|

시장보고서

상품코드

1773346

강화우유 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Fortified Milk Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

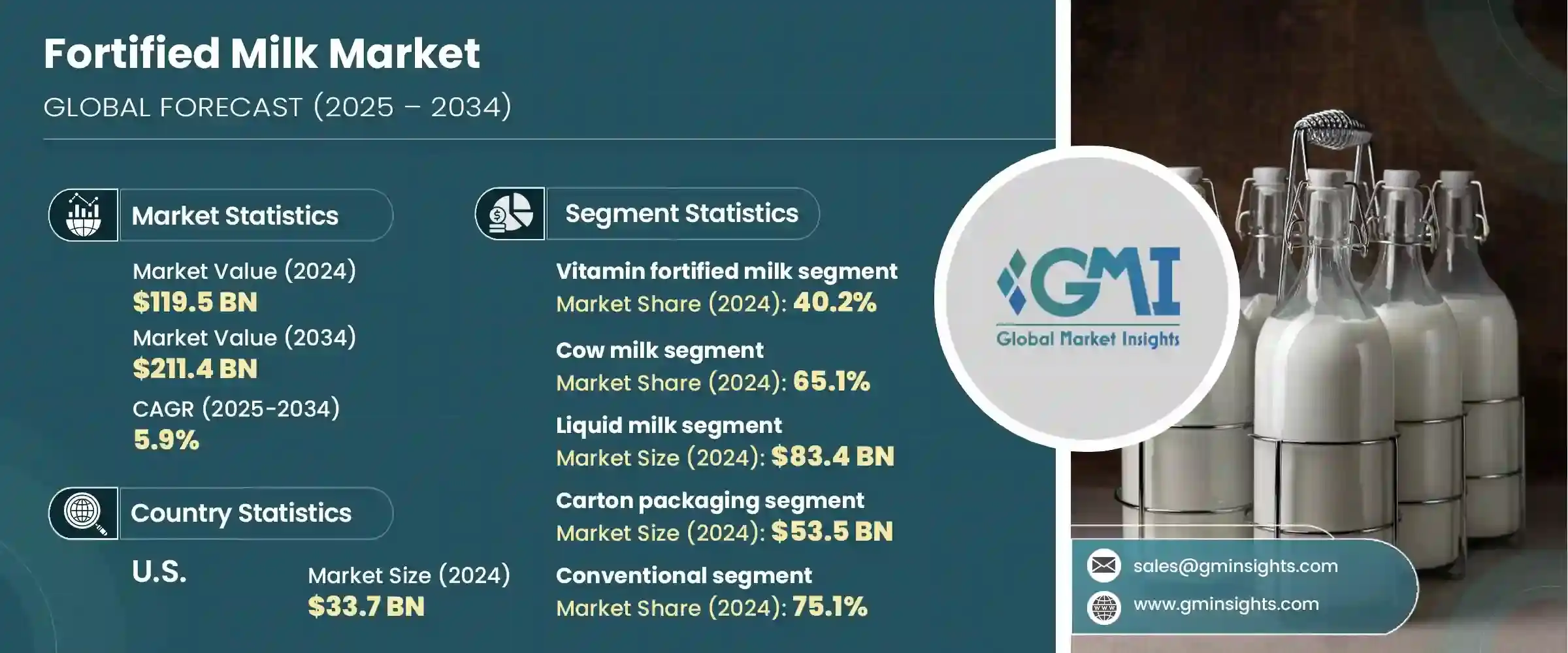

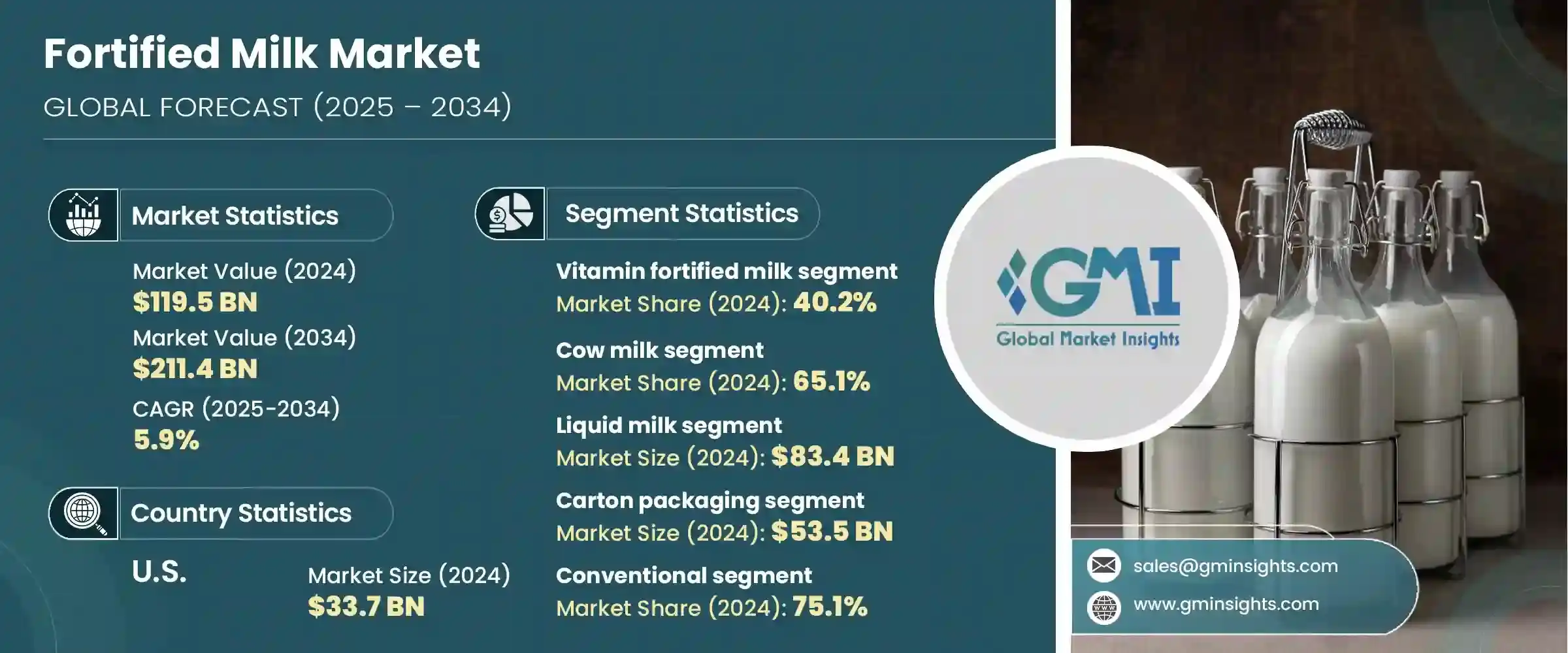

세계의 강화우유 시장은 2024년 1,195억 달러에 달하였고, CAGR 5.9%로 성장하여 2034년에는 2,114억 달러에 이를 것으로 추정되고 있습니다. 소비자들 사이에서는 강화된 유제품에 대한 선호도가 높아지고 있습니다. 이러한 강화 제품은 뼈의 건강, 면역 기능, 인지 기능의 개발을 돕습니다.

도시화의 진전, 가처분 소득 증가, 공중위생 이니셔티브가 추진하는 식품 강화의 대처 또한 특히 아프리카와 아시아의 신흥 경제 국가를 중심으로 시장을 전진시키고 있습니다. 강화우유는 다양한 식생활에 대한 접근이 제한되어 있는 지역에서 실용적인 해결책을 제공합니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작금액 | 1,195억 달러 |

| 예측금액 | 2,114억 달러 |

| CAGR | 5.9% |

비타민 강화우유 분야는 2024년에 40.2%의 점유율을 차지하였으며, 2034년까지의 CAGR은 6.1%로 예측됩니다. 영양소가 풍부한 강화우유는 성장기 어린이, 건강을 지향하는 성인, 더 나은 식사 균형을 요구하는 임산부 등 건강을 중시하는 대상 그룹에 특히 매력적입니다.

