|

시장보고서

상품코드

1773389

자동차 펜더 휠하우스 패널 부품 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Automotive Fender Wheel House Panel Parts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

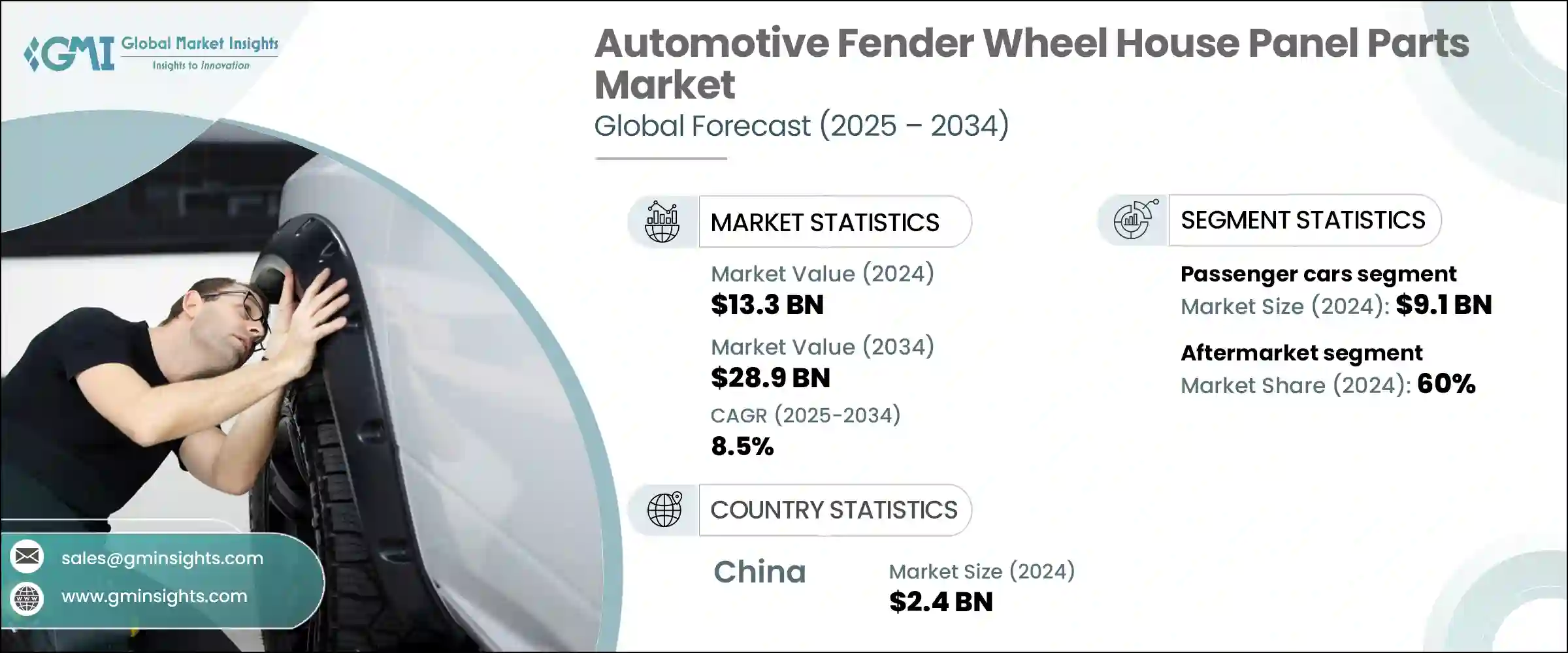

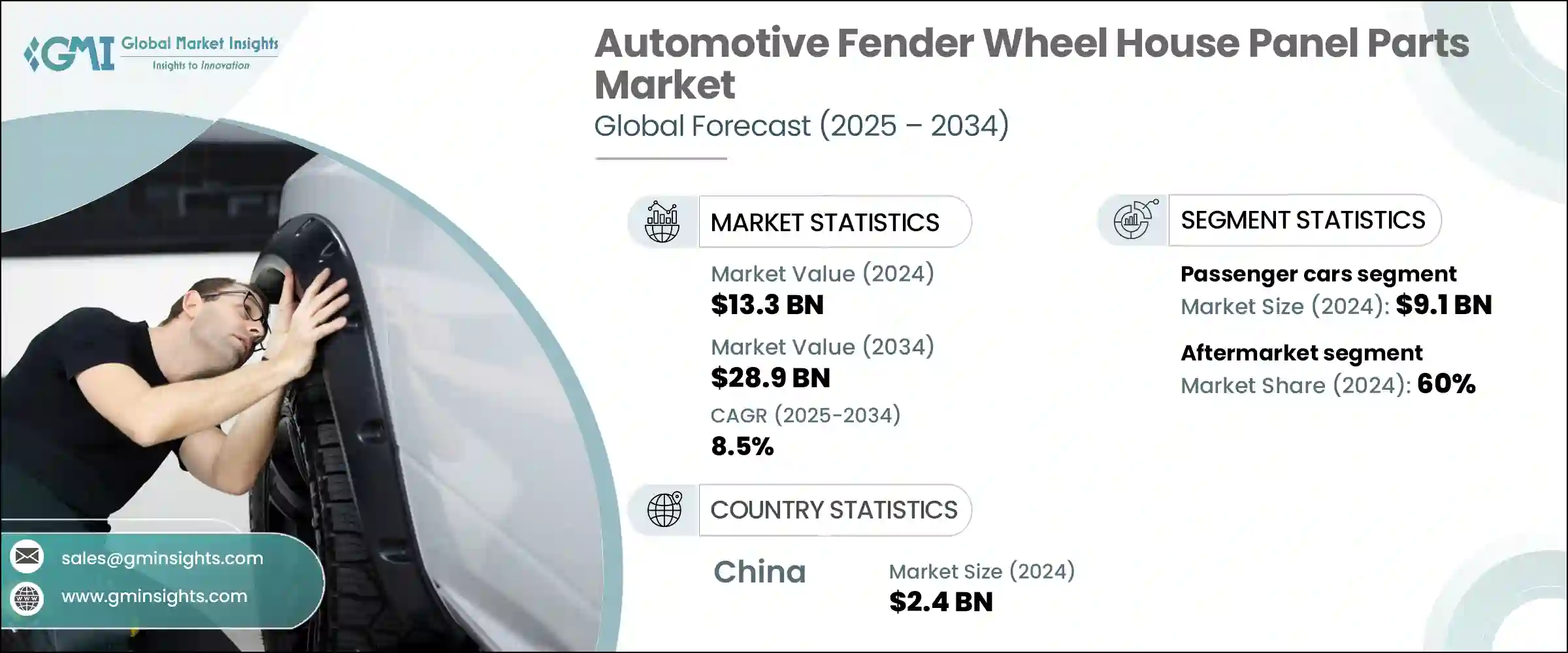

세계의 자동차 펜더 휠하우스 패널 부품 시장 규모는 2024년에 133억 달러에 달하였고, CAGR 8.5%로 성장하여 2034년에는 289억 달러에 이를 것으로 예측되고 있습니다.

자동차 제조업체가 자동차의 효율성, 안전성, 디자인의 혁신에 점점 주력하고 있으며, 따라서 시장은 꾸준히 확대되고 있습니다. 펜더 부품은 공기저항을 줄여 공기역학을 향상시킬 뿐만 아니라 도로의 요소나 파편으로부터 차량의 하부를 보호합니다.

자동차 제조업체는 차량 전체의 무게를 줄이기 위해 강철에서 복합재료, 열가소성 플라스틱, 알루미늄 등의 경량 대체 재료로 전환하고 있습니다. 이는 가벼운 구조로 항속거리를 늘릴 수 있는 전기자동차 분야에서 특히 중요합니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 133억 달러 |

