|

시장보고서

상품코드

1766328

의료용 콜드체인 보관 장비 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Medical Cold Chain Storage Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

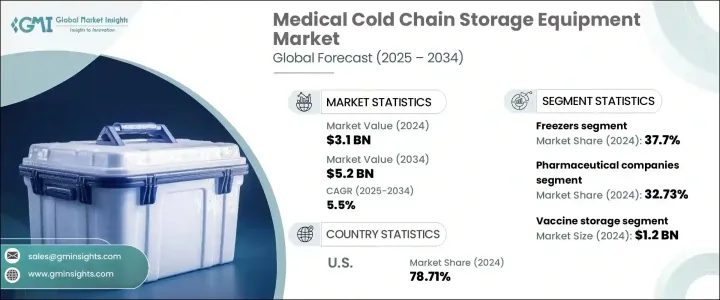

세계의 의료용 콜드체인 보관 장비 시장은 2024년에는 31억 달러로 평가되었고 CAGR 5.5%로 성장하여 2034년에는 52억 달러에 이를 것으로 추정됩니다.

이 시장은 기밀성이 높은 의약품의 온도 관리 물류에 대한 의존도가 높아지고 있기 때문에 세계의 헬스케어 공급 체인의 복잡화에 따라 신뢰성이 높고 안전하며 효율적인 콜드체인 솔루션에 대한 수요는 증가 추세에 있습니다. 생물제제, 세포치료제, 백신 등의 의약품은 운송과 보관을 통해 효능과 안전성을 유지하기 위해 일관된 저온 환경을 필요로 합니다.

공급망의 과제가 증가하는 가운데, 업계 관계자는 콜드체인 전체의 품질 보증을 확보하기 위해 온도 인디케이터, 인텔리전트 센서, 리얼타임 데이터 로거 등의 선진 기술을 통합하고 있습니다. 또한, 스마트 냉각 시스템, 자동화 툴, 친환경 냉매의 채용이 표준화되면서 기업은 환경 규제를 준수하면서도 지속 원격 모니터링, IoT 기능 및 예측 분석 기술의 통합을 통해 콜드체인 관리에서 운영의 투명성과 성능을 크게 향상 시켰습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 31억 달러 |

| 예측 금액 | 52억 달러 |

| CAGR | 5.5% |

제품 유형별로는 냉동고가 2024년 세계 시장을 선도해 총 매출의 37.7%를 차지하였고, 2025년부터 2034년까지의 CAGR은 6%로 예측됩니다. 중요한 헬스케어 제품을 특정 저온에서 보관할 필요성이 냉동고의 사용 확대를 뒷받침하고 있습니다. 또한 정확한 온도 제어와 알람 기능을 갖춘 냉동고는 의료 물류에 필수적이므로 업계 규제를 준수할 필요성도 수요를 지지하고 있습니다. 냉동고는 병원, 의약품 제조 장치, 진단 실험실 등 다양한 환경에서 사용하기에 적합합니다.

최종 사용자 분석에 따르면 2024년 시장 점유율은 제약 기업이 32.73%를 차지하였고 2034년까지 연평균 복합 성장률(CAGR) 5.8%로 확대될 것으로 예측됩니다. 제약 기업은 엄격한 온도 요건하에서 생물 제제, 임상 연구 재료를 보관하고 운송합니다. 콜드체인을 유지하는 것은 제품의 생존성과 보존 기간에 매우 중요합니다.

용도별로는 백신 보관이 2024년 세계 시장을 주도하여 12억 달러의 수익을 달성하였습니다. 2025년부터 2034년까지의 CAGR은 5.8%를 보일 것으로 예측됩니다. 백신에 대한 접근성과 의식을 향상시키기 위한 세계적인 대처가 백신 보관 장비 수요를 높이고 있습니다.실시간 모니터링 기술은 고성능 냉동 장치와 함께 운송 중 및 보관 중인 백신의 일관된 온도 관리를 보증합니다.

지역별로는 미국이 2024년 세계 시장을 선도해 북미의 총 점유율의 78.71%를 차지했으며, 매출액은 8억 달러에 이르렀습니다. 또한, 주요 헬스케어 물류기업이 존재하여 의약품 제조 시설이 집중하고 있는 점도 이 지역의 우위성을 높이고 있습니다.

