|

시장보고서

상품코드

1766362

제빵 원료 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Baking Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

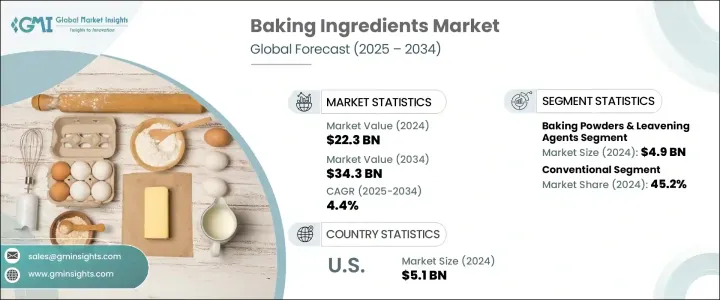

세계의 제빵 원료 시장은 2024년에는 223억 달러로 평가되었고 2034년에는 343억 달러에 이를 것으로 추정되며, CAGR 4.4%로 성장할 전망입니다. 이 시장은 다양한 제빵 제품에 대한 전 세계적 수요 증가에 힘입어 안정적인 성장을 보이고 있습니다. 매출과 판매량 모두 전 세계적으로 소비 패턴의 광범위한 변화를 반영하여 꾸준한 증가세를 보이고 있습니다. 이러한 동향에 기여하는 주요 요인은 식습관의 변화, 도시화의 진행, 즉석 식품에 대한 선호도 증가 등입니다. 특히 신흥 지역에서 포장 및 편의성 베이커리 제품의 인기가 높아짐에 따라 고성능 베이커리 원료에 대한 수요가 가속화되고 있습니다. 동시에 성숙한 경제국들은 계속해서 견조한 수요를 보이며 전체적인 시장 모멘텀을 유지하고 있습니다.

식품 서비스 네트워크와 조직화된 소매 형식의 확장은 제품 접근성을 향상시켜 판매량 증가와 시장 내 베이커리 제품의 다양화를 촉진했습니다. 도시와 준도시 지역에서 현대식 소매점의 지속적인 성장으로 소비자들은 아티장 빵부터 포장된 편의 식품까지 다양한 베이커리 제품에 더 쉽게 접근할 수 있게 되었습니다. 이 같은 접근성 향상은 충동 구매를 촉진했을 뿐만 아니라 새로운 제품 유형과 맛에 대한 실험을 장려했습니다. 또한 소매 체인과 제빵 제조업체 간의 파트너십을 통해 제품 배치, 홍보 캠페인 및 매장 내 제빵 코너가 개선되어 소비자의 관심이 더욱 높아지고 여러 인구 통계 및 소비 기회에 걸쳐 카테고리 성장이 촉진되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 223억 달러 |

| 예측 금액 | 343억 달러 |

| CAGR | 4.4% |

2024년에 제빵 분말 및 발효제 부문은 49억 달러의 매출을 올렸으며, 2025년부터 2034년까지 연평균 4.8%의 성장률을 보일 것으로 예상됩니다. 이러한 성분은 일관된 통기성, 부피 및 식감을 보장하는 역할로 인해 제빵 제품 생산에 필수적인 요소로 남아 있습니다. 산업 및 가정 제빵에 널리 사용되어 시장 지배적 위치를 강화하고 있습니다. 특히 대도시를 중심으로 도시 인구가 증가함에 따라 가공 및 포장된 제빵 제품에 대한 수요가 계속 증가하면서 발효제의 소비도 증가하고 있습니다. 또한, 새로운 클린 라벨 옵션과 개선된 제형이 진화하는 소비자 요구를 충족하면서 신뢰할 수 있는 결과를 제공하기 때문입니다. 비용 효율성이 뛰어나 소규모 제과점, 상업용 주방 및 식품 서비스 사업에서 필수적인 성분으로 자리매김했습니다.

기존 원료 부문은 2024년에 101억 달러로 평가되었으며, 2034년까지 연평균 4.6%의 성장률을 보이며 45.2%의 점유율을 차지할 것으로 예상됩니다. 기존 제품의 신뢰성과 경제성은 대량 생산 요구를 충족하는 데 선호되는 옵션으로 남아 있을 것입니다. 한편, 클린 라벨 및 비 GMO 대체품에 대한 관심이 높아지면서 시장 역학이 재편되고 있으며, 건강에 민감한 선택과 비용 효율적인 솔루션이 균형을 이루고 있습니다. 식품 안전 및 환경에 대한 우려로 인해 유기농 및 추적 가능한 제품을 선택하는 소비자가 증가하면서 천연 재료의 인기가 높아지고 있습니다.

