|

시장보고서

상품코드

1773361

쌀 전분 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Rice Starch Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

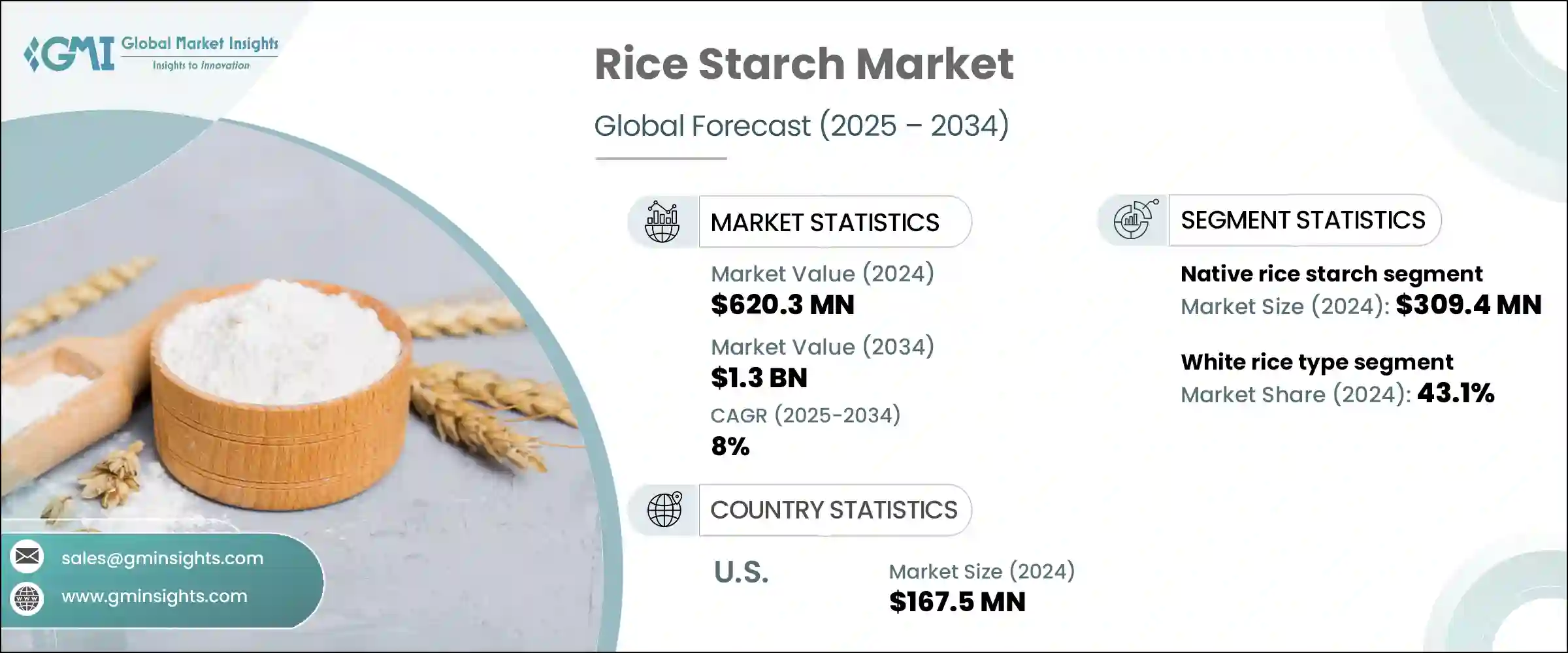

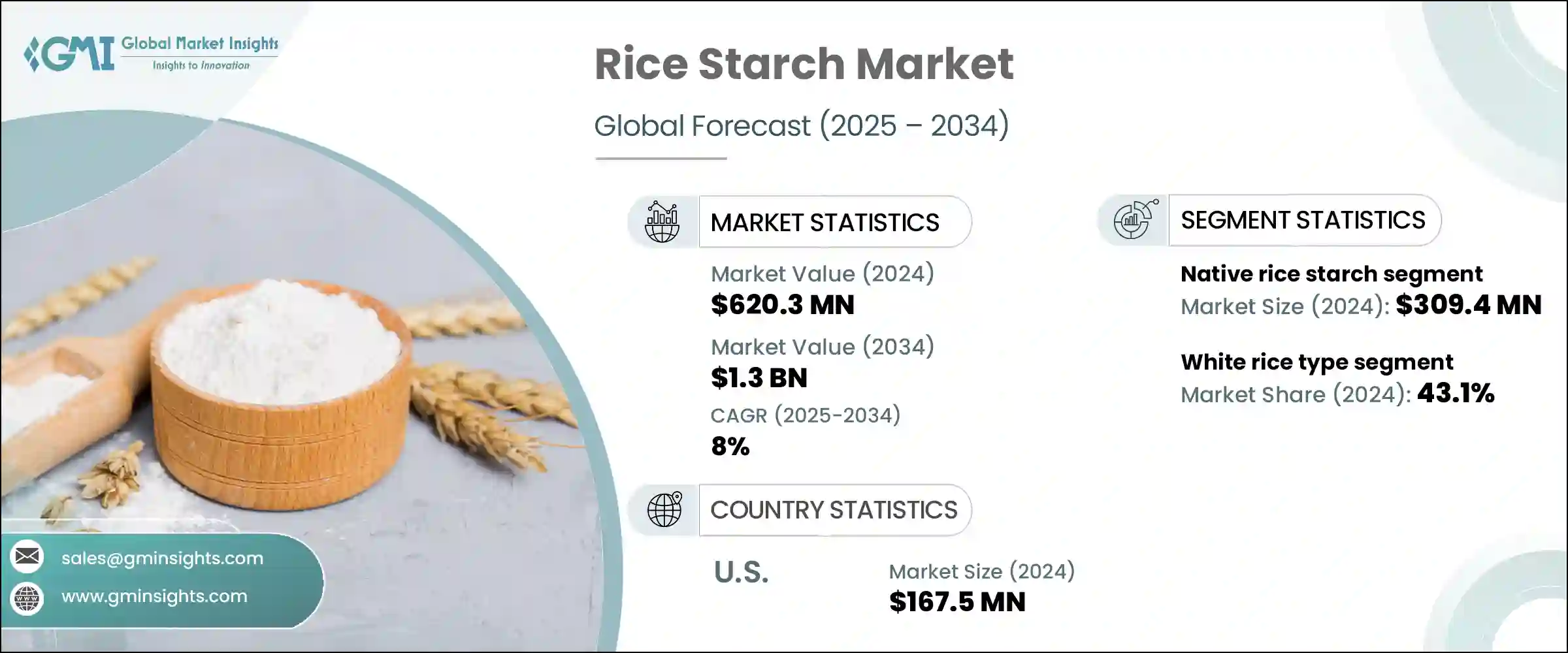

세계의 쌀 전분 시장은 2024년에는 6억 2,030만 달러로 평가되었고, 2034년에는 13억 달러에 달할 것으로 예측되며, CAGR 8%로 성장할 전망입니다.

이러한 시장 확장은 여러 산업에서 쌀 전분의 채택이 증가함에 따라 촉진되고 있습니다. 이 분석은 과거의 성과와 미래의 전망을 균형 있게 제시하여 시장의 전반적인 추이에 대한 귀중한 통찰력을 제공합니다. 잠재적 투자자를 유치하기 위해 시장 가치와 거래량을 모두 분석합니다. 청정 라벨 성분에 대한 수요 증가와 천연 식품 성분으로의 소비자 전환이 지속적인 성장을 뒷받침하고 있습니다. 식품 및 음료 부문은 여전히 주요 동력으로, 쌀 전분의 증점, 텍스처링, 안정화 등 다기능 특성으로 인해 제품 제형에 널리 사용되고 있습니다. 글루텐 및 알레르기 유발 성분이 없는 제품에 대한 수요가 급증하면서 이러한 동향이 더욱 가속화되고 있습니다.

또한, 기존에 성장세가 느린 부문에서 새로운 혁신적인 용도가 등장하면서 쌀 전분 시장의 전반적인 확장에 크게 기여할 것으로 보입니다. 이러한 새로운 응용 분야는 빠르게 성장하는 산업에서 볼 수 있는 모멘텀을 보완하고 강화하는 새로운 수요를 창출합니다. 특수 의약품 제형, 고급 화장품, 틈새 식품 응용 분야 등 최종 용도 범위를 다양화함으로써 이러한 신흥 부문은 성장을 안정화하고 산업 간 통합의 기회를 열어줍니다. 이러한 광범위한 채택은 판매량을 증가시킬 뿐만 아니라 연구 개발에 대한 투자를 촉진하여 제품 혁신을 촉진하고 제조업체가 이전에 개척하지 못한 시장에 진출할 수 있도록 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 6억 2,030만 달러 |

