|

시장보고서

상품코드

1773380

중공 벽돌 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Hollow Bricks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

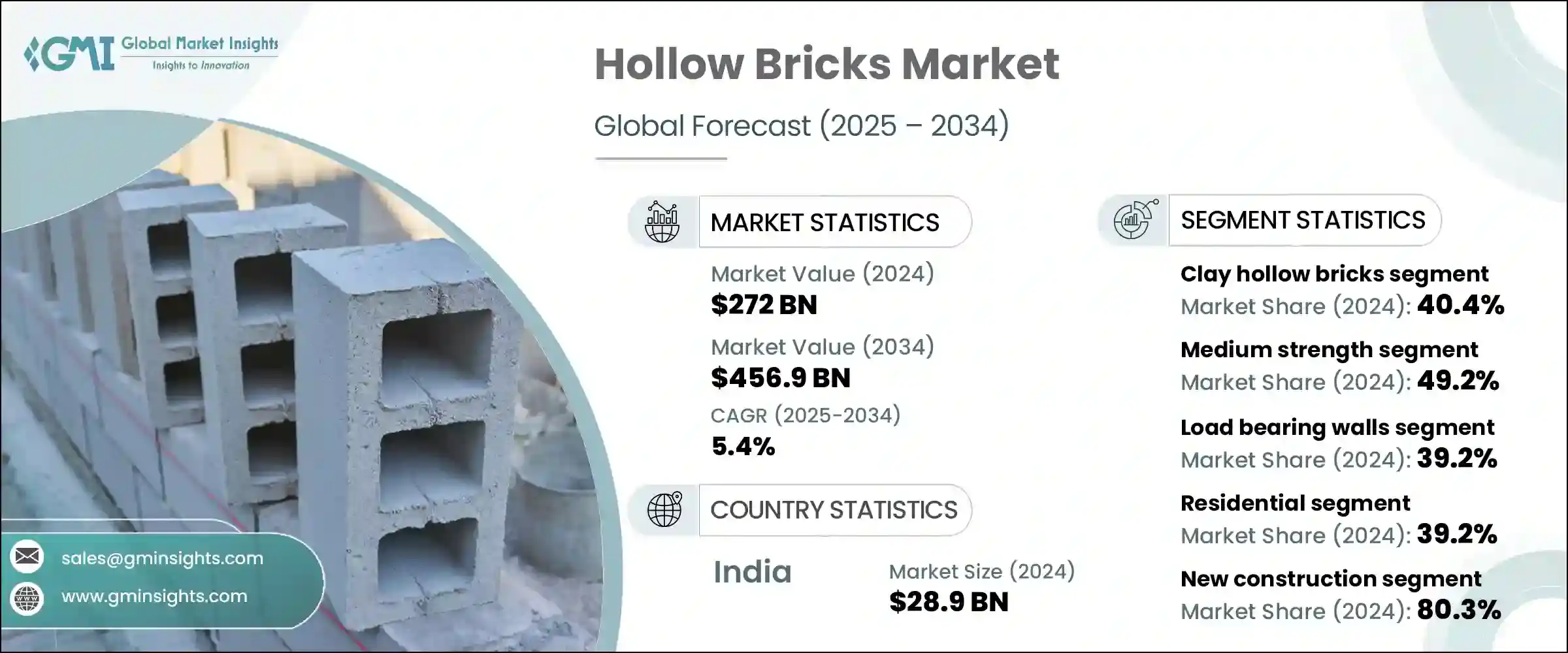

중공 벽돌 시장 규모는 2024년 2,720억 달러로 평가되었고, CAGR 5.4%를 나타내 2034년에는 4,569억 달러에 달할 것으로 예상되고 있습니다. 경제적이고 지속 가능한 건축자재의 사용을 장려함으로써 이 상승세에 공헌하고 있습니다.

이 벽돌은 실내 온도와 소음 수준을 조정하는 데 도움이 되며, 기후가 변동하기 쉽고 소음 수준이 높은 도시 환경에서 건물을 보다 쾌적하게 만들어줍니다. 특히 노동력과 예산이 엄격한 경우 운송과 조립을 보다 신속하고 자원 효율적으로 합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 2,720억 달러 |

| 예측 금액 | 4,569억 달러 |

| CAGR | 5.4% |

2024년에는 점토 중공 벽돌 부문이 40.4%의 점유율을 차지했습니다. 건설 업계가 고강도이고 경량인 선택으로 이동하는 가운데, 이러한 벽돌 수요는 다양한 재료 유형으로 상승을 계속하고 있습니다. 점토를 주성분으로 하는 벽돌이, 특히 저층 개발에서는 그 폭넓은 입수성과 비용 효율적인 제조 공정에 의해 여전히 유력한 옵션이 되고 있습니다. 열적 성능과 강도 특성은 농촌 지역과 신흥 도시 지역 모두에서 특히 합리적인 가격과 재료에 대한 접근이 중요한 신흥 경제 국가에서 널리 사용됩니다.

