|

시장보고서

상품코드

1773392

유기종자 품종 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Organic Seed Varieties Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

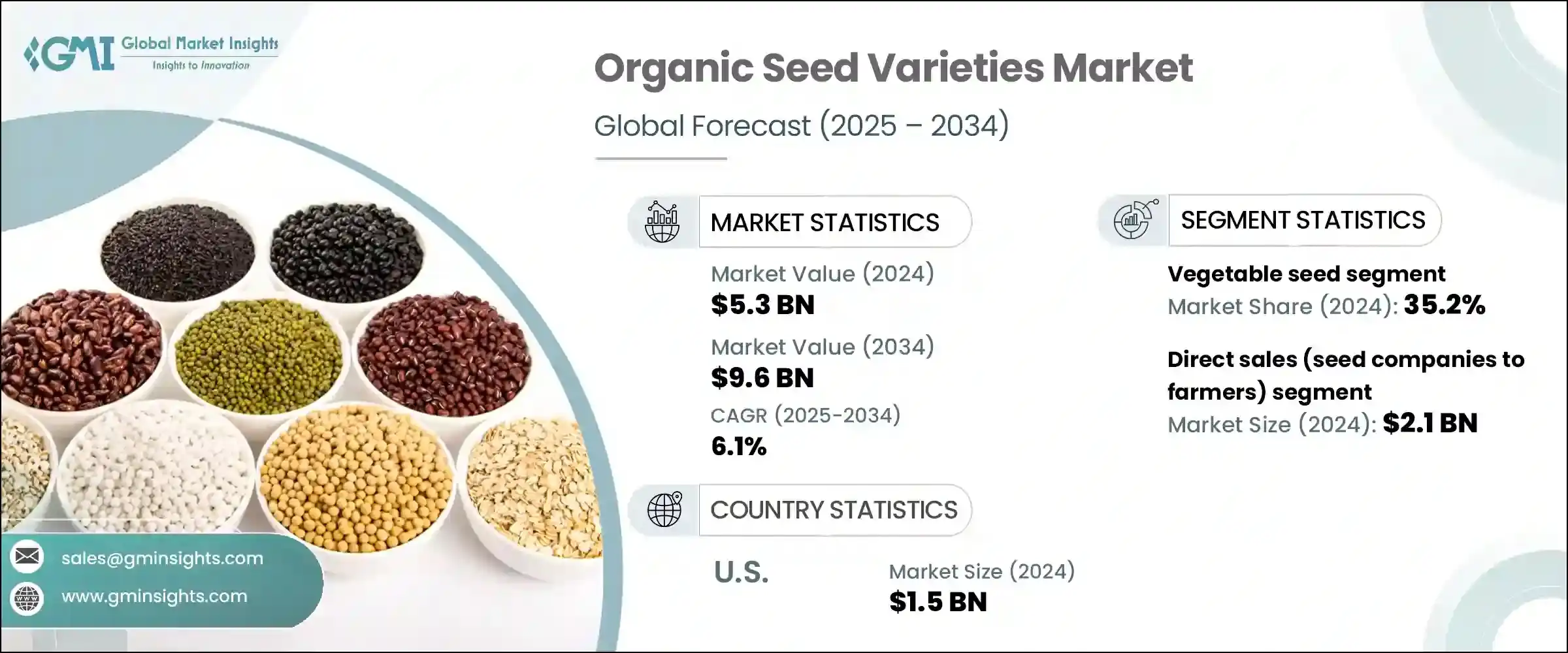

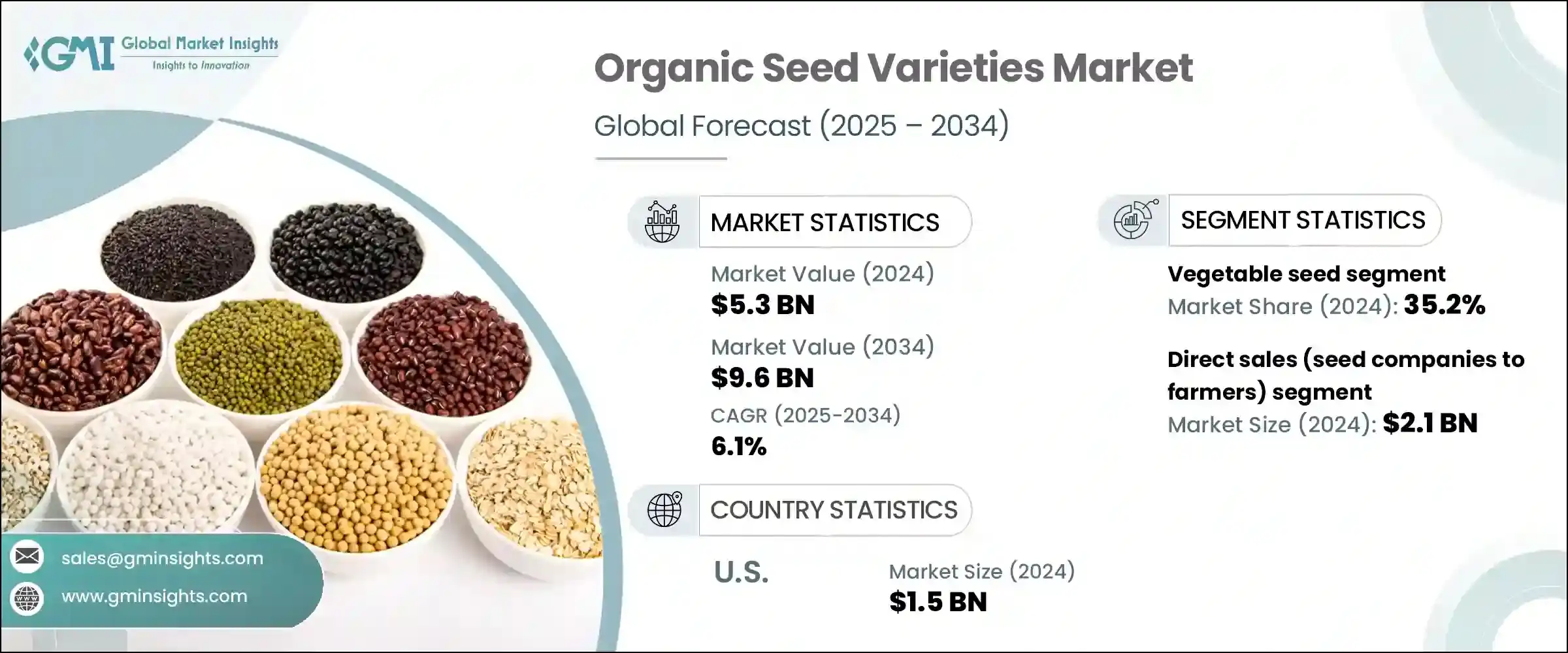

세계의 유기종자 품종 시장은 2024년에는 53억 달러에 달하였고, CAGR 6.1%로 성장하여 2034년에는 96억 달러에 이를 것으로 추정됩니다.

이 성장의 원동력이 되고 있는 것은 건강, 지속 가능성, 식량 안보를 둘러싼 소비자의 의식 고조입니다. 유기종자에 대한 수요는 증가의 길을 걷고 있습니다. 유기농 종자는 일반적으로 토착 품종과 특정 기후에 적합한 품종이며, 농가의 어려운 환경 하에서 작물 재배 능력을 높여 식량 안보에 공헌하고 있습니다. 종자주권 유지에도 도움이 되며 농업에서 유전적 다양성을 유지하는 데 필수적입니다.

