|

시장보고서

상품코드

1773336

가황 고체 고무 시장(2025-2034년) : 기회와 촉진요인, 업계 동향 분석, 예측Vulcanised Solid Rubber Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

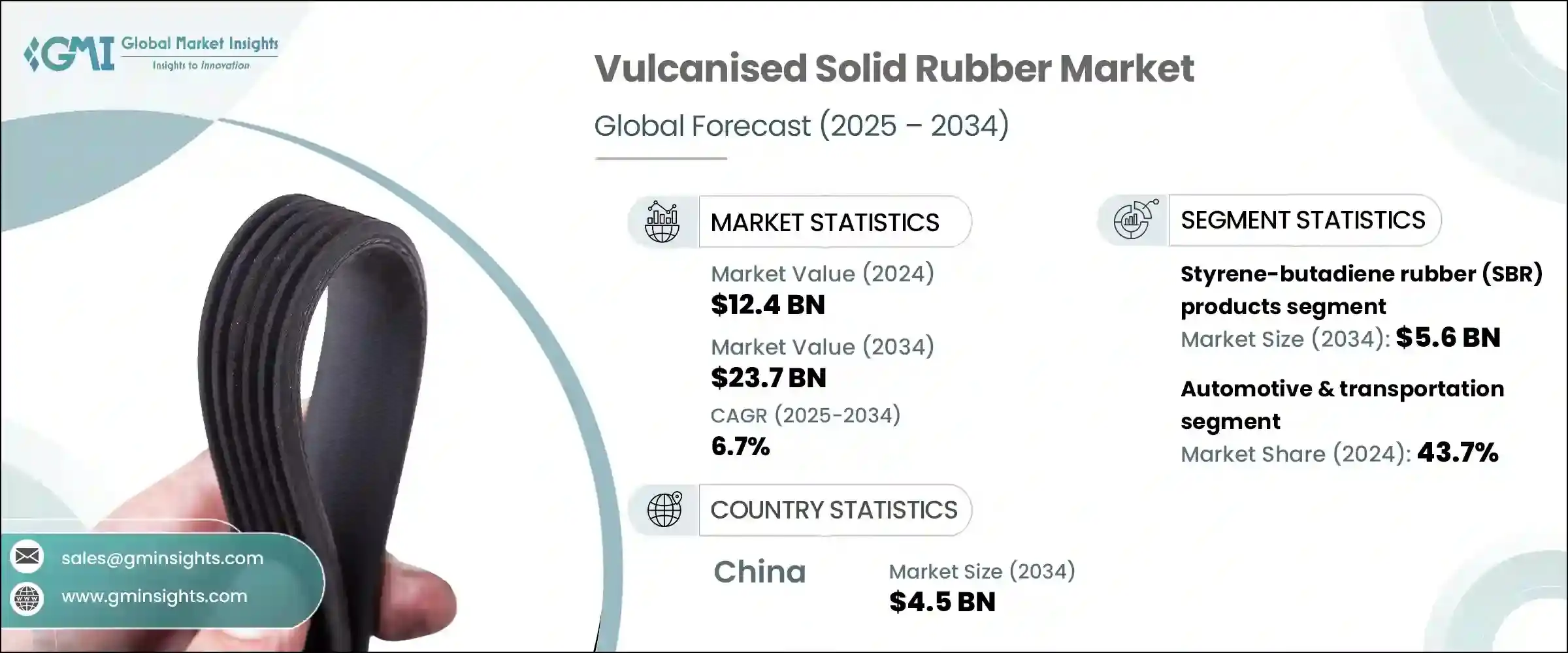

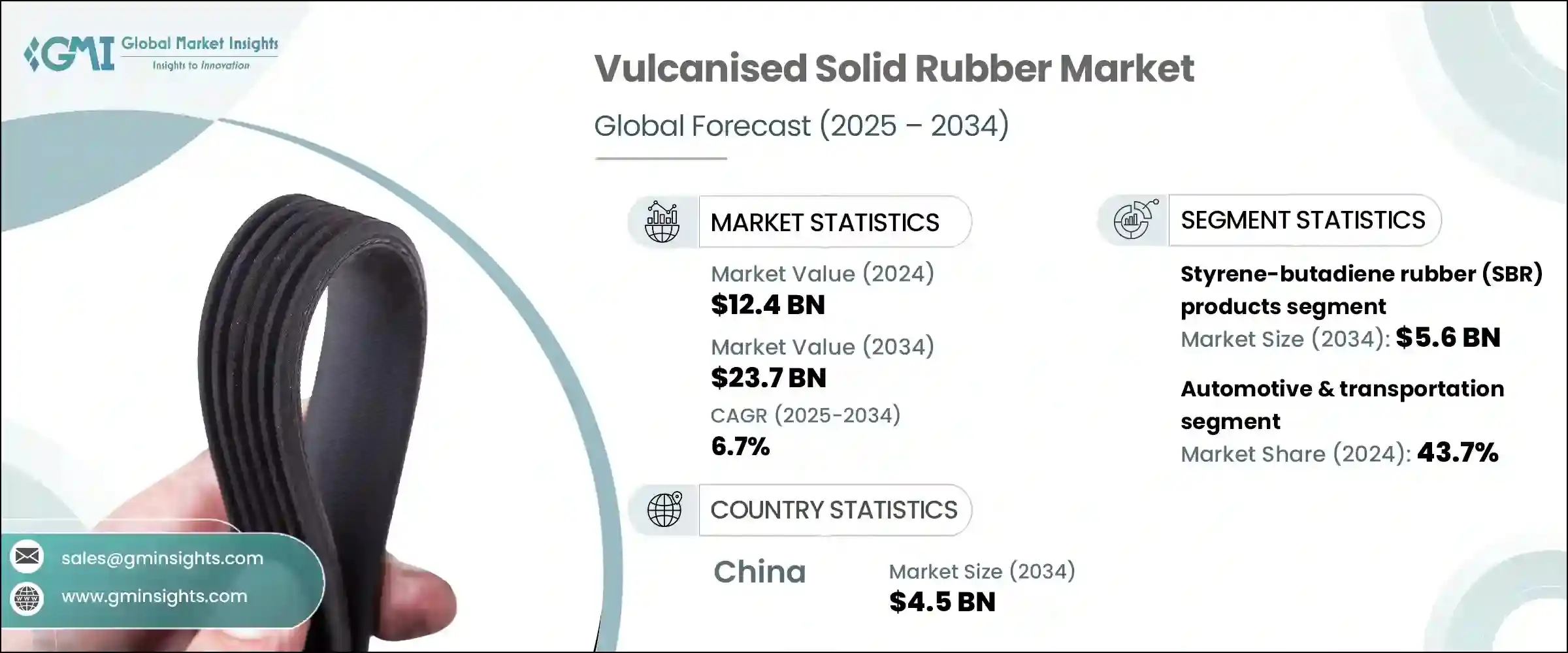

세계의 가황 고체 고무 시장 규모는 2024년에 124억 달러에 달하였고, CAGR 6.7%로 성장하여 2034년에는 237억 달러에 이를 것으로 예측되고 있습니다.

이러한 증가 추세는 특히 유럽과 같은 선진국 및 중국과 같은 경제가 급속히 발전하고 있는 지역에서 자동차산업과 건설산업 전반에 걸친 소비 증가로 크게 뒷받침되고 있습니다. 가황 고체 고무는 뛰어난 내후성, 높은 내구성, 탄력성으로 인해 다양한 산업분야에 필수적인 재료로 계속 지지를 받고 있습니다. 가황 고체 고무는 씰링, 진동 감쇠, 보호 패딩, 내구성있는 바닥재 시스템 등에 필요한 특성으로 인해 세계 산업에서 점점 신뢰받고 있습니다. 또한 기계적 스트레스가 높고 다양한 환경 요인에 노출되는 환경에서도 우수한 성능을 발휘하므로 성숙 시장과 신흥시장 모두에서 안정적인 수요가 있습니다.

