|

시장보고서

상품코드

1773255

전기자동차용 단열재 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Electric Vehicle Insulation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

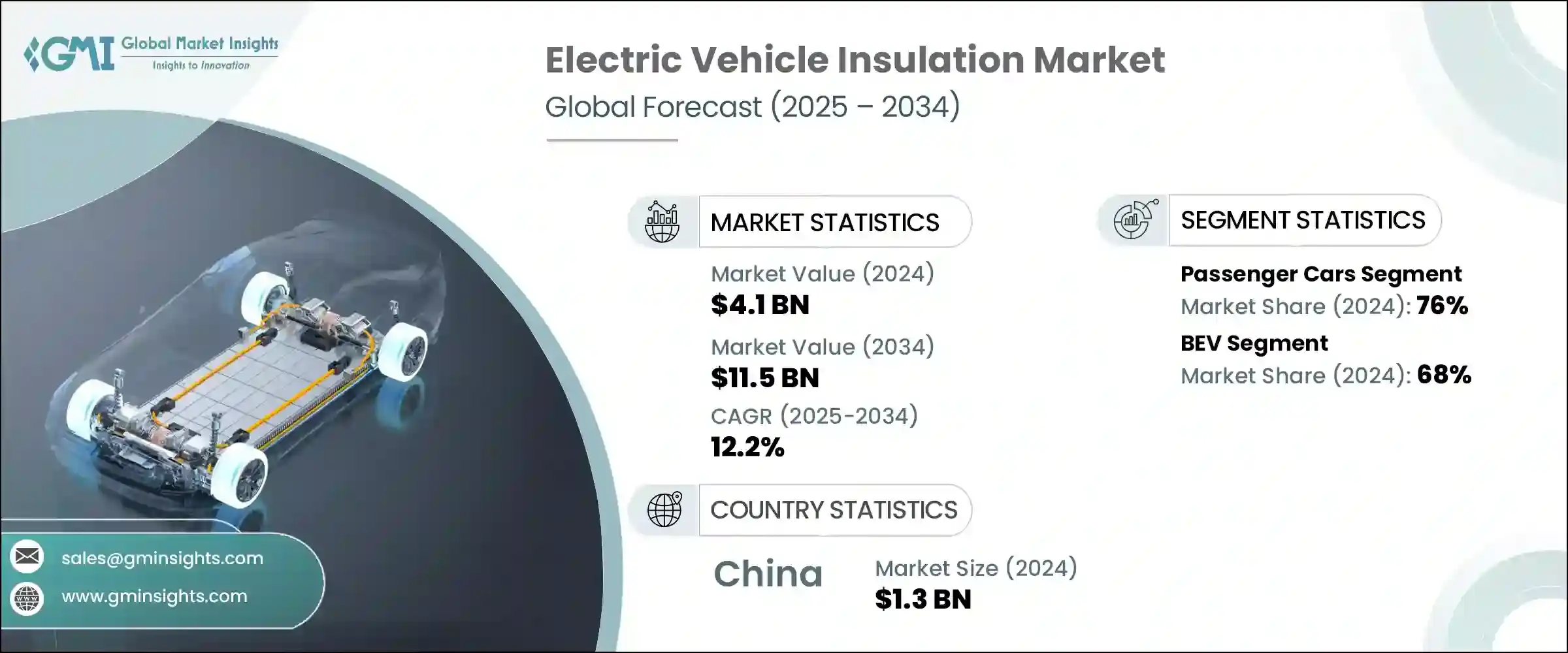

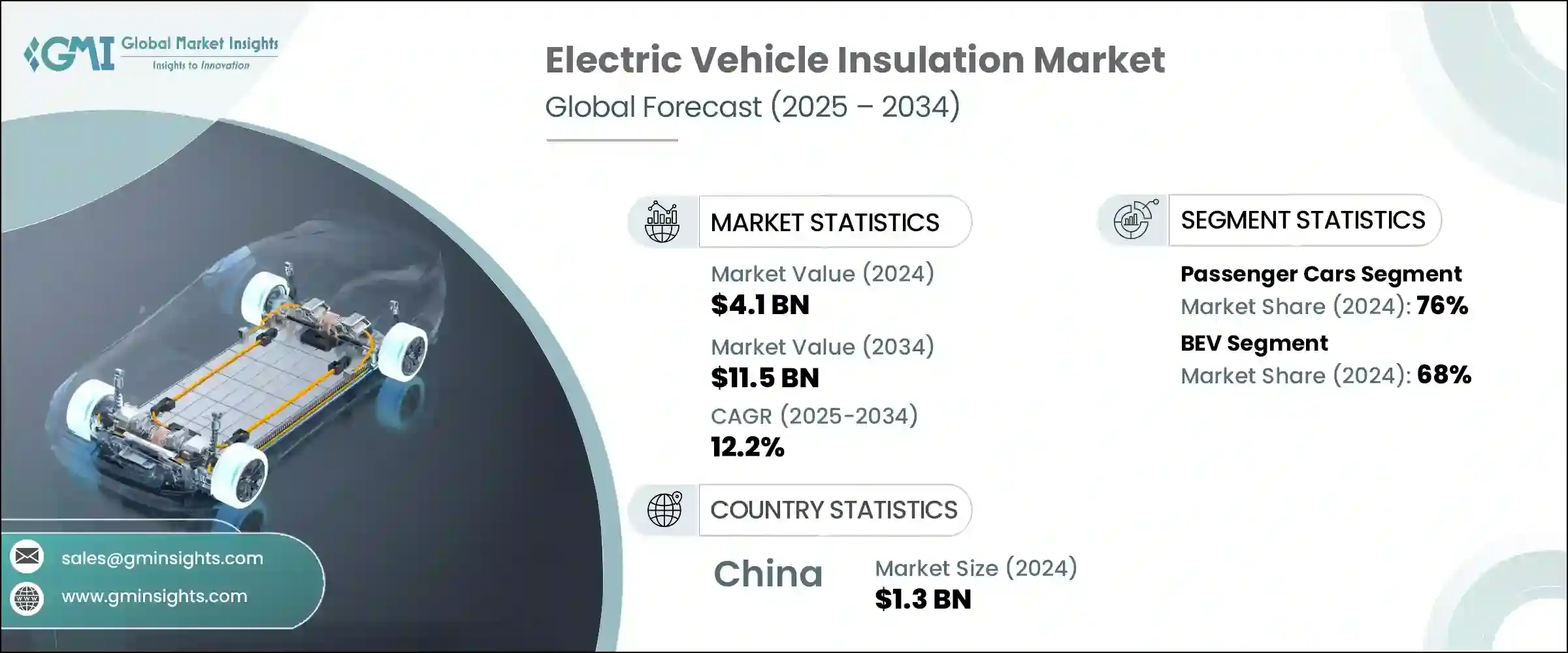

세계의 전기자동차용 단열재 시장은 2024년에 41억 달러로 평가되며, CAGR 12.2%로 성장하며, 2034년에는 115억 달러에 달할 것으로 예측됩니다.

전기 모빌리티로의 전환과 전 세계에서 급속히 확대되고 있는 충전 네트워크는 고급 단열재에 대한 수요에 큰 영향을 미치고 있으며, EV가 주류가 되면서 단열재는 기존 자동차보다 훨씬 더 중심적인 역할을 하고 있습니다. 전기 구동계가 복잡해지고 소형화됨에 따라 높은 열을 견딜 수 있을 뿐만 아니라 고전압 환경에서도 전기적 절연을 유지할 수 있는 소재가 요구되고 있습니다. 배터리 온도 제어에서 전자 부품의 차폐에 이르기까지 절연은 자동차의 효율성, 신뢰성 및 장기적인 안전성을 향상시키는 데 필수적인 요소로 자리 잡았습니다.

특히 제조업체들이 배터리의 고용량화 및 충전 주기의 고속화를 추진함에 따라 열 관리는 EV 엔지니어링의 핵심 우선순위가 되고 있습니다. 이러한 요구사항을 충족시키기 위해 시장에서는 높은 내열성과 경량 설계를 모두 제공하는 소재에 대한 관심이 높아지고 있습니다. 전기 구동계는 종종 최대 800V의 전압으로 작동하므로 절연체는 극한의 열 구배를 견뎌야 할 뿐만 아니라 반복되는 열 사이클에서도 안정적인 성능을 유지해야 합니다. 더 많은 자동차 제조업체들이 주행거리, 내구성 및 운전자 경험을 향상시키기 위해 경쟁하는 가운데, 절연은 단순한 장벽이 아니라 배터리 모듈, 전기 모터 및 전력 전자 장비 전체에 통합된 성능을 달성하기 위해 설계되고 있습니다. 새로운 EV 플랫폼 개발에서 컴팩트한 디자인과 효과적인 열 및 소음 제어의 균형이 점점 더 중요해지고 있으며, 단열재는 자동차 안전 및 성능 기준의 중심에 자리 잡고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 41억 달러 |

