|

시장보고서

상품코드

1766333

자동차 수리 및 유지보수 서비스 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Automotive Repair and Maintenance Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

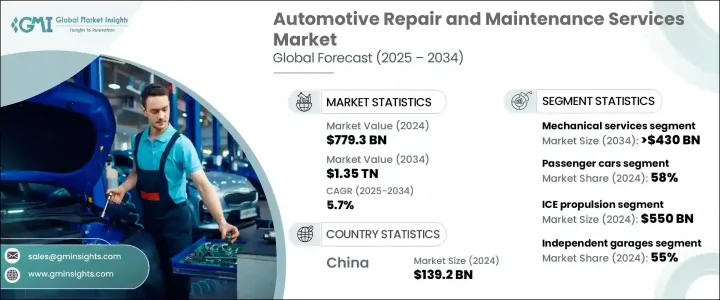

세계의 자동차 수리 및 유지보수 서비스 시장 규모는 2024년에 7,793억 달러에 달하였고, CAGR 5.7%로 성장하여 2034년에는 1조 3,500억 달러에 이를 것으로 예측됩니다.

이 시장은 자동차의 복잡화, 소비자의 기대의 진화, 자동차 기술의 급속한 진보로 역동적인 변화를 이루고 있습니다. 이에 따라 기술적이고 정밀한 서비스에 대한 수요가 급증하고 있습니다. 기계, 전기, 구조, 일반 유지보수 서비스는 커넥티드 자동차 및 전기자동차에 맞는 솔루션에 대한 수요가 증가함에 따라 발전하고 있습니다. 전기자동차의 채용 증가로 부품 및 서비스 생태계가 재구축되면서 서비스 제공업체는 기술 능력을 확대할 필요가 있습니다. 업계 각사가 커넥티드 자동차 환경에 적응하여 전기자동차 특유의 유지보수 요건 증가에 대비하는 가운데 새로운 서비스 모델이 출현하고 있습니다.

기계 서비스 분야는 2024년에 35%의 점유율을 차지하였으며, 2034년에는 4,300억 달러에 달할 것으로 예측됩니다. 브레이크 시스템, 서스펜션 및 드라이브 트레인 구성 요소는 특히 자동차의 주행 거리가 증가하고 소유 주기가 길어짐에 따라 정기적인 정비가 필요합니다. 렌트 및 상업 이용이 증가하고 있기 때문에 타이어나 휠의 유지관리와 같은 마모 서비스도 필수 불가결한 요소입니다. 진화하는 기술로 인해 서비스 주기가 달라지고 전통적인 유지보수 방문의 빈도도 줄어들고 있습니다. 자동차 가운데 특히 EV는 가동 부품이 줄어들면서 필요한 기계적 서비스의 유형과 빈도도 달라집니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7,793억 달러 |

| 예측 금액 | 1조 3,500억 달러 |

| CAGR | 5.7% |

승용차 부문은 2024년에 58%의 점유율을 차지하였으며, 2034년까지 연평균 복합 성장률(CAGR) 6%를 보일 것으로 예측됩니다. 안전 시스템, 인포테인먼트 및 배기 가스 제어의 기술 발전으로 유지보수 및 수리 작업이 더욱 복잡해지고 있습니다. 이러한 모델이 확대됨에 따라 사용이 증가하고 유지보수 요구가 가속화되어 수리 주기가 더 빈번하고 전문화되고 있습니다.

2024년 중국의 자동차 수리 및 유지관리 서비스 시장 점유율은 60%로, 1,392억 달러를 창출하였습니다. 전기자동차 대수가 증가하면서 정비소에서는 고압 장비와 교육에 대한 투자의 필요성이 높아지고 있습니다. 이러한 마이그레이션은 안전과 성능 벤치 마크 준수를 요구하는 규제 기관의 모니터링 증가에 영향을 받는 서비스 표준을 재구성하고 있습니다.

