|

시장보고서

상품코드

1773232

유아용 조제분유 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Infant Formula Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

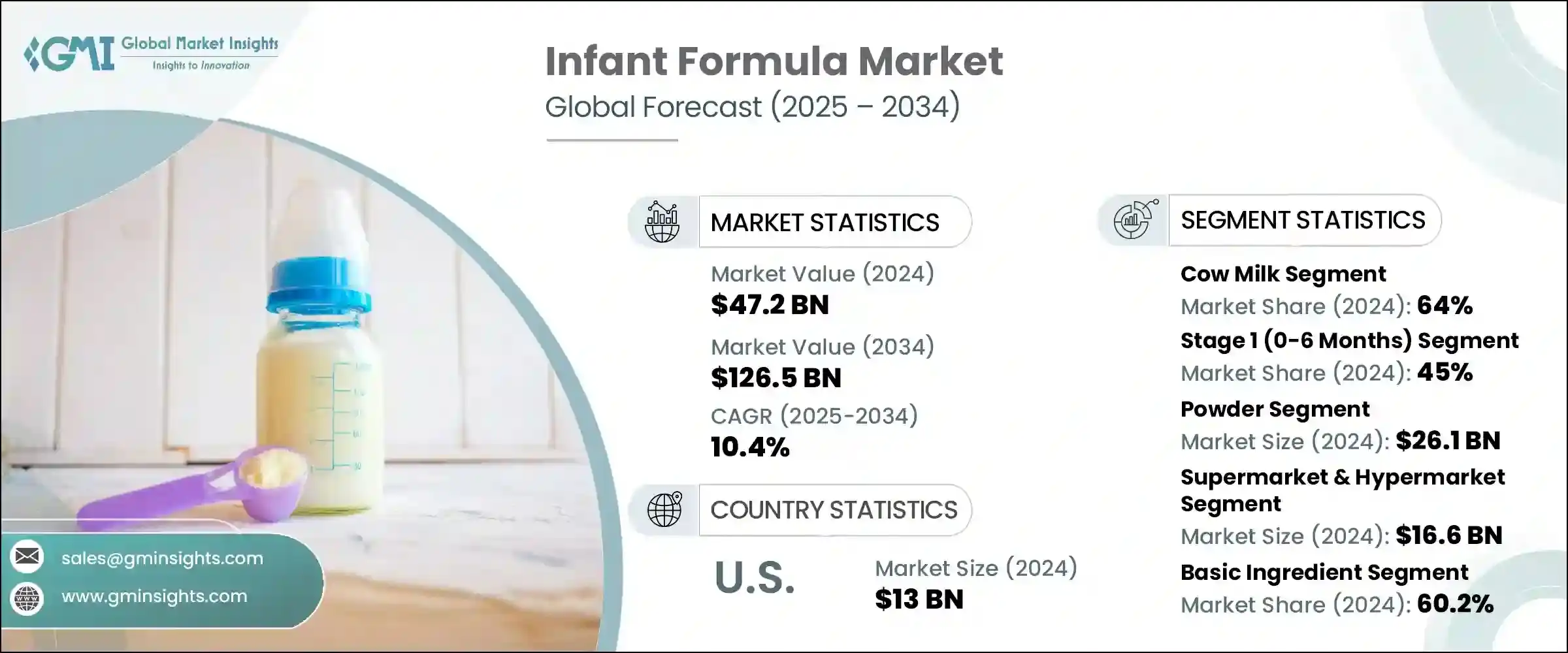

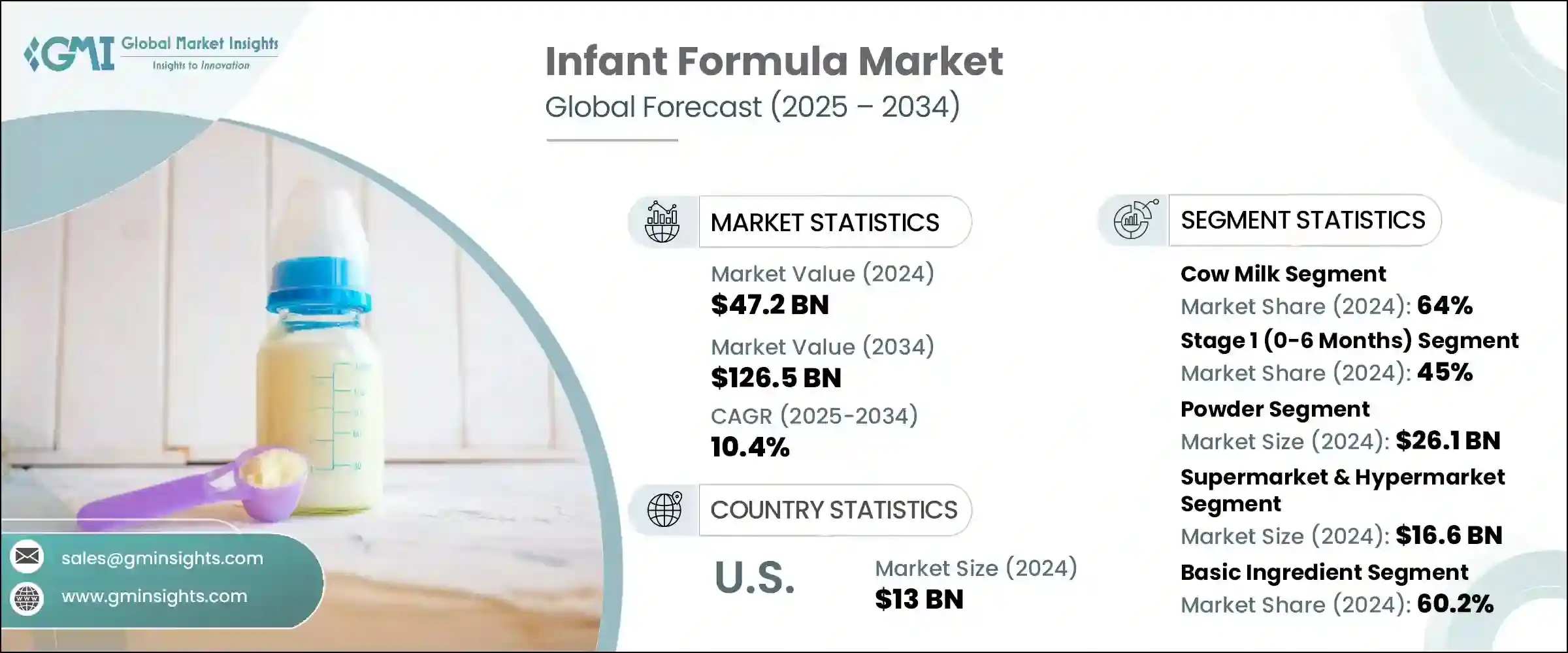

세계의 유아용 조제분유 시장은 2024년에 472억 달러로 평가되며, CAGR 10.4%로 성장하며, 2034년에는 1,265억 달러에 달할 것으로 추정되고 있습니다.

성장의 주요 요인은 영유아 영양에 대한 인식 증가, 일하는 어머니 증가, 특히 개발도상국의 출산율 증가입니다. 도시화, 가처분 소득 증가, 여성의 노동 참여율 증가도 시장 확대의 요인입니다. 또한 부모들이 제품의 안전성, 소화성, 영양가를 중시하게 되면서 유기농, 무유당, 저알레르기 등 고급 분유에 대한 수요가 급증하고 있습니다.

프리바이오틱스, 프로바이오틱스, HMO(Human Milk Oligosaccharide), DHA/ARA와 같은 분유 성분의 기술적 발전은 이러한 제품의 수용을 더욱 촉진하고 있습니다. 