|

시장보고서

상품코드

1773426

견착식 무기 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Shoulder Fired Weapons Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

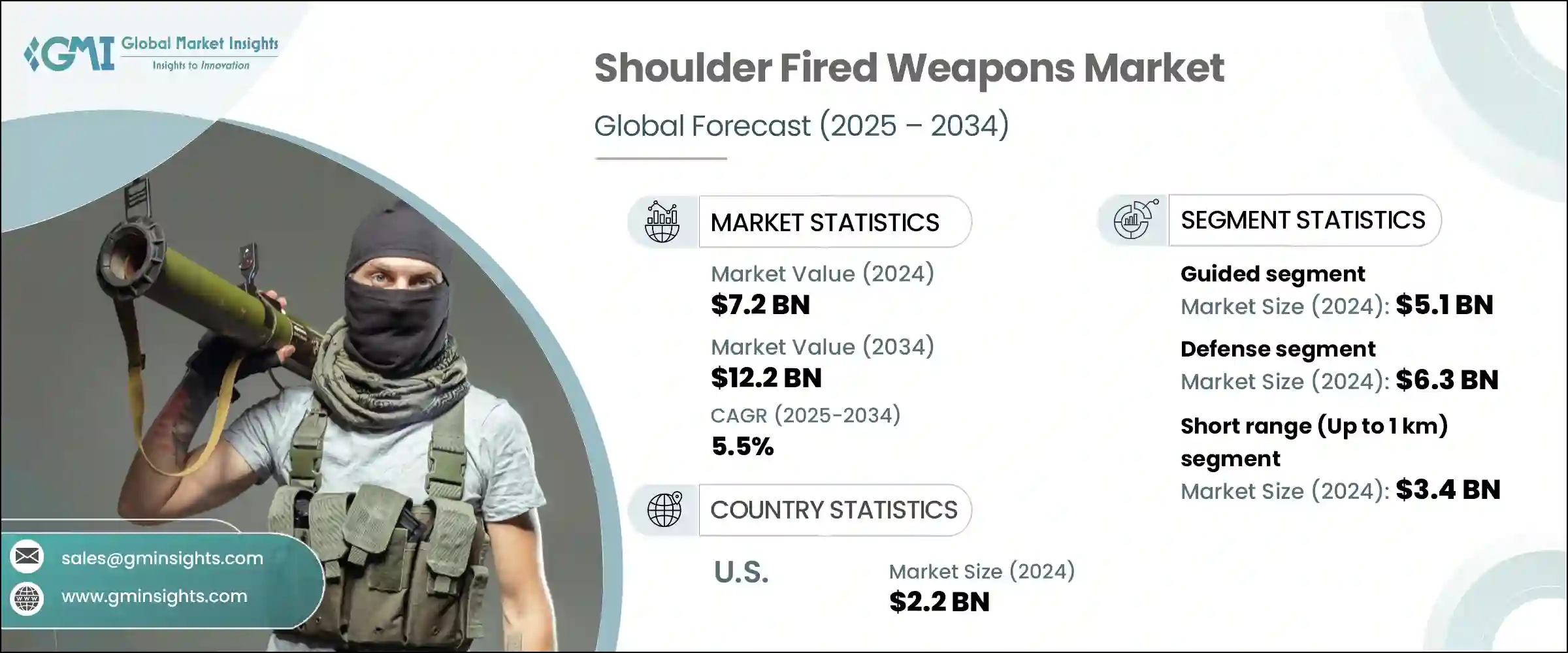

세계의 견착식 무기 시장 규모는 2024년에 72억 달러에 달하며, CAGR 5.5%로 성장하며, 2034년에는 122억 달러에 달할 것으로 예측됩니다.

이러한 성장은 주로 세계 각국의 군 현대화 계획의 강화에 기인합니다. 지정학적 긴장이 고조되고 국경 분쟁이 진행됨에 따라 군가 저렴한 가격에 배치할 수 있는 전력 증강 무기를 요구함에 따라 어깨 발사 무기에 대한 수요가 크게 증가하고 있습니다. 다양한 지역에서의 분쟁과 대치 상황으로 인해 휴대 가능하고 정밀한 대 장갑 및 대공 시스템의 필요성이 증가하고 있습니다. 또한 군의 현대화 노력은 도시 및 비대칭전 시나리오에서 기동성과 효율성을 향상시키는 차세대 경량 무기 개발에 초점을 맞추었습니다. 이러한 프로그램은 향상된 조준 및 발사 중량 감소와 같은 업그레이드를 우선시하고 있으며, 이는 첨단 어깨 발사 미사일에 대한 수요를 촉진하고 있습니다.