온도 변화를 견디고 신뢰성이 높은 단열성을 발휘하는 이 소재는 긴 수명과 탄력성을 필요로 하는 제조 환경에서 선호되는 옵션이 되고 있습니다. 아시아 등지에서는 인프라 프로젝트에 대한 지출이 증가하면서 장기적인 효율성을 제공하는 산업용 고무 솔루션에 주목하는 프로젝트가 늘고 있습니다. 그리고 방음, 방진, 온도 관리 능력의 강화를 실현하는 소재에 대한 수요가 더욱 높아질 것으로 예측됩니다. 이러한 요구의 진화에 의해 공급자는 보다 지속 가능하고, 성능이 뛰어나며, 용도에 특화한 차세대 고무 배합 기술을 제공하면서 시장의 기세를 한층 더 가속시키고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작금액 | 124억 달러 |

| 예측금액 | 237억 달러 |

| CAGR | 6.7% |

제품 유형별로는 스티렌 부타디엔 고무(SBR)가 계속 세계 시장을 독점하고 있습니다. 내마모성과 시간에 따른 안정성에 의해 가스켓, 씰, 벨트, 공업용 패드등의 부품에 매우 적합합니다. 또한, 이 소재는 천연고무와 조화를 이루므로 자동차, 신발류, 건축 등 다양한 산업에서 뛰어난 적응성을 가지고 있습니다.

용도별로 분류하면, 2024년 세계의 가황 고체 고무 시장에서는 자동차 및 운수 부문이 43.7%의 수익 기여로 최대의 점유율을 차지하였습니다. 이러한 성장은 내응력과 내구성이 요구되는 자동차 부품에 가황 고무 부품이 폭넓게 사용되고 있는 것에 의해 발생하고 있습니다. 가황 고체 고무는 소음 방지 시스템 등에 적합합니다. 전기자동차가 기세를 늘리는 가운데, 소음, 진동, 불쾌감(NVH) 저감 시스템 등, 비구조적이면서 중요한 부품이 고무에 의존하는 현상은 업계에서 점점 더 두드러지고 있습니다. EV의 실내 정숙성 및 단열에 대한 요구는 고무 배합의 기술 혁신에 박차를 가해 새로운 모빌리티 플랫폼 전체에 그 관련성을 넓혀가고 있습니다.

지역별로는 중국이 주요 공헌국으로 부상하면서 2024년에는 23억 달러의 매출을 올렸고, 2034년에는 CAGR 6.9%의 성장률로 45억 달러에 이를 것으로 예측됩니다. 중국은 고무 컴파운드를 개발하는 노력을 강화하고 있습니다. 기술적 자립과 진보를 중시하는 중국은 부가가치가 높은 고무 제품의 채용을 촉진해, 국제 무대에서의 경쟁력을 높이고 있습니다. 또한, 국내 소비는 꾸준히 증가하고 있어 내수 시장을 지지하며 장기적인 성장 기회를 가져오고 있습니다.

세계의 가황 고체 고무 업계는 여전히 고도로 통합되어 있으며, 주요 기업 5개사가 시장 전체의 40% 이상의 점유율을 차지하고 있습니다. 각사는 까다로운 조건 하에서도 긴 라이프사이클에 견딜 수 있는 고도의 고무 컴파운드를 개발하기 위해 연구개발에 많은 투자를 하고 있습니다.

목차

제1장 조사방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품 유형별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(주 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속 가능성과 환경 측면

- 지속 가능한 실천

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경친화적인 노력

- 탄소발자국의 고려

제4장 경쟁구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 천연고무(NR) 제품

- 스티렌 부타디엔 고무(SBR) 제품

- 부타디엔 고무(BR) 제품

- 에틸렌 프로파일렌 디엔 단량체(EPDM) 제품

- 니트릴 고무(NBR) 제품

- 클로로프렌 고무(CR) 제품

- 실리콘 고무 제품

- 기타 특수 고무 제품

제6장 시장 추계 및 예측 : 경도별(2021-2034년)

- 주요 동향

- 연질(쇼어 A 30-50)

- 중질(쇼어 A 50-70)

- 경질(쇼어 A 70-90)

- 초경질(쇼어 A 90 이상)

제7장 시장 추계 및 예측 : 제조 공정별(2021-2034년)