그러나 이러한 제품의 높은 가격, 복잡한 규제, 특히 공중 보건 캠페인이 널리 퍼져 있는 지역에서는 모유 수유에 대한 강한 문화적 선호도 등의 문제가 여전히 남아 있습니다. 또한 일부 시장에서는 위조 분유에 대한 불안감으로 인해 소비자의 신뢰를 얻지 못하는 것도 시장 성장을 제한하고 있습니다. 부모들이 합성 첨가제, 유전자 변형 작물, 인공 감미료가 없는 제품을 요구하면서 클린 라벨, 유기농, 식물성 우유로의 전환이 두드러지게 나타나고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 472억 달러 |

| 예측 금액 | 1,265억 달러 |

| CAGR | 10.4% |

2024년에는 우유 기반 분유가 64%의 점유율을 차지하며, 2034년까지 10.4%의 연평균 복합 성장률(CAGR)로 안정적인 성장세를 유지할 것으로 예측됩니다. 이 분유는 특히 DHA, ARA, 철분 강화 모유와 같은 영양 프로파일로 인해 여전히 가장 선호되는 분유입니다. 표준 조제분유는 일반적으로 모유 수유를 하지 않는 건강한 영아에게 선택됩니다. 개발업체들은 소화불량이나 경미한 우유 불내증이 있는 영아를 위해 부분 가수분해 분유, 광범위 가수분해 분유 등을 개발하기도 합니다.

