|

시장보고서

상품코드

1773237

아스팔트 유화제 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Bitumen Emulsifiers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

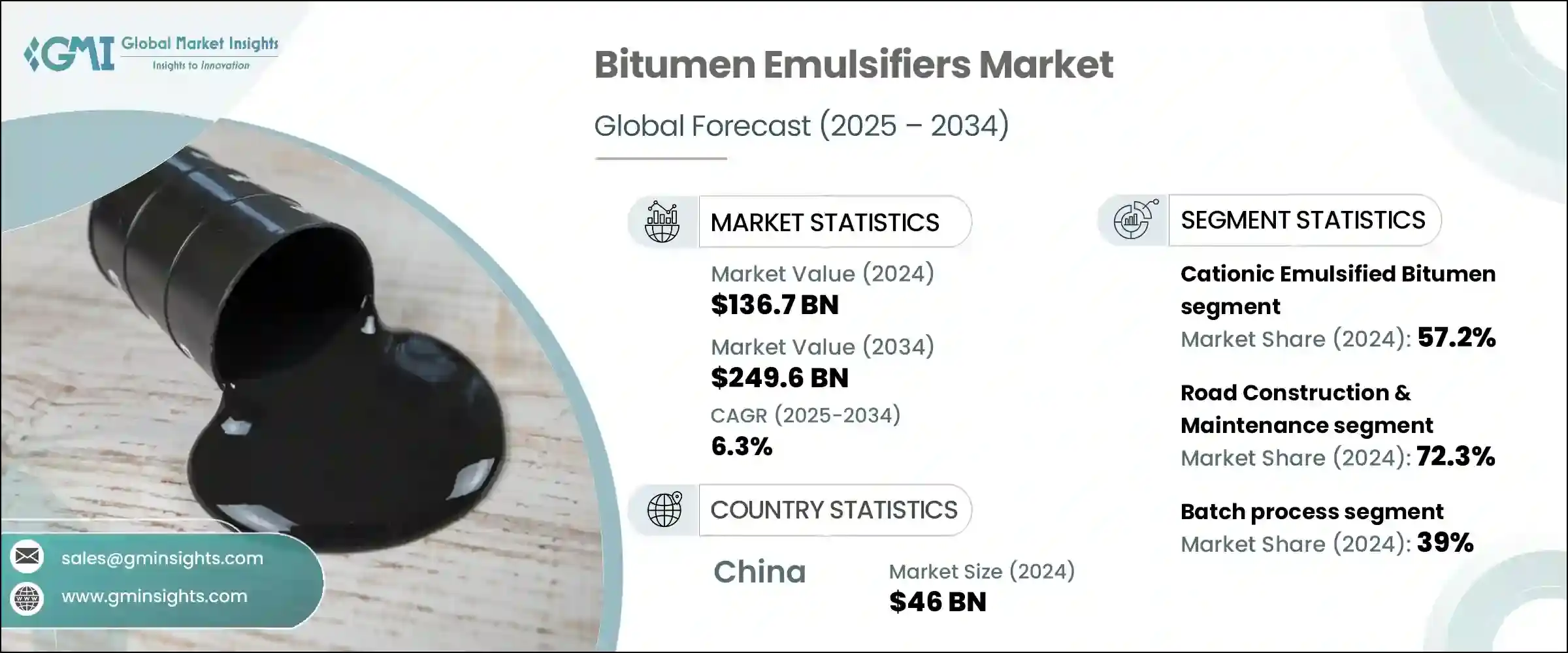

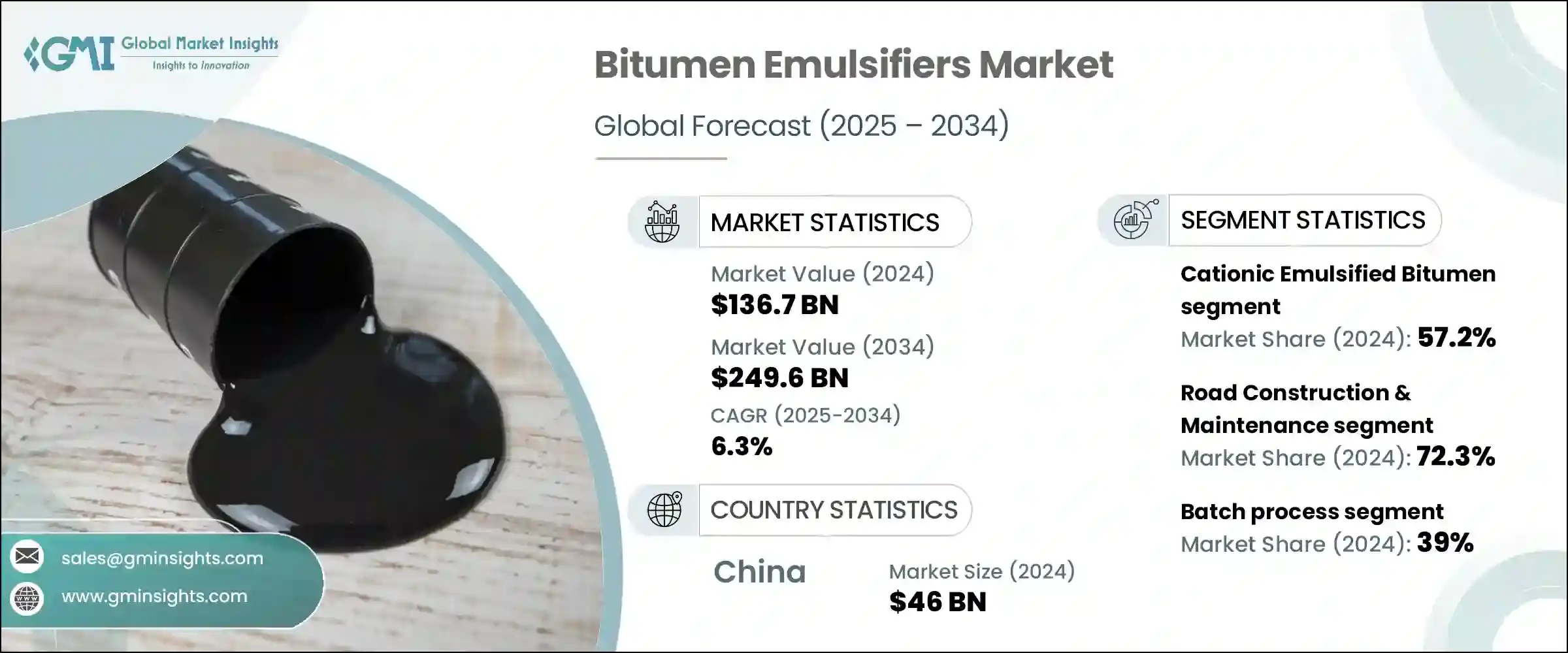

아스팔트 유화제 세계 시장 규모는 2024년에 1,367억 달러로 평가되었고, CAGR 6.3%로 성장하여 2034년에는 2,496억 달러에 이를 것으로 예측됩니다.

이러한 성장의 주요 요인은 인프라에 대한 투자 증가, 특히 까다로운 지형에 대한 정부의 대규모 투자에 기인합니다. 아스팔트 유화제는 추운 지역에서의 사용과 악천후에 대한 강한 내성으로 인해 이러한 프로젝트에 선호되며, 오래 지속되는 도로 건설 및 유지 보수에 이상적입니다. 수성 제제는 탄화수소 배출을 크게 줄이고 가열할 필요가 없기 때문에 전 세계의 엄격한 환경 및 안전 규정을 준수합니다.

이러한 환경 친화적 인 장점으로 인해 특히 탄소 중립과 노동 안전을 우선시하는 지역에서 지속 가능한 건설 관행에서 아스팔트 유화제의 채택이 크게 가속화되고 있습니다. 유화제는 도포 시 고온 가열이 필요하지 않기 때문에 연료 소비와 그에 따른 온실가스 배출을 크게 줄일 수 있습니다. 이러한 에너지 사용량 감소는 그린 인프라와 넷 제로 목표를 향한 전 세계적인 변화에 부합합니다. 또한, 저온 도포의 특성으로 인해 화재 위험과 작업자가 유해 가스에 노출될 위험을 최소화하여 건설 현장의 안전성을 향상시킬 수 있습니다. 북미, 유럽 및 아시아태평양의 정부 및 규제 기관은 공공 인프라 프로젝트에서 저 VOC 및 친환경 소재 사용을 의무화하고 있으며, 기존 아스팔트를 대체할 수 있는 보다 안전하고 깨끗하며 효율적인 소재로서 아스팔트 유화제에 대한 수요가 더욱 증가하고 있습니다. 더욱 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 1,367억 달러 |

