|

시장보고서

상품코드

1766319

태양광 PV 설치 시스템 시장 : 기회, 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Solar PV Mounting Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

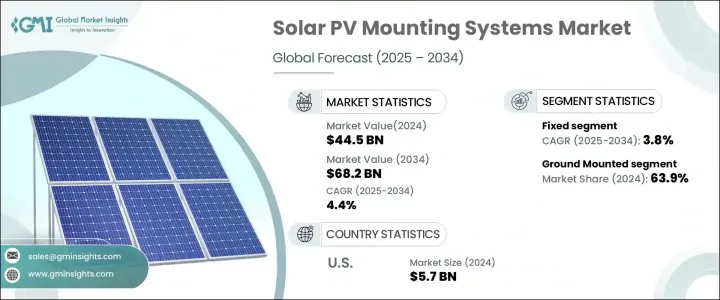

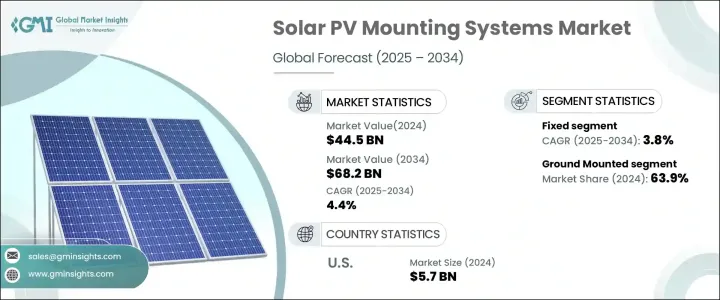

세계의 태양광 PV 설치 시스템 시장 규모는 2024년 445억 달러로 평가되었고, 2034년에는 682억 달러에 달할 것으로 예측되며, CAGR 4.4%로 성장할 전망입니다. 경량 및 사전 조립된 마운팅 구조에 대한 수요가 증가하면서, 특히 제조업체들이 내식성 개선과 모듈식 설계에 집중함에 따라 제품 채택이 크게 증가하고 있습니다. 이러한 혁신은 운송 및 설치를 더욱 효율적으로 만들어 인건비를 절감하고 대규모 태양열 발전 시설에 대한 채택을 증가시킵니다.

사용 가능한 토지의 제한이 증가하고 구현 일정이 단축됨에 따라 공간 효율적이고 적응력이 뛰어난 마운팅 솔루션에 대한 필요성이 높아지고 있습니다. 특히 상업 및 유틸리티 부문에서 탈탄소화 및 에너지 독립에 대한 강력한 모멘텀이 태양광 PV 시스템의 구조적 통합을 계속 촉진하고 있습니다. 지능형 인프라 및 디지털 에너지 관리 시스템에 대한 투자 증가로 시장 개발이 더욱 가속화되고 있습니다. 기후 변화에 따른 전 세계의 자금 지원과 유리한 정책 프레임워크에 힘입어 부유식 태양광 설비의 모멘텀이 강화되면서, 첨단 고도 전문 마운팅 기술에 대한 수요도 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 445억 달러 |

| 예측 금액 | 682억 달러 |

| CAGR | 4.4% |

추적 시스템 부문은 태양열 노출을 극대화하고 출력을 개선하기 위해 이러한 시스템을 채택하는 유틸리티 규모의 프로젝트가 증가함에 따라 2034년까지 168억 달러에 달할 것으로 예상됩니다. 이 시스템은 하루 종일 태양의 궤적을 따라 조정될 수 있기 때문에 고정형 대안에 비해 에너지 생성량이 훨씬 높습니다. 첨단 소프트웨어 기반 제어 시스템과 그리드 규모의 설비 전반에 걸친 통합이 강화되면서 시장 지위가 공고해지고 있습니다.

지상 설치형 솔루션은 확장성과 유지 보수의 용이성으로 인해 2024년에 63.9%의 점유율을 차지했습니다. 최적의 경사 구성과 그늘의 영향을 줄여 에너지 성능을 개선하는 능력으로 태양열 발전소 및 유틸리티 응용 분야에서 선호되는 옵션이 되었습니다. 미개발 토지에 태양열 인프라를 확장하면 부문 확장이 더욱 촉진될 것입니다.