단계별로는 1단계(0-6개월 유아)가 2024년 45%의 점유율로 가장 큰 비중을 차지할 것으로 예측됩니다. 이 부문은 2034년까지 10.6%의 연평균 복합 성장률(CAGR)로 빠르게 성장할 것으로 예측됩니다. 영아기의 이 중요한 시기에는 소화기관이 아직 성숙하지 않기 때문에 모유나 분유에만 의존하여 영양을 공급받습니다. 1단계 분유는 DHA, ARA, 프리바이오틱스, 철분 등 필수 영양소를 함유하고 인지, 면역, 소화기 건강을 촉진하도록 설계된 위 친화적인 분유입니다. 규제기관은 이 제품들이 엄격한 안전성과 유효성 기준을 충족하는지 확인하여 소비자의 신뢰를 높이고 있습니다.

2024년 미국 시장 규모는 130억 달러로, 2034년까지 CAGR 8.4%로 성장할 전망입니다. 미국은 높은 출산율, 첨단화된 의료 시스템, 유아용 조제분유의 보급, 높은 브랜드 충성도를 바탕으로 시장을 선도하고 있습니다. 이 시장 특징은 유기농, 비GMO, 식물성 원료, HMO 및 DHA/ARA 강화 제제 등 프리미엄 제제 및 특수 제제의 인기가 높아지고 있다는 점입니다.

이 분야의 주요 기업에는 Nestle, Abbott Nutrition, Arla Food, Bellamy's Organic, Bubs Australia 등이 있으며, 이들은 시장에서의 입지를 강화하기 위해 경쟁하고 있습니다. 유아용 조제분유 기업은 시장에서의 입지를 강화하고 영향력을 확대하기 위해 몇 가지 전략적 구상을 채택하고 있습니다. 특히 분유 배합에서 HMO, DHA, ARA, 프리바이오틱스 등 모유에 함유된 영양소와 유사한 영양소를 도입하는 등 기술 혁신에 주력하고 있습니다. 이러한 개선은 유아의 인지 발달, 면역력, 소화기 건강을 향상시키는 것을 목표로 하고 있습니다. 또한 이들 기업은 연구개발에 대한 투자를 크게 늘려 무유당, 유기농, 저알레르기 등 특수 우유에 대한 수요 증가에 대응하기 위해 더욱 진보된 신제품을 생산하고 있습니다.

클린 라벨, 비 GMO, 식물성 분유로 전환하는 것도 건강을 중시하는 부모들의 선호를 충족시키기 위해 받아들여지고 있습니다. 또한 각 업체들은 유통망을 강화하고, 소매점과의 제휴를 강화하며, 신흥 시장에서 사업을 확장하여 자사 제품을 더 널리 이용할 수 있도록 하고 있습니다. 주요 브랜드들은 또한 최고 수준의 안전 기준을 준수하고 투명한 제품 표시를 제공함으로써 소비자의 신뢰를 구축하는 데 주력하고 있으며, 이는 오늘날 시장에서 점점 더 중요해지고 있습니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 어프로치

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사·검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 공급업체의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 촉진요인

- 업계의 잠재적 리스크·과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter의 산업 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술·혁신의 상황

- 현재 기술 동향

- 신규 기술

- 특허 상황

- 무역통계(HS 코드)(주 : 무역통계는 주요 국가만 제공)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능 관행

- 폐기물 삭감 전략

- 생산에서의 에너지 효율

- 친환경 구상

- 영양 과학과 제품 개발

- 유아 영양 소요량

- 주요 영양소 필요량

- 단백질 필요량

- 탄수화물 필요량

- 지방 필요량

- 미량영양소 필요량

- 비타민 필요량

- 미네랄 필요량

- 연령 특정 영양 요구

- 특별한 식사 제한

- 주요 영양소 필요량

- 처방 구성과 기준

- 국제기준

- 지역에 의한 차이

- 품질 사양

- 안전 파라미터

- 기능성 성분 혁신

- 모유 올리고당(HMO)