| 예측 금액 | 2,496억 달러 |

| CAGR | 6.3% |

양이온성 아스팔트 유화제 분야는 2024년 시장 점유율 57.2%로 압도적인 위치를 차지했으며, 그 주된 이유는 음전하를 띤 골재 표면과의 우수한 접착력에 있습니다. 이러한 우수한 접착력은 교통량이 많고 날씨가 변덕스러운 노면의 내구성과 탄력성을 향상시킵니다. 또한, 양이온 배합은 다재다능하여 산악 지대에서 해안 기후에 이르기까지 다양한 건설 환경에 적합합니다. 다양한 온도와 수분 수준에서 안정적인 성능을 발휘하기 때문에 특히 대규모 도시 개발 및 주요 도로 인프라 프로젝트에서 수요가 지속되고 있습니다.

2024년 도로 건설 및 유지보수 부문은 72.3%의 점유율을 차지했습니다. 아스팔트 유화제는 택코트, 패치 컴파운드, 칩 씰링, 표면 드레싱에 널리 사용되기 때문에 현대의 포장 작업에서 중요한 역할을 합니다. 저온 도포 특성으로 인해 작업상의 위험을 줄이고 저온 조건에서도 시공이 가능하여 에너지 사용량과 프로젝트 지연을 줄일 수 있습니다. 이러한 장점으로 인해 특히 교통량이 많은 도로 및 신속한 복구 공사 등 신설 공사와 일상적인 유지 관리 모두에 이상적인 제품입니다. 또한, 빠른 경화로 인해 도시 지역에서 필수적인 교통 혼잡을 최소화할 수 있습니다.

2024년 중국 아스팔트 유화제 시장 규모는 460억 달러에 달했습니다. 중국에서는 국도, 농촌 도로, 스마트 시티 회랑 등 교통 인프라에 대한 투자가 계속되고 있어 고성능 아스팔트 유화제의 보급에 박차를 가하고 있습니다. 지속 가능한 저배출 건설에 중점을 둔 정부 이니셔티브는 VOC 배출이 적고 에너지 소비가 적은 저온 유화 아스팔트의 환경적 이점과 더욱 일치합니다. 장기적인 전략적 인프라 프로젝트가 시행됨에 따라 환경 친화적이고 내구성이 뛰어난 도로 자재에 대한 수요가 증가하여 시장 성장의 최전선에서 중국의 입지가 더욱 강화될 것으로 보입니다.

아스팔트 유화제 산업에 영향을 미치는 주요 기업은 Ingevity Corporation, Arkema Group, Evonik Industries AG, Nouryon, BASF SE 등입니다. 이들 기업은 지속적인 제품 개발과 시장 개척을 통해 경쟁 환경을 형성하고 있습니다. 아스팔트 유화제 분야의 기업들은 그 입지를 강화하기 위해 기후 및 환경 변화에 대응하는 고도의 배합 연구개발을 우선시하고 있습니다. 또한, 지역 유통망을 확장하고 도로 건설 회사 및 공공 인프라 기관과 전략적 파트너십을 맺고 있습니다. 지속가능성은 핵심 초점으로, 회사는 친환경 저 VOC 유화제에 대한 투자를 늘리고 녹색 건설 의무를 충족하는 솔루션을 추진하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술 및 혁신 상황

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 대처

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 유형별, 2021년-2034년

- 주요 동향

- 양이온계 아스팔트 유화제

- 급속 설정(CRS)

- 중속 설정(CMS)

- 저속 설정(CSS)

- 음이온성 아스팔트 유화제

- 급속 설정(RS)

- 중속 설정(MS)

- 저속 설정(SS)

- 비이온성 아스팔트 유화제

- 변경된 아스팔트 유화제

- 폴리머 개질

- SBS 수정

- SBR 개량

- 기타

- 라텍스 개질

- 기타

- 폴리머 개질

제6장 시장 추산·예측 : 용도별, 2021년-2034년

- 주요 동향

- 도로 건설 및 유지관리

- 표면 드레싱

- 택 코트

- 프라임 코트

- 슬러리 씰

- 마이크로 서페이싱

- 콜드 믹스 아스팔트

- 포그 씰

- 칩 씰

- 방수

- 건축공사

- 인프라

- 포장 재활용

- Full depth reclamation (FDR)