아시아태평양 태양광 PV 설치 시스템 시장은 2025년부터 2034년까지 연평균 5.1%의 성장률을 기록할 것으로 예상되며, 도시화 진행, 재생 가능 에너지 채택에 대한 정부의 유리한 목표, 설치 비용 감소가 지역 수요를 촉진할 것으로 보입니다. 태양광 프로젝트 입찰에 민간 기업의 참여가 증가하고, 설치 부품의 현지 생산으로의 전환이 진행되면, 설비 구축이 효율화되고 시장 침투가 확대될 것입니다.

전 세계 태양광 PV 설치 시스템 시장에서 활동하는 주요 기업으로는 FTC Solar, First Solar, GameChange Solar, Mounting Systems, Jinko Solar, Trina Tracker, Arctech, Soltec, Clenergy, PV Hardware, SunPower Corporation, Valmont Industries, Xiamen Grace Solar New Energy Technology, Unirac, Schletter Group, Versolsolar Hangzhou, Ideematec, K2 Systems, Array Technologies 및 Nextracker 등이 있습니다. 태양광 PV 설치 시스템 업계의 주요 업체들은 시장 도달 범위를 확대하고 경쟁 우위를 강화하기 위해 여러 가지 전략적 이니셔티브를 채택하고 있습니다. 주요 초점은 기술 혁신으로, 부식 저항성이 높고 옥상 및 부유식 태양광 설비 모두에 호환되는 더 가볍고 모듈식 시스템을 개발하는 것입니다. 기업들은 에너지 생성을 최적화하기 위해 실시간 모니터링, 예측 유지보수 및 자동 정렬을 제공하는 디지털 플랫폼에 투자하고 있습니다. 지역 확장 전략으로 파트너십, 합작 투자, 현지 제조 시설을 통해 고성장 시장에 접근하고 있습니다. 또한 기업들은 국가 및 국제 지속 가능성 목표와 일치하도록 저탄소, 재활용 가능한 마운팅 재료를 제공함으로써 환경 친화적 제품을 강조하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

- 산업 생태계

- 규제 상황

- 산업에 미치는 영향요인

- 성장 촉진요인

- 산업의 잠재적 리스크 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율

- 전략적 대시보드

- 전략적 노력

- 경쟁 벤치마킹

- 혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 기술별(2021-2034년)

- 주요 동향

- 마운팅

- 추적 시스템

제6장 시장 규모와 예측 : 제품별(2021-2034년)

- 주요 동향

- 지상 설치형

- 옥상 설치형

제7장 시장 규모와 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 주거용

- 상업용 및 산업용

- 유틸리티

제8장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 오스트리아

- 노르웨이

- 덴마크

- 핀란드

- 프랑스

- 독일

- 이탈리아

- 스위스

- 스페인

- 스웨덴

- 영국

- 네덜란드

- 폴란드

- 벨기에

- 아일랜드

- 발트 국가

- 포르투갈

- 아시아태평양

- 중국

- 호주

- 인도

- 일본

- 한국

- 태국

- 필리핀

- 베트남

- 말레이시아

- 싱가포르

- 중동

- 이스라엘

- 사우디아라비아

- 아랍에미리트(UAE)

- 요르단

- 오만

- 쿠웨이트

- 튀르키예

- 아프리카

- 남아프리카

- 이집트

- 알제리

- 나이지리아

- 모로코

- 라틴아메리카

- 브라질

- 칠레

- 아르헨티나

- 페루

제9장 기업 프로파일

- Arctech

- Array Technologies

- Clenergy

- First Solar

- FTC Solar

- GameChange Solar

- Ideematec

- Jinko Solar

- K2 Systems

- Mounting Systems

- Nextracker

- PV Hardware

- Schletter Group

- Soltec

- SunPower Corporation

- Trina Tracker

- Unirac

- Valmont Industries

- Versolsolar Hangzhou

- Xiamen Grace Solar New Energy Technology

The Global Solar PV Mounting Systems Market was valued at USD 44.5 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 68.2 billion by 2034. The growing demand for lightweight and pre-assembled mounting structures is significantly enhancing product adoption, especially as manufacturers focus on improving corrosion resistance and ensuring modular design. These innovations make transportation and installation more efficient, thereby reducing labor costs and increasing adoption across large-scale solar deployments.