세계 전략 방위 구상은 인간형 휴대용 무기 시스템의 연구개발에 막대한 자원을 투입하여 기술 혁신을 가속화하고 역량을 확장하고 있습니다. 이 투자는 현대 전투 시나리오의 요구 사항을 충족하는 보다 진보되고 가볍고 다용도한 어깨 발사 무기를 만드는 데 초점을 맞추었습니다. 정확도 향상, 조준 기술 개선, 휴대성 향상은 이러한 노력을 추진하는 데 있으며, 중요한 우선순위입니다. 군이 다양한 작전 환경에 적응할 수 있는 최첨단 시스템으로 무기를 업그레이드하기 위해 노력하는 가운데, R&D에 대한 자금은 지속적으로 증가하고 있으며, 시장 확대에 박차를 가하고 병사의 효율성과 전장 민첩성의 새로운 기준을 설정하는 획기적인 기술을 육성하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작 금액 | 72억 달러 |

| 예측 금액 | 122억 달러 |

| CAGR | 5.5% |

2024년 시장 규모는 51억 달러로 유도무기 분야가 시장을 주도했습니다. 첨단 지휘통제시스템과 같은 종합적인 방어 네트워크에 유도 어깨 화기가 통합됨에 따라 그 전략적 중요성이 증가하고 있습니다. 이러한 무기는 정확성, 유연성, 실시간 표적 조정 능력을 제공하여 현대 전장에서 필수 불가결한 요소로 자리 잡았습니다. 이러한 통합은 작전의 효율성을 높이고 첨단 유도 시스템에 대한 수요를 자극하여 시장 성장을 가속하고 있습니다.

국방 분야는 2024년 63억 달러 시장을 창출했습니다. 군인의 민첩성과 전투 효율성을 높이기 위해 가볍고 쉽게 배치할 수 있는 무기에 대한 요구가 증가하고 있으며, 어깨 발사 무기가 최전방으로 밀려나고 있습니다. 이러한 시스템은 대 장갑 및 대공 역할에서 점점 더 중요해지고 있으며, 다용도하고 정확한 솔루션으로 구식 무기를 대체하는 것을 목표로 하는 국방 현대화 프로그램의 중심이 되고 있습니다. 정규전과 비정규전에 걸친 적응성으로 인해 다양한 군 분야에서 확고한 입지를 확보하고 있습니다.

미국 어깨 발사 무기 2024년 시장 규모는 22억 달러였습니다. 이 시장의 성장을 촉진하는 것은 미 국방부의 지속적인 첨단 휴대용 시스템 조달입니다. 도시 전투에서 병사의 치명성, 기동성 및 능력 강화에 중점을 둔 프로그램은 어깨 발사 대 장갑 및 대구조물 무기의 지속적인 업그레이드를 촉진하고 있습니다. 시가전 준비태세와 배치에 대한 관심이 높아지면서 수요를 더욱 지원하고 있습니다.

견착식 무기 시장의 주요 기업에는 Lockheed Martin Corporation, RTX, Saab AB, MBDA가 포함됩니다. 어깨 발사 무기 시장의 기업은 시장에서의 입지를 확고히 하기 위해 여러 전략을 채택하고 있습니다. 각 업체들은 연구개발에 많은 투자를 하고 있으며, 진화하는 전장의 요구를 충족시키기 위해 더 가볍고, 더 정확하고, 더 많은 기능을 갖춘 무기를 혁신하고 있습니다.

군 기관과의 전략적 파트너십 및 협력 관계는 주요 계약을 확보하고 특정 국방 요구 사항에 맞게 제품을 조정하는 데 도움이 됩니다. 또한 각 업체들은 타겟 마케팅과 지역 거점을 통해 세계 입지를 확장하고 고객 지원 및 애프터 서비스를 강화하는 데 주력하고 있습니다. 또한 많은 기업이 정밀 유도 및 연결 기능과 같은 첨단 기술을 통합하여 작전 효율성을 높이는 것을 우선순위에 두고 현대전 솔루션의 선두주자로 자리매김하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 공급업체의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 트럼프 정권 관세에 대한 영향