미국의 제빵 원료 2024년 시장 규모는 51억 달러로 평가되었으며, 2025년부터 2034년까지 연평균 4.2%의 성장률을 보일 것으로 예상됩니다. 이러한 꾸준한 성장은 강력한 식품 제조 기반, 가공 제빵 제품에 대한 소비자 수요 증가, 견고한 공급망 인프라에 의해 촉진되고 있습니다. 원료 배합의 혁신은 시장 성장을 유지하는 데 중요한 역할을 하며, 특히 식물성, 글루텐 프리, 저당, 비건 옵션에 대한 수요를 충족하기 위해 맞춤 제작된 제품의 경우 그 중요성이 더욱 커집니다. 소매업의 확장과 전국적으로 포장 베이커리 제품에 대한 선호도가 높아지는 것도 이러한 상승 추세를 뒷받침하고 있습니다.

Puratos Group, Lesaffre, Cargill 등 전 세계 제빵 재료 업계의 주요 기업들은 글로벌 입지를 강화하기 위해 혁신적인 접근 방식을 적극적으로 도입하고 있습니다. 이 기업들은 현대의 식생활 선호도에 맞는 클린 라벨, 기능성, 영양이 풍부한 원료를 도입하기 위해 연구 개발에 우선순위를 두고 있습니다. 식품 서비스 체인 및 소매 베이커리와의 협력을 통해 고객 도달 범위를 확대하고 있습니다. 또한 공급망의 효율성과 현지 수요에 대한 대응력을 확보하기 위해 지역 생산 허브에 투자하고 있습니다. 많은 기업들이 제품 개발 및 유통에 디지털화 전략을 도입하여 민첩성과 고객 참여를 개선하고, 산업 및 소비자 부문 모두에서 시장 리더십을 강화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

- TAM 분석(2025-2034년)

- CXO 관점: 전략적 필수 사항

- 경영상의 의사결정 포인트

- 중요한 성공 요인

- 미래의 전망과 전략적 제안

제3장 산업 고찰

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 산업에 미치는 영향요인

- 성장 촉진요인

- 편의식품에 대한 수요 증가

- 상업용 제과 산업의 성장

- 가처분 소득 증가

- 소비자의 생활 방식 변화

- 산업의 잠재적 리스크 및 과제

- 원료 가격의 변동

- 첨가물에 관한 건강상의 우려

- 시장 기회

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속 가능한 사례

- 폐기물 삭감 전략

- 생산에 있어서의 에너지 효율

- 친환경 활동

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카 항공

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정 및 예측, 원료별(2021-2034년)

- 주요 동향

- 제빵 분말 및 발효제

- 유화제

- 효소

- 유지, 쇼트닝

- 감미료

- 색상 및 향료

- 방부제

- 밀가루

- 전분

- 기타

제6장 시장 추정 및 예측, 성질별(2021-2034년)

- 주요 동향

- 기존

- 유기농

- 클린 라벨

- 비유전자 재조합

제7장 시장 추정 및 예측, 용도별(2021-2034년)

- 주요 동향

- 빵

- 케이크 및 페이스트리

- 쿠키 및 비스킷

- 롤 및 파이

- 피자 크러스트

- 기타

제8장 시장 추정 및 예측, 최종 용도별(2021-2034년)

- 주요 동향

- 상업용 및 산업용 빵집

- 소매 빵집

- 수제 빵집

- 식품서비스 산업

- 가정/소매 소비자

제9장 시장 추정 및 예측, 유통 채널별(2021-2034년)

- 주요 동향

- B2B

- B2C

- 슈퍼마켓 및 대형 슈퍼마켓

- 전문점

- 편의점

- 온라인 소매

- 기타

제10장 시장 추정 및 예측, 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제11장 기업 프로파일

- AAK AB

- Archer Daniels Midland Company

- Associated British Foods plc

- Bakels Group

- BASF SE

- Cargill, Incorporated

- Corbion NV

- Dawn Food Products, Inc.

- DuPont de Nemours, Inc.

- DSM-Firmenich AG

- Flowers Foods, Inc.

- General Mills, Inc.

- Grupo Bimbo, SAB de CV

- Ingredion Incorporated

- Kerry Group plc

- Koninklijke DSM NV

- Lesaffre Group

- Mondelez International, Inc.

- Puratos Group

- Tate & Lyle PLC

The Global Baking Ingredients Market was valued at USD 22.3 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 34.3 billion by 2034. This market demonstrates stable growth, fueled by rising global demand across various categories of baked products. Both revenue and volume have shown consistent increases, reflecting widespread changes in consumption patterns worldwide. Key factors contributing to this trend include shifting dietary habits, growing urbanization, and a rising preference for ready-made food solutions. The growing popularity of packaged and convenience baked items, particularly in emerging regions, is accelerating the need for high-performance baking ingredients. At the same time, mature economies continue to show solid demand, helping to maintain overall market momentum.