세계 자동차 수리 및 유지보수 서비스 시장의 주요 기업은 AutoNation, LKQ, Driven Brands, TBC, Genuine Parts Company, O'Reilly Automotive, Robert Bosch 등입니다. 시장에서의 지위를 높이기 위해 자동차 수리 및 유지보수 서비스 분야의 주요 기업은 여러 전략적 접근을 활용하고 있습니다. 디지털 플랫폼은 부드러운 실시간 서비스 경험을 제공하는 데 도움이 됩니다. 브랜드는 또한 전기자동차와 하이브리드 자동차 서비스를 지원하기 위해 기술자의 기술에 많은 자원을 투자합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 부품 공급자

- 진단 장비 공급자

- 윤활유 및 유체 공급자

- 공구 및 장비 제공업체

- 기술 및 텔레매틱스 통합 제공업체

- 최종 사용 및 교통당국

- 비용 구조

- 이익률

- 각 단계에서의 부가가치

- 공급망에 영향을 미치는 요인

- 파괴자

- 공급자의 상황

- 영향요인

- 성장 촉진요인

- 차량의 복잡화와 전자제어장치의 통합 증가

- ADAS와 센서 기반 안전 시스템의 발전

- 원격 진단을 가능하게 하는 커넥티드카 기술의 성장

- 전문적인 유지보수가 필요한 전기자동차와 하이브리드 자동차의 보급 증가

- 업계의 잠재적 위험 및 과제

- 첨단 진단 도구 및 장비에 대한 고액의 초기 투자

- EV나 ADAS 기술의 훈련을 받은 숙련 기술자의 부족

- 시장 기회

- AI 기반 예측 유지보수 시스템의 개발

- 스마트 진단에 의한 모바일 플랫폼의 확장

- 원격 트레이닝과 실시간 수리 지원을 위한 AR/VR 통합

- EV에 특화된 서비스 인프라와 배터리 진단 수요 증가

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술

- 온보드 진단 II(OBD-II) 시스템

- ADAS(첨단 운전자 지원 시스템)(ADAS) 캘리브레이션 툴

- 디지털 차량 검사(DVI) 플랫폼

- 타이어 공압 모니터링 시스템(TPMS)

- 신흥 기술

- AI와 IoT를 활용한 예측 유지보수

- 원격 진단 및 무선(OTA) 업데이트

- 기술자 지원을 위한 증강현실(AR)

- EV 배터리의 전압 상태 모니터링 및 열 관리 툴

- 회생 브레이크 기술

- 첨단 제어 시스템과 안전 메커니즘

- 현재의 기술

- 특허 분석

- 총소유비용(TCO) 분석

- 취득 비용

- 인프라 비용

- 운영 비용

- 유지보수 비용

- 수명과 폐기 비용

- 수리 서비스의 평균 가격

- 기계 서비스

- 전기 서비스

- 예방 점검

- 바디 수리 서비스

- 타이어 서비스

- 기타 서비스

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지속 가능성 분석

- 지속 가능한 관행

- 폐기물 절감 전략

- 생산 과정에서의 에너지 효율

- 환경친화적인 노력

- 탄소발자국 고려

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획과 자금 조달

제5장 시장 추계 및 예측 : 서비스별(2021-2034년)