- 무역에 대한 영향

- 무역량 혼란

- 보복 조치

- 업계에 대한 영향

- 공급측 영향

- 주요 부품의 가격 변동

- 공급망 재구축

- 생산비용에 대한 영향

- 수요측 영향(판매 가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자 반응 패턴

- 공급측 영향

- 영향을 받는 주요 기업

- 전략적 업계 대응

- 공급망 재구성

- 가격결정과 제품 전략

- 정책 관여

- 전망과 향후 검토 사항

- 무역에 대한 영향

- 업계에 대한 영향요인

- 촉진요인

- 지정학적 긴장과 국경 분쟁의 증가

- 군 현대화 프로그램의 강화

- 휴대용 경량 무기의 수요 증가

- 비대칭전과 시가전 시나리오의 급증

- 유도·조준 시스템에서의 기술적 진보

- 업계의 잠재적 리스크 & 과제

- 첨단 시스템의 높은 수명주기와 정비 비용

- 엄격한 수출 관리와 규제 장벽

- 시장 기회

- 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter의 산업 분석

- PESTEL 분석

- 테크놀러지와 혁신의 상황

- 현재 기술 동향

- 첨단 타겟팅 시스템의 통합

- 우수한 휴대성과 경량 소재

- 개량된 탄두와 추진 능력

- 신규 기술

- AI 대응 사격 관제 시스템

- 네트워크 중심 전쟁 통합

- 지향성 에너지 및 전자 발사 시스템

- 현재 기술 동향

- 새로운 비즈니스 모델

- 컴플라이언스 요건

- 국방 예산 분석

- 세계의 방위비의 동향

- 지역 방위 예산배분

- 북미

- 유럽

- 아시아태평양

- 중동 및 아프리카

- 라틴아메리카

- 주요 방위 현대화 프로그램

- 예산 예측(2025-2034)

- 업계의 성장에 대한 영향

- 국가별 방위 예산

- 분야별 방위 예산배분

- 인사

- 운영과 유지보수

- 조달

- 조사, 개발, 시험, 평가

- 인프라와 건설

- 테크놀러지와 혁신

- 지속가능성 구상

- 공급망 레질리언스

- 지정학적 분석

- 인재 분석

- 디지털 변혁

- 합병, 인수, 전략적 제휴의 상황

- 리스크 평가와 관리

- 주요 계약 패스닝(2021-2024)

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 시장 집중 분석

- 지역별

- 주요 기업의 경쟁 벤치마킹

- 재무 실적의 비교

- 매출

- 이익률

- 연구개발

- 제품 포트폴리오의 비교

- 제품 라인 업 넓이

- 테크놀러지

- 혁신

- 지역적 프레즌스의 비교

- 세계 발자국 분석

- 서비스 네트워크의 범위

- 지역별 시장 침투율

- 경쟁 포지셔닝 매트릭스

- 리더

- 챌린저

- 팔로워

- 니치 플레이어

- 전략적 전망 매트릭스

- 재무 실적의 비교

- 주요 발전, 2021-2024

- 합병과 인수

- 파트너십과 협업

- 기술적 진보

- 확대와 투자전략

- 지속가능성 구상

- 디지털 변혁 구상

- 신규 기업/스타트업 기업의 경쟁 구도

제5장 시장 추산·예측 : 기술별, 2021 – 2034

- 주요 동향

- 가이드 첨부

- 가이드 없음

제6장 시장 추산·예측 : 범위별, 2021 – 2034

- 주요 동향

- 단거리(최대 1km)

- 중거리(1-2.5km)

- 장거리(2.5km 이상)

제7장 시장 추산·예측 : 용도별, 2021 – 2034

- 주요 동향

- 방위

- 대공포

- 대전차포

- 기타

- 국토안보부

제8장 시장 추산·예측 : 지역별, 2021 – 2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

제9장 기업 개요

- Daycraft Systems

- Dynamit Nobel Defence GmbH

- Lockheed Martin Corporation

- MBDA

- Nammo AS

- RAFAEL Advanced Defense Systems Ltd.

- Rheinmetall AG

- RTX

- Saab AB

The Global Shoulder Fired Weapons Market was valued at USD 7.2 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 12.2 billion by 2034. This growth is primarily driven by intensified military modernization programs worldwide. Rising geopolitical tensions and ongoing border disputes are significantly fueling demand for shoulder-fired weapons, as armed forces seek affordable, deployable force multipliers. Conflicts and standoffs in various regions have heightened the need for portable, precise anti-armor and anti-air systems. Additionally, military modernization efforts focus on developing next-generation lightweight weapons that enhance mobility and effectiveness in urban and asymmetric warfare scenarios. These programs prioritize upgrades like improved targeting and reduced launch weight, which propel demand for advanced shoulder-fired missiles.

Strategic defense initiatives worldwide are channeling significant resources into the research and development of man-portable weapon systems, accelerating innovation, and expanding capabilities. This investment focuses on creating more advanced, lightweight, and versatile shoulder-fired weapons that meet the demands of modern combat scenarios. Enhanced precision, improved targeting technologies, and greater portability are key priorities driving these efforts. As militaries seek to upgrade their arsenals with cutting-edge systems capable of adapting to diverse operational environments, funding for R&D continues to rise, fueling market expansion and fostering breakthroughs that set new standards in soldier effectiveness and battlefield agility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.2 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 5.5% |

The guided weapons segment led the market in 2024, valued at USD 5.1 billion. The integration of guided shoulder-fired weapons into comprehensive defense networks, such as advanced command and control systems, has elevated their strategic importance. These weapons deliver precision, flexibility, and real-time target adjustment capabilities, making them indispensable on modern battlefields. This integration enhances operational effectiveness and stimulates demand for sophisticated guided systems, driving market growth.