지속 가능성과 식량 안보에 대한 우려가 계속 높아지는 가운데 세계 각국의 정부는 유기농업에 대한 지원을 강화하고 있습니다. 이는 종자산업의 성장을 가속화하고 대규모 생산자와 영세농가 모두 유기농법으로의 이행을 촉진하는데 중요한 역할을 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 53억 달러 |

| 예측금액 | 96억 달러 |

| CAGR | 6.1% |

채소종자(종자회사에서 농가) 부문은 2024년에 35.2%의 점유율을 차지했습니다. 해당 부분의 성장세는 CAGR 6.4%로 견조하게 확대될 것으로 예측됩니다. 건강 지향이 높아지고 무농약 채소를 요구하는 개인이 늘어남에 따라 가정에서 재배하는 사람과 상업 농가 모두 유기농 채소의 품종에 주목하고 있습니다.

직접판매 부문은 2024년 21억 달러로 평가되었으며 2034년까지 연평균 복합 성장률(CAGR) 6.3%를 보일 것으로 예측됩니다. 이 모델은 종자 생산자가 개별 농가의 독자적인 요구에 대응하는 맞춤형 솔루션을 제공할 수 있는 개별 서비스를 제공하면서 지지되고 있습니다. 또한 고객과 보다 견고한 관계와 높은 고객 만족도를 제공합니다. 그리고 전문가의 조언, 물류 지원, 맞춤형 배송 옵션을 제공할 수 있는 것도 직접판매의 성공에 공헌하고 있어 대규모 농업 경영자와 소규모 독립 농가 모두에게 선호되는 채널이 되고 있습니다.

미국의 2024년 유기종자 품종 시장 규모는 15억 달러를 달성하였습니다. 유기농 농산물에 대한 수요는 정부의 유리한 정책과 강력한 유기농 공급 체인과 결합하여 이러한 성장을 지원하고 있습니다. 농민들이 규제를 준수하기 위해 유기종자 생산을 채택하고 있으며, 종자회사는 제품 제공의 혁신과 확대를 계속하고 있습니다.

세계의 유기종자 품종 시장의 주요 기업은 Farm Direct Organic Seeds, Baker Creek Heirloom Seeds, Fedco Seeds, High Mowing Organic Seeds, Johnny's Selected Seeds 등입니다. 유기종자 품종 시장의 각사는 그 지위를 강화하기 위해 특정의 환경 조건이나 소비자의 기호에 대응하고 고품질로 현지에 적합한 종자 품종의 제공에 주력하고 있습니다. 종자의 보존 기술 혁신과 탄력성이 있는 신품종의 개발은 각사의 전략 핵심 요소입니다. 또, 많은 기업이 직접판매를 통해 농가와의 관계를 강화하고 농가의 요구를 확실히 충족하기 위한 개별 서비스를 제공합니다.

목차

제1장 조사방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 북미 : 유기농 소비자의 주류화

- 유럽 : 지속 가능한 식량 생산 관행이 유기 종자 수요를 밀어올림

- 아시아태평양 : 유기농업으로의 전환

- 업계의 잠재적 위험 및 과제

- 유기종자 품종의 입수가 한정적

- 가격 프리미엄과 인증 부담

- 시장 기회

- 작물 다양화와 틈새 시장 성장

- 지역 번식과 기후 적응

- 디지털화와 소비자 직접판매 채널

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 작물 유형별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속 가능성과 환경 측면

- 지속 가능한 관행

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경친화적인 노력

- 밸류체인 분석

- 종자의 육종과 생산

- 인증 및 테스트

- 유통과 소매

- 최종 용도 부문(상업 재배자, 소규모 농가, 가정 재배자)

- 지속 가능성과 생물다양성

- 농업 생태학과 식량 안보에서 유기종자의 역할

- 생물다양성 보전의 대처

- 종자주권과 지역 종자 시스템

- 인증 및 규제

- USDA NOP 인증 유기종자

- EU 인증 유기종자

- 기타 국가 및 지역의 인증

- 비유전자 재조합 인증 종자

- 종자 처리 및 코팅(유기농 등급)

- 컴플라이언스 비용과 시장에 미치는 영향

제4장 경쟁구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 작물별(2021-2034년)

