|

시장보고서

상품코드

1766344

산업용 유압 장비 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Industrial Hydraulic Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

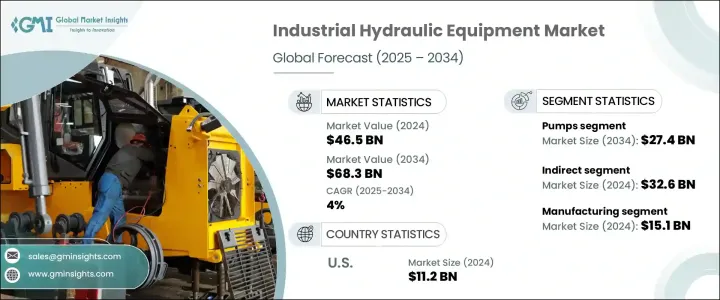

세계의 산업용 유압 장비 시장 규모는 2024년에는 465억 달러에 달하였고, CAGR 4%로 성장하여 2034년에는 683억 달러에 이를 것으로 예측되고 있습니다.

산업 시설 전체에서 인더스트리 4.0의 채용이 확대됨으로써 유압 시스템의 통합 방법과 이용 방법에 현저한 변화가 발생하고 있습니다. 유량 등의 중요한 파라미터를 실시간으로 추적할 수 있게 되어 예측 유지보수 전략이 대폭 개선되고 다운타임이 최소한으로 억제되어 전체적인 에너지 효율이 향상합니다.

신흥 경제 국가에서는 급속한 도시 개발로 대형 건설 기계와 토목 기계 수요가 급증하고 있습니다. 이러한 기계는 정밀도, 신뢰성, 내구성 측면에서 고성능 유압 시스템에 의존하고 있습니다. 또한, 산업계는 에너지 소비의 저감과 환경 안전성을 촉진하는 지속 가능한 대체 수단에 점점 중점을 두고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 465억 달러 |

| 예측 금액 | 683억 달러 |

| CAGR | 4% |

제품 유형별로 보면 시장은 펌프, 실린더, 모터, 밸브, 기타로 구분됩니다. 펌프는 다양한 산업용도에서 필수적입니다. 조립 라인에서 리프팅 시스템과 재료 운송 작업에 이르기까지 펌프는 고정식과 이동식 산업기기 모두에서 유체 동력 시스템의 백본으로 기능하고 있습니다.

유압 펌프의 안정적인 수요는 활발한 산업 환경에서 정기적인 유지보수 및 부품 교체 사이클을 통해 발생합니다. 기업들은 보다 새롭고 효율적인 유압 솔루션에 대한 투자를 계속하고 있습니다. 펌프, 실린더, 모터, 밸브 등을 포함한 광범위한 제품 부문은 2024년 326억 달러에 이르렀으며 예측 기간 동안 CAGR 3.4%를 보일 것으로 예측됩니다.

이 시장의 성장에 기여하는 또 다른 요인은 간접적인 유통 채널의 확대입니다. 정규 벤더, 전문 딜러, 디지털 플랫폼 증가로 다양한 업계와 지역에서 제품에 대한 접근성이 향상되고 있습니다. 이러한 유통업체는 서비스 또한 함께 제공하는 경우가 많습니다. 이러한 올인원 접근 방식은 조달을 간소화하고 고객과의 관계를 강화합니다.

시장을 최종 이용 산업별로 분류하면 제조업, 건설업, 임업 및 농업, 광업, 석유 및 가스, 해양, 항공 및 우주, 기타로 구분됩니다. 유압 장비는 특히 재료 성형, 금속 성형 및 고압 기계 작업에 사용되는 장비에 사용되어 제조 작업에서 중요한 역할을 수행합니다. 산업계가 완전히 자동화된 생산 라인으로 전환함에 따라 유압 시스템은 보다 높은 수준의 응답성, 에너지 관리성, 일관성을 제공해야 합니다.

지역별로는 미국이 북미 산업용 유압 장비 시장을 선도하고 있으며 2024년 시장 규모는 112억 달러를 달성하였고 2034년까지 연평균 복합 성장률(CAGR)은 3.8%로 확대될 것으로 예측되고 있습니다. 업계에서는 신뢰성과 지능적인 자동화 기능을 제공하는 유압 시스템에 대한 강한 수요가 지속되고 있습니다.

전체 시장 상황에서 각사는 기술적으로 선진적이고 에너지 효율이 높으며 커스터마이즈 가능한 유압 장비를 도입함으로써 진화하는 고객의 기대에 부응하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 기회

- 성장 가능성 분석

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥 기술

- 가격 동향

- 지역별

- 제품별

- 규제 프레임워크

- 표준 및 컴플라이언스 요건

- 지역 규제 프레임워크

- 인증 기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카 항공

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 펌프

- 실린더

- 모터

- 밸브

- 기타

제6장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 제조업

- 건설

- 임업과 농업

- 광업

- 석유 및 가스

- 해양

- 항공우주 및 항공

- 기타

제7장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접

- 간접

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

제9장 기업 프로파일

- Bosch Rexroth

- Bucher Hydraulics

- Caterpillar

- Danfoss

- Eaton

- HAWE Hydraulik

- Hitachi Construction Machinery

- HYDAC International

- Kawasaki Heavy Industries

- Komatsu

- KTI Hydraulics

- KYB

- Liebherr-International

- Mitsubishi Heavy Industries

- Parker-Hannifin

The Global Industrial Hydraulic Equipment Market was valued at USD 46.5 billion in 2024 and is estimated to grow at a CAGR of 4% to reach USD 68.3 billion by 2034. The growing adoption of Industry 4.0 across industrial facilities is driving a notable shift in how hydraulic systems are integrated and utilized. By incorporating intelligent components such as sensors, IoT-enabled modules, and AI-powered predictive technologies, manufacturers are enhancing the operational capabilities of hydraulic systems. These advanced solutions enable real-time tracking of essential parameters, including pressure, temperature, and fluid flow, which significantly improves predictive maintenance strategies, minimizes downtime, and boosts overall energy efficiency. As a result, modern electro-hydraulic systems now function seamlessly within fully automated industrial frameworks, establishing hydraulics as an essential pillar in the rise of smart manufacturing.