강화우유 시장의 우유 부문은 2024년에 65.1%의 점유율을 차지했으며, 2034년까지의 CAGR은 5.9%로 예측되고 있습니다. 우유는 신뢰성이 높은 단백질, 칼슘, 비타민공급원이며, 영양 강화를 위한 자연적인 선택지로 자리잡고 있습니다.

미국의 2024년 강화우유 시장 규모는 337억 달러였으며 2034년까지의 CAGR은 6.1%로 예상되고 있습니다. 미국은 유제품 산업이 발달하였고 영양면에서 건강을 중시하는 인구가 많기 때문에 북미 중에서도 두드러지고 있습니다. 강화우유는 광범위한 유통 채널을 통해 널리 이용 가능합니다.

세계의 강화우유 시장을 형성하고 있는 주요 기업으로는 Arla Foods amba, Nestle SA, The Coca-Cola Company(Fairlife), Fonterra Co-operative Group Limited, Danone SA 등이 있습니다. 주요 강화우유 기업은 시장에서의 리더십을 확고히 하기 위해 기술 혁신, 전략적 확대, 타겟형 건강 마케팅의 조합을 채용하고 있습니다.

많은 기업들이 서로 다른 소비자층에 호소하기 때문에 다양한 연령을 타겟으로 하는 제품 라인을 출시하고 있습니다. 또한 공중보건기관과의 제휴와 영양 캠페인 프로그램 참가는 신뢰 구축과 브랜드의 프레즌스 강화에 도움이 되고 있습니다.