| 예측 금액 | 13억 달러 |

| CAGR | 8% |

2024년에 천연 쌀 전분 부문은 3억 940만 달러의 가치를 기록했으며, 2034년까지 연평균 7.9%의 성장률을 보일 것으로 예상됩니다. 천연 쌀 전분은 다양한 산업에서 폭넓게 사용되고 있어 시장을 계속 지배하고 있습니다. 특히 제분에서 추출된 형태, 다목적성, 클린 라벨 요구 사항에 부합한다는 점에서 선호되고 있습니다. 식품 및 음료 산업은 유제품, 소스, 유아 영양 식품 등 제품에 증점, 겔화, 안정화 기능을 활용하여 천연 쌀 전분의 최대 소비 기반을 차지하고 있습니다. 천연 유래 및 기능적 이점으로 인해 많은 제형에 필수적인 성분으로 사용되고 있습니다.

미국의 쌀 전분 시장은 2024년에 1억 6,750만 달러로 평가되었고, 2025년부터 2034년까지 7.8%의 연평균 성장률(CAGR)로 성장할 것으로 예상됩니다. 미국의 성장은 클린 라벨, 글루텐 프리, 식물성 원료에 대한 선호도가 증가함에 따라 발생하고 있습니다. 식품 및 음료 산업은 특히 제빵, 유제품 및 편의 식품 분야에서 계속해서 주요 소비 분야로 남아 있습니다. 쌀 전분은 저자극성 및 생분해성 특성으로 인해 제약 및 화장품 분야에서도 수요가 증가하고 있습니다. 가공 기술의 발전으로 제품 품질이 향상되고 응용 분야가 확대되어 시장 성장이 더욱 강화되었습니다. 미국은 북미에서 가장 활발한 시장 업체로, 이 지역의 성장을 촉진하고 있습니다.

세계적으로 쌀 전분 시장은 Roquette Freres, Cargill Incorporation, BENEO GmbH, AGRANA Beteiligungs-AG, Ingredient Incorporated 등 주요 업체들이 경쟁을 주도하며 적당히 통합되어 있습니다. 이 기업들은 상당한 시장 점유율을 차지하고 있으며, 업계 동향을 형성하는 데 중요한 역할을 하고 있습니다. 쌀 전분 시장 선도 기업들은 시장 지위를 강화하기 위해 다양한 전략적 이니셔티브를 채택하고 있습니다. 이들은 제품 기능성을 향상시키고 클린 라벨 요구사항을 충족시키기 위해 새로운 제형과 가공 기술을 개발하는 데 집중하고 있습니다. 식품 및 음료 제조업체와의 전략적 파트너십과 협력을 통해 유통 네트워크와 최종 사용 분야를 확장하고 있습니다. 지속 가능한 원료 조달 및 생산 방식에 대한 투자는 환경 책임에 대한 그들의 헌신을 강화하며, 이는 환경 의식이 높은 소비자에게 어필하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 클린 라벨 원료 수요 증가

- 글루텐 불내증의 유병률 상승

- 식품 및 음료 업계에서의 적용 확대

- 의약품 및 화장품에 사용 확대

- 업계의 잠재적 위험 및 과제

- 대체 전분과의 경쟁

- 원재료 가격 변동

- 시장 기회

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적 인 노력

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 천연 쌀 전분

- 가공 쌀 전분

- 물리적 가공

- 젤라틴화된 쌀 전분

- 열처리된 쌀 전분

- 기타 물리적 가공 쌀 전분

- 화학적 가공

- 교차 결합 된 쌀 전분

- 산화된 쌀 전분

- 아세틸화 쌀 전분

- 기타 화학적 가공 쌀 전분

- 효소 수식

- 물리적 가공

- 내성이 있는 쌀 전분

제6장 시장 추계 및 예측 : 원료별(2021-2034년)

- 주요 동향

- 백미

- 현미

- 쇄미 및 부산물

- 기타

제7장 시장 추계 및 예측 : 형태별(2021-2034년)