Expanding food service networks and organized retail formats have also improved product accessibility, leading to increased sales volumes and broader diversification of baked offerings in the market. As modern retail outlets continue to grow in both urban and semi-urban areas, consumers now have greater exposure to a wide variety of baked goods, ranging from artisanal breads to packaged convenience items. This enhanced availability has not only boosted impulse purchases but has also encouraged experimentation with new product types and flavors. Additionally, partnerships between retail chains and bakery manufacturers have led to better product placement, promotional campaigns, and in-store bakery sections, further elevating consumer interest and driving category growth across multiple demographics and consumption occasions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.3 Billion |

| Forecast Value | $34.3 Billion |

| CAGR | 4.4% |

In 2024, the baking powders and leavening agents segment generated USD 4.9 billion and is forecast to grow at a 4.8% CAGR between 2025 and 2034. These ingredients remain vital in baked goods production due to their role in ensuring consistent aeration, volume, and texture. Their widespread use in both industrial and home baking reinforces their dominant market position. As urban populations grow, particularly in large cities, demand for processed and pre-packaged bakery items continues to rise-driving higher consumption of leavening agents. Additionally, newer clean-label options and improved formulations are catering to evolving consumer demands while delivering reliable results. Their cost-efficiency makes them an essential component across small bakeries, commercial kitchens, and food service operations.

The conventional ingredients segment was valued at USD 10.1 billion in 2024 and is projected to grow at a 4.6% CAGR through 2034, holding a 45.2% share. The reliability and affordability of conventional products ensure they remain a preferred option to meet high-volume production needs. Meanwhile, increased attention toward clean-label and non-GMO alternatives is reshaping market dynamics, offering a balance between health-conscious choices and cost-effective solutions. A growing segment of consumers is turning to organic and traceable options in response to concerns over food safety and environmental impact, signaling rising traction for natural ingredient formats.

United States Baking Ingredients Market was valued at USD 5.1 billion in 2024 and is expected to grow at a 4.2% CAGR from 2025 to 2034. This steady performance is driven by a strong food manufacturing base, rising consumer demand for processed baked items, and a robust supply chain infrastructure. Innovation in ingredient formulations plays a major role in sustaining market growth, especially for products tailored to meet demands for plant-based, gluten-free, sugar-reduced, and vegan options. Retail expansion and increasing preference for packaged baked goods across the country further support this upward trend.

Key players in the Global Baking ingredient industry, including Puratos Group, Lesaffre, Cargill, and others, are actively deploying innovative approaches to strengthen their global footprint. These companies are prioritizing research and development to introduce clean-label, functional, and nutrient-rich ingredients tailored to modern dietary preferences. Collaborations with food service chains and retail bakeries are helping them expand their customer reach. They are also investing in regional production hubs to ensure supply chain efficiency and responsiveness to local demands. Many are adopting digitalization strategies in product development and distribution to improve agility and customer engagement, reinforcing their market leadership across both industrial and consumer-facing segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1.1 Regional

- 2.2.1.2 Ingredient type

- 2.2.1.3 Nature

- 2.2.1.4 Application

- 2.2.1.5 End use

- 2.2.1.6 Distribution channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for convenience foods

- 3.2.1.2 Growth in commercial bakery sector

- 3.2.1.3 Increasing disposable income

- 3.2.1.4 Changing consumer lifestyles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuating raw material prices

- 3.2.2.2 Health concerns related to additives

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle east & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Ingredient Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Baking powders & leavening agents

- 5.3 Emulsifiers

- 5.4 Enzymes

- 5.5 Oils, fats & shortenings

- 5.6 Sweeteners

- 5.7 Colors & flavors

- 5.8 Preservatives

- 5.9 Flour

- 5.10 Starches

- 5.11 Others

Chapter 6 Market Estimates & Forecast, By Nature, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Organic

- 6.4 Clean label

- 6.5 Non-GMO

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bread

- 7.3 Cakes & pastries

- 7.4 Cookies & biscuits

- 7.5 Rolls & pies

- 7.6 Pizza crusts

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Commercial/industrial bakeries

- 8.3 Retail bakeries

- 8.4 Artisanal bakeries

- 8.5 Foodservice industry

- 8.6 Household/retail consumers

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 B2B

- 9.3 B2C

- 9.3.1 Supermarkets & hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Convenience stores

- 9.3.4 Online retail

- 9.3.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 AAK AB

- 11.2 Archer Daniels Midland Company

- 11.3 Associated British Foods plc

- 11.4 Bakels Group

- 11.5 BASF SE

- 11.6 Cargill, Incorporated

- 11.7 Corbion N.V.

- 11.8 Dawn Food Products, Inc.

- 11.9 DuPont de Nemours, Inc.

- 11.10 DSM-Firmenich AG

- 11.11 Flowers Foods, Inc.

- 11.12 General Mills, Inc.

- 11.13 Grupo Bimbo, S.A.B. de C.V.

- 11.14 Ingredion Incorporated

- 11.15 Kerry Group plc

- 11.16 Koninklijke DSM N.V.

- 11.17 Lesaffre Group

- 11.18 Mondelez International, Inc.

- 11.19 Puratos Group

- 11.20 Tate & Lyle PLC