|

시장보고서

상품코드

1773246

히알루론산 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Hyaluronic Acid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

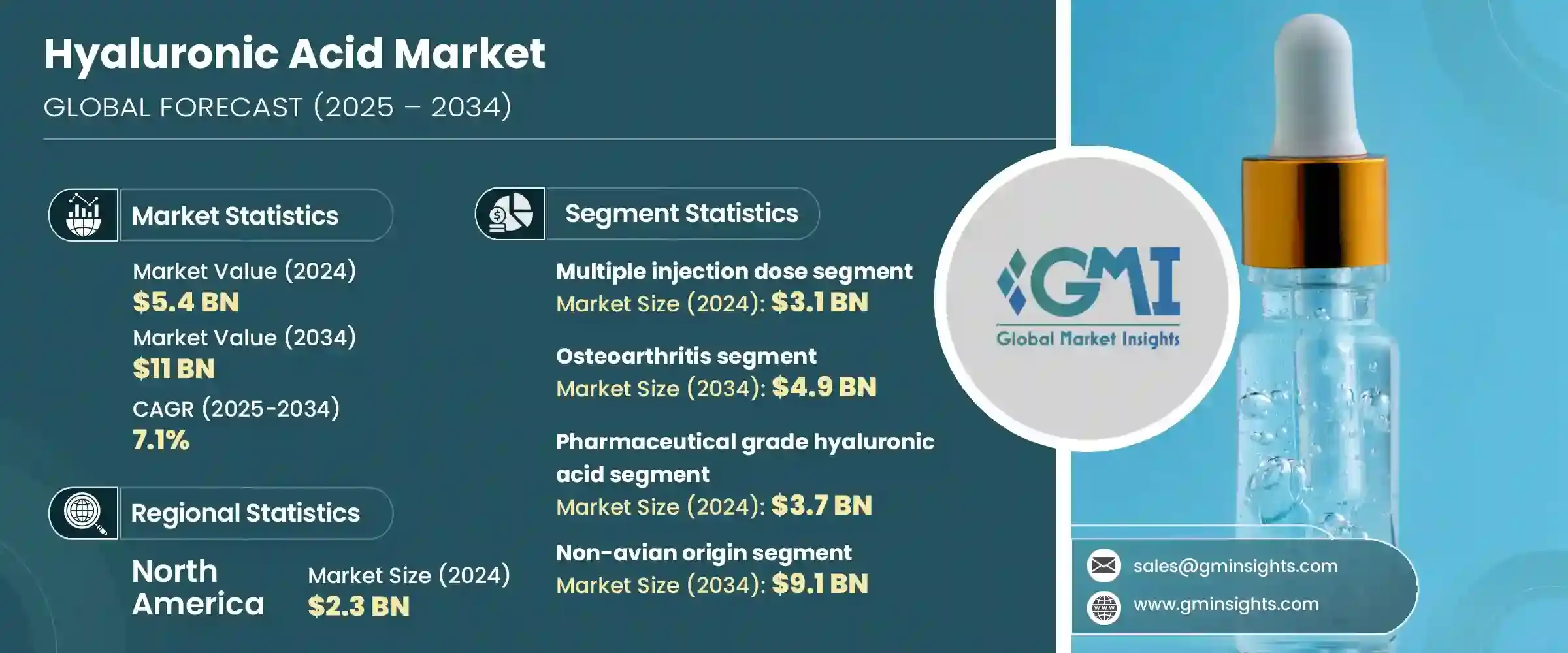

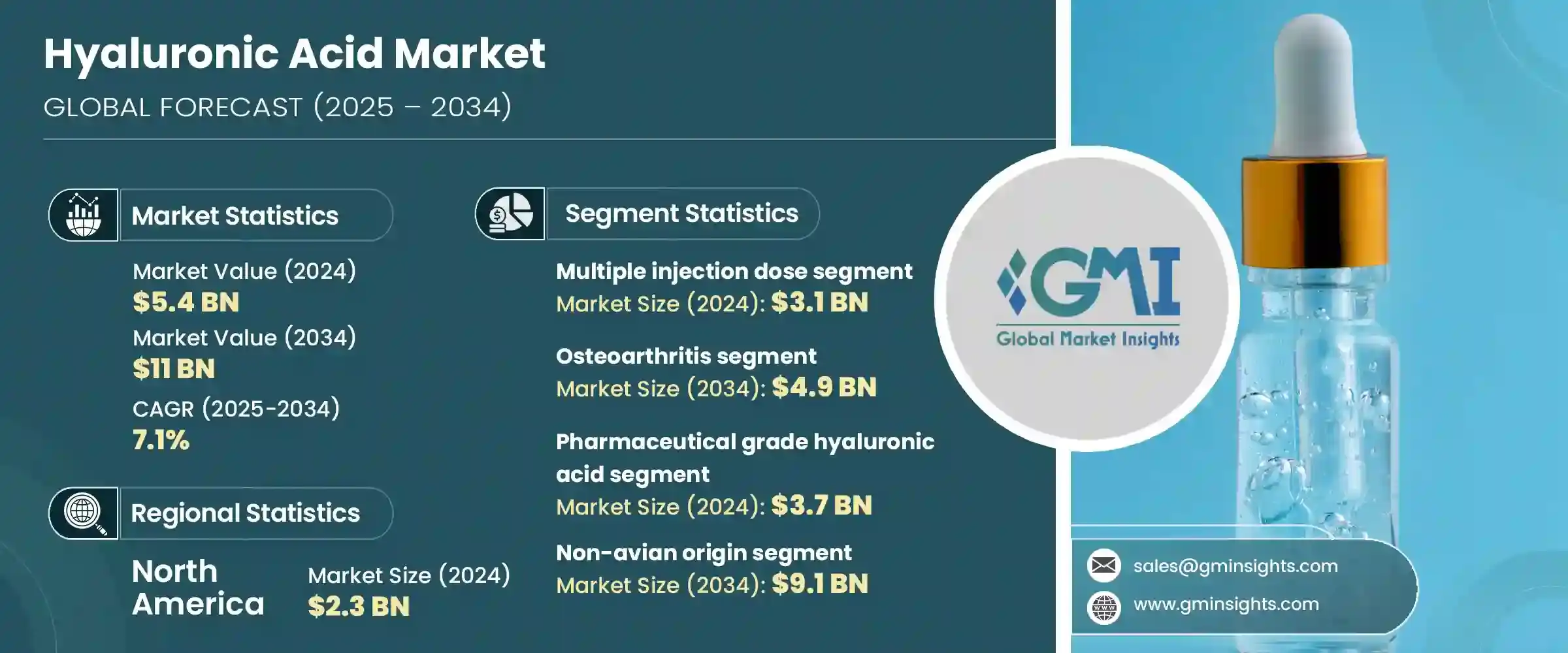

세계의 히알루론산 시장 규모는 2024년에는 54억 달러에 달하며, CAGR 7.1%로 성장하며, 2034년에는 110억 달러에 달할 것으로 예측됩니다.

이러한 상승 추세에 박차를 가하는 주요 요인 중 하나는 의약품 및 화장품 분야에서 히알루론산 기반 제제의 급속한 발전입니다. 외모에 대한 관심 증가, 미용 시술 증가, 최소침습적 치료에 대한 수요 증가는 HA 제품에 대한 비옥한 환경을 조성하고 있습니다. 또한 보다 빠른 결과와 부작용이 적은 치료에 대한 선호도 변화도 눈에 띄게 나타나고 있습니다. 젊은 층은 자기 이미지에 대한 인식이 높아지고 디지털 문화의 영향으로 미용성형에 적극적으로 임하고 있습니다. 동시에 전 세계 고령화로 인해 관절 관련 질환 관리에 있으며, HA에 대한 수요가 증가하고 있습니다.