| 예측금액 | 289억 달러 |

| CAGR | 8.5% |

이러한 기능 강화는 소음 저감과 효율이 세일즈 포인트인 전기자동차나 고성능 모델에 특히 유익합니다. 제조업체가 국제적인 에너지 기준 준수에 대한 노력을 지속하는 가운데 모듈식 조립 기술도 대두하고 있으며 복수의 부품을 1개의 유닛에 통합하여 신속한 제조와 용이한 설치를 가능하게 하고 있습니다.

승용차 부문은 2024년에 91억 달러를 창출하였습니다. 이 부문은 특히 개인 이동이 증가하고 있는 라틴아메리카와 아시아태평양과 같은 지역에서 번영을 지속하고 있습니다. 승용차는 날렵한 디자인과 공기역학 구조에 의존하고 있으며 따라서 향상된 펜더 시스템 수요가 증가하고 있습니다. 그리고 전기자동차나 하이브리드 자동차의 대두에 의해 펜더의 설계 요건도 변화하고 있습니다. 또한, 엄격한 소음 기준을 충족하고 노상의 파편으로부터 보다 뛰어난 보호능력을 제공할 필요성으로 인해 기능성과 안전성 모두의 역할을 하는 다층 펜더 패널의 개발이 제조업체에 요구되고 있습니다.

