|

시장보고서

상품코드

1773406

타일 접착제 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Tile Adhesive Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

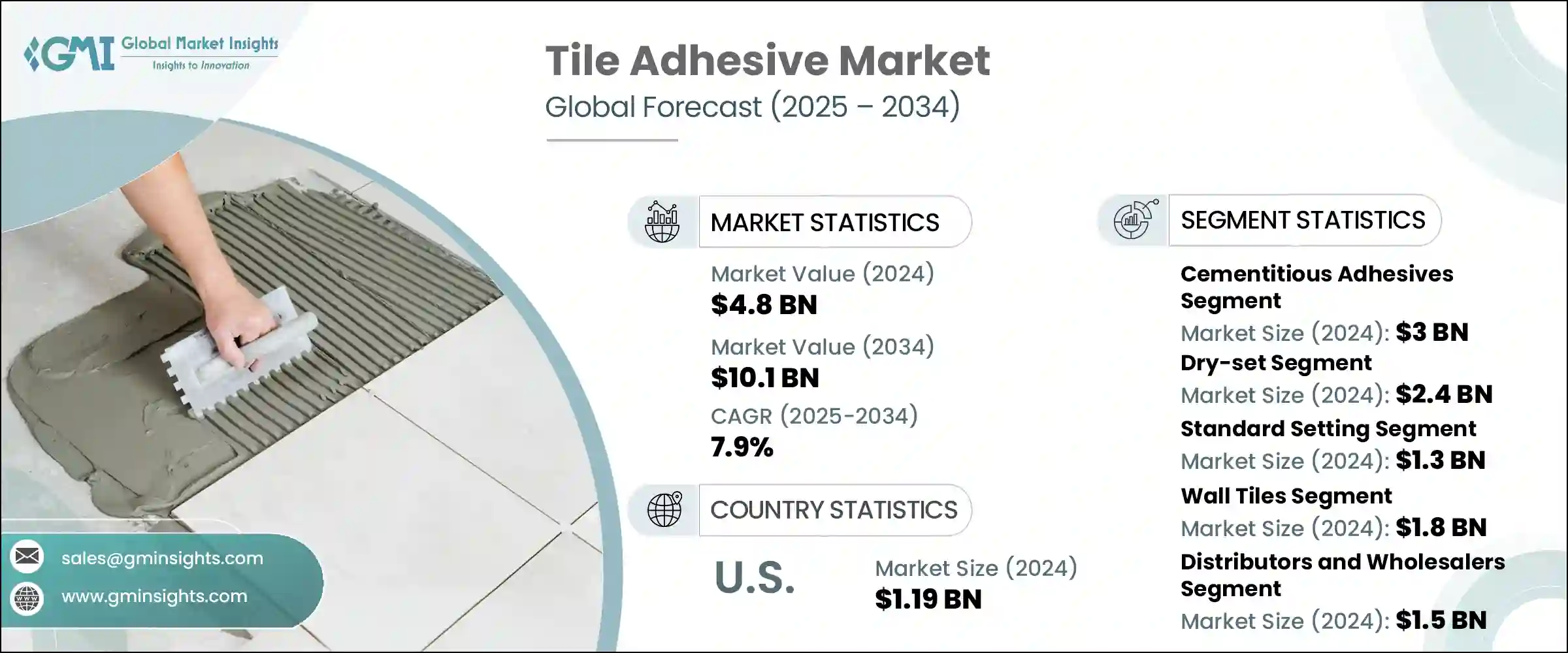

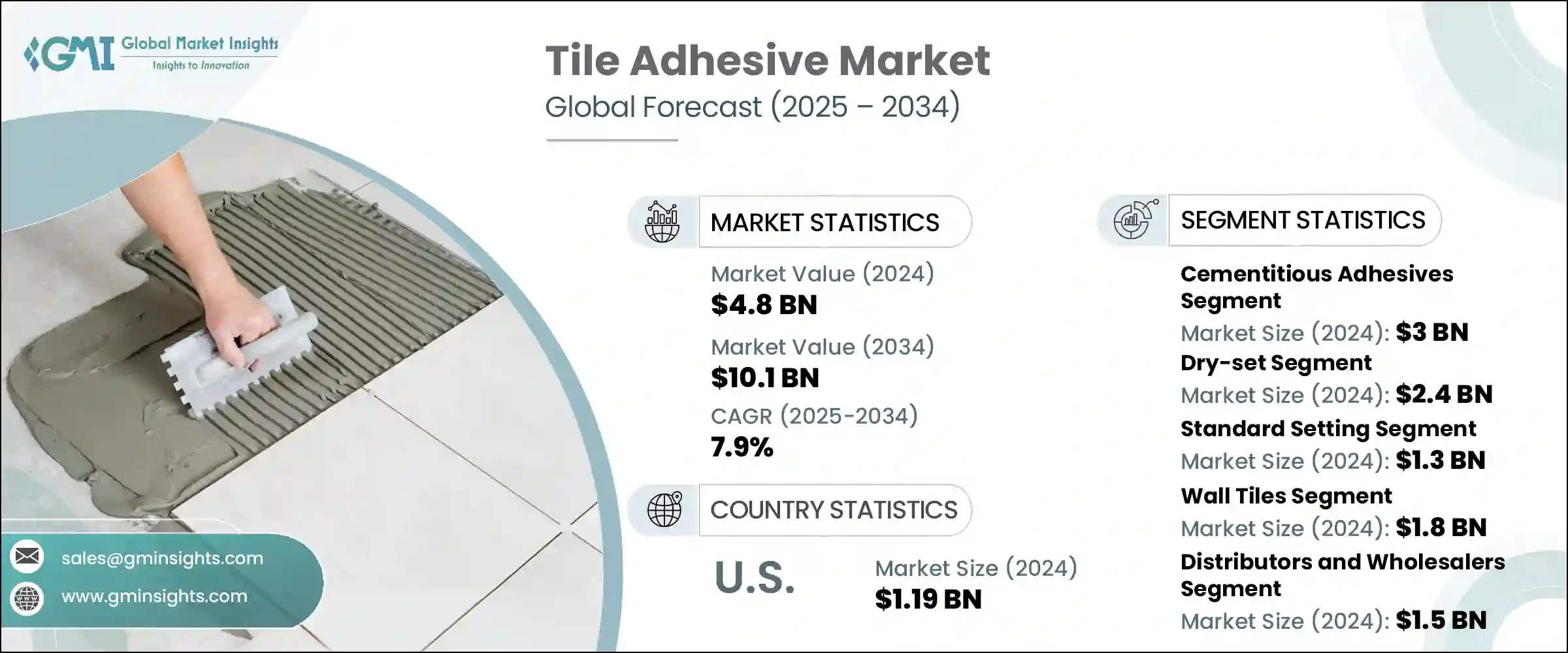

세계의 타일 접착제 시장 규모는 2024년에 48억 달러를 달성하였고, CAGR 7.9%로 성장하여 2034년에는 101억 달러에 달할 것으로 예측되고 있습니다.

이 성장은 개발도상지역과 선진지역 모두에서 건설활동이 활발해지고 있는 추세에 강하게 영향을 받고 있습니다. 뛰어난 접착 강도, 시공의 용이성, 그리고 뛰어난 효율성으로 기존의 시멘트계 솔루션을 대체하고 있습니다.