목차

제1장 조사방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속 가능성과 환경 측면

- 지속 가능한 관행

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경친화적인 노력

- 영양분석과 건강효과

- 강화우유의 영양 성분

- 주요 영양소

- 미량 영양소

- 생리활성 화합물

- 대상 소비자별 건강 효과

- 영유아

- 아이와 청소년

- 성인

- 노인

- 임신 및 수유 중인 여성

- 선수와 피트니스 애호가

- 영양 부족에 대처

- 비타민D 결핍증

- 칼슘 결핍증

- 철 결핍증

- 기타 영양 부족

- 임상 연구와 조사 결과

- 뼈의 건강

- 면역 기능

- 인지 개발

- 기타 건강 분야

- 비교 분석

- 강화우유 vs. 일반우유

- 강화우유 vs. 식물유래 대체품

- 강화우유 vs. 영양보조식품

- 강화우유의 영양 성분

- 소비자 행동 분석

- 소비자의 인구통계

- 연령층 분석

- 소득수준 분석

- 지리적 분포

- 학력

- 구매 결정 요인

- 영양상의 이점

- 가격 감도

- 브랜드 충성도

- 포장 취향

- 맛과 향

- 소비 패턴

- 소비 빈도

- 기회에 근거한 소비

- 계절의 변화

- 소비자의 인지와 인식

- 강화의 이점에 관한 지식

- 라벨을 읽는 행동

- 건강에 관한 주장의 신뢰도

- 소비자 세분화

- 건강 지향의 소비자

- 가치추구자

- 프리미엄 구매자

- 편리성을 중시하는 소비자

- 소비자의 인구통계

- 마케팅 및 가격 전략

- 브랜드 포지셔닝

- 프리미엄 포지셔닝

- 가치 포지셔닝

- 건강 중시의 포지셔닝

- 타겟 고유의 포지셔닝

- 마케팅 채널

- 종래의 미디어

- 디지털 마케팅

- 소셜미디어 전략

- 인플루언서 마케팅

- 브랜드 포지셔닝

- 생산 및 가공 분석

- 원재료 조달

- 우유 조달

- 강화원료 조달

- 품질관리조치

- 강화 프로세스

- 직접 첨가

- 마이크로 캡슐화

- 리포솜 전달

- 기타 강화방법

- 가공기술

- 살균

- 초고온(UHT) 처리

- 스프레이 건조

- 기타 가공기술

- 품질 보증 및 테스트

- 영양안정성 시험

- 미생물학적 검사

- 관능평가

- 보존기간 시험

- 포장기술

- 무균포장

- 가스치환포장

- 활성포장

- 지속 가능한 포장 솔루션

- 원재료 조달

- 미래 전망과 전략적 제안

- 시장 발전 시나리오

- 낙관적인 시나리오

- 현실적인 시나리오

- 비관적인 시나리오

- 새로운 동향

- 개인화된 영양

- 클린라벨 강화

- 새로운 전달 시스템

- 디지털 통합

- 혁신의 기회

- 새로운 강화성분

- 포장 혁신

- 가공기술

- 제품의 배합

- 전략적 제안

- 제조업체용

- 소매업체용

- 투자자용

- 규제당국용

- 시장 발전 시나리오

제4장 경쟁구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 강화 유형별(2021-2034년)

- 주요 경향

- 비타민 강화우유

- 비타민A

- 비타민D

- 비타민B 복합체

- 비타민E

- 기타 비타민

- 미네랄 강화우유

- 칼슘

- 철

- 아연

- 기타 미네랄

- 단백질 강화우유

- 오메가3 강화우유

- 프로바이오틱스 강화우유

- 멀티영양소 강화우유

- 기타 강화 유형

제6장 시장 추계 및 예측 : 우유 유형별(2021-2034년)

- 주요 경향

- 우유

- 전유

- 저지방우유

- 스킴밀크

- 물소 우유

- 염소 우유

- A2 우유

- 기타 우유 유형

제7장 시장 추계 및 예측 : 형태별(2021-2034년)

- 주요 경향

- 액체우유

- 신선한 액체우유

- UHT 우유

- 가향우유

- 분유

- 전유분유

- 탈지분유

- 가향분유

- 연유

- 무가당연유

제8장 시장 추계 및 예측 : 포장형태별(2021-2034년)

- 주요 경향

- 판지 포장

- 테트라팩

- 게이블 탑

- 기타 카톤 유형

- 플라스틱 병

- 페트병

- HDPE병

- 기타 플라스틱 유형

- 유리병

- 파우치

- 캔

- 기타 포장 유형

제9장 시장추계 및 예측 : 타겟 소비자별(2021-2034년)

- 주요 경향

- 영유아(0-3세)

- 어린이(4-12세)

- 청소년(13-18세)

- 성인(19-50세)

- 고령자(50세 이상)

- 임신 및 수유 중인 여성

- 선수와 피트니스 애호가

제10장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 경향

- 슈퍼마켓 및 하이퍼마켓

- 편의점

- 온라인 소매

- 전자상거래 플랫폼

- 소비자 직접판매 웹사이트

- 전문점

- 약국 및 드럭스토어

- 푸드서비스

- HoReCa(호텔, 레스토랑, 카페)

- 기관

- 기타

제11장 시장 추계 및 예측 : 성질별(2021-2034년)

- 주요 경향

- 기존

- 유기농

- 락토프리

제12장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제13장 기업 프로파일

- Alaska Milk Corporation

- Almarai Company

- Arla Foods amba

- Dairy Farmers of America

- Danone SA

- Dean Foods Company

- Fonterra Co-operative Group Limited

- Groupe Lactalis

- Gujarat Cooperative Milk Marketing Federation(Amul)

- Inner Mongolia Yili Industrial Group Co., Ltd.

- Meiji Holdings Co., Ltd.

- Mother Dairy Fruit &Vegetable Pvt Ltd

- Nestle SA

- Parmalat SpA

- Saputo Inc.

- The Coca-Cola Company(Fairlife)

- Vinamilk

The Global Fortified Milk Market was valued at USD 119.5 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 211.4 billion by 2034. This steady growth is being fueled by a heightened awareness of nutritional deficiencies and a rising demand for functional dairy products. As consumer health consciousness broadens, there is a growing inclination toward dairy options enhanced with essential micronutrients like vitamin D, vitamin A, calcium, zinc, and iron. These enriched products support bone health, immune function, and cognitive development. Post-pandemic priorities have shifted significantly toward immune-boosting nutrition, driving manufacturers to launch fortified milk options that cater to every life stage, from young children to the elderly.