세계 의료용 콜드체인 보관 장비 시장에서 사업을 전개하는 주요 기업은 Binder, Azenta, Cardinal Health, Darwin Chambers, Carebios Biological Technology, Elanpro, Haier Biomedical, Farrar, Hoshizaki America, Memmert, Philipp Kirsch, Kendall Cold Chain Industries, Thalheimer Kuhlung 등이 있습니다. 이러한 회사는 진화하는 시장 수요에 부응하고 경쟁력을 유지하기 위해 제품 혁신과 디지털 솔루션에 계속 투자하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 생물제제와 백신 수요 증가

- 엄격한 규제 준수

- 기술적 진보

- 업계의 잠재적 위험 및 과제

- 높은 초기 자본 투자액

- 신흥 시장의 인프라 갭

- 기회

- 성장 촉진요인

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 기기 유형별

- 규제 프레임워크

- 표준 및 컴플라이언스 요건

- 지역 규제 프레임워크

- 인증 기준

- 무역 통계(84186990)

- 주요 수입국

- 주요 수출국

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 기기 유형별(2021-2034년)

- 냉장고

- 실험실 냉장고

- 혈액은행 냉장고

- 약국 냉장고

- 크로마토그래피용 냉장고

- 냉동고

- 초저온 냉동고

- 플라즈마 냉동기

- 쇼크 프리저

- 극저온 저장 시스템

- 액체 질소 저장 시스템

- 기상 저장 시스템

- 냉장실

- 기타

제6장 시장 추계 및 예측 : 온도 범위별(2021-2034년)

- 2°C-8°C

- -20°C--40°C

- -40°C--80°C

- -80°C 이하

제7장 시장 추계 및 예측 : 용량별(2021-2034년)

- 소형(최대 300리터)

- 중형(300-700리터)

- 대형(700리터 이상)

제8장 시장 추계 및 예측 : 기술별(2021-2034년)

- 컴프레서 기반 시스템

- 흡수 기반 시스템

- 열전도 기반 시스템

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 백신 보관

- 혈액 및 혈액제제 보관

- 생물학적 샘플 보관

- 의약품 보관

- 기타

제10장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원 및 진료소

- 제약회사

- 연구실

- 혈액은행

- 약국

- 기타

제11장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제12장 기업 프로파일

- Azenta Inc.

- Binder

- Cardinal Health

- Carebios Biological Technology

- Darwin Chambers

- Elanpro

- Farrar

- Haier Biomedical

- Hoshizaki America

- Kendall Cold Chain System

- Memmert

- Philipp Kirsch

- Roemer Industries

- Summit Appliances

- Thalheimer Kuhlung

The Global Medical Cold Chain Storage Equipment Market was valued at USD 3.1 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 5.2 billion by 2034. The market is witnessing significant momentum due to the growing reliance on temperature-controlled logistics for sensitive pharmaceutical products. As global healthcare supply chains become more complex, the demand for reliable, secure, and efficient cold chain solutions continues to rise. Pharmaceuticals such as biologics, cell therapies, and vaccines require consistent low-temperature environments to maintain efficacy and safety throughout transportation and storage. Regulatory agencies worldwide are also enforcing stricter temperature-control guidelines, which drives the adoption of high-performance refrigeration systems.

With increasing supply chain challenges, industry participants are integrating advanced technologies, including temperature indicators, intelligent sensors, and real-time data loggers, to ensure quality assurance across the entire cold chain. Furthermore, the adoption of smart cooling systems, automation tools, and eco-conscious refrigerants is becoming a standard, enabling companies to align with global sustainability mandates while remaining compliant with environmental regulations. The integration of remote monitoring, IoT capabilities, and predictive analytics has greatly enhanced operational transparency and performance in cold chain management. The ongoing investment in digital infrastructure, combined with international immunization initiatives and expanded access to life-saving treatments, is further accelerating the need for medical cold storage systems across various healthcare segments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.1 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 5.5% |

In terms of product type, freezers led the global market in 2024, accounting for 37.7% of total revenue, and are projected to register a CAGR of 6% from 2025 to 2034. Their growing use is driven by the need to store critical healthcare products such as vaccines, drugs, and laboratory samples at specific low temperatures. These systems are widely regarded for their stability and ability to function efficiently under diverse environmental conditions. The demand is also supported by the need for compliance with industry regulations, as freezers equipped with accurate temperature controls and alarm mechanisms are considered essential in medical logistics. Their adaptability in handling varying volumes makes them suitable for use in different environments, including hospitals, pharmaceutical manufacturing units, and diagnostic laboratories. Multipurpose features such as dual compartments and energy-efficient designs also contribute to their widespread preference.