미국과 유럽에서는 특히 노후화된 물건의 주택 개수와 리폼의 급증도 수요에 기여하고 있습니다. 접착제의 배합에서 특히 폴리머의 혁신에 의해 건조 시간의 단축, 유연성의 향상, 내열성의 개선 등 보다 가벼운 제품이 만들어지고 있습니다. 이러한 진보는 시공 시간이나 재료의 낭비를 줄일 뿐만 아니라, 시공 시의 에너지 소비를 줄여 환경 목표도 달성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 48억 달러 |

| 예측금액 | 101억 달러 |

| CAGR | 7.9% |

2024년 시멘트계 접착제 부문은 30억 달러를 창출하였고 2034년까지의 예측 CAGR은 7.1%로 강력한 성장을 유지할 것으로 예측됩니다. 시멘트계 접착제는 상업과 주택 건설 모두를 위한 적응성을 위해 선호되는 선택입니다. 시멘트계 접착제는 대형 타일과 습기가 발생하기 쉬운 영역을 포함한 설치용으로 향상된 성능을 제공하여 점점 일반화되어 왔습니다. 건설 공법이 더 엄격한 성능 기준을 충족하도록 진화함에 따라 이러한 업그레이드된 시멘트계 접착제는 여러 프로젝트 유형 및 지역 시장에서 지배적인 역할을 유지하고 있습니다.

표준 경화성 접착제 부문은 2024년에 13억 달러로 평가되었으며, 2034년까지 5.9%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 일반적인 건축에서는 표준 경화성 접착제가 널리 사용되고 있습니다. 그러나 상업시설의 개수나 공공시설의 업그레이드 등 일분일초가 중요한 환경에서는 완성을 앞당기고 다운타임을 단축할 수 있는 속경화성 접착제가 선호됩니다.

미국의 2024년 타일 접착제 시장 규모는 11억 9,000만 달러였으며, 2034년까지 7.6%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되고 있습니다. 건축 관행을 중시하는 국민성과 더불어, 주택 및 상업시설의 건설 활동이 증가하고 있는 것이 성장에 기여하고 있습니다. 미국의 소비자는 인테리어의 외관을 개선할 뿐만 아니라 오래 지속되는 내구성을 갖춘 제품에 높은 가치를 두고 있습니다.

세계의 타일 접착제 시장에서 경쟁구도는 Ardex Group, Sika AG, Laticrete International, Inc., Saint-Gobain Weber, Mapei SpA 등의 대기업에 의해 형성되고 있습니다.

타일 접착제 시장의 주요 기업은 기술 혁신, 제휴, 지역 확대를 혼합하여 시장 내 지위를 유지하기 위해 적극적으로 노력하고 있습니다. 각사는 새로운 배합을 경량 타일이나 습기가 많은 장소에서의 시공 등 현대적인 건축 요건에 맞추어 조정하고 있습니다.

목차

제1장 조사방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속 가능성과 환경 측면

- 지속 가능한 실천

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경친화적인 노력

- 탄소발자국의 고려

제4장 경쟁구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 화학 유형별(2021-2034년)

- 주요 동향

- 시멘트계 접착제

- 표준 시멘트질(C1)

- 개량 시멘트질(C2)

- 속경화 시멘트질

- 기타

- 분산 접착제

- 표준 분산(D1)

- 분산 개선(D2)

- 기타

- 반응성 수지 접착제

- 에폭시계

- 폴리우레탄계

- 기타

- 기타

제6장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 건식

- RTU(Ready-to-Use)

- 2성분

- 기타

제7장 시장 추계 및 예측 : 기능별(2021-2034년)

- 주요 동향

- 표준

- 속건

- 유연/변형 가능

- 방활성

- 내수성

- 방한성

- 기타

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 벽 타일

- 내벽

- 외벽

- 기타

- 바닥 타일

- 실내 바닥

- 실외 바닥

- 기타

- 씰링

- 수영장과 습지대

- 기타

제9장 시장 추계 및 예측 : 타일 유형별(2021-2034년)

- 주요 동향

- 세라믹 타일

- 도자기 타일

- 천연석 타일

- 대리석

- 화강암

- 슬레이트

- 기타

- 유리 타일

- 모자이크 타일

- 대형 타일

- 기타

제10장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 주택용

- 신축

- 리노베이션과 리모델링

- 기타

- 상업용

- 사무용 빌딩

- 상가

- 접객

- 의료시설

- 교육기관

- 기타

- 산업

- 제조시설

- 창고

- 기타

- 기관

- 정부청사

- 종교시설

- 기타

- 기타

제11장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 직접판매

- 판매자 및 도매업체

- 철물점

- 전문점

- 온라인 소매

제12장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제13장 기업 프로파일

- Sika AG

- Mapei SpA

- Ardex Group

- Laticrete International, Inc.