Increased urbanization, higher disposable incomes, and food fortification efforts promoted by public health initiatives are also propelling the market forward, particularly across developing economies in Africa and Asia. Fortified milk is playing a pivotal role in addressing widespread nutritional concerns, such as anemia, osteoporosis, and vitamin deficiencies, offering a practical solution in regions with limited access to diverse diets. In many areas, it is also a key component of large-scale nutritional programs designed to improve the well-being of school children and expectant mothers, further reinforcing its relevance as a mainstream health product.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $119.5 Billion |

| Forecast Value | $211.4 Billion |

| CAGR | 5.9% |

Vitamin-enriched milk segment held a 40.2% share in 2024 and is forecasted to grow at a CAGR of 6.1% through 2034. Its rising popularity is largely attributed to consumer preference for convenient sources of daily nutrition. Fortified milk rich in essential vitamins such as A, D, and B-complex is especially appealing to target groups focused on health, including growing children, wellness-minded adults, and expectant mothers seeking better dietary balance. These nutrient additions significantly boost milk's functional value and expand its appeal to broader demographics.

The cow milk segment in the fortified milk market held 65.1% share in 2024 and is projected to grow at a CAGR of 5.9% through 2034. Its widespread use stems from both its nutritional profile and its position as the most familiar and accepted milk type globally. Cow milk offers a reliable source of protein, calcium, and vitamins, making it a natural choice for fortification. Its compatibility with a range of nutritional additives, including omega-3 fatty acids and minerals, supports its continued growth as a convenient and nutrient-rich base.

United States Fortified Milk Market generated USD 33.7 billion in 2024 and is anticipated to grow at a CAGR of 6.1% through 2034. The US market stands out within North America due to its well-developed dairy industry and a population that places a high value on nutritional health. Consumers across the country actively seek functional foods, and fortified milk is widely accessible through extensive distribution channels. Growing public interest in wellness, preventive nutrition, and daily health optimization is reinforcing consumer demand and accelerating product innovation. National advertising campaigns and education on the benefits of fortified dairy have further driven adoption.

Key players shaping the Global Fortified Milk Market include Arla Foods amba, Nestle S.A., The Coca-Cola Company (Fairlife), Fonterra Co-operative Group Limited, and Danone S.A. To solidify their market leadership, top fortified milk companies are employing a combination of innovation, strategic expansion, and targeted health marketing. They are investing in research to develop nutrient-specific formulations aimed at immunity, bone strength, and overall wellness.

Many are launching age-targeted product lines to appeal to different consumer segments. Expanding global distribution networks, especially in emerging markets, allows these companies to capture untapped demand. Additionally, partnerships with public health agencies and participation in nutrition outreach programs help build trust and strengthen brand presence. Eco-friendly packaging and clean-label initiatives are also part of their strategy to meet evolving consumer expectations.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fortification type

- 2.2.3 Milk type

- 2.2.4 Target customer

- 2.2.5 Form

- 2.2.6 Packaging type

- 2.2.7 Distribution channel

- 2.2.8 Nature

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Nutritional analysis & health benefits

