|

시장보고서

상품코드

1766339

대장암 진단 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Colorectal Cancer Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

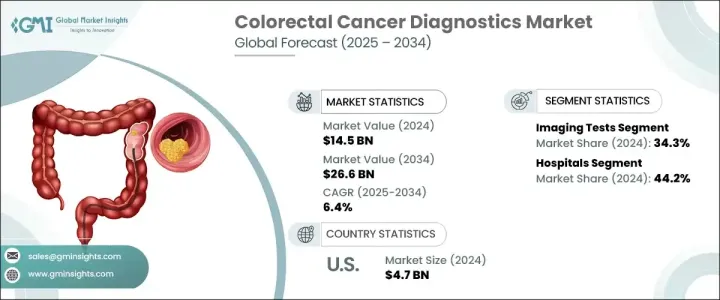

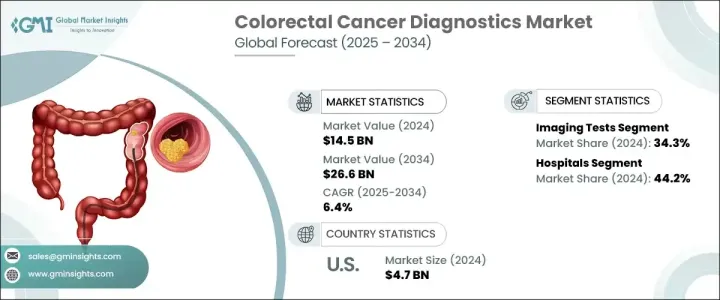

세계의 대장암 진단 시장 규모는 2024년에 145억 달러를 달성하였고 CAGR 6.4%로 성장하여 2034년에는 266억 달러에 이를 것으로 추정됩니다.

시장 성장의 원동력은 대장암의 이환율 증가, 조기 스크리닝을 위한 공중 보건 이니셔티브의 개선, 진단 모달리티에 대한 지속적인 기술 진보를 들 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 145억 달러 |

| 예측 금액 | 266억 달러 |

| CAGR | 6.4% |

정기적인 CRC 검진의 권장 연령을 45세로 낮추는 등 계발 캠페인이나 검진 가이드라인의 개선이 진행되면서 조기 진단률 향상에 기여하고 있습니다. 앉아서 생활하는 라이프스타일이나 식습관과 같은 생활 습관의 요인이 더해져 세계적으로 대장암에 대한 부담이 증가하고 있어 효과적이고 이용하기 쉬운 진단법의 필요성이 부각되고 있습니다. 세계 정부 및 의료기관이 대장암 검진에 대한 접근성을 개선하기 위한 대규모 이니셔티브를 시작하는 한편 비공개회사는 차세대 진단 툴을 시장에 투입하기 위해 연구 개발에 많은 투자를 하고 있습니다.

대장암 진단 시장은 주로 검사 유형별로 구분되며, 이미지 검사 부문이 2024년에 34.3%의 점유율을 차지하였습니다. AI를 활용한 영상 진단의 채용에 의해 검출 정밀도가 향상하여 전암 병변의 조기 발견에 도움이 되고 있습니다. 또한, 영상 검사는 비침습성 또는 저침습성이므로 환자의 수용도와 검진율이 향상되고 있습니다.

최종 사용자별로는 병원 부문이 2024년에 44.2%의 점유율을 차지하면서 대장암 진단의 주요 최종 사용자로서의 지위를 굳히고 있습니다. 병원 부문은 외과 종양학 유닛 등을 포함한 종합적인 진단 인프라에 의해 지원되고 있습니다.

북미 대장암 진단 시장은 2024년에 35.2%의 점유율을 차지했으며 이는 마커 검사 등의 고도 진단 기술의 높은 채용율에 기인합니다.

Abbott Laboratories, Exact Sciences Corporation, Siemens Healthineers AG, Guardant Health Inc., F-Hoffmann-La Roche Ltd., GE HealthCare Technologies, Inc.와 같은 주요 시장 기업은 액체 생검, AI 주도 영상 진단, 분자 진단 혁신을 통해 진단 포트폴리오 확대에 많은 투자를 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 대장암의 발생률과 유병률 증가

- 암 검진에 관한 정부의 대처와 정책

- 암 진단 분야 기술의 진보

- 조기 진단에 관한 의식의 고조

- 업계의 잠재적 위험 및 과제

- 진단 검사 및 처치의 높은 비용

- 진단 검사에 대한 보험 환급 정책의 부족

- 시장 기회

- 비침습성 및 AI 기반 진단 기술의 확대와 도입

- 신흥 지역의 급속한 시장 성장

- 성장 촉진요인

- 장래 시장 동향

- 보험 환급 시나리오

- 소비자 행동 분석

- 성장 가능성 분석

- 기술의 상황

- 규제 상황

- 갭 분석

- 특허 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 검사 유형별(2021-2034년)

- 주요 동향

- 혈액검사

- 대변 검사

- 분변잠혈검사(FOBT)

- 바이오마커 패널 검사

- CRC DNA 스크리닝 검사

- 영상 검사

- CT

- 초음파

- MRI

- PET

- 대장 내시경 검사

- 기타 영상 검사

- 생검

- 기타 검사 유형

제6장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 영상진단센터

- 암연구센터

- 기타 용도

제7장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제8장 기업 프로파일

- Abbott Laboratories

- Danaher Corporation

- DiaCarta

- Exact Sciences Corporation

- F-Hoffmann-La Roche

- GE HealthCare Technologies

- Geneoscopy

- Guardant Health

- HU Group Holdings

- New Day Diagnostics

- Olympus Corporation

- Phase Scientific International

- QIAGEN NV

- Siemens Healthineers

- Sysmex Corporation

- Thermo Fisher Scientific

The Global Colorectal Cancer Diagnostics Market was valued at USD 14.5 billion in 2024 and is estimated to grow at a CAGR of 6.4% to reach USD 26.6 billion by 2034.