- Cold in-place recycling (CIR)

- Cold central plant recycling (CCPR)

- 기타

- 토양 안정화

- 접착제

- 산업

제7장 시장 추산·예측 : 최종 이용 산업별, 2021년-2034년

- 주요 동향

- 도로 및 고속도로 건설

- 공항 건설

- 건축공사

- 주택용

- 상업용

- 산업용

- 기타

- 철도

- 해양

- 농업

제8장 시장 추산·예측 : 제조 공정별, 2021년-2034년

- 주요 동향

- 배치처리

- 연속 프로세스

- 반연속 프로세스

제9장 시장 추산·예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

제10장 기업 개요

- Alternative Environmental Technologies(AET)

- Arkema Group

- BASF SE

- Bharat Petroleum Corporation Limited(BPCL)

- BTBA

- Dow Chemical Company

- Evonik Industries AG

- GlobeCore

- Hindustan Colas Limited(HINCOL)

- Hindustan Petroleum Corporation Limited(HPCL)

- Ingevity Corporation

- Jey Oil Refining Company

- Kao Corporation

- Marathon Petroleum Asphalt &Emulsions

- Nouryon

- Nynas AB

- Petro Naft

- Pro-Road Global

- Royal Dutch Shell plc

- Tiki Tar Industries

- Total Energies SE

- Winstrol Petrochemicals Pvt. Ltd.

The Global Bitumen Emulsifiers Market was valued at USD 136.7 billion in 2024 and is estimated to grow at a CAGR of 6.3% to reach USD 249.6 billion by 2034. This growth is primarily driven by increased investment in infrastructure, particularly large-scale government initiatives across challenging terrains. Bitumen emulsifiers are preferred for these projects due to their cold application and strong resistance to adverse weather, making them ideal for long-lasting road construction and maintenance. Their water-based formulation significantly reduces hydrocarbon emissions and eliminates the need for heating, aligning well with stricter environmental and safety regulations across global regions.

These eco-friendly benefits have significantly accelerated the adoption of bitumen emulsifiers in sustainable construction practices, particularly in regions prioritizing carbon neutrality and occupational safety. Since emulsifiers eliminate the need for high-temperature heating during application, they drastically lower fuel consumption and associated greenhouse gas emissions. This reduction in energy usage aligns with the global shift toward green infrastructure and net-zero targets. Additionally, their cold-application nature minimizes risks of fire hazards and worker exposure to harmful fumes, enhancing safety on construction sites. Governments and regulatory bodies across North America, Europe, and Asia-Pacific are increasingly mandating the use of low-VOC and environmentally responsible materials in public infrastructure projects, which has further reinforced the demand for bitumen emulsifiers as a safer, cleaner, and more efficient alternative to conventional asphalt.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $136.7 Billion |

| Forecast Value | $249.6 Billion |

| CAGR | 6.3% |

The cationic bitumen emulsifiers segment held the dominant position with a 57.2% market share in 2024, largely attributed to its excellent bonding ability with negatively charged aggregate surfaces. This superior adhesion ensures better durability and resilience of road surfaces under heavy traffic and shifting weather conditions. Cationic formulations also offer versatility, making them highly suitable for a range of construction environments-from mountainous terrains to coastal climates. Their consistent performance under various temperature and moisture levels continues to drive their demand, particularly in large-scale urban development and major roadway infrastructure projects.

The road construction and maintenance segment held a 72.3% share in 2024. Bitumen emulsifiers are critical in modern paving operations as they are widely used in tack coats, patching compounds, chip seals, and surface dressings. Their cold-application properties reduce operational hazards and allow construction even in low-temperature conditions, cutting down on energy usage and project delays. These advantages make them ideal for both new construction and routine maintenance, especially for high-traffic roads and rapid rehabilitation efforts. Their quick-setting nature also minimizes traffic disruptions, which is essential in urban areas.

China Bitumen Emulsifiers Market generated USD 46 billion in 2024. The country's ongoing investments in transportation infrastructure-including national highways, rural roads, and smart city corridors-have fueled the widespread adoption of high-performance bitumen emulsifiers. Government initiatives focused on sustainable, low-emission construction practices further align with the environmental benefits of cold-applied emulsified bitumen, which releases fewer VOCs and requires less energy. With long-term strategic infrastructure projects in place, the demand for eco-friendly, durable road materials is set to increase, reinforcing China's position at the forefront of market growth.