내력벽 분야에서 사용되는 중공 벽돌의 2024년 점유율은 39.2%였습니다. 내력벽은 현대 건축 설계의 기본 부분이며 주거 및 상업 프로젝트에 내구성과 필수적인 구조적지지를 제공합니다. 내력벽 용도가 대부분을 차지하는 한편, 사용의 용이성과 경량성으로부터 비내력 내벽으로의 중공 벽돌의 사용도 현저하게 성장하고 있습니다. 중공 벽돌의 인기가 높아지고 있는 배경에는 신속한 시공과 다양한 레이아웃이 선호되는 신축 건물의 설계 요구의 진화가 있습니다.

인도의 중공 벽돌 시장 점유율은 82%로, 2024년에는 289억 달러에 이르렀습니다. 가능성은 시장의 우위성을 더욱 강화하고 있으며, 소규모 도시와 2급 시장에서의 채용이 증가하여 국내 소비의 밑단이 퍼지고 있습니다.

중공 벽돌 산업을 형성하는 가장 영향력있는 기업은 Xella Group, HH International A/S, UltraTech Cement Ltd, Biltech Building Elements Limited, Wienerberger AG 등이 있습니다. 이러한 기업은 제품 혁신과 주요 지역에서의 전략적 존재를 통해 시장의 진화에 적극적으로 기여하고 있습니다. 향상을 위한 지역 제조 허브의 설치, 일관성을 유지하면서 생산량을 확대하기 위한 자동 생산에 대한 투자, 강도와 열성능을 강화한 첨단 제품 변형의 도입 등이 포함됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 성장하는 건설 업계

- 에너지 효율에 중점이 증가

- 비용 효율과 재료 사용량 절감

- 뛰어난 단열성과 차음성

- 업계의 잠재적 위험 및 과제

- 대체 건축재료와의 경쟁

- 변동하는 강도 클래스의 가격

- 지역의 건축 기준법의 준수

- 품질관리와 일관성 문제

- 시장 기회

- 친환경 중공 벽돌 개발

- 신흥 시장으로 확대

- 제조업에 있어서 기술의 진보

- 현대 건설 기술과의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 점토 중공 벽돌

- 콘크리트 중공 블록

- 플라이 애쉬 중공 벽돌

- AAC(오토클레이브 폭기 콘크리트) 중공 블록

- 기타

제6장 시장 추계·예측 : 강도별(2021-2034년)

- 주요 동향

- 저강도

- 중강도

- 고강도

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 내력벽

- 외부 내력벽

- 내부 내력벽

- 기타

- 비내력벽

- 칸막이벽

- 충전 벽

- 기타

- 기초

- 기둥 및 지주

- 상인방 및 보

- 기타

제8장 시장 추계·예측 : 최종 이용 산업별(2021-2034년)

- 주요 동향

- 주택용

- 단독주택

- 다가구 건물

- 저렴한 주택

- 기타

- 상업용

- 사무실 건물

- 소매 공간

- 접객

- 의료시설

- 교육기관

- 기타

- 산업용

- 제조 시설

- 창고

- 기타

- 인프라

- 기타

제9장 시장추계·예측 : 건축 유형별(2021-2034년)

- 주요 동향

- 신축

- 개수 및 개조

제10장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접 판매

- 판매업체 및 도매업체

- 홈센터

- 온라인 소매

- 기타

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제12장 기업 프로파일

- AERCON AAC

- Biltech Building Elements Limited

- Eco Green Products Pvt. Ltd

- Fusion Blocks

- HH International A/S

- Infra.Market

- Jindal Mechno Bricks Private Limited

- Magicrete Building Solutions Pvt. Ltd

- MRF Bricks

- NICBM

- Paver India

- SOLBET

- UltraTech Cement Ltd

- Wienerberger AG

- Xella Group

The Global Hollow Bricks Market was valued at USD 272 billion in 2024 and is estimated to grow at a CAGR of 5.4 % to reach USD 456.9 billion by 2034. The rising demand for new residential and commercial structures, particularly in metropolitan and suburban areas, is significantly boosting the need for hollow bricks. Their ease of installation and cost-effectiveness make them an ideal choice for large-scale construction projects. Government-backed affordable housing initiatives have also contributed to this upward trend by encouraging the use of economical and sustainable building materials. Hollow bricks provide natural insulation against heat and cold, making them energy efficient. Their ability to help reduce cooling and heating costs aligns with the growing focus on green buildings and energy-efficient construction, making them preferred material among environmentally conscious developers.