- 프로바이오틱스·프리바이오틱스

- 장쇄 다가불포화지방산

- 뉴클레오티드·성장인자

- 제품 개발 프로세스

- 연구개발

- 임상 연구·시험

- 규제 승인 프로세스

- 상업 발매

- 영양 성분 표시와 포지셔닝

- 건강 강조 표시에 관한 규제

- 과학적 근거

- 마케팅 커뮤니케이션

- 소비자 교육

- 향후 영양 동향

- 맞춤형 영양

- 마이크로바이옴 연구

- 인지 발달 지원

- 면역 시스템 강화

- 유아 영양 소요량

- 제조 및 품질관리

- 제조 공정

- 원재료 준비

- 혼합·조제

- 열처리

- 분무 건조

- 포장·밀봉

- 품질관리 시스템

- 적정 제조 규범(GMP)

- HACCP(azard Analysis Critical Control Points)

- 품질 보증 테스트

- 배치 테스트 프로토콜

- 안전·오염 관리

- 미생물학적 안전성

- 화학 오염물질 제어

- 물리적 위험 방지

- 알레르겐 관리

- 설비·기술

- 처리 장비

- 시험·분석 기기

- 포장기계

- 자동화 및 제어 시스템

- 공급망 관리

- 원재료 조달

- 공급업체 자격

- 재고 관리

- 콜드체인 관리

- 규제 준수

- 제조 기준

- 시설 검사

- 문서화 요건

- 리콜 절차

- 제조 공정

- 소비자 행동과 시장 역학

- 소비자의 인구통계

- 부모 연령층

- 소득수준

- 교육 레벨

- 지역적 분포

- 구입 결정 요인

- 영양상 이점

- 브랜드 신뢰와 평판

- 가격 민감도

- 헬스케어 프로바이더 권장사항

- 편리성 요인

- 섭식 패턴과 선호도

- 완전 분유 수유

- 혼합 수유(모유+분유)

- 이동기 수유

- 문화적 수유 습관

- 정보원·영향

- 헬스케어 종사자

- 온라인 리소스

- 가족·친구

- 소셜미디어의 영향 요인

- 브랜드 로열티·변환 행동

- 브랜드 로열티 요인

- 변환 트리거

- 트라이얼과 채택 패턴

- 권장 행동

- 지역별 소비자의 차이

- 북미의 소비자

- 유럽의 소비자

- 아시아태평양의 소비자

- 기타 지역

- 소비자의 인구통계

- 마케팅·유통 전략

- 마케팅 전략

- 브랜드 포지셔닝

- 프리미엄 포지셔닝

- 가치 포지셔닝

- 전문 분야 포지셔닝

- 타겟 청중 세분화

- 마케팅 채널

- 헬스케어 전문가 관여

- 디지털 마케팅

- 기존 미디어

- 교육 프로그램

- 브랜드 포지셔닝

- 유통 전략

- 멀티채널 유통

- 채널 파트너 관리

- 지역적 확대

- 시장 침투 전략

- 가격 전략

- 프리미엄 가격

- 경쟁력 있는 가격

- 가치에 기반한 가격결정

- 지역에 의한 가격차

- 프로모션 활동

- 헬스케어 전문가용 프로그램

- 소비자 교육 캠페인

- 샘플링 프로그램

- 로열티 프로그램

- 디지털 변혁

- E-Commerce 전략

- 디지털 고객 관여

- 데이터 분석과 인사이트

- 옴니채널 통합

- 규제상 마케팅상의 고려 사항

- WHO 코드 준거

- 광고 제한

- 건강 강조 표시 규제

- 윤리적인 마케팅 관행

- 마케팅 전략

- 혁신과 향후 동향

- 현재 혁신의 동향

- 기능성 성분

- 오가닉 & 클린 라벨

- 맞춤형 영양

- 지속가능 포장

- 신규 기술

- 정밀 영양

- 마이크로캡슐

- 새로운 처리 기술

- 스마트 패키지

- 연구개발 중점

- 장내세균총 연구

- 인지 발달

- 면역 시스템 지원

- 알레르기 예방

- 지속가능성 구상

- 지속가능 조달

- 이산화탄소 배출량의 삭감

- 순환형 경제 원칙

- 환경 영향 완화

- 디지털 혁신

- 스마트 수유 솔루션

- 모바일 앱

- IoT 통합

- AI를 활용한 권장사항

- 향후 시장 동향

- 시장의 통합

- 프리미엄 부문의 성장

- 신흥 시장의 확대

- 규제의 진화

- 현재 혁신의 동향

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십과 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 제품 유형별, 2021-2034년