- 주요 동향

- 기계 서비스

- 엔진 수리

- 변속기 수리

- 배기 시스템 수리

- 브레이크 수리

- 서스펜션과 스티어링 수리

- 연료 시스템 서비스

- 클러치&기어박스 서비스

- 전기 서비스

- 배터리 교환

- 얼터네이터와 스타터 모터 수리

- 조명 시스템 수리

- 전자제어유닛 진단

- 배선과 퓨즈 교환

- 예방 점검

- 오일과 필터 교환

- 액체류 보충

- 타이밍 벨트 교환

- 검사 서비스

- 기타

- 바디 수리 서비스

- 충돌 수리

- 찌그러짐 복원

- 도장 서비스

- 유리 교환

- 프레임 배치

- 타이어 서비스

- 타이어 교환

- 타이어 수리

- 휠 얼라인먼트

- 휠 밸런스 조정

- 기타 서비스

제6장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 기계 서비스

- 전기 서비스

- 예방 점검

- 바디 수리 서비스

- 타이어 서비스

- 기타 서비스

- 세단

- 기계 서비스

- 전기 서비스

- 예방 점검

- 바디 수리 서비스

- 타이어 서비스

- 기타 서비스

- SUV

- 기계 서비스

- 전기 서비스

- 예방 점검

- 바디 수리 서비스

- 타이어 서비스

- 기타 서비스

- MPV

- 기계 서비스

- 전기 서비스

- 예방 점검

- 바디 수리 서비스

- 타이어 서비스

- 기타 서비스

- 해치백

- 상용차

- 소형 상용차

- 기계 서비스

- 전기 서비스

- 예방 점검

- 바디 수리 서비스

- 타이어 서비스

- 기타 서비스

- 중형 상용차

- 기계 서비스

- 전기 서비스

- 예방 점검

- 바디 수리 서비스

- 타이어 서비스

- 기타 서비스

- 대형 상용차

- 기계 서비스

- 전기 서비스

- 예방 점검

- 바디 수리 서비스

- 타이어 서비스

- 기타 서비스

- 소형 상용차

- 이륜차

- 기계 서비스

- 전기 서비스

- 예방 점검

- 바디 수리 서비스

- 타이어 서비스

- 기타 서비스

제7장 시장 추계 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- ICE

- 전기

- 하이브리드

제8장 시장 추계 및 예측 : 서비스 제공업체별(2021-2034년)

- 주요 동향

- 정식 판매점

- 개인 정비소

- OEM 정비소

- 기타

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 우크라이나

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 칠레

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- ADNOC

- AutoNation

- Belron International

- Bosch Car Service

- Car Parts.com

- EUROPART Holding

- Genuine Parts Company

- Hance's European

- Inter cars

- LKQ Corporations

- M&M Auto Repair

- Mekonomen Group

- Mobivia Groupe

- My TVS

- Nippon Express

- O'Reilly Automotive

- Sun Auto Service

- TBC

- USA Automotive

- Wrench

The Global Automotive Repair and Maintenance Services Market was valued at USD 779.3 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 1.35 trillion by 2034. This market is undergoing a dynamic transformation driven by the increasing complexity of vehicles, evolving consumer expectations, and rapid advancements in automotive technologies. As vehicles become more integrated with telematics, semi-autonomous features, and solid-state electronic systems, the demand for technical and precision-based services is surging. Workshops are investing in high-end diagnostic tools and updating service infrastructure to meet evolving repair needs. Mechanical, electrical, structural, and general maintenance services are evolving with a growing demand for solutions tailored to connected and electric vehicles. The rising adoption of electric vehicles is gradually reshaping the parts and service ecosystem, pushing service providers to expand technical capabilities. New service models are emerging as industry players adapt to a connected automotive environment and prepare for the rise of EV-specific maintenance requirements.

The mechanical services segment accounted for a 35% share in 2024 and is forecasted to reach USD 430 billion by 2034. Despite shifts in vehicle architecture, demand for essential mechanical services remains stable. Braking systems, suspensions, and drivetrain components continue to require routine servicing, especially as vehicles are driven longer and ownership cycles extend. With fleets and commercial use on the rise, wear-intensive services like tire and wheel maintenance also remain vital. However, evolving technologies such as synthetic lubricants and hybrid drivetrains are changing service intervals and reducing the frequency of traditional maintenance visits. As vehicles incorporate fewer moving parts, particularly in EVs, the type and frequency of mechanical services required are transitioning.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $779.3 Billion |

| Forecast Value | $1.35 Trillion |

| CAGR | 5.7% |

The passenger car segment represented a 58% share in 2024 and is expected to grow at a CAGR of 6% throughout 2034. Technological advancements in safety systems, infotainment, and emissions controls are making maintenance and repair tasks more intricate. This is boosting demand for advanced diagnostic and repair solutions capable of handling new-generation systems. As ride-sharing and shared mobility models expand, increased utilization is accelerating maintenance needs, resulting in more frequent and specialized repair cycles. Service centers are adapting their capabilities to accommodate this shift, especially in metropolitan areas where shared fleets are heavily used.

China Automotive Repair and Maintenance Services Market held a 60% share in 2024, generating USD 139.2 billion. The market is expanding rapidly in the region, mainly due to a strong push toward vehicle electrification and stricter environmental regulations. As the number of electric vehicles on the road increases, workshops are being compelled to invest in tools and training for high-voltage systems, battery diagnostics, and regenerative braking services. This transition is reshaping service standards, influenced by growing oversight from regulatory bodies that demand compliance with safety and performance benchmarks. Certifications from regulatory agencies reinforce consistent quality in aftermarket services and parts across the region, adding to the professionalism and standardization of the repair ecosystem.