| 예측 금액 | 115억 달러 |

| CAGR | 12.2% |

추진력에서 배터리 전기자동차(BEV)는 2024년시장을 주도하여 세계 점유율의 약 68%를 차지할 것으로 예측됩니다. 이 분야는 2025-2034년 13.1% 이상의 CAGR로 성장할 것으로 예상되며, BEV는 전적으로 전력에 의존하므로 모든 고전압 및 열에 민감한 부품에 대한 종합적인 절연의 필요성이 증가하고 있으며, BEV에는 대형 배터리 팩이 장착되어 주행 및 충전 중에 상당한 열을 발생시킵니다. BEV의 절연은 전기장을 절연하고 전자기 간섭을 감소시켜 전기 시스템의 효율성과 안전성을 더욱 향상시키는 역할을 하며, OEM이 더 작고 에너지 밀도가 높은 배터리 구성에 대한 요구가 증가하고 있습니다. 소형 및 고에너지 밀도 배터리 구성을 모색하는 가운데, 절연 솔루션은 긴밀한 통합, 최소 무게, 고성능을 위해 최적화되어 있습니다.

제품별로는 단열재 부문이 2024년 압도적인 점유율을 차지하며, 예측 기간 중도 선두를 유지할 것으로 예측됩니다. 단열재는 중요한 시스템 전체의 온도 균일성을 관리하기 위해 EV에 필수적입니다. 과열의 위험과 에너지 효율 저하로 인해 차량의 안전과 배터리 수명이 모두 손상될 수 있으므로 고성능 단열재가 널리 채택되고 있습니다. 이러한 소재는 현재 열 축적으로부터 배터리를 보호하고, 파워 일렉트로닉스의 최적 성능을 유지하며, 가혹한 주행 조건에서 승객의 안전을 유지하는 데 기본이 되고 있으며, EV 기술이 성숙함에 따라 단열재는 급속 충전 시스템과 점점 더 소형화되는 배터리 어셈블리 증가하는 열 수요를 충족시켜야 합니다. 에 대응해야 합니다.

지역별로는 중국이 2024년 아시아태평양 EV 단열재 시장의 약 68.3%를 차지하여 약 13억 달러의 매출을 창출할 것으로 예측됩니다. 중국은 고도로 발달한 현지 공급망과 EV 기술에 대한 적극적인 투자로 세계 EV 생산의 최전선에 위치하고 있습니다. 중국은 제조 규모와 탄탄한 내수 수요가 결합되어 단열재 기술 혁신과 대량 보급을 주도하는 압도적인 힘이 되고 있습니다. 이 지역의 제조업체들이 생산 능력 확대와 제품 성능 향상에 주력하는 한편, 세계 기업도 내수 및 수출 시장 모두를 지원하기 위해 이 지역에 투자하고 있습니다. 자동차 아키텍처가 진화하고 성능 기준이 강화됨에 따라 모든 유형의 전기자동차를 위한 특수 절연 재료에 대한 수요가 크게 증가할 것으로 예측됩니다.

전기자동차 단열재 시장은 차량 아키텍처의 변화와 에너지 효율과 승객의 편안함에 대한 기대치가 높아짐에 따라 빠르게 변화하고 있으며, EV가 더욱 복잡해짐에 따라 단열 시스템은 단순히 부품을 보호하는 것뿐만 아니라 열을 적극적으로 관리하고, 소음을 줄이고, 밀집된 파워트레인 환경에서 전류를 차단해야 합니다. 열차 환경 내의 전류를 절연해야 합니다. 단열재는 고전압 드라이브 트레인, 모듈식 배터리 시스템, 조용한 실내 환경 등 차세대 EV 기능을 지원하는 데 중요한 역할을 하고 있습니다. 현재 에너지 소비를 개선하고 주행거리를 늘리기 위해 가볍고 내구성이 뛰어난 소재가 개발되고 있습니다. 이러한 솔루션은 EV의 구조 설계에 원활하게 통합될 수 있도록 설계되어 자동차 제조업체가 성능, 안전 및 규제 목표를 달성할 수 있도록 돕고 있습니다. 전 세계에서 전기 이동성이 가속화됨에 따라 단열재는 지속가능하고 효율적인 차량 시스템을 구현하는 데 있으며, 중요한 요소로 자리매김할 것으로 보입니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 어프로치

