|

시장보고서

상품코드

1773217

자동 창고 시스템(ASRS) 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Automated Storage and Retrieval System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

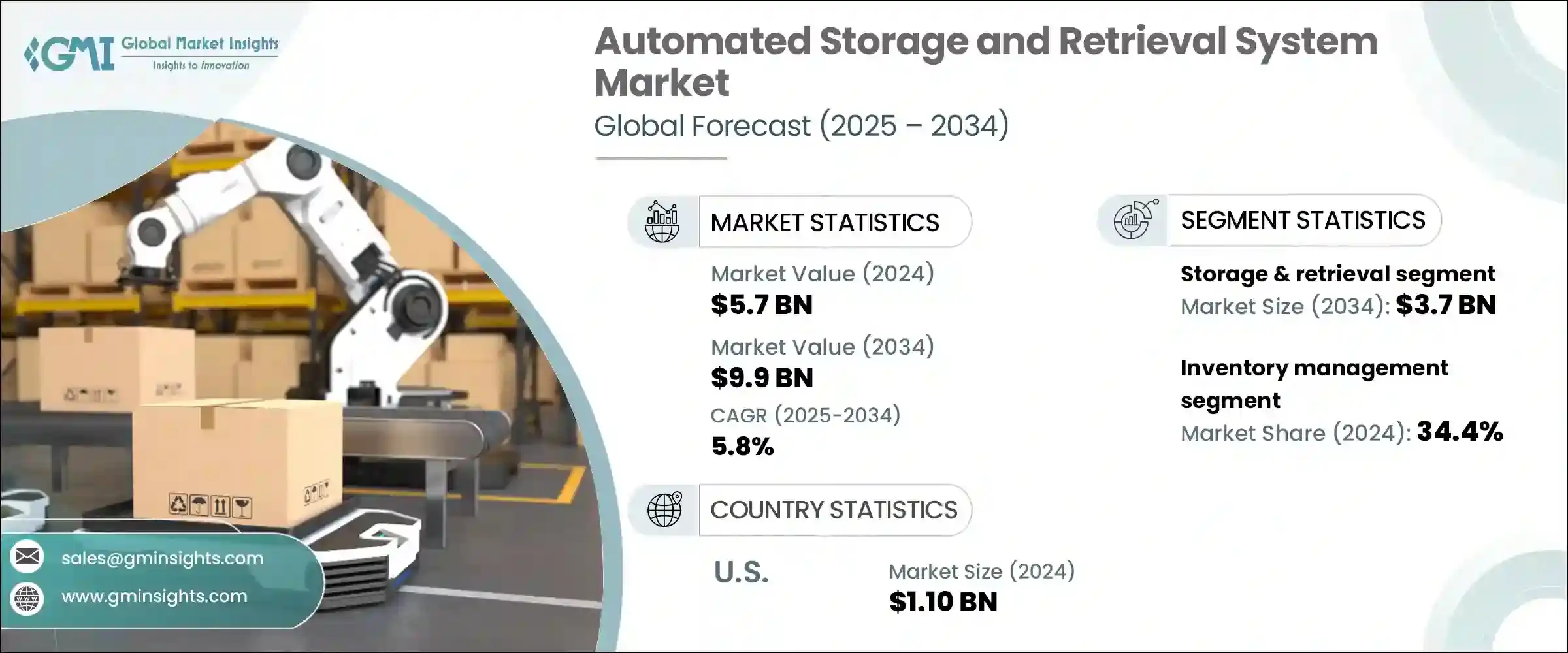

자동 창고 시스템(ASRS) 세계 시장 규모는 2024년에 57억 달러로 평가되었고, CAGR 5.8%로 성장하여 2034년에는 99억 달러에 이를 것으로 예측됩니다.

