|

시장보고서

상품코드

1766241

도세탁셀 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Docetaxel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

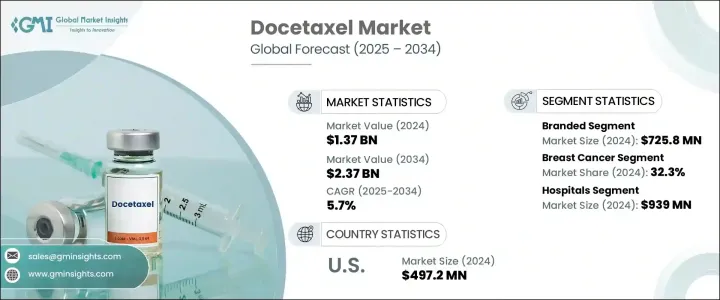

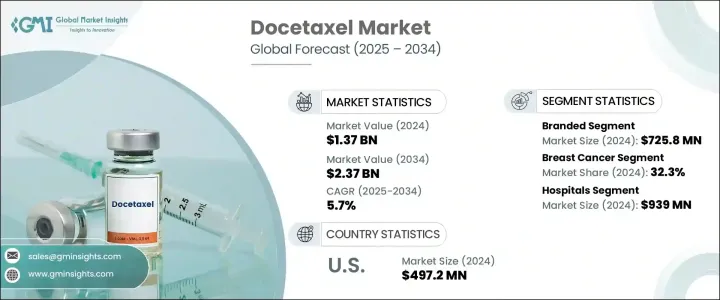

세계의 도세탁셀 시장 규모는 2024년 13억 7,000만 달러에 달했고, CAGR 5.7%로 성장하여 2034년까지 23억 7,000만 달러에 이를 것으로 예측됩니다.

이 성장은 도세탁셀이 널리 사용되는 유방암, 폐암, 전립선암, 위암 등 다양한 암의 이환율 증가가 주요 요인입니다. 트리플 네거티브 유방암이나 거세 저항성 전립선암 등의 진행암 환자의 생존율 향상에 도움이 되고 있습니다. 또한 나노 입자 제제나 리포솜 캡슐화 등의 약물 전달 방법의 혁신에 의해 생체이용률이 향상되어, 독성도 경감되었기 때문에

바이오시밀러나 제네릭 의약품의 승인이 진행됨에 따라, 특히 중저소득 지역에서는 약제가 보다 입수하기 쉬워지고 있는 한편, 암 연구개발에 대한 주목의 고조가 이 필수 세포독성 약제 수요를 밀어 올리고 있습니다. 부작용의 원격 모니터링을 통해 보다 나은 치료의 개별화를 가능하게 하는 역할을 담당하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 13억 7,000만 달러 |

| 예측 금액 | 23억 7,000만 달러 |

| CAGR | 5.7% |

도세탁셀 시장의 브랜드 부문은 2024년에 7억 2,580만 달러를 창출해 확립된 임상적 평판과 오리지널 제제의 유효성으로 이익을 얻고 있습니다. 유방암, 비소세포폐암(NSCLC), 전립선암 등의 복잡한 암을 치료하는 경우, 특히 병원에서의 치료에서는 종양 전문의에게 브랜드품의 도세탁셀이 선호되는 경우가 많습니다. 또한, 새로운 투여 방법이나 병용 요법에 대한 투자가,

2024년에는 유방암 분야가 HER2 음성 및 트리플 네거티브 유방암 환자의 조기 및 진행 치료 요법으로 32.3%를 차지했습니다.

미국의 도세탁셀 시장은 2024년에 4억 9,720만 달러로 평가되었습니다. 암에 대한 의식이 높아지면서 지속적인 임상 연구가 미국 시장의 성장을 뒷받침하고 있습니다.

세계 도세탁셀 업계의 주요 기업으로는 Alchem International, Alkem Labs, Arch Pharmalabs, Aspen Pharmacare, Cipla, Cisen Pharmaceutical, LGM Pharma, Phyton Biotech, Qilu Pharmaceutical, Teva Active Pharmaceutical Ingredients(TAPI) Remedies, Xiromed 등이 있습니다. 도세탁셀 시장에서 사업을 전개하는 기업은 새로운 제제, 전달 방법 및 병용 요법을 제공함으로써 제품 포트폴리오의 확대에 주력하고 있습니다. 기업이 바이오시밀러나 제네릭 의약품에 투자하고 비용에 민감한 시장에 진입함으로써, 이 중요한 의약품에 대한 폭넓은 액세스를 확보하고 있습니다. 또한, 맞춤형 의료나 첨단 디지털 헬스 기술의 개발에 의해 기업은 환자의 요구에 보다 잘 대응해, 치료 성적을 향상시킬 수 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계의 암 이환율의 상승

- 병용 요법의 채용 증가

- 선호되는 규제 승인 및 지침

- 의약품 제제에 있어서의 기술의 진보

- 업계의 잠재적 위험 및 과제

- 심각한 부작용과 독성 우려

- 특허의 만료와 제네릭 의약품의 경쟁

- 시장 기회

- 개별화 종양 치료 접근법 확대

- 종양학 연구개발 투자 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 가격 동향

- 지역별

- 제품 유형별

- 미래 시장 동향

- 상환 시나리오

- 상환 정책이 시장 성장에 미치는 영향

- 소비자 행동 분석

- 무역 통계(HS코드)

