|

시장보고서

상품코드

1773234

결절성 양진 치료 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Prurigo Nodularis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

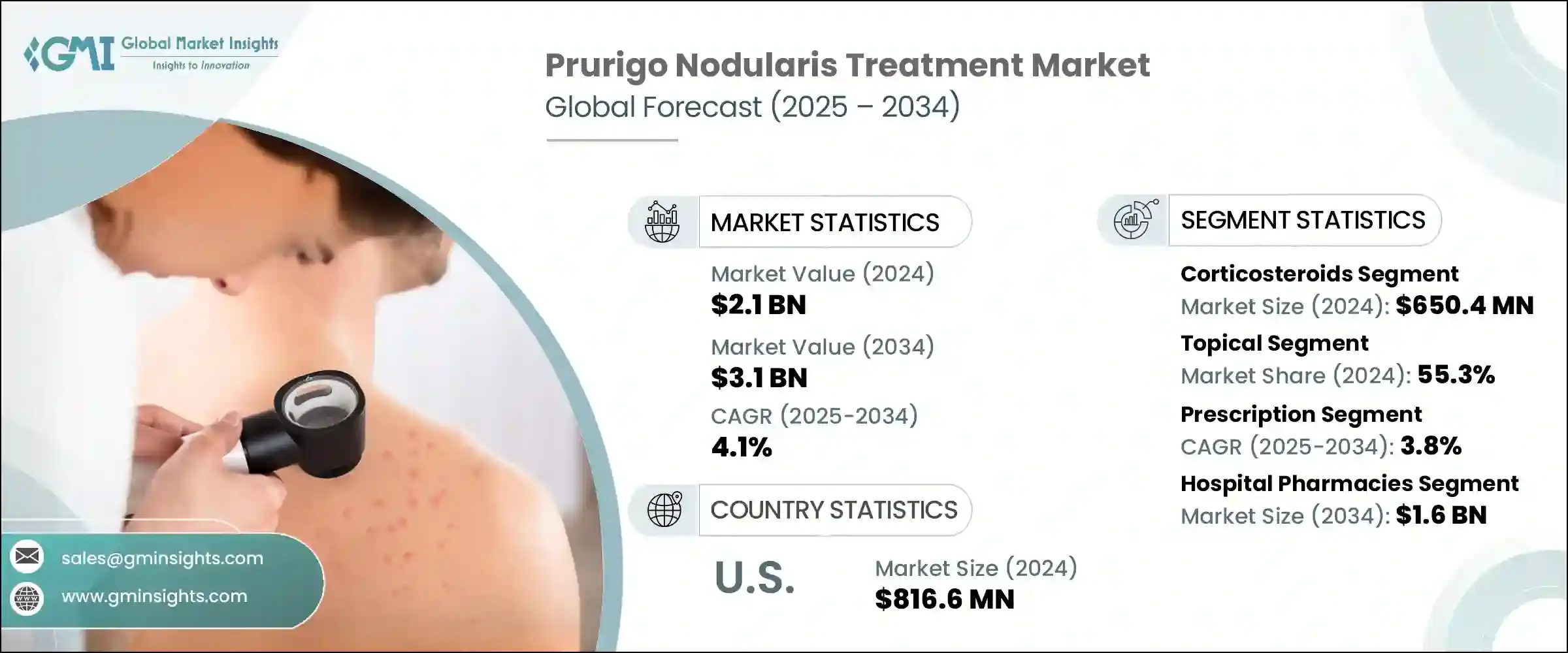

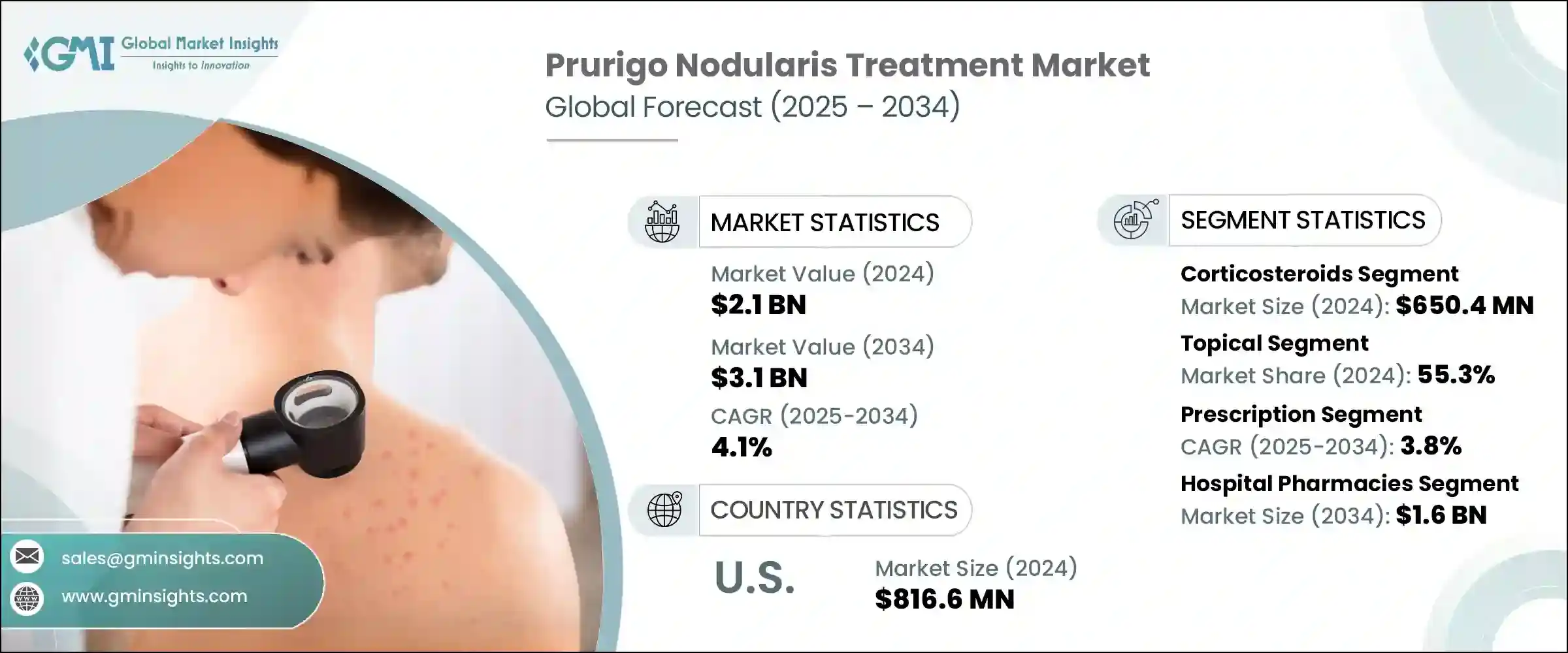

결절성 양진 치료 세계 시장 규모는 2024년에 21억 달러로 평가되었고, CAGR 4.1%로 성장하여 2034년에는 31억 달러에 이를 것으로 예측됩니다.

이러한 꾸준한 성장은 여러 가지 상호 연관된 요인에 기인합니다. 전 세계적으로 결절성 소양증(PN) 진단을 받는 사람이 증가하고 있으며, PN은 20-60세 사이의 성인에게 주로 발생하는 만성적이고 강한 가려움증을 동반하는 피부 질환입니다. 결절성 소양증은 간, 신장, 신경 질환 등 전신 질환과 연관된 경우가 많아 효과적인 치료법의 필요성이 더욱 커지고 있습니다.