전자상거래의 급격한 성장으로 인해 창고는 더 빠르고, 더 정확하고, 더 저렴한 비용으로 배송할 필요가 있으며, ASRS 시스템은 이동 시간을 단축하고 피킹의 정확도를 높이는 "사람 대 사람" 모델을 촉진합니다. 수직 스토리지를 사용하여 입방 공간을 최대화함으로써 이러한 시스템은 간접비를 절감하고 경작업 및 특수 취급과 같은 부가가치 활동을 위해 지상 공간을 확보할 수 있습니다. 노동력 부족과 임금 상승도 물류센터를 자동화의 길로 이끌고 있습니다. ASRS는 노동집약적인 피킹 작업의 최대 3분의 2를 대체할 수 있는 ASRS를 통해 기업은 직원을 감독 및 유지보수 역할로 전환하여 효율성을 높이고 노동력 제약에 대처할 수 있습니다.

창고 효율성에 대한 관심이 높아지면서 고밀도 자동 창고 시스템(ASRS)으로의 전환이 가속화되고 있습니다. 특히 도시 지역과 임대료가 높은 지역에서는 모든 업종의 기업들이 평방피트당 공간을 최대한 활용해야 하기 때문에 수직형 및 모듈형 ASRS 구성에 대한 수요가 증가하고 있습니다. 이러한 시스템을 통해 기업은 재고에 대한 신속하고 정확한 접근을 유지하면서 입방체 부피를 최대화할 수 있습니다. 또한, ASRS 기술은 다양한 평면도와 천장 높이에 맞게 설계되어 기존 시설을 개조하거나 새로운 스마트 창고에 통합하는 데 적합하도록 설계되고 있습니다. 물리적 공간을 확장하지 않고도 스토리지를 확장할 수 있는 능력은 부동산 비용을 절감할 뿐만 아니라, 보다 슬림한 운영을 지원하여 공간 제약이 있는 환경에서 전략적 우위를 점할 수 있게 해줍니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 57억 달러 |

| 예측 금액 | 99억 달러 |

| CAGR | 5.8% |

보관 및 검색 기능 분야는 2024년 22억 달러, 2034년에는 37억 달러에 달할 것으로 예측됩니다. 이 기능은 ASRS 시스템의 핵심으로, 고밀도 재고 관리와 신속한 SKU 접근을 가능하게 하여 소매, 제약, 전자, 자동차에 이르기까지 모든 분야에서 필수적인 요소로 자리 잡고 있습니다. 창고 공간의 제약이 갈수록 심해지는 가운데, ASRS 시스템의 수직 보관 기능은 실시간 재고 동기화와 함께 수축 및 인적 오류를 줄이는 데 도움이 됩니다.

재고 관리 분야는 2024년 20억 달러 규모로 34.4%의 점유율을 차지했습니다. 실시간 재고 가시성, 자동 재고 회전(FIFO/LIFO), 과잉 재고 및 품절 방지 등을 통해 재고 관리는 ASRS 도입의 핵심 요소로 자리 잡았으며, RFID 및 바코드 스캐닝과 같은 기술을 사용하여 ERP/WMS 플랫폼과 통합함으로써 공급망 전반에 걸쳐 데이터의 정확성과 운영 효율성을 보장합니다. 데이터의 정확성과 업무 효율성을 확보할 수 있습니다.

미국 자동 창고 시스템(ASRS) 2024년 시장 규모는 11억 달러로 평가되었고, 2034년까지 5.8%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 미국은 강력한 제조업, 소매업, 물류 부문에 힘입어 창고 자동화 분야에서 선두를 달리고 있습니다. 업계 리더들이 공급망 디지털화의 벤치마크를 설정하면서 확장 가능하고 효율적인 스토리지 솔루션에 대한 수요가 증가하고 있으며, ASRS 기술은 특히 대규모 물류센터에서 인건비 절감, 정확도 향상, 처리 능력 향상에 중요한 역할을 하고 있습니다. 중요한 역할을 하고 있습니다.

이 업계의 주요 기업으로는 Symbotic LLC, Symbotic LLC, Daifuku Co., Ltd., TGW Logistics Group, Kardex Group, and Kion Group AG가 있으며, 이들은 시장의 약 15%를 점유하고 있습니다. 업계 리더들은 일련의 전략적 이니셔티브를 통해 시장에서의 입지를 강화하고 있습니다. 이들은 유연한 구성과 로봇 공학, AI, IoT 시스템과의 통합을 지원하는 모듈식 ASRS 설계와 확장 가능한 소프트웨어 플랫폼에 투자하고 있습니다.