- 주요 수입국

- 주요 수출국

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별, 2021-2034년

- 주요 동향

- 브랜드

- 제네릭 의약품

제6장 시장 추계 및 예측 : 적응증별, 2021-2034년

- 주요 동향

- 유방암

- 비소세포폐암(NSCLC)

- 호르몬 저항성 전립선암

- 위선암

- 두경부 편평상피암(HNSCC)

- 기타 적응증

제7장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 종양학 클리닉

- 기타 최종 용도

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Alchem International

- Alkem Labs

- Arch Pharmalabs

- Aspen Pharmacare

- Cipla

- Cisen Pharmaceutical

- LGM Pharma

- Phyton Biotech

- Qilu Pharmaceutical

- Teva Active Pharmaceutical Ingredients(TAPI)

- Teva Pharmaceuticals

- Venus Remedies

- Xiromed

The Global Docetaxel Market was valued at USD 1.37 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 2.37 billion by 2034. This growth is largely driven by the increasing incidence of various cancers, including breast, lung, prostate, and gastric cancers, where docetaxel is widely used. As a second-generation taxane, docetaxel stabilizes microtubules and halts the division of cancer cells, making it a crucial part of chemotherapy regimens. It is particularly effective in combination therapies, helping to improve survival rates for patients with advanced cancers, such as triple-negative breast cancer and castration-resistant prostate cancer. Additionally, innovations in drug delivery methods, such as nanoparticle formulations and liposomal encapsulations, have improved their bioavailability and reduced toxicity, expanding their clinical applications.

The growing approvals for biosimilars and generic docetaxel are making the drug more accessible, particularly in lower-middle-income regions, while the increasing focus on oncology R&D boosts demand for this essential cytotoxic agent. Digital health technologies also play a role by enabling better treatment personalization through remote monitoring of treatment responses and side effects. Furthermore, greater cancer awareness, urbanization, and early diagnosis efforts are contributing to the broader reliance on chemotherapy and drugs like docetaxel.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.37 Billion |

| Forecast Value | $2.37 Billion |

| CAGR | 5.7% |

The branded segment of the docetaxel market generated USD 725.8 million in 2024, benefiting from the established clinical reputation and efficacy of original formulations. Despite the presence of generics, branded products continue to dominate in developed markets due to their trusted safety profiles, regulatory approvals, and high-quality standards. Branded docetaxel is often preferred by oncologists for treating complex cancers such as breast cancer, non-small cell lung cancer (NSCLC), and prostate cancer, particularly in hospital settings. Moreover, the investment in new delivery methods and combination therapies further strengthens the brand's value.

In 2024, breast cancer segment held 32.3% driven by early and advanced treatment regimens for HER2-negative and triple-negative breast cancer patients. It is commonly used in combination treatments like TAC (docetaxel, doxorubicin, and cyclophosphamide), which have been shown to improve survival outcomes. Advances in personalized oncology systems continue to increase the demand for docetaxel in managing breast cancer cases.

U.S. Docetaxel Market was valued at USD 497.2 million in 2024. Factors such as favorable reimbursement policies, growing precision oncology services, and a focus on personalized medicine are fueling the demand. Furthermore, the expansion of outpatient chemotherapy access, increasing cancer awareness, and continuous clinical research are reinforcing the U.S. market's growth. The role of the U.S. as a key market is further strengthened by strategic partnerships between pharmaceutical companies and research centers, which accelerate drug development and market growth.

Leading players in the Global Docetaxel Industry include Alchem International, Alkem Labs, Arch Pharmalabs, Aspen Pharmacare, Cipla, Cisen Pharmaceutical, LGM Pharma, Phyton Biotech, Qilu Pharmaceutical, Teva Active Pharmaceutical Ingredients (TAPI), Teva Pharmaceuticals, Venus Remedies, and Xiromed. Companies operating in the docetaxel market are focusing on expanding their product portfolios by offering new formulations, delivery methods, and combination therapies. Partnerships with research institutions and hospitals are vital to enhancing the clinical applications and adoption of docetaxel. Many players are investing in biosimilars and generics to tap into cost-sensitive markets, ensuring broader access to this essential drug. Additionally, the development of personalized medicine and advanced digital health technologies allows companies to better cater to patient needs, improving treatment outcomes.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Indication

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global cancer prevalence

- 3.2.1.2 Increasing adoption of combination therapies

- 3.2.1.3 Favorable regulatory approvals and guidelines

- 3.2.1.4 Technological advancements in drug formulation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Severe side effects and toxicity concerns

- 3.2.2.2 Patent expirations and generic competition

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of personalized oncology treatment approaches

- 3.2.3.2 Increasing investments in oncology research and development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Reimbursement scenario

- 3.10.1 Impact of reimbursement policies on market growth

- 3.11 Consumer behaviour analysis

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Branded

- 5.3 Generics

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Breast cancer

- 6.3 Non-small cell lung cancer (NSCLC)

- 6.4 Hormone refractory prostate cancer

- 6.5 Gastric adenocarcinoma

- 6.6 Head and neck squamous cell carcinoma (HNSCC)

- 6.7 Other indications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Oncology clinics

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Alchem International

- 9.2 Alkem Labs

- 9.3 Arch Pharmalabs

- 9.4 Aspen Pharmacare

- 9.5 Cipla

- 9.6 Cisen Pharmaceutical

- 9.7 LGM Pharma

- 9.8 Phyton Biotech

- 9.9 Qilu Pharmaceutical

- 9.10 Teva Active Pharmaceutical Ingredients (TAPI)

- 9.11 Teva Pharmaceuticals

- 9.12 Venus Remedies

- 9.13 Xiromed