Leading market players in the Global Automotive Repair and Maintenance Services Market include AutoNation, LKQ, Driven Brands, TBC, Genuine Parts Company, O'Reilly Automotive, and Robert Bosch. To enhance their market position, key companies in the automotive repair and maintenance services sector are leveraging multiple strategic approaches. Many are expanding their global service networks and acquiring regional operators to gain local market traction. Investment in digital platforms, such as connected diagnostics and customer-facing applications, is helping them offer seamless, real-time service experiences. Brands are also allocating significant resources to upskilling technicians to support electric and hybrid vehicle servicing. Additionally, partnerships with OEMs and fleet operators enable providers to ensure consistent volume and technical collaboration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Parts suppliers

- 3.1.1.2 Diagnostic equipment suppliers

- 3.1.1.3 Lubricants & fluids suppliers

- 3.1.1.4 Tool and equipment providers

- 3.1.1.5 Technology & Telematics Integration providers

- 3.1.1.6 End use and transit authorities

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing vehicle complexity and integration of electronic control units

- 3.2.1.2 Advancements in ADAS and sensor-based safety systems

- 3.2.1.3 Growth in connected car technologies enabling remote diagnostics

- 3.2.1.4 Rising adoption of electric and hybrid vehicles requiring specialized maintenance

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment in advanced diagnostic tools and equipment

- 3.2.2.2 Shortage of skilled technicians trained in EVs and ADAS technologies

- 3.2.3 Market Opportunities

- 3.2.3.1 Development of AI-based predictive maintenance systems

- 3.2.3.2 Expansion of mobile platforms with smart diagnostics

- 3.2.3.3 Integration of AR/VR for remote training and real-time repair assistance

- 3.2.3.4 Growing demand for EV-focused service infrastructure and battery diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology & innovation landscape

- 3.6.1 Current technologies

- 3.6.1.1 On-board Diagnostics II (OBD-II) Systems

- 3.6.1.2 Advanced Driver Assistance Systems (ADAS) Calibration Tools

- 3.6.1.3 Digital Vehicle Inspection (DVI) Platforms

- 3.6.1.4 Tire Pressure Monitoring Systems (TPMS)

- 3.6.2 Emerging technologies

- 3.6.2.1 Predictive maintenance using AI and IoT

- 3.6.2.2 Remote Diagnostics & Over-the-Air (OTA) updates

- 3.6.2.3 Augmented Reality (AR) for technician assistance

- 3.6.2.4 EV battery health monitoring and thermal management tools

- 3.6.3 Regenerative braking technologies

- 3.6.4 Advanced control systems and safety mechanisms

- 3.6.1 Current technologies

- 3.7 Patent analysis

- 3.8 Total Cost of Ownership (TCO) analysis

- 3.8.1 Acquisition cost

- 3.8.2 Infrastructure costs

- 3.8.3 Operational costs

- 3.8.4 Maintenance costs

- 3.8.5 End-of-life and disposal costs

- 3.9 Average price of repair services

- 3.9.1 Mechanical services

- 3.9.2 Electrical services

- 3.9.3 Preventive maintenance

- 3.9.4 Body repair services

- 3.9.5 Tire services

- 3.9.6 Other services

- 3.10 Regulatory landscape

- 3.10.1 North America

- 3.10.2 Europe

- 3.10.3 Asia Pacific

- 3.10.4 Latin America

- 3.10.5 Middle East & Africa

- 3.11 Sustainability analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Mechanical services