- 주요 경향

- 우유 기반 분유

- 표준적 우유 배합

- 부분 가수분해 배합

- 완전 가수분해 배합

- 대두 기반 분유

- 단백질 가수분해물 배합

- 특수 배합

- 미숙아용 조제분유

- 역류 방지 처방

- 무유당

- 아미노산 기반 배합

- 기타

- 오가닉 분유

- 산양유 기반 분유

제6장 시장 추산·예측 : 스테이지별, 2021-2034년

- 주요 경향

- 스테이지 1(0-6개월)

- 스테이지 2(6-12개월)

- 스테이지 3(12-24개월)

- 스테이지 4(24개월 이상)

제7장 시장 추산·예측 : 형태별, 2021-2034년

- 주요 경향

- 분말

- 액체 농축물

- Ready-to-feed

제8장 시장 추산·예측 : 유통 채널별, 2021-2034년

- 주요 경향

- 슈퍼마켓·하이퍼마켓

- 약국·드러그스토어

- 온라인 소매

- E-Commerce 플랫폼

- 소비자 직판 웹사이트

- 유아 용품 전문점

- 병원·클리닉

- 편의점

- 기타

제9장 시장 추산·예측 : 성분별, 2021-2034년

- 주요 경향

- 기본적인 재료

- 단백질

- 유청 단백질

- 카제인

- 대두 단백질

- 탄수화물

- 유당

- 콘 시럽 고형물

- 기타

- 지방·오일

- 식물성 오일

- DHA·ARA

- 단백질

- 기능성 성분

- 프리바이오틱스

- 프로바이오틱스

- 모유 올리고당(HMO)

- 뉴클레오티드

- 비타민·미네랄

- 비타민

- 미네랄

제10장 시장 추산·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카 지역

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

- 기타 중동 및 아프리카

제11장 기업 개요

- Abbott Nutrition

- Arla Food

- Bellamy's Organic

- BUBS Australia

- Hero Group

- Mead Johnson Nutrition

- Nestle

- Nutricia

- The Kraft Heinz Company

- Danone S.A.

- Reckitt Benckiser Group plc(Mead Johnson)

- Perrigo Company plc

The Global Infant Formula Market was valued at USD 47.2 billion in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 126.5 billion by 2034. The growth is largely attributed to rising awareness around infant nutrition, the increasing number of working mothers, and higher birth rates, especially in developing nations. Urbanization, an increase in disposable income, and higher female workforce participation are also contributing factors to the market expansion. Additionally, parents are becoming more concerned with product safety, digestibility, and nutritional value, leading to a surge in demand for premium formulas, including organic, lactose-free, and hypoallergenic options.

Technological advancements in formula composition, like incorporating prebiotics, probiotics, HMOs (human milk oligosaccharides), and DHA/ARA, are further boosting the acceptance of these products. However, challenges remain, including the high cost of these products, complex regulations, and strong cultural preferences for breastfeeding, particularly in regions where public health campaigns are prevalent. Market growth is also limited by a lack of consumer trust in some markets due to fears about counterfeit formulas. There is a noticeable shift towards clean-label, organic, and plant-based formulas, as parents demand products free of synthetic additives, GMOs, and artificial sweeteners.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $47.2 Billion |

| Forecast Value | $126.5 Billion |

| CAGR | 10.4% |

In 2024, the cow milk-based formula segment commanded a 64% share and is expected to maintain steady growth with a CAGR of 10.4% through 2034. This formula remains the most preferred due to its nutritional profile, which is like breast milk, especially when fortified with DHA, ARA, and iron. Standard cow's milk formula is typically chosen for healthy, full-term infants who are not breastfed. Manufacturers have also developed varieties like partially and extensively hydrolyzed formulas to cater to infants with digestive issues or mild cow's milk intolerance.