- Saint-Gobain Weber

- HB Fuller Company

- Bostik SA(Arkema Group)

- Henkel AG &Co. KGaA

- Pidilite Industries Ltd.

- Wacker Chemie AG

- Custom Building Products

- Parex Group(Sika AG)

- Fosroc International Ltd.

- Kerakoll SpA

- 3M Company

The Global Tile Adhesive Market was valued at USD 4.8 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 10.1 billion by 2034. This growth is strongly influenced by rising construction activity across both developing and developed regions. As urban infrastructure expands and new commercial and residential projects break ground, demand for high-performance, time-saving building materials continues to rise. Tile adhesives are rapidly replacing conventional cement-based solutions due to their superior bond strength, easier application, and efficiency. Large urbanization efforts, especially in fast-growing areas across the Middle East and Asia-Pacific, have made these products essential for modern building practices.

In the U.S. and Europe, a surge in home improvement and remodeling efforts, particularly in aging properties, is also contributing to demand. Renovation projects are increasingly using tile adhesives in kitchens, bathrooms, and high-traffic interiors due to their resistance to moisture and their compatibility with a range of materials. Additionally, innovation in adhesive formulations-especially with polymers-has resulted in lighter products with faster drying times, enhanced flexibility, and improved thermal resistance. These advancements not only reduce installation time and material waste but also support environmental goals by lowering energy use during application.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 7.9% |

In 2024, the cementitious adhesives segment generated USD 3 billion and is expected to maintain strong growth with a projected CAGR of 7.1% through 2034. These adhesives remain a preferred choice due to their cost-effectiveness, durability, and adaptability for both commercial and residential construction. Their widespread use in developing nations reflects their affordability and proven strength. Polymer-modified variants have become increasingly common, offering enhanced performance for installations involving large-format tiles or moisture-prone areas. Their improved flexibility and water resistance make them ideal for modern building applications. As construction methods evolve to meet more demanding performance criteria, these upgraded cementitious adhesives are securing a dominant role across multiple project types and geographic markets.

The standard-setting adhesives segment was valued at USD 1.3 billion in 2024 and is expected to grow at a CAGR of 5.9% during 2034. The choice between standard and fast-setting adhesives depends heavily on the nature of the project and the required timelines. For typical construction where schedules allow, standard-setting adhesives are widely used because they provide strong adhesion and ample working time. However, in time-sensitive environments-such as commercial refurbishments or public facility upgrades-fast-setting adhesives are preferred for their ability to expedite completion and reduce downtime. As commercial spaces and retail outlets often demand minimal operational disruption, the demand for high-performance, quick-curing adhesives will continue to rise.

United States Tile Adhesive Market was valued at USD 1.19 billion in 2024 and is expected to grow at a CAGR of 7.6% through 2034. This expansion is fueled by increasing residential and commercial construction activity, coupled with a national emphasis on sustainable building practices. As older buildings are updated and replaced, there is a growing demand for efficient, environmentally conscious adhesive products. U.S. consumers are placing a higher value on products that not only enhance the appearance of interiors but also offer long-lasting durability. This shift is pushing manufacturers to focus more on advanced, eco-friendly adhesives that meet modern performance standards while aligning with green construction initiatives.

The competitive landscape in the Global Tile Adhesive Market is shaped by major players such as Ardex Group, Sika AG, Laticrete International, Inc., Saint-Gobain Weber, and Mapei S.p.A. These companies are known for their consistent investment in product development and market expansion.