의료 분야, 특히 정형외과에서는 관절의 뻣뻣함과 통증을 완화하는 방법으로 HA 주사가 널리 사용되고 있습니다. 특히 고관절과 무릎 관절의 골관절염이 증가함에 따라 관절에 직접 HA를 주입하는 기술인 관절내 치환술을 선택하는 환자 수가 증가하고 있습니다. 이 접근법은 관절의 윤활을 회복하고 마찰을 줄이는 데 도움이 되며, 관절 치환술에 대한 덜 침습적인 대안을 제공합니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 54억 달러 |

| 예측 금액 | 110억 달러 |

| CAGR | 7.1% |

환자가 수술을 지연시키거나 피할 수 있는 치료법을 찾는 가운데, 히알루론산 주사에 대한 수요는 지속적으로 증가하고 있으며, HA는 결합조직과 활액에 자연적으로 존재하는 물질이기 때문에 의료용으로 더욱 우위를 점하고, 충격 흡수제 및 윤활유 역할을 하며, 관절의 이동성과 편안함을 향상시키는 역할을 합니다. 또한 그 특성은 상처 치유 제품 및 피부 관리와 같은 외부 용도에도 활용되어 그 상업적 범위가 더욱 다양해졌습니다.

제품 유형에 따라 시장은 다회 주사제와 1회 주사제로 나뉘며, 2024년 세계 시장은 다회 주사제가 31억 달러로 가장 큰 비중을 차지하고 있습니다. 이 유형은 장기간에 걸쳐 관절의 불편함을 감소시키는 효과가 입증되었으므로 골관절염을 관리하는 임상의와 환자들에게 여전히 인기가 있습니다. 일반적으로 치료 프로토콜은 특히 중등도에서 중증의 관절 기능 저하를 경험하는 환자에게 지속적인 완화를 제공하는 주사를 일주일에 한 번씩 연속적으로 투여합니다. 이 제품들은 풍부한 임상 데이터에 의해 지원되며, 일반적으로 보험이 적용되며, 안전성과 효과에 대한 입증된 실적을 바탕으로 지지받고 있습니다.

용도별로 분석하면, 골관절염 분야가 시장을 주도하며 2034년에는 약 49억 달러에 달할 것으로 예측됩니다. 고령화 사회로 인해 관절통이 지속적으로 증가함에 따라 증상을 관리하기 위해 HA를 기반으로 한 솔루션을 찾는 사람들이 증가하고 있습니다. 히알루론산은 기존의 진통제와 내복약이 효과가 제한적일 때 특히 가치가 높습니다. 이러한 주사의 최소 침습성은 관절 기능을 회복하고 외과적 개입의 필요성을 지연시키는 능력과 함께 점점 더 매력적인 선택이 되고 있습니다.

등급별로는 의약품 등급 히알루론산이 2024년 약 37억 달러의 가치로 지배적인 카테고리로 부상했습니다. 이 등급은 분자량 조절, 생체 적합성 강화 등 엄격한 품질 기준으로 인해 높은 인기를 누리고 있습니다. 관절 주사, 안과 수술, 약물전달 시스템 등의 치료에 널리 사용되고 있습니다. 고순도 및 안전성이 높아 주사제로 사용할 수 있으며, 임상 현장에서의 채택이 확대되고 있습니다.

최종사용자의 경우, 병원이 2024년 가장 큰 점유율을 차지하며, 예측 기간 중 꾸준한 수요를 보일 것으로 예측됩니다. 이들 기관은 특히 성형외과, 안과, 성형외과 병동에서 HA 기반 치료법 채택에 있으며, 매우 중요한 역할을 하고 있습니다. 숙련된 의료 서비스 프로바이더의 집중, 지원적인 상환 프레임워크, 명확한 규제는 병원에서 HA 제품 사용을 촉진하는 주요 동력이 되고 있습니다. 의료 행위가 비침습적 또는 저침습적 개입을 점점 더 선호함에 따라 제약 등급 히알루론산에 대한 의존도는 계속 증가하고 있습니다.

미국에서는 2021년 16억 달러에서 2022년 17억 달러로 증가하여 2024년에는 21억 달러에 달합니다. 이러한 성장은 골관절염의 높은 유병률, 미용 시술의 대중화, 관절내 치환술 주사를 보장하는 유리한 보험 정책을 반영하고 있습니다. 인도는 의료 수요와 미용 기술 혁신의 결합으로 인해 HA에 있으며, 가장 성숙한 시장 중 하나로 남아 있습니다.