또한, 삶의 질에 심각한 영향을 미치고 장기적인 치료가 필요한 쇠약성 질환이라는 점도 수요를 촉진하고 있습니다. 인지도가 높아짐에 따라 환자와 의료진 모두 증상뿐만 아니라 근본적인 원인을 겨냥한 의료 솔루션을 추구하는 경향이 강해지고 있습니다. 최근 제약사들은 가려움증과 긁는 습관의 악순환을 끊고 만성 피부 염증을 완화하기 위한 치료제 연구개발에 대한 투자를 강화하고 있으며, PN의 근본적인 메커니즘을 표적으로 삼는 혁신적인 생물학적 제제는 기존 치료법에 비해 더 타겟팅되고 지속적인 결과를 가져와 치료의 전망을 점차 바꾸고 있습니다. 치료의 전망을 점차 바꾸고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 21억 달러 |

| 예측 금액 | 31억 달러 |

| CAGR | 4.1% |

민간 투자자와 공공 의료 이니셔티브의 자금 유입은 미래의 발전을 위한 탄탄한 기반이 되고 있습니다. 이러한 자금은 임상시험에서 유망한 결과를 보인 생물학적 제제 기반 치료제를 출시하고 개발할 수 있게 해줍니다. 생물학적 제제는 치료 패러다임에서 점차 선호되는 선택이 되고 있습니다. 이러한 추세는 보다 진보된 치료제가 규제 당국의 승인을 받아 시장에 진입함에 따라 더욱 가속화될 것으로 예측됩니다.

결절성 가려움증 치료제 시장에는 염증, 가려움증, 피부 병변을 관리하기 위한 다양한 약물이 포함되어 있습니다. 여기에는 코르티코스테로이드, 항히스타민제, 완화제, 캡사이신 크림, 생물학적 제제 등이 포함됩니다. 이 중 코르티코스테로이드는 2024년 6억 5,040만 달러로 세계 시장을 이끌었습니다. 코르티코스테로이드가 널리 사용되는 이유는 강력한 항염증 효과, 저렴한 가격 및 접근성 때문입니다. 코르티코스테로이드는 단기 재발과 경증에서 중등도 PN의 장기적인 관리를 위해 1차 선택 약물로 처방되는 경우가 많습니다. 처방약과 일반의약품을 모두 이용할 수 있다는 점도 코르티코스테로이드의 매력으로 작용하여 외래 치료와 자가 관리를 위한 최적의 선택이 되고 있습니다.

국소 치료제는 2024년 시장 점유율의 55.3%를 차지하며 국소적 증상 관리의 역할을 강조했습니다. 국소 치료제는 환부에 직접 바르기 때문에 전신 노출과 부작용을 최소화할 수 있다는 장점이 있습니다. 완화제, 코르티코스테로이드 크림, 캡사이신 기반 제제 등의 제품이 일반적으로 사용되며, 사용의 용이성과 상대적으로 저렴한 가격으로 인해 선호되고 있습니다. 의료 서비스 제공업체와 소매 약국 모두에서 쉽게 구할 수 있다는 점이 지속적인 이점을 강화하고 있습니다.

처방약 부문은 예측 기간 동안 3.8%의 연평균 복합 성장률(CAGR)로 성장하며 괄목할 만한 성장을 보일 것으로 예측됩니다. 이 분야는 의사의 감독 하에 치료 계획을 세우고 면역 억제제, 칼시뉴린 억제제, 생물학적 제제와 같은 고효능 약물의 사용이 증가함에 따라 PN의 심각한 증상으로 병원을 찾는 환자가 증가함에 따라 처방전 전용 의약품에 대한 수요가 증가하고 있습니다. 특히 생물학적 제제는 장기적인 조절이 가능하고 일관된 의학적 모니터링이 필요한 복잡한 환자들을 위해 특별히 설계되었기 때문에 이러한 추세에 기여하고 있습니다.