창고업체, 전자상거래 업체, 물류 통합업체와의 파트너십을 통해 맞춤형 솔루션을 제공합니다. 현지 제조 및 서비스 센터를 통해 전 세계에 거점을 확대함으로써 보다 신속한 배포 및 지원이 가능합니다. 또한, 기업의 진입장벽을 낮추기 위해 구독 기반 및 관리형 서비스 모델을 출시하고 있습니다. 실시간 분석, 예지보전, 원격 시스템 모니터링을 제공함으로써 성능과 신뢰성으로 차별화를 꾀하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 기회

- 성장 가능성 분석

- 향후 시장 동향

- 기술 및 혁신 상황

- 현재 기술 동향

- 신기술

- 가격 동향

- 지역별

- 제품별

- 규제 상황

- 표준과 컴플라이언스 요건

- 지역 규제 구조

- 인증 기준

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 시스템 유형별, 2021년-2034년

- 주요 동향

- 유닛 로드 크레인

- 미니 로드 크레인

- 수직 리프트 모듈

- 로봇 셔틀 기반

- 로봇 큐브 기반

- 카르세르베이스

- 수직 캐러셀

- 수평 캐러셀

- 기타

제6장 시장 추산·예측 : 기능별, 2021년-2034년

- 주요 동향

- 보관 및 검색

- 주문 피킹 및 통합

- 버퍼링 및 시퀀싱

- 키팅 및 조립 지원

- 보충

제7장 시장 추산·예측 : 용도별, 2021년-2034년

- 주요 동향

- 콜드체인 보관

- 재고 관리

- 주문 처리

- 제작 지원

- 역물류

제8장 시장 추산·예측 : 최종 이용 산업별, 2021년-2034년

- 주요 동향

- 항공우주 및 방위

- 자동차

- 일렉트로닉스 및 반도체

- 헬스케어

- 금속 및 중기

- 소매 및 E-Commerce

- 기타

제9장 시장 추산·예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카공화국

제10장 기업 개요

- Automation Logistics Corporation

- Bastian Solutions

- Beumer Group

- Daifuku Co., Ltd.

- Dematic

- Egemin Automation

- Kardex Group

- Kion Group AG

- Knapp AG

- Mecalux, S.A.

- Murata Machinery, Ltd.

- Schaefer Systems International, Inc.

- Swisslog Holding AG

- Symbotic LLC

- System Logistics Corporation

- TGW Logistics Group

- Vanderlande Industries

- Westfalia Technologies, Inc.

- Witron Logistik+Informatik GmbH

The Global Automated Storage and Retrieval System Market was valued at USD 5.7 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 9.9 billion by 2034. The rapid growth of e-commerce is putting mounting pressure on warehouses to deliver faster, more accurately, and at a lower cost. ASRS systems facilitate a "goods-to-person" model that slashes travel time and boosts picking accuracy. By using vertical storage to maximize cubic space, these systems lower overheads and free up ground-level space for value-added activities like light manufacturing and specialized handling. Labor shortages and rising wages are also pushing distribution centers toward automation. With ASRS capable of replacing up to two-thirds of labor-intensive picking tasks, companies can redirect staff to supervisory and maintenance roles, enhancing efficiency and addressing workforce constraints.