The defense segment generated USD 6.3 billion in 2024. The increasing need for lightweight, easily deployable weaponry to enhance soldier agility and combat effectiveness is pushing shoulder-fired weapons to the forefront. These systems are increasingly vital in anti-armor and anti-air roles and are central to defense modernization programs aiming to replace outdated weaponry with versatile, accurate solutions. Their adaptability across conventional and irregular warfare ensures a solid position within various military branches.

United States Shoulder Fired Weapons Market was valued at USD 2.2 billion in 2024. Growth here is fueled largely by ongoing procurements of advanced portable systems by the Department of Defense. Programs focused on enhancing soldier lethality, mobility, and capabilities in urban combat are driving continuous upgrades in shoulder-fired anti-armor and anti-structure weaponry. Heightened attention to urban warfare readiness and deployment further sustains demand.

Key players in the Shoulder Fired Weapons Market include Lockheed Martin Corporation, RTX, Saab AB, and MBDA. Companies in the shoulder-fired weapons market are adopting multiple strategies to solidify their market presence. They invest heavily in research and development to innovate lighter, more accurate, and multifunctional weapons that meet evolving battlefield needs.

Strategic partnerships and collaborations with military agencies help them secure key contracts and tailor products to specific defense requirements. Firms also focus on expanding their global footprint through targeted marketing and regional offices, enhancing customer support and after-sales services. Moreover, many players prioritize integrating cutting-edge technologies such as precision guidance and connectivity features to improve operational effectiveness, positioning themselves as leaders in modern warfare solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Technology

- 2.2.2 Range

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Trump Administration Tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising geopolitical tensions and border conflicts

- 3.3.1.2 Increased military modernization programs

- 3.3.1.3 Growing demand for portable and lightweight weaponry

- 3.3.1.4 Surge in asymmetric and urban warfare scenarios

- 3.3.1.5 Technological advancements in guidance and targeting systems

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High lifecycle and maintenance costs of advanced systems

- 3.3.2.2 Stringent export controls and regulatory barriers

- 3.3.3 Market opportunities

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.1.1 Integration of advanced targeting systems

- 3.8.1.2 Enhanced portability and lightweight materials

- 3.8.1.3 Improved warhead and propulsion capabilities

- 3.8.2 Emerging technologies

- 3.8.2.1 AI-enabled fire control systems

- 3.8.2.2 Network-centric warfare integration

- 3.8.2.3 Directed energy and electromagnetic launch systems

- 3.8.1 Current technological trends

- 3.9 Emerging business models

- 3.10 Compliance requirements

- 3.11 Defense budget analysis

- 3.12 Global defense spending trends

- 3.13 Regional defense budget allocation

- 3.13.1 North America

- 3.13.2 Europe

- 3.13.3 Asia Pacific

- 3.13.4 Middle East and Africa

- 3.13.5 Latin America

- 3.14 Key defense modernization programs

- 3.15 Budget forecast (2025-2034)

- 3.15.1 Impact on industry growth

- 3.15.2 Defense budgets by country

- 3.15.3 Defense budget allocation by segment

- 3.15.3.1 Personnel

- 3.15.3.2 Operations and maintenance

- 3.15.3.3 Procurement

- 3.15.3.4 Research, development, test and evaluation

- 3.15.3.5 Infrastructure and construction

- 3.15.3.6 Technology and innovation

- 3.16 Sustainability initiatives

- 3.17 Supply chain resilience

- 3.18 Geopolitical analysis

- 3.19 Workforce analysis

- 3.20 Digital transformation

- 3.21 Mergers, acquisitions, and strategic partnerships landscape

- 3.22 Risk assessment and management

- 3.23 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Guided

- 5.3 Unguided

Chapter 6 Market Estimates and Forecast, By Range, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Short range (up to 1 km)

- 6.3 Medium range (1–2.5 km)

- 6.4 Long range (above 2.5 km)

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Defense

- 7.2.1 Anti-aircraft

- 7.2.2 Anti-tank

- 7.2.3 Others

- 7.3 Homeland Security

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Daycraft Systems

- 9.2 Dynamit Nobel Defence GmbH

- 9.3 Lockheed Martin Corporation

- 9.4 MBDA

- 9.5 Nammo AS

- 9.6 RAFAEL Advanced Defense Systems Ltd.

- 9.7 Rheinmetall AG

- 9.8 RTX

- 9.9 Saab AB