The market growth is driven by the increasing incidence of colorectal cancer, rising public health initiatives for early screening, and continuous technological advancements in diagnostic modalities. Innovations such as liquid biopsy, AI-assisted imaging, and stool-based DNA tests are reshaping the landscape of colorectal cancer detection, offering less invasive, more accurate, and patient-friendly diagnostic options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.5 Billion |

| Forecast Value | $26.6 Billion |

| CAGR | 6.4% |

Growing awareness campaigns and updated screening guidelines, such as lowering the recommended age for routine CRC screening to 45, contribute to early diagnosis rates. Furthermore, an aging global population, combined with lifestyle factors like sedentary behavior and dietary habits, has heightened the global burden of colorectal cancer, underscoring the urgent need for effective and accessible diagnostics. Governments and healthcare organizations worldwide are launching large-scale initiatives to improve access to colorectal cancer screening, while private companies are investing heavily in R&D to bring next-generation diagnostic tools to the market. Artificial intelligence, next-generation sequencing (NGS), and microfluidic technologies are poised to enhance diagnostic precision and patient outcomes significantly.

The colorectal cancer diagnostics market is primarily segmented by test type, with the imaging tests segment holding 34.3% share in 2024. Imaging modalities such as CT colonography, MRI, and PET scans remain crucial for early detection, staging, and treatment planning. Adopting AI-enhanced imaging has improved detection accuracy, helping to identify precancerous lesions at earlier stages. Moreover, imaging tests' non-invasive or minimally invasive nature continues to drive patient acceptance and screening rates.

In terms of end-use, the hospitals segment held 44.2% share in 2024, solidifying its position as the leading end-user for colorectal cancer diagnostics. Hospitals are the primary centers for colorectal cancer detection, diagnosis, staging, and treatment planning, supported by a comprehensive diagnostic infrastructure that includes advanced imaging systems, molecular pathology labs, endoscopic equipment, and surgical oncology units. Their multidisciplinary approach-bringing together oncologists, radiologists, pathologists, gastroenterologists, and surgeons-enables the seamless coordination of care for colorectal cancer patients, from early detection through post-treatment monitoring.

North America Colorectal Cancer Diagnostics Market held a 35.2% share in 2024. The region's dominance stems from a robust healthcare infrastructure, widespread implementation of screening programs, and high adoption rates of advanced diagnostic technologies, such as AI-enabled colonoscopy, liquid biopsies, and molecular biomarker testing. In the United States, initiatives like the Colorectal Cancer Control Program (CRCCP) by the CDC have been instrumental in increasing early screening rates, particularly among underserved populations.

Key market players such as Abbott Laboratories, Exact Sciences Corporation, Siemens Healthineers AG, Guardant Health Inc., F-Hoffmann-La Roche Ltd., and GE HealthCare Technologies, Inc. are heavily investing in expanding their diagnostic portfolios through innovations in liquid biopsy, AI-driven imaging, and molecular diagnostics. Strategic partnerships, mergers and acquisitions, and regulatory approvals for new products remain crucial strategies for these players to strengthen their global presence and drive future market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Test type

- 2.2.2 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence and prevalence of colorectal cancer

- 3.2.1.2 Government initiatives and policies associated with cancer screening tests

- 3.2.1.3 Technological advancements in field of cancer diagnostics

- 3.2.1.4 Growing awareness regarding early diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of diagnostic tests and procedures

- 3.2.2.2 Lack of reimbursement policies for diagnostic tests

- 3.2.3 Market Opportunities

- 3.2.3.1 Expansion and Adoption of Non-Invasive and AI-Driven Diagnostic Technologies

- 3.2.3.2 Rapid Market Growth in Emerging Regions

- 3.2.1 Growth drivers

- 3.3 Future market trends

- 3.4 Reimbursement scenario

- 3.5 Consumer behaviour analysis

- 3.6 Growth potential analysis

- 3.7 Technology landscape

- 3.8 Regulatory landscape

- 3.9 Gap analysis

- 3.10 Patent analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Blood tests

- 5.3 Stool tests

- 5.3.1 Fecal occult blood test (FOBT)

- 5.3.2 Fecal biomarker test

- 5.3.3 CRC DNA screening test

- 5.4 Imaging tests

- 5.4.1 CT

- 5.4.2 Ultrasound

- 5.4.3 MRI

- 5.4.4 PET

- 5.4.5 Colonoscopy

- 5.4.6 Other imaging tests

- 5.5 Biopsy

- 5.6 Other test types

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Diagnostic imaging centers

- 6.4 Cancer research centers

- 6.5 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Abbott Laboratories

- 8.2 Danaher Corporation

- 8.3 DiaCarta

- 8.4 Exact Sciences Corporation

- 8.5 F-Hoffmann-La Roche

- 8.6 GE HealthCare Technologies

- 8.7 Geneoscopy

- 8.8 Guardant Health

- 8.9 H.U. Group Holdings

- 8.10 New Day Diagnostics

- 8.11 Olympus Corporation

- 8.12 Phase Scientific International

- 8.13 QIAGEN N.V.

- 8.14 Siemens Healthineers

- 8.15 Sysmex Corporation

- 8.16 Thermo Fisher Scientific