Key players influencing the Bitumen Emulsifiers Industry include Ingevity Corporation, Arkema Group, Evonik Industries AG, Nouryon, and BASF SE. These companies shape the competitive environment through ongoing product development and market expansion. To strengthen their position, companies in the bitumen emulsifiers space are prioritizing R&D for advanced formulations that address varying climatic and environmental demands. They are expanding their regional distribution networks and engaging in strategic partnerships with road construction firms and public infrastructure agencies. Sustainability is a core focus-firms are increasing investment in eco-friendly, low-VOC emulsifiers and promoting solutions that meet green construction mandates.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Manufacturing process

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising infrastructure development

- 3.2.1.2 Environmental benefits & regulations

- 3.2.1.3 Cost-effectiveness

- 3.2.1.4 Technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited temperature range for application

- 3.2.2.2 Storage stability concerns

- 3.2.2.3 Lower strength compared to hot mix asphalt

- 3.2.2.4 Fluctuating crude oil prices

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand in emerging economies

- 3.2.3.2 Increasing focus on sustainable construction

- 3.2.3.3 Development of bio-based emulsifiers

- 3.2.3.4 Rising adoption in cold recycling technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cationic bitumen emulsifiers

- 5.2.1 Rapid setting (CRS)

- 5.2.2 Medium setting (CMS)

- 5.2.3 Slow setting (CSS)

- 5.3 Anionic bitumen emulsifiers

- 5.3.1 Rapid setting (RS)

- 5.3.2 Medium setting (MS)

- 5.3.3 Slow setting (SS)

- 5.4 Non-ionic bitumen emulsifiers

- 5.5 Modified bitumen emulsifiers

- 5.5.1 Polymer modified

- 5.5.1.1 SBS modified

- 5.5.1.2 SBR modified

- 5.5.1.3 Others

- 5.5.2 Latex modified

- 5.5.3 Others

- 5.5.1 Polymer modified

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Road construction & maintenance

- 6.2.1 Surface dressing

- 6.2.2 Tack coat

- 6.2.3 Prime coat

- 6.2.4 Slurry seal

- 6.2.5 Micro surfacing

- 6.2.6 Cold mix asphalt

- 6.2.7 Fog seal

- 6.2.8 Chip seal

- 6.3 Waterproofing

- 6.3.1 Building construction

- 6.3.2 Infrastructure

- 6.4 Pavement recycling

- 6.4.1 Full depth reclamation (FDR)

- 6.4.2 Cold in-place recycling (CIR)

- 6.4.3 Cold central plant recycling (CCPR)

- 6.5 Others

- 6.5.1 Soil stabilization

- 6.5.2 Adhesives

- 6.5.3 Industrial applications

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Road & highway construction

- 7.3 Airport construction

- 7.4 Building construction

- 7.4.1 Residential

- 7.4.2 Commercial

- 7.4.3 Industrial

- 7.5 Others

- 7.5.1 Railways

- 7.5.2 Marine

- 7.5.3 Agriculture

Chapter 8 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Batch process

- 8.3 Continuous process

- 8.4 Semi-continuous process

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Alternative Environmental Technologies (AET)

- 10.2 Arkema Group

- 10.3 BASF SE

- 10.4 Bharat Petroleum Corporation Limited (BPCL)

- 10.5 BTBA

- 10.6 Dow Chemical Company

- 10.7 Evonik Industries AG

- 10.8 GlobeCore

- 10.9 Hindustan Colas Limited (HINCOL)

- 10.10 Hindustan Petroleum Corporation Limited (HPCL)

- 10.11 Ingevity Corporation

- 10.12 Jey Oil Refining Company

- 10.13 Kao Corporation

- 10.14 Marathon Petroleum Asphalt & Emulsions

- 10.15 Nouryon

- 10.16 Nynas AB

- 10.17 Petro Naft

- 10.18 Pro-Road Global

- 10.19 Royal Dutch Shell plc

- 10.20 Tiki Tar Industries

- 10.21 Total Energies SE

- 10.22 Winstrol Petrochemicals Pvt. Ltd.