- 주요 경향

- 채소종자

- 양상추

- 토마토

- 시금치

- 당근

- 오이

- 피망

- 곡물종자

- 밀

- 옥수수

- 쌀

- 보리

- 귀리

- 기장

- 퀴노아

- 과일종자

- 멜론

- 수박

- 딸기

- 베리류

- 허브와 꽃의 종자

- 바질

- 고수

- 파슬리

- 해바라기

- 백일홍

- 마리골드

- 유지종 및 대체 곡물

- 콩

- 아마

- 메밀

- 아마란스

- 참깨

제6장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 경향

- 직접판매(종자회사에서 농가)

- 소매 채널(원예센터, 농업용품점)

- 온라인 판매 및 전자상거래 플랫폼

- 협동조합과 공동구매

- 도매업체 및 기관 투자자

제7장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제8장 기업 프로파일

- Adaptive Seeds

- Baker Creek Heirloom Seeds

- Eden Seeds

- Farm Direct Organic Seeds

- Fedco Seeds

- High Mowing Organic Seeds

- Johnny's Selected Seeds

- Kusa Seed Society

- Quality Organic

- Resilient Seeds

- Seed Savers Exchange

- Southern Exposure Seed Exchange

- Victory Seeds

- Vitalis Organic Seeds

The Global Organic Seed Varieties Market was valued at USD 5.3 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 9.6 billion by 2034. This growth is being driven by increasing consumer awareness surrounding health, sustainability, and food security. As more people shift toward healthier lifestyles and environmentally conscious choices, the demand for organic seeds continues to rise. Organic farming is gaining momentum as a key strategy to preserve biodiversity, reduce chemical use, and promote resilient agricultural practices. Organic seeds, typically heirloom varieties or those well-suited to specific climates, contribute to food security by enhancing farmers' ability to grow crops in challenging environments. They also help to maintain seed sovereignty and are vital in maintaining genetic diversity in agriculture. Climate change has highlighted the importance of resilient crops that can endure unpredictable weather, further boosting the market.

Moreover, as concerns about sustainability and food security continue to rise, governments globally are intensifying their support for organic farming. This includes increased funding, grants, and policy initiatives designed to promote organic seed production and facilitate the transition toward eco-friendly agricultural practices. Such government backing plays a critical role in fostering the growth of the organic seed industry, encouraging both large-scale producers and smallholder farmers to shift towards organic farming methods. These efforts not only help ensure the long-term sustainability of agriculture but also support the broader goals of biodiversity conservation and reduced chemical usage in farming.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.3 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 6.1% |

The vegetable seed (seed companies to farmers) segment held a 35.2% share in 2024. This segment is projected to expand at a solid CAGR of 6.4% over the next decade, reflecting growing consumer preferences for organic, locally grown produce. As more individuals become health-conscious and seek chemical-free vegetables, both home gardeners and commercial farmers are increasingly turning to organic vegetable seed varieties. This trend is driving demand for vegetable seeds, which are considered essential for promoting better nutrition and healthier eating habits.

The direct sales segment was valued at USD 2.1 billion in 2024 and is expected to grow at a CAGR of 6.3% through 2034. This model is favored for its personalized service, allowing seed producers to offer tailored solutions that address the unique needs of individual farmers. By eliminating intermediaries, direct sales help ensure that customers receive products in a timely manner, fostering stronger relationships and higher levels of customer satisfaction. The ability to offer expert advice, logistical support, and customized delivery options also contributes to the success of direct sales, making it a preferred channel for both large-scale agricultural operations and smaller, independent farmers.

U.S. Organic Seed Varieties Market was valued at USD 1.5 billion in 2024. The demand for organic produce, coupled with favorable government policies and a strong organic supply chain, supports this growth. As organic farming standards become more stringent, many farmers are adopting organic seed production to comply with regulations, while seed companies continue to innovate and expand their product offerings. With large-scale agricultural operations and a growing number of organic farms, the U.S. market is poised for continued expansion.