- 3.13.1 Nutritional profile of fortified milk

- 3.13.1.1 Macronutrients

- 3.13.1.2 Micronutrients

- 3.13.1.3 Bioactive compounds

- 3.13.2 Health benefits by target consumer

- 3.13.2.1 Infants & toddlers

- 3.13.2.2 Children & adolescents

- 3.13.2.3 Adults

- 3.13.2.4 Elderly

- 3.13.2.5 Pregnant & lactating women

- 3.13.2.6 Athletes & fitness enthusiasts

- 3.13.3 Addressing nutritional deficiencies

- 3.13.3.1 Vitamin d deficiency

- 3.13.3.2 Calcium deficiency

- 3.13.3.3 Iron deficiency

- 3.13.3.4 Other nutritional deficiencies

- 3.13.4 Clinical studies & research findings

- 3.13.4.1 Bone health

- 3.13.4.2 Immune function

- 3.13.4.3 Cognitive development

- 3.13.4.4 Other health areas

- 3.13.5 Comparative analysis

- 3.13.5.1 Fortified milk vs. Regular milk

- 3.13.5.2 Fortified milk vs. Plant-based alternatives

- 3.13.5.3 Fortified milk vs. Dietary supplements

- 3.13.1 Nutritional profile of fortified milk

- 3.14 Consumer behavior analysis

- 3.14.1 Consumer demographics

- 3.14.1.1 Age group analysis

- 3.14.1.2 Income level analysis

- 3.14.1.3 Geographic distribution

- 3.14.1.4 Educational background

- 3.14.2 Purchase decision factors

- 3.14.2.1 Nutritional benefits

- 3.14.2.2 Price sensitivity

- 3.14.2.3 Brand loyalty

- 3.14.2.4 Packaging preferences

- 3.14.2.5 Taste & flavor

- 3.14.3 Consumption patterns

- 3.14.3.1 Frequency of consumption

- 3.14.3.2 Occasion-based consumption

- 3.14.3.3 Seasonal variations

- 3.14.4 Consumer awareness & perception

- 3.14.4.1 Knowledge of fortification benefits

- 3.14.4.2 Label reading behavior

- 3.14.4.3 Trust in health claims

- 3.14.5 Consumer segmentation

- 3.14.5.1 Health-conscious consumers

- 3.14.5.2 Value seekers

- 3.14.5.3 Premium buyers

- 3.14.5.4 Convenience-oriented consumers

- 3.14.1 Consumer demographics

- 3.15 Marketing & pricing strategies

- 3.15.1 Brand positioning

- 3.15.1.1 Premium positioning

- 3.15.1.2 Value positioning

- 3.15.1.3 Health-focused positioning

- 3.15.1.4 Target-specific positioning

- 3.15.2 Marketing channels

- 3.15.2.1 Traditional media

- 3.15.2.2 Digital marketing

- 3.15.2.3 Social media strategies

- 3.15.2.4 Influencer marketing

- 3.15.1 Brand positioning

- 3.16 Production & processing analysis

- 3.16.1 Raw material sourcing

- 3.16.1.1 Milk sourcing

- 3.16.1.2 Fortification ingredients sourcing

- 3.16.1.3 Quality control measures

- 3.16.2 Fortification process

- 3.16.2.1 Direct addition

- 3.16.2.2 Microencapsulation

- 3.16.2.3 Liposomal delivery

- 3.16.2.4 Other fortification methods

- 3.16.3 Processing technologies

- 3.16.3.1 Pasteurization

- 3.16.3.2 Ultra-High Temperature (UHT) processing

- 3.16.3.3 Spray drying

- 3.16.3.4 Other processing technologies

- 3.16.4 Quality assurance & testing

- 3.16.4.1 Nutrient stability testing

- 3.16.4.2 Microbiological testing

- 3.16.4.3 Sensory evaluation

- 3.16.4.4 Shelf-life testing

- 3.16.5 Packaging technologies

- 3.16.5.1 Aseptic packaging

- 3.16.5.2 Modified atmosphere packaging

- 3.16.5.3 Active packaging

- 3.16.5.4 Sustainable packaging solutions

- 3.16.1 Raw material sourcing

- 3.17 Future outlook & strategic recommendations

- 3.17.1 Market evolution scenario

- 3.17.1.1 Optimistic scenario

- 3.17.1.2 Realistic scenario

- 3.17.1.3 Pessimistic scenario

- 3.17.2 Emerging trends

- 3.17.2.1 Personalized nutrition

- 3.17.2.2 Clean label fortification

- 3.17.2.3 Novel delivery systems

- 3.17.2.4 Digital integration

- 3.17.3 Innovation opportunities

- 3.17.3.1 New fortification ingredients

- 3.17.3.2 Packaging innovations

- 3.17.3.3 Processing technologies

- 3.17.3.4 Product formulations

- 3.17.4 Strategic recommendations

- 3.17.4.1 For manufacturers

- 3.17.4.2 For retailers

- 3.17.4.3 For investors

- 3.17.4.4 For regulatory bodies

- 3.17.1 Market evolution scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Fortification Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trend