병원 약국은 2024년 선두를 차지했으며, 2034년에는 16억 달러 규모에 달할 것으로 예측됩니다. 이들 시설은 특히 지속적인 치료를 받고 있거나 중증 PN을 관리하는 환자들을 위해 생물학적 제제 및 주사용 코르티코스테로이드와 같은 특수 치료제를 조제하는 데 중요한 역할을 담당하고 있습니다. 이러한 시설들은 고가의 약품에 대한 합리적인 접근을 가능하게 하는 중앙 집중식 조달 시스템 하에서 운영되는 경우가 많습니다. 또한, 피부과 및 면역학과의 통합은 적절한 치료 모니터링과 용량 준수를 보장하기 때문에 고급 PN 치료제의 주요 유통 채널이 되고 있습니다.

2024년 세계 시장은 북미가 41.3%의 점유율로 선두를 달렸으며, 미국에서만 8억 1,660만 달러에 달했습니다. 이 지역의 발전을 뒷받침하는 것은 잘 정비된 의료 시스템, 높은 진단율, 첨단 치료에 대한 접근성입니다. 더 많은 환자들이 임상에서 평가받고 인식 개선 노력이 확산됨에 따라 첨단 치료법에 대한 수요는 계속 증가하고 있습니다.

경쟁 구도도 변화하고 있습니다. 항히스타민제, 부신피질 스테로이드제 등 전통적인 치료제가 여전히 존재감을 드러내고 있지만, 생물학적 제제의 진입으로 치료 역학이 재편되고 있습니다. 제약사와 바이오텍 기업 모두 질환에 특화된 치료법 개발에 집중하고 있으며, 증상 완화에 그치지 않고 장기적인 전신 치료로 전환하는 추세입니다. 그 결과, 강력한 규제 프레임워크와 상업적 기반이 있는 지역에서는 시장 경쟁이 치열해지고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 향후 시장 동향

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 제품 유형별, 2021년-2034년

- 주요 동향

- 코르티코스테로이드

- 항히스타민제

- 완화제

- 캡사이신 크림

- 생물학적 제제

- 칼시뉴린 억제제

- 면역 억제제

- 기타 제품 유형

제6장 시장 추산·예측 : 투여 경로별, 2021년-2034년

- 주요 동향

- 외용약

- 경구

- 주사제

제7장 시장 추산·예측 : 약 유형별, 2021년-2034년

- 주요 동향

- 처방전

- 시판약

제8장 시장 추산·예측 : 유통 채널별, 2021년-2034년

- 주요 동향

- 병원 약국

- 소매 약국

- 온라인 약국

제9장 시장 추산·예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 개요

- Bayer

- Galderma

- GlaxoSmithKline

- Johnson &Johnson

- Merck

- Pfizer

- Rugby Pharma

- Sanofi

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- Trevi Therapeutics

- VYNE Therapeutics

The Global Prurigo Nodularis Treatment Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 4.1% to reach USD 3.1 billion by 2034. This steady growth stems from various interrelated factors. A rising number of individuals across the globe are being diagnosed with prurigo nodularis (PN), a chronic and intensely itchy skin condition that often develops in adults between the ages of 20 and 60. PN has been increasingly associated with underlying systemic disorders, including liver, kidney, and neurological conditions, which has further driven the need for effective therapies.

What's also driving the demand is the debilitating nature of the disease, which severely affects the quality of life and often demands long-term treatment. As awareness grows, both patients and medical professionals are more inclined to pursue medical solutions that target not only the symptoms but also the root causes of the condition. In recent years, pharmaceutical companies have ramped up investments in the research and development of therapies that aim to break the itch-scratch cycle and mitigate chronic skin inflammation. Innovative biologics targeting the underlying mechanisms of PN are gradually changing the landscape of care, offering more targeted and durable outcomes compared to traditional therapies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 4.1% |

The influx of funding from private investors and public healthcare initiatives has provided a solid foundation for future advancements. These resources are enabling the launch and development of biologic-based treatments that have demonstrated promising results in clinical studies. The availability of new targeted options is shifting prescriber behavior, with biologics gradually becoming a preferred choice in the treatment paradigm. This trend is expected to further accelerate as more advanced therapies gain regulatory approval and enter the market.