시장 기업은 제품의 성능과 사용자 편리성의 향상에 주력 하고 있습니다. Allergan Aesthetics, Anika Therapeutics, Ferring Pharmaceuticals, BLOOMAGE, Bioventus를 포함한 주요 기업은 치료 요법 간소화를 위한 1회 투여 옵션을 포함한 첨단 제제에 투자하고 있습니다. 이들 기업은 전 세계 시장 점유율의 40% 이상을 차지하고 있습니다. 주목할 만한 업계 동향은 안전성, 순도, 환자 적합성을 향상시키는 박테리아 발효를 통해 생산된 비아비안 HA에 대한 선호도가 높아지고 있다는 점입니다. 경쟁력을 유지하기 위해 기업은 진화하는 규제에 대응하고, 실제 사용 데이터를 생성하고, 의료진과의 적극적인 소통을 통해 근거에 기반한 제품 채택을 지원해야 합니다.

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 공급업체의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 촉진요인

- 골관절염의 유병률 증가

- 미용 시술 건수의 증가

- 저침습수술의 수요 증가

- HA 기반 제품의 기술적 진보

- 업계의 잠재적 리스크 & 과제

- 높은 치료비

- 잠재적 유해 반응과 부작용

- 기회

- 의료관광의 확대

- E-Commerce와 원격 피부과의 통합

- 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 테크놀러지와 혁신의 상황

- 현재 기술 동향

- 신규 기술

- 제품별 가격 동향

- 향후 시장 동향

- 상환 시나리오

- 소비자 행동 분석

- 갭 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 세계의 기타 지역

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십과 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 제품별, 2021-2034년

- 주요 동향

- 다수 주사 투여

- 단회 주사 용량

제6장 시장 추산·예측 : 용도별, 2021-2034년

- 주요 동향

- 골관절염

- 더말 필러

- 안과

- 방광 요관 역류증

- 기타 용도

제7장 시장 추산·예측 : 등급별, 2021-2034년

- 주요 동향

- 의약품 등급 히알루론산

- 화장품 등급 히알루론산

제8장 시장 추산·예측 : 유래별, 2021-2034년

- 주요 동향

- 비조류 기원

- 조류 기원

제9장 시장 추산·예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 병원

- 피부과 클리닉

- 외래 수술 센터

- 기타 용도

제10장 시장 추산·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제11장 기업 개요

- Allergan Aesthetics

- altergon

- ANIKA

- bioventus

- BLOOMAGE

- FERRING PHARMACEUTICALS

- GALDERMA

- kewpie

- LG Chem

- Lifecore BIOMEDICAL

- Roche

- Sanofi

- SEIKAGAKU CORPORATION

- Teleflex(Deflux)

- TOPSCIENCE

The Global Hyaluronic Acid Market was valued at USD 5.4 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 11 billion by 2034. One of the core factors fueling this upward trend is the rapid development of hyaluronic acid-based formulations across both pharmaceutical and cosmetic domains. The increasing focus on personal appearance, growing uptake of aesthetic procedures, and rising demand for minimally invasive treatments have created a fertile landscape for HA products. There is also a visible shift in public preference towards treatments that offer faster results and fewer side effects. Younger populations are engaging more with cosmetic enhancements, largely influenced by greater self-image awareness and digital culture. At the same time, aging demographics globally are creating a growing need for HA in managing joint-related conditions.

In the medical sector, particularly in orthopedics, HA injections have become a widely accepted method for alleviating joint stiffness and pain. The rising incidence of osteoarthritis-particularly in hips and knees-has increased the number of patients opting for viscosupplementation, a technique where HA is injected directly into the joints. This approach helps restore joint lubrication and reduce friction, offering a less invasive alternative to joint replacement surgeries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.4 Billion |

| Forecast Value | $11 Billion |

| CAGR | 7.1% |

As patients seek treatments that delay or avoid surgery, demand for hyaluronic acid injections is seeing consistent growth. HA's role as a naturally occurring substance in connective tissues and synovial fluids gives it an added edge in medical applications, where it functions as a shock absorber and lubricant, improving joint mobility and comfort. Additionally, its properties are being harnessed in external applications like wound healing products and skincare, further diversifying its commercial reach.

In terms of product segmentation, the market is split into multiple injection dose and single injection dose types. The multiple injection dose segment dominated the global market in 2024, accounting for USD 3.1 billion. This form remains popular among clinicians and patients managing osteoarthritis due to its proven efficacy in reducing joint discomfort over a longer duration. Typically, treatment protocols involve a series of weekly injections that offer sustained relief, especially for those experiencing moderate to severe joint degradation. These products are backed by a wealth of clinical data, are generally covered by insurance, and are favored for their track record of safety and effectiveness.