- 주요 동향

- 압축 성형

- 트랜스퍼 성형

- 사출 성형

- 압출

- 캘린더 가공

- 기타

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 자동차 및 운송

- 타이어와 타이어 부품

- 씰과 개스킷

- 진동 아이솔레이터와 마운트

- 호스와 벨트

- 기타 자동차 부품

- 산업기계 및 장비

- 산업용 씰과 개스킷

- 컨베이어 벨트와 부품

- 롤러와 휠

- 진동 절연 시스템

- 기타 산업용도

- 건설 및 인프라

- 교량 지승과 신축 조인트

- 면진 시스템

- 방수 및 씰링 제품

- 바닥재 및 포장재

- 기타 건설용도

- 전기 및 전자공학

- 절연재 및 케이블 부품

- 커넥터와 씰

- 기타 전기용도

- 헬스케어 및 의료기기

- 의료용 튜브 및 부품

- 스토퍼와 씰

- 기타 의료 용도

- 소비재

- 신발 부품

- 스포츠 용품

- 가정용품

- 기타 소비자용 용도

- 기타

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Arlanxeo

- Bridgestone Corporation

- Continental AG

- Dow Inc.

- ExxonMobil Corporation

- Freudenberg Group

- Gates Corporation

- Goodyear Tire &Rubber Company

- JSR Corporation

- Kumho Petrochemical

- LANXESS AG

- Michelin

- Momentive Performance Materials Inc.

- NOK Corporation

- Parker Hannifin Corporation

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Rubber Industries, Ltd.

- Trelleborg AB

- Wacker Chemie AG

- Zeon Corporation

The Global Vulcanised Solid Rubber Market was valued at USD 12.4 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 23.7 billion by 2034. This upward trend is largely fueled by rising consumption across the automotive and construction industries, particularly in well-established regions like Europe and rapidly advancing economies such as China. Vulcanised solid rubber continues to gain traction due to its impressive resistance to weathering, high durability, and elasticity, making it an essential material in a wide variety of industrial applications. Industries across the globe increasingly rely on it for its performance in sealing, vibration dampening, protective padding, and durable flooring systems. Its robust performance under high mechanical stress and exposure to various environmental factors ensures consistent demand across both mature and emerging industrial markets.

The material's ability to withstand temperature fluctuations and provide reliable insulation positions it as a preferred choice in manufacturing environments that require longevity and resilience. As infrastructure spending rebounds globally, especially across Southeast Asia and parts of the Middle East, more projects are turning to industrial-grade rubber solutions for long-term efficiency. Meanwhile, the ongoing transformation of the automotive sector-particularly the shift toward electric and hybrid mobility-is expected to further strengthen demand for materials that deliver noise insulation, vibration control, and enhanced thermal management. As a result, vulcanized solid rubber is increasingly being adopted in advanced vehicle designs, supporting a surge in innovation and component integration within the industry. These evolving requirements are prompting suppliers to adapt by offering next-generation rubber formulations that are more sustainable, performance-oriented, and application-specific, further driving the market's momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.4 Billion |

| Forecast Value | $23.7 Billion |

| CAGR | 6.7% |

In terms of product types, styrene-butadiene rubber (SBR) continues to dominate the global market landscape. This segment generated a revenue of USD 2.9 billion in 2024 and is forecasted to grow to USD 5.6 billion by 2034, registering a CAGR of 6.9% over the period. SBR's popularity is driven by its cost-efficiency and exceptional mechanical performance, especially in high-friction and wear-intensive applications. Its abrasion resistance and aging stability make it highly suitable for use in components such as gaskets, seals, belts, and industrial pads. Additionally, the material blends well with natural rubber, improving its adaptability across different industries like automotive, footwear, and construction. This compatibility not only enhances its physical properties but also broadens its range of use cases, reinforcing its dominance in the market.

When segmented by application, the automotive and transportation sector accounted for the largest share of the global vulcanized solid rubber market in 2024, with a revenue contribution of 43.7%. The sector's leadership is underpinned by the broad use of vulcanized rubber parts in vehicle components that demand heat resistance, oil tolerance, and stress durability. These characteristics make the material well-suited for use in engine mounts, underbody shields, floor liners, and noise-control systems. With electric vehicles gaining momentum, the industry's reliance on rubber for non-structural yet critical components such as noise, vibration, and harshness (NVH) reduction systems is becoming more pronounced. The need for quieter cabins and thermal insulation in EVs is fueling innovation in rubber formulations and expanding their relevance across new mobility platforms.