Leading companies in the tile adhesive market are actively working to strengthen their market foothold through a mix of innovation, partnerships, and regional expansion. Product development is a top priority, with many firms investing in advanced polymer-modified adhesives that offer greater durability, water resistance, and flexibility. These new formulations are often tailored for modern building requirements, including lightweight tiles and wet-area installations. In parallel, companies are enhancing their global distribution networks by forming strategic partnerships with contractors and distributors.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Chemical Type

- 2.2.3 Type

- 2.2.4 Feature

- 2.2.5 Application

- 2.2.6 Tile Type

- 2.2.7 End Use Sector

- 2.2.8 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Chemical Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cementitious Adhesives

- 5.2.1 Standard Cementitious (C1)

- 5.2.2 Improved Cementitious (C2)

- 5.2.3 Fast-Setting Cementitious

- 5.2.4 Others

- 5.3 Dispersion Adhesives

- 5.3.1 Standard Dispersion (D1)

- 5.3.2 Improved Dispersion (D2)

- 5.3.3 Others

- 5.4 Reaction Resin Adhesives

- 5.4.1 Epoxy-Based

- 5.4.2 Polyurethane-Based

- 5.4.3 Others

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Dry-Set

- 6.3 Ready-to-Use

- 6.4 Two-Component

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Feature, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Standard Setting

- 7.3 Fast Setting

- 7.4 Flexible/Deformable

- 7.5 Slip-Resistant

- 7.6 Water-Resistant

- 7.7 Frost-Resistant

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Wall Tiles

- 8.2.1 Interior Walls

- 8.2.2 Exterior Walls

- 8.2.3 Others

- 8.3 Floor Tiles

- 8.3.1 Interior Floors

- 8.3.2 Exterior Floors

- 8.3.3 Others

- 8.4 Ceiling

- 8.5 Swimming Pools and Wet Areas

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Tile Type, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Ceramic Tiles

- 9.3 Porcelain Tiles

- 9.4 Natural Stone Tiles

- 9.4.1 Marble

- 9.4.2 Granite

- 9.4.3 Slate

- 9.4.4 Others

- 9.5 Glass Tiles

- 9.6 Mosaic Tiles

- 9.7 Large Format Tiles

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By End Use Sector, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Residential

- 10.2.1 New Construction

- 10.2.2 Renovation and Remodeling

- 10.2.3 Others

- 10.3 Commercial

- 10.3.1 Office Buildings

- 10.3.2 Retail Spaces

- 10.3.3 Hospitality

- 10.3.4 Healthcare Facilities

- 10.3.5 Educational Institutions

- 10.3.6 Others

- 10.4 Industrial

- 10.4.1 Manufacturing Facilities

- 10.4.2 Warehouses

- 10.4.3 Others

- 10.5 Institutional

- 10.5.1 Government Buildings

- 10.5.2 Religious Buildings

- 10.5.3 Others

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 Direct Sales

- 11.3 Distributors and Wholesalers

- 11.4 Home Improvement Stores

- 11.5 Specialty Stores

- 11.6 Online Retail

Chapter 12 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Rest of Europe

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.4.6 Rest of Asia Pacific

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.5.4 Rest of Latin America

- 12.6 Middle East & Africa

- 12.6.1 Saudi Arabia

- 12.6.2 South Africa

- 12.6.3 UAE

- 12.6.4 Rest of Middle East & Africa

Chapter 13 Company Profiles

- 13.1 Sika AG

- 13.2 Mapei S.p.A.

- 13.3 Ardex Group

- 13.4 Laticrete International, Inc.

- 13.5 Saint-Gobain Weber

- 13.6 H.B. Fuller Company

- 13.7 Bostik SA (Arkema Group)

- 13.8 Henkel AG & Co. KGaA

- 13.9 Pidilite Industries Ltd.

- 13.10 Wacker Chemie AG

- 13.11 Custom Building Products

- 13.12 Parex Group (Sika AG)

- 13.13 Fosroc International Ltd.

- 13.14 Kerakoll S.p.A.

- 13.15 3M Company