2024년에는 애프터마켓 분야가 60%의 점유율을 차지하였습니다. 소비자는 온라인 채널, 개인 상점 및 현지 공급업체를 통해 제공되는 비용 효율적인 애프터마켓 옵션의 광범위한 선택에 매료되어 있습니다.

중국의 2024년 자동차 펜더 휠하우스 패널 부품 시장 규모는 24억 달러를 달성하였습니다. 국가 차원에서 지원되는 중국의 전동 이동성에 대한 추진 정책은 자동차 부품에서 첨단 재료와 공기역학 설계의 도입을 촉진하고 있습니다.

세계의 자동차 펜더 휠하우스 패널 부품 시장의 주목할 만한 시장 진출기업은 Kostal Group, Valeo SA, Yazaki Corporation, Flex-N-Gate Corporation, Lear Corporation, Magna International Inc., Aisin Seiki Co., Ltd. 등이 있습니다. 자동차 펜더 휠하우스 패널 부품 시장의 주요 기업은 경쟁력을 유지하기 위해 혁신적인 재료 개발과 고급 제조 기술에 주력하고 있습니다. 그리고 전기자동차 제조사와의 협력을 통해 부품을 전동 드라이브 트레인이나 구조 레이아웃에 맞출 수 있습니다. 기업은 또한 확대하는 지역 수요에 대응하고 비용을 절감하기 위해 신흥시장에서의 생산을 확대하고 있습니다.

목차

제1장 조사방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 영향요인

- 성장 촉진요인

- 차량의 복잡화와 전자제어장치의 통합 증가

- ADAS와 센서 기반 안전 시스템의 발전

- 원격 진단을 가능하게 하는 커넥티드카 기술의 성장

- 전문적인 유지보수가 필요한 전기자동차와 하이브리드 자동차의 보급 증가

- 업계의 잠재적 위험 및 과제

- 고급 진단 도구 및 장비에 대한 고액의 초기 투자

- EV나 ADAS 기술에 대한 숙련 기술자의 부족

- 시장 기회

- AI 기반의 예측 유지보수 시스템 개발

- 스마트 진단에 의한 모바일 플랫폼 확장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산통계

- 생산거점

- 소비거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 지속 가능성과 환경 측면

- 지속 가능한 관행

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경친화적인 노력

- 탄소발자국의 고려

제4장 경쟁구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 프론트 펜더 패널

- 펜더 라이너

- 리어 펜더 패널

- 휠하우스 패널

- 이너 펜더 패널

제6장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 강철

- 플라스틱

- 알루미늄

- 복합

- 탄소섬유

제7장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 세단

- 해치백

- SUV

- 상용차

- 소형상용차

- 중형상용차

- 대형상용차

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 자동차 부품 판매 및 도매업체

- 플릿 오퍼레이터

- 정부 및 지방자치단체

- 특수차량 제조업체

- DIY 또는 취미용

- 기타

제9장 시장 추계 및 예측 : 판매채널별(2021-2034년)

- 주요 동향

- 애프터마켓

- OEM

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Aisin Seiki

- Dongfeng Liuzhou

- Dongfeng Motor

- Ficosa International

- Flex-N-Gate

- Gestamp Automocion

- Hyundai Mobis

- Inteva Products

- Kostal

- Lear Corporation

- Magna International

- Martinrea International

- Plastic Omnium

- Sanden

- Siemens

- Schaeffler

- Toyoda Gosei

- Toyota Boshoku

- Valeo

- Yazaki

The Global Automotive Fender Wheel House Panel Parts Market was valued at USD 13.3 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 28.9 billion by 2034. The market is experiencing steady expansion as automakers increasingly focus on vehicle efficiency, safety features, and design innovation. Fender components, including liners, front and rear fenders, and wheel house panels, are essential for both visual appeal and functional performance. These parts not only help reduce wind resistance and increase aerodynamics but also protect vehicles' underbodies from road elements and debris. Stricter crash safety regulations and design demands have made them more critical in new vehicle platforms, especially as carmakers aim for stronger, more aerodynamic vehicle builds.

Automotive manufacturers are transitioning from steel to lighter alternatives like composites, thermoplastics, and aluminum to reduce overall vehicle weight. This shift plays a critical role in supporting fuel efficiency, which is especially vital in the electric vehicle space, where lighter structures can boost driving range. The trend toward aerodynamic paneling is also shaping product development, as smooth fender contours and integrated wheel arches improve airflow and reduce energy consumption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.3 Billion |

| Forecast Value | $28.9 Billion |

| CAGR | 8.5% |

These enhancements are particularly beneficial for electric and high-performance models, where noise reduction and efficiency are selling points. As manufacturers continue adapting to international energy standards, modular assembly techniques are also gaining ground, allowing multiple components to be integrated into single units for quicker manufacturing and easier installation.