- 5.2 Vitamin fortified milk

- 5.2.1 Vitamin A

- 5.2.2 Vitamin D

- 5.2.3 Vitamin B Complex

- 5.2.4 Vitamin E

- 5.2.5 Other vitamins

- 5.3 Mineral fortified milk

- 5.3.1 Calcium

- 5.3.2 Iron

- 5.3.3 Zinc

- 5.3.4 Other minerals

- 5.4 Protein fortified milk

- 5.5 Omega-3 fortified milk

- 5.6 Probiotic fortified milk

- 5.7 Multi-nutrient fortified milk

- 5.8 Other fortification types

Chapter 6 Market Estimates & Forecast, By Milk Type, 2021-2034 (USD Billion) (Thousand Litres)

- 6.1 Key trend

- 6.2 Cow milk

- 6.2.1 Whole milk

- 6.2.2 Semi-skimmed milk

- 6.2.3 Skimmed milk

- 6.3 Buffalo milk

- 6.4 Goat milk

- 6.5 A2 milk

- 6.6 Other milk types

Chapter 7 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Thousand Litres)

- 7.1 Key trend

- 7.2 Liquid milk

- 7.2.1 Fresh liquid milk

- 7.2.2 UHT milk

- 7.2.3 Flavored milk

- 7.3 Powdered milk

- 7.3.1 Whole milk powder

- 7.3.2 Skimmed milk powder

- 7.3.3 Flavored milk powder

- 7.4 Condensed milk

- 7.5 Evaporated milk

Chapter 8 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion) (Thousand Litres)

- 8.1 Key trend

- 8.2 Carton packaging

- 8.2.1 Tetra pak

- 8.2.2 Gable top

- 8.2.3 Other carton types

- 8.3 Plastic bottles

- 8.3.1 Pet bottles

- 8.3.2 HDPE bottles

- 8.3.3 Other plastic types

- 8.4 Glass bottles

- 8.5 Pouches

- 8.6 Cans

- 8.7 Other packaging types

Chapter 9 Market Estimates & Forecast, By Target Consumer, 2021-2034 (USD Billion) (Thousand Litres)

- 9.1 Key trend

- 9.2 Infants & toddlers (0-3 years)

- 9.3 Children (4-12 years)

- 9.4 Adolescents (13-18 years)

- 9.5 Adults (19-50 years)

- 9.6 Elderly (above 50 years)

- 9.7 Pregnant & lactating women

- 9.8 Athletes & fitness enthusiasts

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Litres)

- 10.1 Key trend

- 10.2 Supermarkets & hypermarkets

- 10.3 Convenience stores

- 10.4 Online retail

- 10.4.1 E-commerce platforms

- 10.4.2 Direct-to-consumer websites

- 10.5 Specialty stores

- 10.6 Pharmacies & drug stores

- 10.7 Foodservice

- 10.7.1 HoReCa (Hotels, Restaurants, Cafes)

- 10.7.2 Institutional

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Nature, 2021-2034 (USD Billion) (Thousand Litres)

- 11.1 Key trend

- 11.2 Conventional

- 11.3 Organic

- 11.4 Lactose-free

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Litres)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Rest of Europe

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Rest of Asia Pacific

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Rest of Latin America

- 12.6 Middle East & Africa

- 12.6.1 Saudi Arabia

- 12.6.2 South Africa

- 12.6.3 UAE

- 12.6.4 Rest of Middle East & Africa

Chapter 13 Company Profiles

- 13.1 Alaska Milk Corporation

- 13.2 Almarai Company

- 13.3 Arla Foods amba

- 13.4 Dairy Farmers of America

- 13.5 Danone S.A.

- 13.6 Dean Foods Company

- 13.7 Fonterra Co-operative Group Limited

- 13.8 Groupe Lactalis

- 13.9 Gujarat Cooperative Milk Marketing Federation (Amul)

- 13.10 Inner Mongolia Yili Industrial Group Co., Ltd.

- 13.11 Meiji Holdings Co., Ltd.

- 13.12 Mother Dairy Fruit & Vegetable Pvt Ltd

- 13.13 Nestle S.A

- 13.14 Parmalat S.p.A.

- 13.15 Saputo Inc.

- 13.16 The Coca-Cola Company (Fairlife)

- 13.17 Vinamilk