Regionally, China emerged as a leading contributor, generating USD 2.3 billion in revenue in 2024 and is expected to reach USD 4.5 billion by 2034, growing at a CAGR of 6.9%. The country's strong position is supported by its massive production capacity and ongoing shift towards innovation-led manufacturing. Despite rising raw material costs, local producers are ramping up efforts to develop high-performance rubber compounds that meet the quality expectations of global markets. China's emphasis on self-reliance and technological advancement is fostering greater adoption of value-added rubber products, enhancing its competitiveness on the international stage. Additionally, domestic consumption continues to rise steadily, supporting internal demand and driving long-term growth opportunities.

The global vulcanized solid rubber industry remains highly consolidated, with the top five market players accounting for over 40% of the total share. These companies maintain a competitive edge through vertical integration, comprehensive product offerings, and expansive manufacturing networks. Leading players are investing heavily in research and development to engineer advanced rubber compounds that are bio-based, low in volatile organic compounds (VOCs), and capable of withstanding longer life cycles under demanding conditions. Strategic acquisitions are also playing a significant role in shaping the market, with major companies expanding their footprint through targeted takeovers of niche compounders and joint ventures with regional producers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only )

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Tons)

- 5.1 Key trends

- 5.2 Natural rubber (NR) products

- 5.3 Styrene-butadiene rubber (SBR) products

- 5.4 Butadiene rubber (BR) products

- 5.5 Ethylene propylene diene monomer (EPDM) products

- 5.6 Nitrile rubber (NBR) products

- 5.7 Chloroprene rubber (CR) products

- 5.8 Silicone rubber products

- 5.9 Other specialty rubber products

Chapter 6 Market Estimates and Forecast, By Hardness Grade, 2021 - 2034 (USD Billion) (Tons)

- 6.1 Key trends

- 6.2 Soft (shore a 30-50)

- 6.3 Medium (shore a 50-70)

- 6.4 Hard (shore a 70-90)

- 6.5 Extra hard (shore a 90+)

Chapter 7 Market Estimates and Forecast, By Manufacturing Process, 2021 - 2034 (USD Billion) (Tons)

- 7.1 Key trends

- 7.2 Compression molding

- 7.3 Transfer molding

- 7.4 Injection molding

- 7.5 Extrusion

- 7.6 Calendering

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Tons)

- 8.1 Key trends

- 8.2 Automotive & transportation

- 8.2.1 Tires & tire components

- 8.2.2 Seals & gaskets

- 8.2.3 Vibration isolators & mounts

- 8.2.4 Hoses & belts

- 8.2.5 Other automotive components

- 8.3 Industrial machinery & equipment

- 8.3.1 Industrial seals & gaskets

- 8.3.2 Conveyor belts & components

- 8.3.3 Rollers & wheels

- 8.3.4 Vibration isolation systems

- 8.3.5 Other industrial applications

- 8.4 Construction & infrastructure

- 8.4.1 Bridge bearings & expansion joints

- 8.4.2 Seismic isolation systems

- 8.4.3 Waterproofing & sealing products

- 8.4.4 Flooring & paving materials

- 8.4.5 Other construction applications

- 8.5 Electrical & electronics

- 8.5.1 Insulation & cable components

- 8.5.2 Connectors & seals

- 8.5.3 Other electrical applications

- 8.6 Healthcare & medical devices

- 8.6.1 Medical tubing & components

- 8.6.2 Stoppers & seals

- 8.6.3 Other medical applications

- 8.7 Consumer goods

- 8.7.1 Footwear components

- 8.7.2 Sporting goods

- 8.7.3 Household products

- 8.7.4 Other consumer applications

- 8.8 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arlanxeo

- 10.2 Bridgestone Corporation

- 10.3 Continental AG

- 10.4 Dow Inc.

- 10.5 ExxonMobil Corporation

- 10.6 Freudenberg Group

- 10.7 Gates Corporation

- 10.8 Goodyear Tire & Rubber Company

- 10.9 JSR Corporation

- 10.10 Kumho Petrochemical

- 10.11 LANXESS AG

- 10.12 Michelin

- 10.13 Momentive Performance Materials Inc.

- 10.14 NOK Corporation

- 10.15 Parker Hannifin Corporation

- 10.16 Shin-Etsu Chemical Co., Ltd.

- 10.17 Sumitomo Rubber Industries, Ltd.

- 10.18 Trelleborg AB

- 10.19 Wacker Chemie AG

- 10.20 Zeon Corporation