Based on end-user analysis, pharmaceutical companies held a 32.73% share of the market in 2024 and are anticipated to expand at a CAGR of 5.8% through 2034. These companies operate under strict temperature requirements to store and transport vaccines, biologics, and clinical research materials. Adherence to international standards for temperature control is non-negotiable, especially when dealing with sensitive or experimental compounds. Maintaining an uninterrupted cold chain is critical for product viability and shelf life. As production volumes increase, pharmaceutical firms require scalable and compliant storage systems that reduce the risk of spoilage and optimize inventory management. These capabilities not only help in meeting regulatory requirements but also enhance operational efficiency, encouraging further investment in advanced cold storage equipment.

In terms of applications, vaccine storage dominated the global market in 2024, generating USD 1.2 billion in revenue. It is expected to grow at a CAGR of 5.8% from 2025 to 2034. Vaccines must be stored within a narrow temperature range to retain their potency, making dedicated cold chain systems essential. Global efforts to improve vaccination access and awareness continue to boost demand for vaccine storage equipment. Real-time monitoring technologies, coupled with high-performance refrigeration units, ensure consistent temperature control during transit and storage. This application segment remains a cornerstone of the medical cold chain industry due to the critical role vaccines play in public health.

Regionally, the United States led the global market in 2024, accounting for 78.71% of North America's total share, with revenue reaching USD 800 million. The country benefits from a robust healthcare infrastructure and a highly regulated pharmaceutical logistics environment. Investments in innovative storage technologies and end-to-end supply chain visibility tools have made the US a leader in cold chain management. Additionally, the presence of major healthcare logistics providers and a high concentration of pharmaceutical manufacturing facilities contribute to regional dominance. Stringent regulations from US agencies have also pushed companies to deploy advanced cold storage systems that offer energy efficiency and real-time compliance tracking.

Key companies operating in the global medical cold chain storage equipment market include Binder, Azenta, Cardinal Health, Darwin Chambers, Carebios Biological Technology, Elanpro, Haier Biomedical, Farrar, Hoshizaki America, Memmert, Philipp Kirsch, Kendall Cold Chain System, Summit Appliances, Roemer Industries, and Thalheimer Kuhlung. These players continue to invest in product innovation and digital solutions to meet evolving market demands and maintain a competitive edge.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collections methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 By region

- 2.2.2 By equipment type

- 2.2.3 By temperature range

- 2.2.4 By capacity

- 2.2.5 By technology

- 2.2.6 By application

- 2.2.7 By end use

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for biologics and vaccines

- 3.2.1.2 Stringent regulatory compliance

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Infrastructure gaps in emerging markets

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Equipment type

- 3.7 Regulatory framework

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (84186990)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger & acquisitions

- 4.6.2 Partnership & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021 - 2034 ($Bn) (Thousand Units)

- 5.1 Refrigerators

- 5.1.1 Laboratory refrigerators

- 5.1.2 Blood bank refrigerators

- 5.1.3 Pharmacy refrigerators

- 5.1.4 Chromatography refrigerators

- 5.2 Freezers

- 5.2.1 Ultra-low temperature freezers

- 5.2.2 Plasma freezers

- 5.2.3 Shock freezers

- 5.3 Cryogenic storage systems

- 5.3.1 Liquid nitrogen storage systems

- 5.3.2 Vapor phase storage systems

- 5.4 Cold rooms

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Temperature Range, 2021 - 2034 ($Bn) (Thousand Units)

- 6.1 2°C to 8°C

- 6.2 -20°C to -40°C

- 6.3 -40°C to -80°C

- 6.4 Below -80°C

Chapter 7 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Bn) (Thousand Units)

- 7.1 Small (up to 300 liters)

- 7.2 Medium (300-700 liters)

- 7.3 Large (above 700 liters)

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn) (Thousand Units)

- 8.1 Compressor-based systems

- 8.2 Absorption-based systems

- 8.3 Thermoelectric-based systems

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn) (Thousand Units)

- 9.1 Key trends

- 9.2 Vaccine storage

- 9.3 Blood & blood products storage

- 9.4 Biological sample storage

- 9.5 Drug & pharmaceutical storage

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn) (Thousand Units)

- 10.1 Key trends

- 10.2 Hospitals & clinics

- 10.3 Pharmaceutical companies

- 10.4 Research laboratories

- 10.5 Blood banks

- 10.6 Pharmacies

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Azenta Inc.

- 12.2 Binder

- 12.3 Cardinal Health

- 12.4 Carebios Biological Technology

- 12.5 Darwin Chambers

- 12.6 Elanpro

- 12.7 Farrar

- 12.8 Haier Biomedical

- 12.9 Hoshizaki America

- 12.10 Kendall Cold Chain System

- 12.11 Memmert

- 12.12 Philipp Kirsch

- 12.13 Roemer Industries

- 12.14 Summit Appliances

- 12.15 Thalheimer Kuhlung