These bricks help regulate indoor temperatures and noise levels, making buildings more comfortable in urban environments with fluctuating climates and higher sound levels. Their structure reduces the need for excess mortar and minimizes the demand for high-strength materials, which cuts down overall construction costs. Lightweight properties make transportation and assembly faster and more resource-efficient, especially where labor and budgets are tight. Moreover, the growing adoption of modular and prefabricated construction techniques is further increasing the demand for hollow bricks due to their compatibility with modern construction practices and their contribution to accelerated project timelines.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $272 Billion |

| Forecast Value | $456.9 Billion |

| CAGR | 5.4% |

In 2024, the clay hollow bricks segment held a 40.4% share. The demand for these bricks continues to rise across various material types as the construction industry shifts toward high-strength yet lightweight options. Clay-based variants remain a dominant choice, particularly in low-rise developments, due to their wide availability and cost-efficient manufacturing processes. Their thermal performance and strength properties support their widespread use in both rural and developing urban regions, especially in emerging economies where affordability and access to materials are critical.

Hollow bricks used in the load-bearing walls segment contributed a 39.2% share in 2024. These walls are a fundamental part of modern building design, providing durability and essential structural support for residential and commercial projects alike. While load-bearing applications dominate, there is also notable growth in the use of hollow bricks in non-load-bearing interior walls due to their ease of use and lightweight nature. Their growing popularity is tied to evolving design needs that favor faster installation and versatile layout options in new buildings.

India Hollow Bricks Market held an 82% share and generated USD 28.9 billion in 2024. The country's leadership is driven by rapid urban growth, widespread construction activities, and the momentum created by public infrastructure and housing schemes. India's robust manufacturing ecosystem and ample availability of strength-class raw materials further strengthen its market dominance. Additionally, rising adoption in smaller cities and tier-two markets has broadened the domestic consumption base. Meanwhile, policy efforts aimed at promoting sustainable and energy-efficient building materials have further accelerated the use of hollow bricks across various regions.

Some of the most influential players shaping the Hollow Bricks Industry include Xella Group, H+H International A/S, UltraTech Cement Ltd, Biltech Building Elements Limited, and Wienerberger AG. These companies are actively contributing to the market's evolution through product innovation and strategic presence across key regions. To solidify their positions in the hollow bricks market, leading manufacturers are leveraging multiple growth strategies. These include setting up regional manufacturing hubs to reduce logistics costs and improve distribution efficiency, investing in automated production to scale output while maintaining consistency, and introducing advanced product variants with enhanced strength and thermal performance. Partnerships with real estate developers and construction firms have also proven effective in driving adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Strength Class

- 2.2.4 Application

- 2.2.5 End use industry

- 2.2.6 Production process

- 2.2.7 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing construction industry

- 3.2.1.2 Increasing focus on energy efficiency

- 3.2.1.3 Cost-effectiveness and reduced material usage

- 3.2.1.4 Superior thermal and acoustic insulation properties

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Competition from alternative building materials

- 3.2.2.2 Fluctuating Strength Class prices

- 3.2.2.3 Regional building code compliance

- 3.2.2.4 Quality control and consistency issues

- 3.2.3 Market opportunities

- 3.2.3.1 Development of eco-friendly hollow bricks

- 3.2.3.2 Expansion in emerging markets

- 3.2.3.3 Technological advancements in manufacturing

- 3.2.3.4 Integration with modern construction techniques

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Clay hollow bricks

- 5.3 Concrete hollow blocks

- 5.4 Fly ash hollow bricks

- 5.5 AAC (Autoclaved Aerated Concrete) hollow blocks

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Strength Class, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Low strength

- 6.3 Medium strength

- 6.4 High strength

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Load bearing walls

- 7.2.1 External load bearing walls

- 7.2.2 Internal load bearing walls

- 7.2.3 Others

- 7.3 Non-load bearing walls

- 7.3.1 Partition walls

- 7.3.2 Infill walls

- 7.3.3 Others

- 7.4 Foundations

- 7.5 Columns and pillars

- 7.6 Lintels and beams

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential

- 8.2.1 Single-family homes

- 8.2.2 Multi-family buildings

- 8.2.3 Affordable housing

- 8.2.4 Others

- 8.3 Commercial

- 8.3.1 Office buildings

- 8.3.2 Retail spaces

- 8.3.3 Hospitality

- 8.3.4 Healthcare facilities

- 8.3.5 Educational institutions

- 8.3.6 Others

- 8.4 Industrial

- 8.4.1 Manufacturing facilities

- 8.4.2 Warehouses

- 8.4.3 Others

- 8.5 Infrastructure

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Construction Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 New construction

- 9.3 Renovation and retrofitting

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Distributors and wholesalers

- 10.4 Home improvement stores

- 10.5 Online retail

- 10.6 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 AERCON AAC

- 12.2 Biltech Building Elements Limited

- 12.3 Eco Green Products Pvt. Ltd

- 12.4 Fusion Blocks

- 12.5 H+H International A/S

- 12.6 Infra.Market

- 12.7 Jindal Mechno Bricks Private Limited

- 12.8 Magicrete Building Solutions Pvt. Ltd

- 12.9 MRF Bricks

- 12.10 NICBM

- 12.11 Paver India

- 12.12 SOLBET

- 12.13 UltraTech Cement Ltd

- 12.14 Wienerberger AG

- 12.15 Xella Group