- 주요 동향

- 분말

- 액체와 젤

- 기타

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 식품 및 음료

- 제빵 및 제과

- 유제품

- 수프, 소스, 드레싱

- 육류 및 가금류 제품

- 스낵과 편의점 식품

- 음료

- 유아식 및 유아용 제품 유형

- 글루텐 프리 제품

- 기타 식품 용도

- 의약품

- 정제의 결합과 붕괴

- 캡슐 제품 솔루션

- 약물전달 시스템

- 기타 의약품 용도

- 화장품 및 퍼스널케어

- 스킨케어 제품

- 헤어 케어 제품

- 컬러 화장품

- 기타 화장품 용도

- 종이 및 섬유

- 종이 사이즈 가공 및 코팅

- 섬유의 사이즈 가공 및 마무리

- 기타 종이 및 섬유 용도

- 기타 용도

- 접착제

- 생분해성 포장

- 기타 산업용도

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- A&B Ingredients

- AGRANA Beteiligungs-AG

- Agrana Group

- Anhui Lianhe

- Archer Daniels Midland Company

- Bangkok Starch Industrial Co., Ltd.

- Beneo(Sudzucker Group)

- Cargill, Incorporated

- Golden Agriculture Co., Ltd.

- Herba Ingredients

- Hunan ER-KANG

- Ingredion Incorporated

- Jiangxi Golden Agriculture Co., Ltd.

- Roquette Freres

- Shaanxi Tianyu Pharmaceutical Co., Ltd.

- Sonish Starch Technology Co., Ltd.

- Tate &Lyle PLC

- THAI WAH PUBLIC COMPANY LIMITED

- Thai Flour Industry Co., Ltd.

- Wuxi Chuangda Food Co., Ltd.

The Global Rice Starch Market was valued at USD 620.3 million in 2024 and is estimated to grow at a CAGR of 8% to reach USD 1.3 billion by 2034. This market expansion is driven by the increasing adoption of rice starch across multiple industries. The analysis provides a balanced view of past performance alongside future projections, offering valuable insights into the market's overall trajectory. Both market value and volume are analyzed to attract potential investors. Consistent growth has been supported by rising demand for clean-label ingredients and a broader consumer shift towards natural food components. The food and beverage sector remains the primary driver, with rice starch's multifunctional properties, like thickening, texturizing, and stabilizing, leading to its widespread inclusion in product formulations. The surge in demand for gluten-free and allergen-free products has further fueled this trend.

Additionally, new and innovative uses emerging within traditionally slower-growing segments are poised to contribute significantly to the rice starch market's overall expansion. These developing applications create fresh demand streams that complement and strengthen the momentum seen in faster-growing industries. By diversifying the range of end-use cases, such as specialized pharmaceutical formulations, advanced cosmetic products, and niche food applications, these emerging sectors help stabilize growth and open opportunities for cross-industry integration. This broader adoption not only drives incremental volume but also encourages investment in research and development, fueling product innovation and enabling manufacturers to tap into previously untapped markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $620.3 Million |

| Forecast Value | $1.3 Billion |

| CAGR | 8% |

In 2024, the native rice starch segment held a valuation of USD 309.4 million and is anticipated to grow at a CAGR of 7.9% through 2034. Native rice starch continues to dominate the market due to its extensive use across various industries. It is especially favored because of its milled-derived form, versatility, and alignment with clean-label requirements. The food and beverage industry represents the largest consumer base for native rice starch, leveraging its thickening, gelling, and stabilizing functions in products such as dairy, sauces, and infant nutrition. Its natural origin and functional benefits make it an essential ingredient in many formulations.

The white rice type segment accounted for USD 267.4 million in 2024 and is expected to grow at an 8.1% CAGR through 2034, holding a 43.1% share. White rice remains the leading source of rice starch, thanks to its ease of processing, abundant availability, and neutral flavor profile. Both consumers and manufacturers prefer rice starch derived from white rice due to its consistent, high-quality yield, making it ideal for use in food, pharmaceutical, and cosmetic products that demand superior starch quality. Large-scale producers also favor white rice because of its standardized properties and efficient extraction methods. Additionally, rising interest in organic and minimally processed foods is boosting the demand for rice starch from white rice, which is increasingly perceived as a premium ingredient.

U.S. Rice Starch Market was valued at USD 167.5 million in 2024 and is expected to grow at a 7.8% CAGR from 2025 to 2034. Growth in the U.S. is attributed to the rising preference for clean-label, gluten-free, and plant-based ingredients. The food and beverage industry continues to be the dominant consumer, particularly within bakery, dairy, and convenience food applications. Demand is also increasing in the pharmaceutical and cosmetics sectors due to rice starch's hypoallergenic and biodegradable properties. Advances in processing technologies have enhanced product quality and expanded the range of applications, further strengthening market growth. The U.S. stands as the most active market player in North America, driving growth across the region.