The market for prurigo nodularis treatment includes a wide range of medications aimed at managing inflammation, itch, and skin lesions. These include corticosteroids, antihistamines, emollients, capsaicin creams, and biologics. Among these, corticosteroids led the global market in 2024, with a value of USD 650.4 million. Their widespread use can be attributed to their strong anti-inflammatory effects, affordability, and accessibility. Often used as first-line therapy, corticosteroids are prescribed for both short-term flare-ups and long-term management of mild to moderate PN. Their availability in both prescription and over-the-counter formats adds to their appeal, making them a go-to option for outpatient care and self-management.

Topical treatments accounted for 55.3% of the market share in 2024, highlighting their role in localized symptom management. These therapies offer the advantage of targeted application directly to affected skin areas, minimizing systemic exposure and adverse effects. Products such as emollients, corticosteroid creams, and capsaicin-based formulations are commonly used and are favored for their ease of use and relatively low cost. Their accessibility through both healthcare providers and retail pharmacies reinforces their continued dominance.

The prescription drug category is poised for notable growth, expected to expand at a CAGR of 3.8% over the forecast period. This segment is being driven by a shift toward physician-supervised treatment plans and the increasing use of high-efficacy drugs like immunosuppressants, calcineurin inhibitors, and biologics. As more patients seek medical consultation for PN's severe symptoms, the demand for prescription-only therapies is rising. Biologic agents in particular are contributing to this momentum, as they offer long-term control and are specifically designed for complex cases requiring consistent medical oversight.

Hospital pharmacies held a leading position in 2024 and are projected to reach USD 1.6 billion by 2034. These facilities play a crucial role in dispensing specialized therapies such as biologics and injectable corticosteroids, particularly for patients undergoing continuous treatment or managing severe PN. They often operate under centralized procurement systems that allow for streamlined access to high-cost medications. Moreover, their integration with dermatology and immunology departments ensures proper treatment monitoring and dosage adherence, making them a key distribution channel for advanced PN care.

North America led the global market with a 41.3% share in 2024, with the United States alone accounting for USD 816.6 million. Growth in this region is supported by a well-developed healthcare system, high diagnosis rates, and access to cutting-edge treatments. The demand for advanced therapies continues to grow as more patients are evaluated in clinical settings and awareness initiatives gain traction.

The competitive landscape is transforming. While traditional therapies such as antihistamines and corticosteroids continue to have a presence, the entry of biologics has begun to reshape treatment dynamics. Pharmaceutical leaders and biotech firms alike are focused on the development of disease-specific therapies, creating a shift toward long-term, systemic treatments that go beyond symptom relief. As a result, market competition is intensifying in regions with strong regulatory frameworks and commercial infrastructures.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Route of administration

- 2.2.4 Medication type

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of prurigo nodularis

- 3.2.1.2 Growing innovation and approval of medications

- 3.2.1.3 Rising awareness of disease and accessibility to dermatology consultation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of biologic therapies

- 3.2.2.2 Side effects associated with certain drugs

- 3.2.3 Market opportunities

- 3.2.3.1 Increased adoption of patient-centric digital health solutions

- 3.2.3.2 Development of novel biologics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Pipeline analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Corticosteroids

- 5.3 Antihistamines

- 5.4 Emollients

- 5.5 Capsaicin cream

- 5.6 Biologics

- 5.7 Calcineurin inhibitors

- 5.8 Immunosuppressants

- 5.9 Other product types

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Topical

- 6.3 Oral

- 6.4 Injectable

Chapter 7 Market Estimates and Forecast, By Medication Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Prescription

- 7.3 OTC

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bayer

- 10.2 Galderma

- 10.3 GlaxoSmithKline

- 10.4 Johnson & Johnson

- 10.5 Merck

- 10.6 Pfizer

- 10.7 Rugby Pharma

- 10.8 Sanofi

- 10.9 Takeda Pharmaceuticals

- 10.10 Teva Pharmaceutical Industries

- 10.11 Trevi Therapeutics

- 10.12 VYNE Therapeutics