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 공급업체의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 촉진요인

- 전기자동차 생산 증가

- EV 충전 인프라의 확장

- 재료 기술의 진보

- 정부의 장려책과 투자의 증가

- 업계의 잠재적 리스크 & 과제

- 복잡한 커스터마이즈 요구

- 통합열관리 솔루션과의 경쟁

- 시장 기회

- 배터리 안전성과 방화에 중점을 둔다.

- 경량 소재의 수요 증가

- 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter의 산업 분석

- PESTEL 분석

- 테크놀러지와 혁신의 상황

- 현재 기술 동향

- 신규 기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 허브

- 소비 허브

- 수출과 수입

- 비용 내역 분석

- 특허 분석

- 지속가능성과 환경 측면

- 지속가능 관행

- 폐기물 삭감 전략

- 생산에서의 에너지 효율

- 친환경 구상

- 탄소발자국 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카 항공

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십과 협업

- 신제품 발매

- 확장 계획과 자금조달

제5장 시장 추산·예측 : 차량별, 2021-2034년

- 주요 동향

- 승용차

- 세단

- 해치백

- SUV

- 상용차

- 라이트 듀티

- 미디엄 듀티

- 헤비 듀티

- 이륜차

제6장 시장 추산·예측 : 추진력별, 2021-2034년

- 주요 동향

- 전기자동차

- PHEV

- 하이브리드차

- 연료전지 자동차

제7장 시장 추산·예측 : 제품별, 2021-2034년

- 주요 동향

- 단열재

- 방음

- 전기 절연

- 하이브리드

제8장 시장 추산·예측 : 재료별, 2021-2034년

- 주요 동향

- 열 인터페이스

- 발포 플라스틱

- 세라믹 재료

- 글라스울/유리섬유

- 실리콘 및 고무 기반

- 기타

제9장 시장 추산·예측 : 용도별, 2021-2034년

- 주요 동향

- 배터리 팩과 하우징

- 전기 모터

- 파워 일렉트로닉스

- 객실

- Under the hood/열관리 시스템

- 충전 포트와 시스템

제10장 시장 추산·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제11장 기업 개요

- 3M

- Aerofoam(Hira Industries)

- Armacell International

- Autoneum

- BASF SE

- Covestro AG

- DuPont

- Flex

- ITW Formex

- Johns Manville(Berkshire Hathaway)

- L&L Products

- Morgan Advanced Materials

- Parker Hannifin

- Polymer Technologies

- Rogers Corporation

- Saint-Gobain

- Toray Industries

- UBE Corporation

- Unifrax(Alkegen)

- Zotefoams

The Global Electric Vehicle Insulation Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 12.2% to reach USD 11.5 billion by 2034. The increasing shift toward electric mobility and the global ramp-up of charging networks are significantly influencing the demand for advanced insulation materials. As EVs become more mainstream, insulation is playing a far more central role than in traditional vehicles-it is now critical to managing heat, ensuring electrical integrity, and supporting quieter cabin environments. The growing complexity and compactness of electric drivetrains require materials that not only resist high heat but also maintain electrical separation in high-voltage environments. From controlling battery temperatures to shielding electronic components, insulation is becoming essential in enhancing vehicle efficiency, reliability, and long-term safety.

Thermal management is a core priority in EV engineering, especially as manufacturers push for higher battery capacities and faster charging cycles. To meet these demands, the market is seeing strong interest in materials that offer both high thermal resistance and lightweight design. With electric drivetrains often operating at voltages up to 800V, insulation must not only withstand extreme thermal gradients but also maintain stable performance under repeated thermal cycling. As more automakers compete to improve range, durability, and driver experience, insulation is being engineered not just as a barrier but as a performance enabler integrated across battery modules, electric motors, and power electronics. The development of new EV platforms is increasingly focused on balancing compact design with effective heat and noise control, which places insulation at the center of vehicle safety and performance standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $11.5 Billion |

| CAGR | 12.2% |

In terms of propulsion, Battery Electric Vehicles (BEVs) led the market in 2024, accounting for approximately 68% of the global share. This segment is projected to expand at a CAGR of more than 13.1% from 2025 to 2034. BEVs rely entirely on electric power, which intensifies the need for comprehensive insulation across all high-voltage and thermally sensitive components. Since BEVs contain large battery packs and generate considerable heat during operation and charging, the demand for materials capable of maintaining stable temperatures and preventing energy loss continues to grow. Insulation in BEVs also serves to isolate electric fields and reduce electromagnetic interference, which further improves the efficiency and safety of electric systems. As OEMs explore more compact and high-energy-density battery configurations, insulation solutions are being optimized for tight integration, minimal weight, and high performance.