When analyzed by application, the osteoarthritis segment led the market and is projected to reach approximately USD 4.9 billion by 2034. As joint pain continues to rise among aging populations, more individuals are exploring HA-based solutions to manage symptoms. Hyaluronic acid is especially valued in cases where conventional pain relievers and oral medications provide limited results. The minimally invasive nature of these injections, along with their ability to restore joint function and delay the need for surgical intervention, makes them an increasingly attractive option.

On the basis of grade, pharmaceutical-grade hyaluronic acid emerged as the dominant category, with a valuation of around USD 3.7 billion in 2024. This grade is highly sought-after for its stringent quality standards, including controlled molecular weight and enhanced biocompatibility. It is extensively used in treatments such as joint injections, ocular surgeries, and controlled drug delivery systems. Its high purity and safety profile enable its use in injectable formats, expanding its adoption across clinical settings.

Regarding end users, hospitals accounted for the largest share in 2024 and are expected to continue seeing robust demand over the forecast period. These institutions play a pivotal role in the adoption of HA-based therapies, particularly in orthopedic departments, ophthalmology units, and cosmetic surgery wards. The concentration of skilled healthcare providers, supportive reimbursement frameworks, and regulatory clarity are key drivers for HA product use in hospitals. As medical practices increasingly favor non-invasive or minimally invasive interventions, the reliance on pharmaceutical-grade hyaluronic acid continues to strengthen.

In the United States, the market has shown strong momentum. From USD 1.6 billion in 2021, it rose to USD 1.7 billion in 2022, reaching USD 2.1 billion by 2024. This growth reflects the high prevalence of osteoarthritis, widespread adoption of aesthetic procedures, and favorable insurance policies that cover viscosupplementation injections. The country remains one of the most mature markets for HA, driven by a combination of medical demand and cosmetic innovation.

Market players are focused on improving product performance and user convenience. Key companies, including Allergan Aesthetics, Anika Therapeutics, Ferring Pharmaceuticals, BLOOMAGE, and Bioventus, are channeling investments into advanced formulations, including single-dose options aimed at simplifying treatment regimens. These firms collectively represent over 40% of the global market share. A prominent industry trend is the growing preference for non-avian HA produced via bacterial fermentation, which offers enhanced safety, purity, and patient compatibility. Staying competitive requires companies to align with evolving regulations, generate real-world usage data, and maintain active engagement with healthcare professionals to support evidence-based product adoption.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 Grade

- 2.2.5 Source of origin

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of osteoarthritis

- 3.2.1.2 Rise in number of aesthetic procedures

- 3.2.1.3 Growing demand for minimally invasive procedures

- 3.2.1.4 Technological advancements in HA-based products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Potential adverse reactions and side effects

- 3.2.3 Opportunities

- 3.2.3.1 Expanding medical tourism

- 3.2.3.2 E-commerce and teledermatology integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.9 Consumer behaviour analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Rest of the world

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Multiple injection dose

- 5.3 Single injection dose

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Osteoarthritis

- 6.3 Dermal fillers

- 6.4 Ophthalmic

- 6.5 Vesicoureteral reflux

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By Grade, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pharmaceutical grade hyaluronic acid

- 7.3 Cosmetic grade hyaluronic acid

Chapter 8 Market Estimates and Forecast, By Source of Origin, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Non-Avian origin

- 8.3 Avian origin

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals

- 9.3 Dermatology clinics

- 9.4 Ambulatory surgical centers

- 9.5 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Allergan Aesthetics

- 11.2 altergon

- 11.3 ANIKA

- 11.4 bioventus

- 11.5 BLOOMAGE

- 11.6 FERRING PHARMACEUTICALS

- 11.7 GALDERMA

- 11.8 kewpie

- 11.9 LG Chem

- 11.10 Lifecore BIOMEDICAL

- 11.11 Roche

- 11.12 Sanofi

- 11.13 SEIKAGAKU CORPORATION

- 11.14 Teleflex (Deflux)

- 11.15 TOPSCIENCE