Among different stages, the Stage 1 (for infants aged 0-6 months) segment holds the largest share, accounting for 45% in 2024. This segment is expected to see rapid growth, driven by a CAGR of 10.6% through 2034. At this critical stage of infancy, babies rely solely on breast milk or formula for nourishment as their digestive systems are still maturing. Stage 1 formulas are designed to be gentle on the stomach, containing essential nutrients like DHA, ARA, prebiotics, and iron to promote cognitive, immune, and digestive health. Regulatory bodies ensure that strict safety and efficacy standards are met for these products, thereby enhancing consumer confidence.

U.S. Infant Formula Market generated USD 13 billion in 2024 and is set to grow at a CAGR of 8.4% by 2034. The U.S. leads due to its high birth rates, advanced healthcare systems, widespread availability of infant formula, and strong brand loyalty. The market here is characterized by the increasing popularity of premium and speciality formulas, including organic, non-GMO, and plant-based options, as well as formulas enriched with HMOs and DHA/ARA.

Leading companies in this space include Nestle, Abbott Nutrition, Arla Food, Bellamy's Organic, and Bubs Australia, each vying for a stronger market presence. Infant formula companies have been adopting several strategic initiatives to strengthen their market position and expand their influence. They are focusing heavily on innovation, particularly in formula composition, by incorporating nutrients that closely mimic those found in breast milk, such as HMOs, DHA, ARA, and prebiotics. These improvements aim to enhance cognitive development, immunity, and digestive health for infants. Moreover, these companies are significantly increasing their investments in research and development to create new, more advanced products that cater to the growing demand for speciality formulas, such as lactose-free, organic, and hypoallergenic varieties.

The shift toward clean-label, non-GMO, and plant-based formulas is also being embraced to meet the preferences of health-conscious parents. Additionally, companies are enhancing their distribution networks, strengthening retail partnerships, and expanding in emerging markets to ensure the wider availability of their products. Leading brands are also focusing on building consumer trust by adhering to the highest safety standards and offering transparent product labeling, which is increasingly important in today's market.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Stage

- 2.2.4 Form

- 2.2.5 Distribution channel

- 2.2.6 Ingredient

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Nutritional Science & product development

- 3.13.1 Nutritional Requirements for Infants

- 3.13.1.1 Macronutrient requirements

- 3.13.1.1.1 Protein requirements

- 3.13.1.1.2 Carbohydrate requirements

- 3.13.1.1.3 Fat requirements

- 3.13.1.2 Micronutrient requirements

- 3.13.1.2.1 Vitamin requirements

- 3.13.1.2.2 Mineral requirements

- 3.13.1.3 Age-Specific nutritional needs

- 3.13.1.4 Special dietary requirements

- 3.13.1.1 Macronutrient requirements

- 3.13.2 Formula composition & standards

- 3.13.2.1 International standards

- 3.13.2.2 Regional variations

- 3.13.2.3 Quality specifications

- 3.13.2.4 Safety parameters

- 3.13.3 Functional ingredients innovation

- 3.13.3.1 Human Milk Oligosaccharides (HMO)

- 3.13.3.2 Probiotics & prebiotics

- 3.13.3.3 Long-Chain Polyunsaturated Fatty Acids

- 3.13.3.4 Nucleotides & growth factors

- 3.13.4 Product development process

- 3.13.4.1 Research & development

- 3.13.4.2 Clinical studies & trials

- 3.13.4.3 Regulatory approval process

- 3.13.4.4 Commercial launch

- 3.13.5 Nutritional claims & positioning

- 3.13.5.1 Health claims regulations

- 3.13.5.2 Scientific substantiation

- 3.13.5.3 Marketing communications

- 3.13.5.4 Consumer education

- 3.13.6 Future nutritional trends

- 3.13.6.1 Personalized nutrition

- 3.13.6.2 Microbiome research

- 3.13.6.3 Cognitive development support

- 3.13.6.4 Immune system enhancement

- 3.13.1 Nutritional Requirements for Infants

- 3.14 Manufacturing & quality control

- 3.14.1 Manufacturing process

- 3.14.1.1 Raw material preparation

- 3.14.1.2 Blending & mixing

- 3.14.1.3 Heat treatment

- 3.14.1.4 Spray drying

- 3.14.1.5 Packaging & sealing

- 3.14.2 Quality control systems

- 3.14.2.1 Good Manufacturing Practices (GMP)