In emerging economies, rapid urban development is fueling a surge in demand for heavy-duty construction and earth-moving machinery. Hydraulic systems are indispensable in these machines, delivering the power and control required for operations under extreme conditions. As infrastructure projects expand globally, there is a continuous need for equipment such as cranes, excavators, and drilling systems. These machines depend on high-performance hydraulic systems for precision, reliability, and durability. In parallel, industries are increasingly focusing on sustainable alternatives that promote lower energy consumption and environmental safety. This trend is prompting innovation toward eco-efficient hydraulic solutions, which is expected to unlock new growth avenues in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $46.5 Billion |

| Forecast Value | $68.3 Billion |

| CAGR | 4% |

By product type, the market is segmented into pumps, cylinders, motors, valves, and others. Among these, the pump segment held the largest value share, estimated at USD 18.5 billion in 2024, and is projected to reach USD 27.4 billion by 2034. The widespread use of pumps stems from their fundamental role in converting mechanical energy into hydraulic power, which is vital across a variety of industrial applications. From assembly lines to lifting systems and material transport operations, pumps serve as the backbone of fluid power systems in both fixed and mobile industrial equipment. The increasing push for high-precision metering and energy conservation has led to the development of advanced technologies such as variable displacement pumps, which offer improved efficiency and dynamic control.

Consistent demand for hydraulic pumps is also supported by routine maintenance and part replacement cycles in active industrial environments. As older components reach the end of their service lives, businesses continue to invest in newer, more efficient hydraulic solutions that align with modern performance standards. The broader product segment, encompassing pumps, cylinders, motors, valves, and others, reached USD 32.6 billion in 2024 and is anticipated to grow at a CAGR of 3.4% during the forecast period.

Another factor contributing to the growth of this market is the expansion of indirect distribution channels. A growing number of authorized vendors, specialized dealers, and digital platforms are enhancing product accessibility across diverse industries and geographies. These distributors often bundle core hydraulic products with related engineering services such as fluid condition monitoring, filtration packages, and hydraulic fluid management systems. This all-in-one approach simplifies procurement and strengthens customer relationships. Additionally, on-ground technical support and real-time product demonstrations further reinforce confidence among industrial buyers, enabling distributors to maintain a resilient and competitive market presence.

When segmented by end-use industry, the market includes manufacturing, construction, forestry and agriculture, mining, oil and gas, marine, aerospace and aviation, and others. The manufacturing sector accounted for USD 15.1 billion in 2024 and is projected to grow at a CAGR of 4.5% through 2034. Hydraulics play a critical role in manufacturing operations, particularly in equipment used for material forming, metal shaping, and high-pressure mechanical tasks. As industries move toward fully automated production lines, hydraulic systems must deliver higher levels of responsiveness, energy management, and consistency. The push for automation has increased the demand for integrated hydraulic solutions that provide precise control, reduced cycle times, and lower operational costs.

Regionally, the United States led the North America industrial hydraulic equipment market, which was valued at USD 11.2 billion in 2024 and is forecast to expand at a CAGR of 3.8% through 2034. The country's robust industrial base and consistent investment in infrastructure development have made it a key contributor to regional market growth. Industries such as automotive manufacturing, building construction, and material handling continue to generate strong demand for hydraulic systems that offer reliability and intelligent automation features. The growing emphasis on digital control and smart electro-hydraulics is further fueling innovation across U.S.-based hydraulic equipment suppliers, who are increasingly scaling their operations to meet this demand.

Across the market landscape, companies are responding to evolving customer expectations by introducing technologically advanced, energy-efficient, and customizable hydraulic equipment. Integrating intelligent control features, IoT connectivity, and predictive maintenance capabilities has become a central strategy for meeting modern industrial demands. At the same time, stricter global energy and emissions standards are compelling manufacturers to adopt greener design principles. To stay competitive, businesses are not only diversifying their product lines but also forming strategic partnerships and acquisitions to expand their presence in specialized segments of mobile and industrial automation. This ongoing shift is reshaping the market, steering it toward more intelligent, efficient, and environmentally responsible hydraulic systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 End use industry

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory framework

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's five forces analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 MEA

- 4.2.1.5 LATAM

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Pumps

- 5.3 Cylinder

- 5.4 Motors

- 5.5 Valves

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By End Use Industry, 2021-2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Manufacturing

- 6.3 Construction

- 6.4 Forestry & agriculture

- 6.5 Mining

- 6.6 Oil & Gas

- 6.7 Marine

- 6.8 Aerospace & aviation

- 6.9 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Direct

- 7.3 Indirect

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034, ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 The U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 9.1 Bosch Rexroth

- 9.2 Bucher Hydraulics

- 9.3 Caterpillar

- 9.4 Danfoss

- 9.5 Eaton

- 9.6 HAWE Hydraulik

- 9.7 Hitachi Construction Machinery

- 9.8 HYDAC International

- 9.9 Kawasaki Heavy Industries

- 9.10 Komatsu

- 9.11 KTI Hydraulics

- 9.12 KYB

- 9.13 Liebherr-International

- 9.14 Mitsubishi Heavy Industries

- 9.15 Parker-Hannifin