- 5.2.1 Engine repair

- 5.2.2 Transmission repair

- 5.2.3 Exhaust system repair

- 5.2.4 Brake repair

- 5.2.5 Suspension & steering repair

- 5.2.6 Fuel system services

- 5.2.7 Clutch & gearbox services

- 5.3 Electrical services

- 5.3.1 Battery replacement

- 5.3.2 Alternator & starter motor repair

- 5.3.3 Lighting system repair

- 5.3.4 Electronic control unit diagnostics

- 5.3.5 Wiring & fuse replacement

- 5.4 Preventive maintenance

- 5.4.1 Oil & filter change

- 5.4.2 Fluid top-ups

- 5.4.3 Timing belt replacement

- 5.4.4 Inspection services

- 5.4.5 Others

- 5.5 Body repair services

- 5.5.1 Collision repair

- 5.5.2 Dent removal

- 5.5.3 Paint services

- 5.5.4 Glass replacement

- 5.5.5 Frame alignment

- 5.6 Tire services

- 5.6.1 Tire replacement

- 5.6.2 Tire repair

- 5.6.3 Wheel alignment

- 5.6.4 Wheel balancing

- 5.7 Other services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchbacks

- 6.2.1.1 Mechanical services

- 6.2.1.2 Electrical services

- 6.2.1.3 Preventive maintenance

- 6.2.1.4 Body repair services

- 6.2.1.5 Tire services

- 6.2.1.6 Other services

- 6.2.2 Sedans

- 6.2.2.1 Mechanical services

- 6.2.2.2 Electrical services

- 6.2.2.3 Preventive maintenance

- 6.2.2.4 Body repair services

- 6.2.2.5 Tire services

- 6.2.2.6 Other services

- 6.2.3 SUVs

- 6.2.3.1 Mechanical services

- 6.2.3.2 Electrical services

- 6.2.3.3 Preventive maintenance

- 6.2.3.4 Body repair services

- 6.2.3.5 Tire services

- 6.2.3.6 Other services

- 6.2.4 MPVs

- 6.2.4.1 Mechanical services

- 6.2.4.2 Electrical services

- 6.2.4.3 Preventive maintenance

- 6.2.4.4 Body repair services

- 6.2.4.5 Tire services

- 6.2.4.6 Other services

- 6.2.1 Hatchbacks

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.1.1 Mechanical services

- 6.3.1.2 Electrical services

- 6.3.1.3 Preventive maintenance

- 6.3.1.4 Body repair services

- 6.3.1.5 Tire services

- 6.3.1.6 Other services

- 6.3.2 Medium commercial vehicles

- 6.3.2.1 Mechanical services

- 6.3.2.2 Electrical services

- 6.3.2.3 Preventive maintenance

- 6.3.2.4 Body repair services

- 6.3.2.5 Tire services

- 6.3.2.6 Other services

- 6.3.3 Heavy commercial vehicles

- 6.3.3.1 Mechanical services

- 6.3.3.2 Electrical services

- 6.3.3.3 Preventive maintenance

- 6.3.3.4 Body repair services

- 6.3.3.5 Tire services

- 6.3.3.6 Other services

- 6.3.1 Light commercial vehicles

- 6.4 Two-wheelers

- 6.4.1 Mechanical services

- 6.4.2 Electrical services

- 6.4.3 Preventive maintenance

- 6.4.4 Body repair services

- 6.4.5 Tire services

- 6.4.6 Other services

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Service Provider, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Authorized dealerships

- 8.3 Independent garages

- 8.4 OEM-affiliated workshops

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 North America

- 9.1.1 U.S.

- 9.1.2 Canada

- 9.2 Europe

- 9.2.1 UK

- 9.2.2 Germany

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

- 9.2.6 Ukraine

- 9.2.7 Russia

- 9.3 Asia Pacific

- 9.3.1 China

- 9.3.2 India

- 9.3.3 Japan

- 9.3.4 Australia

- 9.3.5 South Korea

- 9.3.6 Southeast Asia

- 9.4 Latin America

- 9.4.1 Brazil

- 9.4.2 Mexico

- 9.4.3 Argentina

- 9.4.4 Chile

- 9.5 MEA

- 9.5.1 South Africa

- 9.5.2 Saudi Arabia

- 9.5.3 UAE

Chapter 10 Company Profiles

- 10.1 ADNOC

- 10.2 AutoNation

- 10.3 Belron International

- 10.4 Bosch Car Service

- 10.5 Car Parts.com

- 10.6 EUROPART Holding

- 10.7 Genuine Parts Company

- 10.8 Hance’s European

- 10.9 Inter cars

- 10.10 LKQ Corporations

- 10.11 M& M Auto Repair

- 10.12 Mekonomen Group

- 10.13 Mobivia Groupe

- 10.14 My TVS

- 10.15 Nippon Express

- 10.16 O'Reilly Automotive

- 10.17 Sun Auto Service

- 10.18 TBC

- 10.19 USA Automotive

- 10.20 Wrench