- 3.14.2.2 Hazard Analysis Critical Control Points (HACCP)

- 3.14.2.3 Quality assurance testing

- 3.14.2.4 Batch testing protocols

- 3.14.3 Safety & contamination control

- 3.14.3.1 Microbiological safety

- 3.14.3.2 Chemical contaminant control

- 3.14.3.3 Physical hazard prevention

- 3.14.3.4 Allergen management

- 3.14.4 Equipment & technology

- 3.14.4.1 Processing equipment

- 3.14.4.2 Testing & analysis equipment

- 3.14.4.3 Packaging machinery

- 3.14.4.4 Automation & control systems

- 3.14.5 Supply chain management

- 3.14.5.1 Raw material sourcing

- 3.14.5.2 Supplier qualification

- 3.14.5.3 Inventory management

- 3.14.5.4 Cold chain management

- 3.14.6 Regulatory compliance

- 3.14.6.1 Manufacturing standards

- 3.14.6.2 Facility inspections

- 3.14.6.3 Documentation requirements

- 3.14.6.4 Recall procedures

- 3.14.1 Manufacturing process

- 3.15 Consumer behavior & market dynamics

- 3.15.1 Consumer demographics

- 3.15.1.1 Parental age groups

- 3.15.1.2 Income levels

- 3.15.1.3 Education levels

- 3.15.1.4 Geographic distribution

- 3.15.2 Purchase decision factors

- 3.15.2.1 Nutritional benefits

- 3.15.2.2 Brand trust & reputation

- 3.15.2.3 Price sensitivity

- 3.15.2.4 Healthcare provider recommendations

- 3.15.2.5 Convenience factors

- 3.15.3 Feeding patterns & preferences

- 3.15.3.1 Exclusive formula feeding

- 3.15.3.2 Mixed feeding (breast + formula)