The top players in the Global Organic Seed Varieties Market include Farm Direct Organic Seeds, Baker Creek Heirloom Seeds, Fedco Seeds, High Mowing Organic Seeds, and Johnny's Selected Seeds. To strengthen their position, companies in the organic seed varieties market are focusing on offering high-quality, locally adapted seed varieties that cater to specific environmental conditions and consumer preferences. Innovations in seed preservation and the development of new, resilient varieties are central to their strategies. Furthermore, companies are increasingly investing in research and development to improve seed yield and disease resistance. Many are also building stronger relationships with farmers through direct sales and providing personalized services to ensure farmers' needs are met. Environmental sustainability and supporting local economies have become key selling points for companies, as they appeal to both eco-conscious consumers and farmers looking for sustainable solutions.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Crop type

- 2.2.3 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 North America: organic consumers are increasingly mainstream

- 3.2.1.2 Europe: sustainable food production practices to boost the demand of organic seeds

- 3.2.1.3 Asia pacific: transformation towards organic agriculture practices

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited organic variety availability

- 3.2.2.2 Price premiums and certification burden

- 3.2.3 Market opportunities

- 3.2.3.1 Crop diversification and niche market growth

- 3.2.3.2 Regional breeding and climate adaptation

- 3.2.3.3 Digitalization and direct-to-consumer channels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By crop type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Value chain analysis

- 3.13.1 Seed breeding and production

- 3.13.2 Certification and testing

- 3.13.3 Distribution and retail

- 3.13.4 End use segments (commercial growers, smallholders, home gardeners)

- 3.14 Sustainability and biodiversity

- 3.14.1 Role of organic seed in agroecology and food security

- 3.14.2 Biodiversity conservation initiatives

- 3.14.3 Seed sovereignty and local seed systems

- 3.15 Certification and regulation

- 3.15.1 USDA NOP certified organic seeds

- 3.15.2 EU organic certified seeds

- 3.15.3 Other national and regional certifications

- 3.15.4 Non-GMO verified seeds

- 3.15.5 Seed treatment and coating (Organic-Compliant)

- 3.15.6 Compliance costs and market impact

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Crop Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trend

- 5.2 Vegetable seeds

- 5.2.1 Lettuce

- 5.2.2 Tomato

- 5.2.3 Spinach

- 5.2.4 Carrot

- 5.2.5 Cucumber

- 5.2.6 Bell pepper

- 5.3 Grain seeds

- 5.3.1 Wheat

- 5.3.2 Corn

- 5.3.3 Rice

- 5.3.4 Barley

- 5.3.5 Oats

- 5.3.6 Millet

- 5.3.7 Quinoa

- 5.4 Fruit seeds

- 5.4.1 Melon

- 5.4.2 Watermelon

- 5.4.3 Strawberry

- 5.4.4 Berry varieties

- 5.5 Herb and flower seeds

- 5.5.1 Basil

- 5.5.2 Cilantro

- 5.5.3 Parsley

- 5.5.4 Sunflower

- 5.5.5 Zinnia

- 5.5.6 Marigold

- 5.6 Oilseed and alternative grains

- 5.6.1 Soybean

- 5.6.2 Flax

- 5.6.3 Buckwheat

- 5.6.4 Amaranth

- 5.6.5 Sesame

Chapter 6 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Litres)

- 6.1 Key trend

- 6.2 Direct sales (seed companies to farmers)

- 6.3 Retail channels (garden centres, farm supply stores)

- 6.4 Online sales and e-commerce platforms

- 6.5 Cooperatives and buying clubs

- 6.6 Wholesale and institutional buyers

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Litres)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East & Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East & Africa

Chapter 8 Company Profiles

- 8.1 Adaptive Seeds

- 8.2 Baker Creek Heirloom Seeds

- 8.3 Eden Seeds

- 8.4 Farm Direct Organic Seeds

- 8.5 Fedco Seeds

- 8.6 High Mowing Organic Seeds

- 8.7 Johnny's Selected Seeds

- 8.8 Kusa Seed Society

- 8.9 Quality Organic

- 8.10 Resilient Seeds

- 8.11 Seed Savers Exchange

- 8.12 Southern Exposure Seed Exchange

- 8.13 Victory Seeds

- 8.14 Vitalis Organic Seeds