Rising limitations in available land and the push for faster implementation timelines are fueling the need for space-efficient, adaptable mounting solutions. Strong momentum around decarbonization and energy independence, especially in commercial and utility sectors, continues to drive structural integration of solar PV systems. Increased investments in intelligent infrastructure and digital energy management systems are further accelerating market development. The momentum behind floating solar installations, supported by climate-driven global funding and favorable policy frameworks, is also contributing to the growing need for advanced and highly specialized mounting technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $44.5 Billion |

| Forecast Value | $68.2 Billion |

| CAGR | 4.4% |

The tracking systems segment is anticipated to reach USD 16.8 billion by 2034 as more utility-scale projects adopt these systems to maximize solar exposure and improve output. Their ability to align with the sun's path throughout the day results in significantly higher energy generation compared to fixed alternatives. Advanced software-driven control systems and growing integration across grid-scale installations are solidifying their market position.

Ground-mounted solutions captured a 63.9% share in 2024 due to their scalability and ease of maintenance. Their ability to deliver improved energy performance through optimal tilt configurations and reduced shading influence has made them a preferred option for solar farms and utility applications. Expanding solar infrastructure across undeveloped land further supports segmental expansion.

Asia Pacific Solar PV Mounting Systems Market is forecasted to register a CAGR of 5.1% between 2025 and 2034, with growing urbanization, favorable government targets for renewable energy adoption, and declining installation costs driving regional demand. Increasing involvement from private firms in solar project tenders, coupled with a shift toward local production of mounting components, will help streamline deployment and promote broader market penetration.

Key companies active in the Global Solar PV Mounting Systems Market include FTC Solar, First Solar, GameChange Solar, Mounting Systems, Jinko Solar, Trina Tracker, Arctech, Soltec, Clenergy, PV Hardware, SunPower Corporation, Valmont Industries, Xiamen Grace Solar New Energy Technology, Unirac, Schletter Group, Versolsolar Hangzhou, Ideematec, K2 Systems, Array Technologies, and Nextracker. Leading players in the solar PV mounting systems industry are adopting several strategic initiatives to expand market reach and strengthen their competitive edge. A primary focus is on technological innovation-developing lighter, more modular systems with higher corrosion resistance and compatibility with both rooftop and floating solar installations. Companies are investing in digital platforms that provide real-time monitoring, predictive maintenance, and automated alignment to optimize energy generation. Regional expansion through partnerships, joint ventures, and local manufacturing facilities is enabling access to high-growth markets. Additionally, players are aligning with national and international sustainability goals by offering low-carbon, recyclable mounting materials.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Fixed

- 5.3 Tracking

Chapter 6 Market Size and Forecast, By Product, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Ground mounted

- 6.3 Rooftop

Chapter 7 Market Size and Forecast, By End Use, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial & industrial

- 7.4 Utility

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Austria

- 8.3.2 Norway

- 8.3.3 Denmark

- 8.3.4 Finland

- 8.3.5 France

- 8.3.6 Germany

- 8.3.7 Italy

- 8.3.8 Switzerland

- 8.3.9 Spain

- 8.3.10 Sweden

- 8.3.11 UK

- 8.3.12 Netherlands

- 8.3.13 Poland

- 8.3.14 Belgium

- 8.3.15 Ireland

- 8.3.16 Baltics

- 8.3.17 Portugal

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Thailand

- 8.4.7 Philippines

- 8.4.8 Vietnam

- 8.4.9 Malaysia

- 8.4.10 Singapore

- 8.5 Middle East

- 8.5.1 Israel

- 8.5.2 Saudi Arabia

- 8.5.3 UAE

- 8.5.4 Jordan

- 8.5.5 Oman

- 8.5.6 Kuwait

- 8.5.7 Turkey

- 8.6 Africa

- 8.6.1 South Africa

- 8.6.2 Egypt

- 8.6.3 Algeria

- 8.6.4 Nigeria

- 8.6.5 Morocco

- 8.7 Latin America

- 8.7.1 Brazil

- 8.7.2 Chile

- 8.7.3 Argentina

- 8.7.4 Peru

Chapter 9 Company Profiles

- 9.1 Arctech

- 9.2 Array Technologies

- 9.3 Clenergy

- 9.4 First Solar

- 9.5 FTC Solar

- 9.6 GameChange Solar

- 9.7 Ideematec

- 9.8 Jinko Solar

- 9.9 K2 Systems

- 9.10 Mounting Systems

- 9.11 Nextracker

- 9.12 PV Hardware

- 9.13 Schletter Group

- 9.14 Soltec

- 9.15 SunPower Corporation

- 9.16 Trina Tracker

- 9.17 Unirac

- 9.18 Valmont Industries

- 9.19 Versolsolar Hangzhou

- 9.20 Xiamen Grace Solar New Energy Technology