By product, the thermal insulation segment held the dominant share in 2024 and is expected to maintain its lead through the forecast period. Thermal insulation is essential in EVs to manage temperature uniformity across critical systems. Overheating risks and energy inefficiencies can compromise both vehicle safety and battery life, which has led to widespread adoption of high-performance thermal barriers. These materials are now fundamental to shielding batteries from heat buildup, preserving optimal performance of power electronics, and maintaining passenger safety under extreme operating conditions. As EV technology matures, thermal insulation must keep pace with rising thermal demands from fast-charging systems and increasingly compact battery assemblies.

Regionally, China represented about 68.3% of the Asia-Pacific EV insulation market in 2024, contributing approximately USD 1.3 billion in revenue. The country remains at the forefront of global EV production, with a highly developed local supply chain and aggressive investment in EV technologies. Its scale of manufacturing, combined with strong domestic demand, has made China a dominant force in driving innovation and mass deployment of insulation materials. While regional manufacturers are focused on expanding capacity and improving product performance, global companies are also investing in the region to support both local and export markets. As vehicle architectures evolve and performance standards grow more stringent, the demand for specialized insulation materials across all types of electric vehicles is expected to rise significantly.

The electric vehicle insulation market is transforming rapidly in response to shifting vehicle architectures and rising expectations for energy efficiency and passenger comfort. As EVs grow more complex, insulation systems must do more than just protect components-they must actively manage heat, reduce noise, and isolate electrical currents within tightly packed powertrain environments. Insulation has become instrumental in supporting next-generation EV features, including high-voltage drivetrains, modular battery systems, and quiet cabin experiences. Lightweight, high-durability materials are now being developed to improve energy use and extend driving range. These solutions are designed for seamless integration into the structural design of EVs, helping automakers meet performance, safety, and regulatory targets. With electric mobility accelerating worldwide, insulation will continue to be a key enabler of sustainable and efficient vehicle systems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Product

- 2.2.5 Material

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising electric vehicle production

- 3.2.1.2 Expansion of EV charging infrastructure

- 3.2.1.3 Advancements in material technology

- 3.2.1.4 Rising government incentives and investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex customization needs

- 3.2.2.2 Competition from integrated thermal management solutions

- 3.2.3 Market opportunities

- 3.2.3.1 Focus on battery safety and fire protection

- 3.2.3.2 Rising demand for light weight materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

- 5.4 Two-wheelers

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 BEV

- 6.3 PHEV

- 6.4 HEV

- 6.5 FCEV

Chapter 7 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Thermal insulation

- 7.3 Acoustic insulation

- 7.4 Electric insulation

- 7.5 Hybrid

Chapter 8 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Thermal interface

- 8.3 Foamed plastics

- 8.4 Ceramic materials

- 8.5 Glass wool/Fiberglass

- 8.6 Silicon and Rubber-based

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Battery pack and housing

- 9.3 Electric motor

- 9.4 Power electronics

- 9.5 Passenger cabin

- 9.6 Under the hood/thermal management system

- 9.7 Charging port & system

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 3M

- 11.2 Aerofoam (Hira Industries)

- 11.3 Armacell International

- 11.4 Autoneum

- 11.5 BASF SE

- 11.6 Covestro AG

- 11.7 DuPont

- 11.8 Flex

- 11.9 ITW Formex

- 11.10 Johns Manville (Berkshire Hathaway)

- 11.11 L&L Products

- 11.12 Morgan Advanced Materials

- 11.13 Parker Hannifin

- 11.14 Polymer Technologies

- 11.15 Rogers Corporation

- 11.16 Saint-Gobain

- 11.17 Toray Industries

- 11.18 UBE Corporation

- 11.19 Unifrax (Alkegen)

- 11.20 Zotefoams