On a global scale, the Rice Starch Market is moderately consolidated, with major players such as Roquette Freres, Cargill Incorporation, BENEO GmbH, AGRANA Beteiligungs-AG, and Ingredient Incorporated leading the competition. These companies hold significant market shares and are instrumental in shaping industry trends. Leading companies in the rice starch market adopt various strategic initiatives to strengthen their market position. They focus heavily on innovation, developing new formulations and processing techniques that enhance product functionality and meet clean-label demands. Strategic partnerships and collaborations with food and beverage manufacturers help expand their distribution networks and end-use applications. Investment in sustainable sourcing and production practices reinforces their commitment to environmental responsibility, which appeals to eco-conscious consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360 synopsis

- 2.2 Key market trends

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for clean label ingredients

- 3.2.1.2 Rising prevalence of gluten intolerance

- 3.2.1.3 Increasing applications in food & beverage industry

- 3.2.1.4 Expanding use in pharmaceutical & cosmetic products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Competition from alternative starches

- 3.2.2.2 Price volatility of raw materials

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle east & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Price trends

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Native rice starch

- 5.3 Modified rice starch

- 5.3.1 Physically modified

- 5.3.1.1 Pre-gelatinized rice starch

- 5.3.1.2 Heat-moisture treated rice starch

- 5.3.1.3 Other physically modified rice starch

- 5.3.2 Chemically modified

- 5.3.2.1 Cross-linked rice starch

- 5.3.2.2 Oxidized rice starch

- 5.3.2.3 Acetylated rice starch

- 5.3.2.4 Other chemically modified rice starch

- 5.3.3 Enzymatically modified

- 5.3.1 Physically modified

- 5.4 Resistant Rice Starch

Chapter 6 Market Estimates & Forecast, By Source, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 White rice

- 6.3 Brown rice

- 6.4 Broken rice & by-products

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Form, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Powder

- 7.3 Liquid & gel

- 7.4 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverage

- 8.2.1 Bakery & confectionery

- 8.2.2 Dairy products

- 8.2.3 Soups, sauces & dressings

- 8.2.4 Meat & Poultry Products

- 8.2.5 Snacks & convenience foods

- 8.2.6 Beverages

- 8.2.7 Baby food & infant product type

- 8.2.8 Gluten-free products

- 8.2.9 Other food applications

- 8.3 Pharmaceuticals

- 8.3.1 Tablet binding & disintegration

- 8.3.2 Capsule product solutions

- 8.3.3 Drug delivery systems

- 8.3.4 Other pharmaceutical applications

- 8.3.5 Cosmetics & personal care

- 8.3.6 Skin care products

- 8.3.7 Hair care products

- 8.3.8 Color cosmetics

- 8.3.9 Other cosmetic applications

- 8.4 Paper & textile

- 8.4.1 Paper sizing & coating

- 8.4.2 Textile sizing & finishing

- 8.4.3 Other paper & textile applications

- 8.5 Other applications

- 8.5.1 Adhesives & glues

- 8.5.2 Biodegradable packaging

- 8.5.3 Other industrial applications

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 A&B Ingredients

- 10.2 AGRANA Beteiligungs-AG

- 10.3 Agrana Group

- 10.4 Anhui Lianhe

- 10.5 Archer Daniels Midland Company

- 10.6 Bangkok Starch Industrial Co., Ltd.

- 10.7 Beneo (Sudzucker Group)

- 10.8 Cargill, Incorporated

- 10.9 Golden Agriculture Co., Ltd.

- 10.10 Herba Ingredients

- 10.11 Hunan ER-KANG

- 10.12 Ingredion Incorporated

- 10.13 Jiangxi Golden Agriculture Co., Ltd.

- 10.14 Roquette Freres

- 10.15 Shaanxi Tianyu Pharmaceutical Co., Ltd.

- 10.16 Sonish Starch Technology Co., Ltd.

- 10.17 Tate & Lyle PLC

- 10.18 THAI WAH PUBLIC COMPANY LIMITED

- 10.19 Thai Flour Industry Co., Ltd.

- 10.20 Wuxi Chuangda Food Co., Ltd.