The rising emphasis on warehouse efficiency is accelerating the shift toward high-density automated storage and retrieval systems. Companies across industries are under pressure to make the most of every square foot-particularly in urban and high-rent areas-driving strong demand for vertical and modular ASRS configurations. These systems allow businesses to maximize cubic volume while maintaining quick and accurate access to inventory. Additionally, ASRS technologies are increasingly being designed to adapt to varied floor plans and ceiling heights, making them suitable for retrofitting in older facilities and integration into newly constructed smart warehouses. The ability to scale storage without expanding physical footprints not only cuts real estate costs but also supports leaner operations, giving businesses a strategic edge in space-constrained environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.7 Billion |

| Forecast Value | $9.9 Billion |

| CAGR | 5.8% |

The storage & retrieval functionality segment generated USD 2.2 billion in 2024 and is expected to reach USD 3.7 billion by 2034. This capability lies at the heart of ASRS systems, enabling high-density inventory management and rapid SKU access, making it indispensable across sectors from retail and pharmaceuticals to electronics and automotive. As warehouse space becomes more constrained, these systems' ability to leverage vertical storage, paired with real-time inventory synchronization, helps reduce shrinkage and human error.

The inventory management segment generated USD 2 billion in 2024 and accounted for a 34.4% share. Real-time stock visibility, automated stock rotation (FIFO/LIFO), and prevention of overstocking or stockouts make inventory management a critical component of ASRS adoption. Integration with ERP/WMS platforms, using technologies like RFID and barcode scanning, helps ensure data accuracy and operational efficiency throughout the supply chain.

United States Automated Storage and Retrieval System Market was valued at USD 1.1 billion in 2024 and is forecasted to grow at a CAGR of 5.8% through 2034. The country leads in warehouse automation, supported by strong manufacturing, retail, and logistics sectors. With industry leaders setting benchmarks for supply chain digitization, there's a strong demand for scalable, efficient storage solutions. ASRS technology plays a key role in reducing labor costs, improving accuracy, and increasing throughput, especially in large distribution centers.

Among the major players in this industry are Symbotic LLC, Daifuku Co., Ltd., TGW Logistics Group, Kardex Group, and Kion Group AG, which collectively hold approximately 15% of the market. Industry leaders are strengthening their market positions through a series of strategic initiatives. They are investing in modular ASRS designs and scalable software platforms that support flexible configuration and integration with robotics, AI, and IoT systems.

Partnerships with warehouse operators, e-commerce firms, and logistics integrators are helping them deliver tailored solutions. Expanding global footprints via local manufacturing and service centers allows quicker deployment and support. Companies are also launching subscription-based or managed service models to lower entry barriers for businesses. By offering real-time analytics, predictive maintenance, and remote system monitoring, they differentiate themselves through performance and reliability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By System Type, 2021 - 2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Unit load cranes

- 5.3 Mini load cranes

- 5.4 Vertical lift module

- 5.5 Robotic shuttle-based

- 5.6 Robotic cube-based

- 5.7 Carousel-based

- 5.7.1 Vertical carousel

- 5.7.2 Horizontal carousel

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Function, 2021 - 2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Storage & retrieval

- 6.3 Order picking & consolidation

- 6.4 Buffering & sequencing

- 6.5 Kitting & assembly support

- 6.6 Replenishment

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Cold chain storage

- 7.3 Inventory management

- 7.4 Order fulfillment

- 7.5 Production support

- 7.6 Reverse logistics

Chapter 8 Market Estimates & Forecast, By End Use Industry, 2021 - 2034, (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Aerospace & defense

- 8.3 Automotive

- 8.4 Electronics & semiconductors

- 8.5 Healthcare

- 8.6 Metals & heavy machinery

- 8.7 Retail & e-commerce

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 Automation Logistics Corporation

- 10.2 Bastian Solutions

- 10.3 Beumer Group

- 10.4 Daifuku Co., Ltd.

- 10.5 Dematic

- 10.6 Egemin Automation

- 10.7 Kardex Group

- 10.8 Kion Group AG

- 10.9 Knapp AG

- 10.10 Mecalux, S.A.

- 10.11 Murata Machinery, Ltd.

- 10.12 Schaefer Systems International, Inc.

- 10.13 Swisslog Holding AG

- 10.14 Symbotic LLC

- 10.15 System Logistics Corporation

- 10.16 TGW Logistics Group

- 10.17 Vanderlande Industries

- 10.18 Westfalia Technologies, Inc.

- 10.19 Witron Logistik + Informatik GmbH