- 3.15.3.3 Transitional feeding

- 3.15.3.4 Cultural feeding practices

- 3.15.4 Information sources & influences

- 3.15.4.1 Healthcare professionals

- 3.15.4.2 Online resources

- 3.15.4.3 Family & friends

- 3.15.4.4 Social media influence

- 3.15.5 Brand loyalty & switching behavior

- 3.15.5.1 Brand loyalty factors

- 3.15.5.2 Switching triggers

- 3.15.5.3 Trial & adoption patterns

- 3.15.5.4 Recommendation behavior

- 3.15.6 Regional consumer variations

- 3.15.6.1 North American consumers

- 3.15.6.2 European consumers

- 3.15.6.3 Asia-Pacific consumers

- 3.15.6.4 Other regional patterns

- 3.15.1 Consumer demographics

- 3.16 Marketing & distribution strategies

- 3.16.1 Marketing strategies

- 3.16.1.1 Brand positioning

- 3.16.1.1.1 Premium positioning

- 3.16.1.1.2 Value positioning

- 3.16.1.1.3 Specialty positioning

- 3.16.1.2 Target audience segmentation

- 3.16.1.3 Marketing channels

- 3.16.1.3.1 Healthcare professional engagement

- 3.16.1.3.2 Digital marketing

- 3.16.1.3.3 Traditional media

- 3.16.1.3.4 Educational programs

- 3.16.1.1 Brand positioning

- 3.16.2 Distribution strategies

- 3.16.2.1 Multi-channel distribution

- 3.16.2.2 Channel partner management

- 3.16.2.3 Geographic expansion

- 3.16.2.4 Market penetration strategies

- 3.16.3 Pricing strategies

- 3.16.3.1 Premium pricing

- 3.16.3.2 Competitive pricing

- 3.16.3.3 Value-based pricing

- 3.16.3.4 Regional pricing variations

- 3.16.4 Promotional activities

- 3.16.4.1 Healthcare professional programs

- 3.16.4.2 Consumer education campaigns

- 3.16.4.3 Sampling programs

- 3.16.4.4 Loyalty programs

- 3.16.5 Digital transformation

- 3.16.5.1 E-commerce strategies

- 3.16.5.2 Digital customer engagement

- 3.16.5.3 Data analytics & insights

- 3.16.5.4 Omnichannel integration

- 3.16.6 Regulatory marketing considerations

- 3.16.6.1 WHO code compliance

- 3.16.6.2 Advertising restrictions

- 3.16.6.3 Health claims regulations

- 3.16.6.4 Ethical marketing practices

- 3.16.1 Marketing strategies

- 3.17 Innovation & future trends

- 3.17.1 Current innovation trends

- 3.17.1.1 Functional ingredients

- 3.17.1.2 Organic & clean label

- 3.17.1.3 Personalized nutrition

- 3.17.1.4 Sustainable packaging

- 3.17.2 Emerging technologies

- 3.17.2.1 Precision nutrition

- 3.17.2.2 Microencapsulation

- 3.17.2.3 Novel processing technologies

- 3.17.2.4 Smart packaging

- 3.17.3 Research & development focus

- 3.17.3.1 Gut microbiome research

- 3.17.3.2 Cognitive development

- 3.17.3.3 Immune system support

- 3.17.3.4 Allergy prevention

- 3.17.4 Sustainability initiatives

- 3.17.4.1 Sustainable sourcing

- 3.17.4.2 Carbon footprint reduction

- 3.17.4.3 Circular economy principles

- 3.17.4.4 Environmental impact mitigation

- 3.17.5 Digital innovation

- 3.17.5.1 Smart feeding solutions

- 3.17.5.2 Mobile applications

- 3.17.5.3 IoT integration

- 3.17.5.4 AI-Powered recommendations

- 3.17.6 Future market trends

- 3.17.6.1 Market consolidation

- 3.17.6.2 Premium segment growth

- 3.17.6.3 Emerging market expansion

- 3.17.6.4 Regulatory evolution

- 3.17.1 Current innovation trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trend

- 5.2 Cow's milk-based formula

- 5.2.1 Standard cow's milk formula

- 5.2.2 Partially hydrolyzed formula

- 5.2.3 Extensively hydrolyzed formula

- 5.3 Soy-based formula

- 5.4 Protein hydrolysate formula

- 5.5 Specialty formula

- 5.5.1 Premature infant formula

- 5.5.2 Anti-reflux formula

- 5.5.3 Lactose-free formula

- 5.5.4 Amino acid-based formula

- 5.5.5 Other specialty formulas

- 5.6 Organic formula

- 5.7 Goat milk-based formula

Chapter 6 Market Estimates & Forecast, By Stage, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trend

- 6.2 Stage 1 (0–6 months)

- 6.3 Stage 2 (6–12 months)

- 6.4 Stage 3 (12–24 months)

- 6.5 Stage 4 (24+ months)

Chapter 7 Market Estimates & Forecast, By Form, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trend

- 7.2 Powder

- 7.3 Liquid concentrate

- 7.4 Ready-to-feed

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trend

- 8.2 Supermarkets & Hypermarkets

- 8.3 Pharmacies & Drug Stores

- 8.4 Online Retail

- 8.4.1 E-commerce Platforms

- 8.4.2 Direct-to-Consumer Websites

- 8.5 Specialty Baby Stores

- 8.6 Hospitals & Clinics

- 8.7 Convenience Stores

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Ingredient, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trend

- 9.2 Basic Ingredients

- 9.2.1 Proteins

- 9.2.1.1 Whey Protein

- 9.2.1.2 Casein

- 9.2.1.3 Soy Protein

- 9.2.2 Carbohydrates

- 9.2.2.1 Lactose

- 9.2.2.2 Corn Syrup Solids

- 9.2.2.3 Other Carbohydrates

- 9.2.3 Fats & Oils

- 9.2.3.1 Vegetable Oils

- 9.2.3.2 DHA & ARA

- 9.2.1 Proteins

- 9.3 Functional Ingredients

- 9.3.1 Prebiotics

- 9.3.2 Probiotics

- 9.3.3 Human Milk Oligosaccharides (HMO)

- 9.3.4 Nucleotides

- 9.4 Vitamins & Minerals

- 9.4.1 Vitamins

- 9.4.2 Minerals

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East & Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East & Africa

Chapter 11 Company Profiles

- 11.1 Abbott Nutrition

- 11.2 Arla Food

- 11.3 Bellamy's Organic

- 11.4 BUBS Australia

- 11.5 Hero Group

- 11.6 Mead Johnson Nutrition

- 11.7 Nestle

- 11.8 Nutricia

- 11.9 The Kraft Heinz Company

- 11.10 Danone S.A.

- 11.11 Reckitt Benckiser Group plc (Mead Johnson)

- 11.12 Perrigo Company plc