The passenger vehicles segment generated USD 9.1 billion in 2024. This segment continues to thrive, particularly in regions like Latin America and the Asia Pacific, where personal mobility is on the rise. Passenger vehicle types such as sedans, SUVs, and hatchbacks increasingly rely on sleek designs, aerodynamic styling, and lighter materials, driving up demand for enhanced fender systems. The rise of electric and hybrid passenger models is also reshaping Fender design requirements, as newer vehicles require lighter and structurally unique panel configurations. Additionally, the need to meet strict noise standards and provide better protection from road debris is encouraging manufacturers to develop multilayered fender panels that serve both functional and safety roles.

In 2024, the aftermarket segment held a 60% share. This sector continues to grow due to the consistent demand for replacement parts following minor accidents, aging vehicles, or wear and tear. Exterior body parts like wheel house panels and fenders are among the most replaced, especially in areas prone to harsh weather or heavy traffic. Consumers are drawn to the wide selection of cost-effective aftermarket options offered through online channels, independent shops, and local suppliers. The aftermarket also enables consumers to customize or repair their vehicles affordably, particularly in areas with high car ownership but limited warranties.

China Automotive Fender Wheel House Panel Parts Market generated USD 2.4 billion in 2024. The country remains a powerhouse in vehicle manufacturing, particularly in the passenger and EV categories, fueled by growing consumer demand and continued investment in automotive production. China's push toward electric mobility, backed by strong government support and national energy goals, is encouraging the use of advanced materials and aerodynamic designs in vehicle parts. The country's robust supply chain and cost-effective production capabilities are key advantages, making it a leading exporter of both metal and composite fender parts.

Notable market participants in the Global Automotive Fender Wheel House Panel Parts Market include Kostal Group, Valeo S.A., Yazaki Corporation, Flex-N-Gate Corporation, Lear Corporation, Magna International Inc., Aisin Seiki Co., Ltd., among others. Leading companies in the automotive fender wheel house panel parts market are focusing on innovative material development and advanced manufacturing techniques to stay competitive. Many are investing in lightweight composite technologies and modular panel systems that improve assembly time and vehicle aerodynamics. Partnerships with EV manufacturers allow suppliers to tailor parts to electric drivetrains and structural layouts. Firms are also expanding production in emerging markets to meet growing regional demand and reduce costs. To cater to the aftermarket, businesses are diversifying their offerings by introducing customizable, durable, and affordable components.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Vehicle

- 2.2.5 End Use

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing vehicle complexity and integration of electronic control units

- 3.2.1.2 Advancements in ADAS and sensor-based safety systems

- 3.2.1.3 Growth in connected car technologies enabling remote diagnostics

- 3.2.1.4 Rising adoption of electric and hybrid vehicles requiring specialized maintenance

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment in advanced diagnostic tools and equipment

- 3.2.2.2 Shortage of skilled technicians trained in EVs and ADAS technologies

- 3.2.3 Market Opportunities

- 3.2.3.1 Development of AI-based predictive maintenance systems

- 3.2.3.2 Expansion of mobile platforms with smart diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Front fender panels

- 5.3 Fender liners

- 5.4 Rear fender panels

- 5.5 Wheel house panels

- 5.6 Inner fender panels

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Plastic

- 6.4 Aluminum

- 6.5 Composite

- 6.6 Carbon Fiber

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 Sedans

- 7.2.2 Hatchbacks

- 7.2.3 SUV

- 7.3 Commercial Vehicles

- 7.3.1 Light Commercial Vehicles

- 7.3.2 Medium Commercial Vehicles

- 7.3.3 Heavy Commercial Vehicles

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Automotive part distributor and wholesaler

- 8.3 Fleet operators

- 8.4 Government and municipal bodies

- 8.5 Specialty vehicle manufacturers

- 8.6 DIY enthusiasts and hobbyists

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Aftermarket

- 9.3 OEM

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 Dongfeng Liuzhou

- 11.3 Dongfeng Motor

- 11.4 Ficosa International

- 11.5 Flex-N-Gate

- 11.6 Gestamp Automocion

- 11.7 Hyundai Mobis

- 11.8 Inteva Products

- 11.9 Kostal

- 11.10 Lear Corporation

- 11.11 Magna International

- 11.12 Martinrea International

- 11.13 Plastic Omnium

- 11.14 Sanden

- 11.15 Siemens

- 11.16 Schaeffler

- 11.17 Toyoda Gosei

- 11.18 Toyota Boshoku

- 11.19 Valeo

- 11.20 Yazaki