, is also shaped by broader economic shifts. The continued progress in processing technologies has lowered production costs and boosted efficiency, driving market competitiveness.

At the same time, environmental policy regulations have prompted cleaner production practices and recycling across supply chains. This transition is creating new opportunities for sustainable growth. The rising middle class in emerging markets adds further momentum, boosting demand for electronics, transportation, and energy storage solutions-all key end-user sectors. While supply chain challenges persist globally, adaptive frameworks, automation, and technical innovation are enabling the market to grow steadily throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.2 billion |

| Forecast Value | $9.3 billion |

| CAGR | 6% |

The polyaniline (PANI) segment generated notable revenues in 2024 due to its adaptable conductivity and resilience under varying environmental conditions. The polymer has seen approximately 10% annual growth in demand from corrosion protection and sensor-based applications, driven by increased activity across industrial and transportation sectors. Looking ahead, the market is expected to maintain this upward trend as demand accelerates. Other polymer types still face constraints due to complex processing challenges and limited scalability. This points to a need for innovation to improve compatibility, integration, and structural stability in large-scale use.

In 2024, the inherently conductive polymers (ICPs) segment stood at USD 2.3 billion and is anticipated to grow at a 6.1% CAGR through 2034. The rising use of conductive polymer composites-especially Polymer-Metal and Polymer-Carbon combinations-is driving demand due to their enhanced mechanical performance and conductivity. Annual demand for carbon-based composites has reportedly grown by 20%, largely fueled by adoption in the automotive and energy storage industries. These composites gain strength from both their polymer matrices and conductive fillers, creating highly versatile materials for next-gen applications.

Germany Conductive Polymers (PEDOT, PANI) Market held a sizeable share in 2024, due to its strong focus on integrating sustainable polymer composites alongside cutting-edge manufacturing practices. The push toward greener production is aligned with strict environmental policies. Imports of conductive polymers into the region have seen a 12% annual increase, largely to meet the rising demand from automotive and aerospace manufacturers. This highlights how local industries are shifting toward advanced, eco-friendly materials in compliance with EU sustainability mandates.

Key players dominating the Global Conductive Polymers (PEDOT, PANI) Market include Heraeus Holding and Sigma-Aldrich (operating under its parent group, Merck), both of which possess strong product portfolios and established market influence that contribute significantly to ongoing industry expansion. Companies operating in the conductive polymers market are focusing on a mix of innovation, vertical integration, and regional expansion to reinforce their market presence. Leading firms are investing in R&D to advance polymer processing methods, enhance electrical properties, and develop composites that meet evolving industrial standards. Partnerships with end-use industries-especially in electronics, automotive, and energy storage-allow companies to co-develop application-specific materials. Firms are also strengthening their global distribution channels and securing raw material access to reduce supply chain vulnerabilities. Sustainability is another major strategic pillar, with several companies developing recyclable polymers and implementing green manufacturing techniques.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Conduction mechanism

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Poly(3,4-ethylenedioxythiophene) (PEDOT)

- 5.2 Polyaniline (PANI)

- 5.3 Polypyrrole (PPy)

- 5.4 Polythiophene (PTh)

- 5.5 Other conductive polymers

Chapter 6 Market Estimates & Forecast, By Conduction Mechanism, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Inherently conductive polymers (ICPs)

- 6.3 Conductive polymer composites (CPCs)

- 6.3.1 Polymer-carbon composites

- 6.3.2 Polymer-metal composites

- 6.3.3 Other composites

- 6.4 Organic mixed ionic-electronic conductors (OMIECs)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Anti-static packaging

- 7.3 Capacitors

- 7.4 Batteries

- 7.5 Sensors

- 7.6 Organic light-emitting diodes (OLEDs)

- 7.7 Solar cells

- 7.8 Actuators

- 7.9 Electrochromic devices

- 7.10 Electromagnetic interference (EMI) shielding

- 7.11 Printed circuit boards (PCBs)

- 7.12 Supercapacitors

- 7.13 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Electronics & semiconductor

- 8.3 Energy

- 8.4 Healthcare & biomedical

- 8.5 Automotive

- 8.6 Aerospace & defense

- 8.7 Textiles & wearables

- 8.8 Industrial

- 8.9 Packaging

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Agfa-Gevaert N.V.

- 10.2 Celanese Corporation

- 10.3 Merck KGaA

- 10.4 Solvay S.A.

- 10.5 3M Company

- 10.6 SABIC

- 10.7 Covestro AG

- 10.8 Henkel AG & Co. KGaA

- 10.9 Heraeus Holding GmbH

- 10.10 PolyOne Corporation (Avient Corporation)

- 10.11 Rieke Metals, LLC

- 10.12 RTP Company

- 10.13 Lubrizol Corporation

- 10.14 Asbury Carbons

- 10.15 Sigma-Aldrich Corporation (Merck Group)

- 10.16 Panipol Oy

- 10.17 Polyone Corporation

- 10.18 Premix Group

- 10.19 Hyperion Catalysis International

- 10.20 Ormecon GmbH